Fixed income analysts play a crucial role in evaluating debt instruments and advising on investment strategies, offering stability and potential income. At income-partners.net, we illuminate the path to understanding fixed income analysis and how it can significantly benefit your financial portfolio, providing solutions for those seeking stable income streams. Let’s delve into the world of bonds, credit risk, and yield curves to uncover the analyst’s role in the fixed income market.

1. What is Fixed Income Research?

Fixed Income Research Definition: Fixed income research involves analyzing debt instruments to make investment recommendations. These recommendations are based on a deep understanding of credit risk, interest rates, and macroeconomic factors. Think of it as the detective work of the financial world, where analysts piece together clues to determine the value and risk associated with bonds and other debt securities.

The challenging part is understanding that fixed income research exists in various forms across different types of firms. You’ll find it at banks (in “sell-side roles”), buy-side firms like asset managers and hedge funds, and even credit rating agencies. Each setting brings a unique perspective and focus to the research process.

Fixed income research can be quantitative, fundamental, or a combination of both. Different teams specialize in various instruments, such as investment-grade, high-yield, distressed, structured, sovereign, and emerging markets. This article will focus primarily on fundamental research at banks, particularly for investment-grade and high-yield bonds.

All the leading investment banks and multi-manager hedge funds engage in fixed income research, as do top asset managers and credit firms like PIMCO, Brookfield (Oaktree), Fidelity, BlackRock, Wellington, Blackstone (GSO), Octagon, and Ares. Even credit rating agencies such as S&P, Fitch, Moody’s, and Morningstar DBRS specialize in fixed income research.

While each role shares common analytical elements, the specifics and deliverables differ. For example, a credit rating agency might produce a credit rating, while a bank’s research team provides investment recommendations to clients.

Fixed Income Analyst Research

Fixed Income Analyst Research

2. Equity Research vs. Fixed Income Research

The primary difference between equity research and fixed income research is the focus. In fixed income, analysts concentrate on the downside case rather than growth. According to research from the University of Texas at Austin’s McCombs School of Business, risk analysis provides a clearer financial strategy.

Key questions that fixed income analysts consider include:

- What is the likelihood that the company will violate one of its covenants?

- Could the company default on any of its debt issuances?

- What would happen if there were a recession or a slowdown in global trade?

- If the company liquidates, which lenders will be repaid, and in what order?

While the fixed income market is larger than the equities market in terms of market value and trading volume, this does not necessarily mean there are more job opportunities. Liquidity is often more limited, and more trading occurs over the counter (OTC) rather than electronically. Staff turnover is also typically lower, as senior staff tend to remain in their roles for longer periods.

3. What are Some Common Myths About Fixed Income Research?

Some people believe that fixed income research is more macro-focused or quantitative than equity research, resembling the work done at a quant fund. However, these claims only apply to certain areas within fixed income.

For example, if you focus on investment-grade bonds, macro factors become more critical because investment-grade companies rarely default. Movements in interest rates drive bond prices more than company-specific factors.

Similarly, a “quant credit” group might use statistical analysis to analyze bonds rather than traditional 3-statement and cash flow modeling. However, many fundamental roles in FI research still involve financial statements, debt analysis, and company-specific factors.

4. What Do You Do as a Fixed Income Research Analyst or Associate?

In fixed income research, “Analyst” is generally the senior role, while “Associate” is the entry-level position. However, there are often different levels within these titles, such as VP-level and MD-level Analysts. The work tasks are similar to those in equity research but with a focus on credit and debt.

Tasks include:

- Being assigned 1-2 industries and covering a specific set of companies, creating and updating 3-statement models with support for credit features for each company.

- Splitting time between analyzing new bond issuances and existing ones, similar to “initiating coverage” vs. “existing coverage” in equity research.

- Covering quarterly earnings and sending updated models and notes to clients and other teams.

The main differences between fixed income research and equity research are:

- Financial models focus on downside scenarios and analyze each issuance separately, considering Yield to Worst, Yield to Maturity, Recovery percentages, and default risk.

- The output focuses on credit stats and ratios (Debt / EBITDA, EBITDA / Interest, etc.), the appropriate debt vs. equity mix, and additional capital needs over the next few quarters.

- You may have to cover dozens of issuances, limiting the time you can spend on a single company or bond.

- The legal side is vital because you must read debt agreements to understand each issuance’s covenants and other terms.

- Quarterly earnings calls and management interaction are less critical because covering 50+ companies makes it impractical to participate in all calls. Events outside of earnings calls can often be more significant for bond prices.

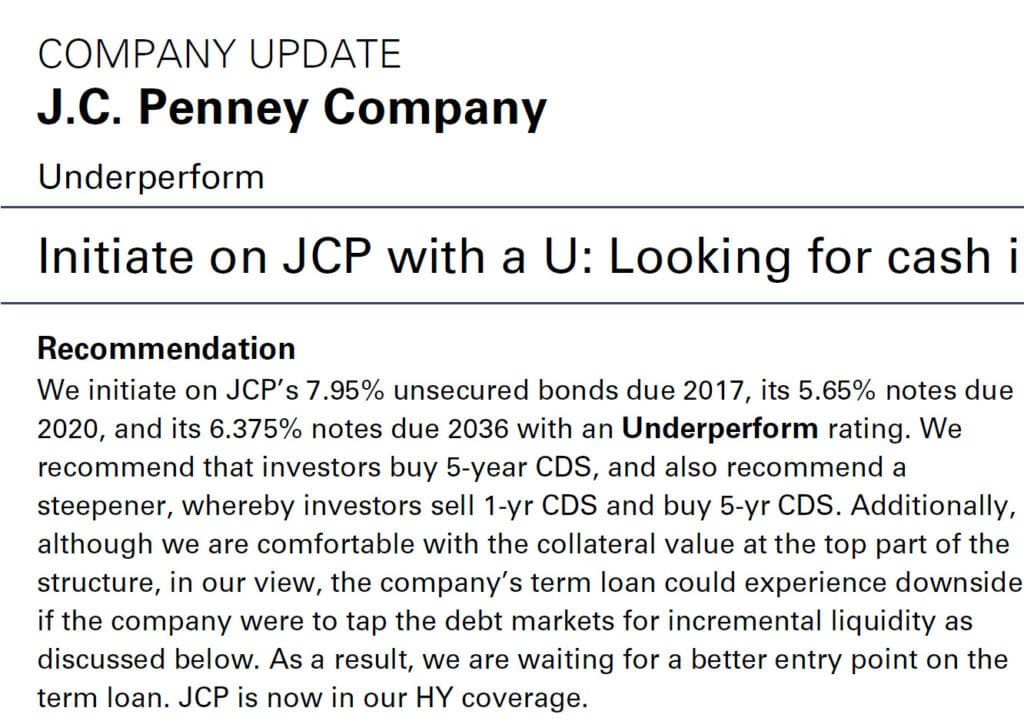

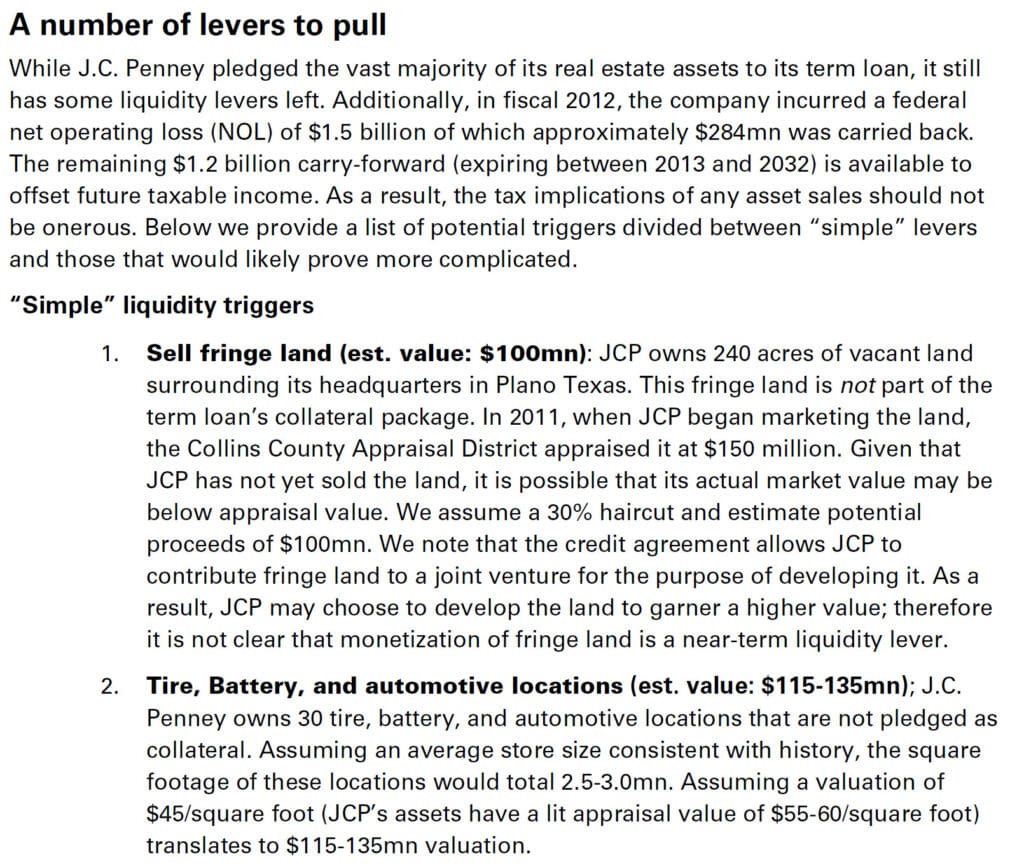

Fixed Income Analyst Report Example

Fixed Income Analyst Report Example

5. What Does a Sample Fixed Income Research Report Look Like?

While you can find fixed income reports on sites like Moody’s, Fitch, and S&P, these reports generally focus on the credit rating process.

A fixed income research report will have an “investment recommendation” that is quite different from that of equity research, with scenarios based on the company’s prospects, such as liquidation vs. going concern vs. debtor-in-possession financing. It will also discuss liquidity triggers rather than traditional catalysts, as analysts are concerned with how events will affect the company’s ability to repay or refinance its debt.

6. How Do You Get Recruited into Fixed Income Research?

As with equity research and hedge fund roles, there are two main ways to break into fixed income research:

- Complete the CFA, obtain fixed income-related internships, and start working directly in FI research at a bank or buy-side firm.

- Gain experience in another area of finance first, such as corporate banking, capital markets, or a credit rating agency (any role with the “Credit Analyst” title works). Fixed income traders sometimes also make the transition, depending on their desk and role.

The hiring process is often random and unstructured, without real “cycles” like those in IB and PE recruiting. Some of the largest asset managers, such as BlackRock and Fidelity, offer internships and entry-level roles in fixed income research, but these are highly competitive.

Banks do not seem to offer many internships in this field. If your goal is a bulge bracket bank, you may need to work in other credit roles first and network your way in.

7. What Kind of Fixed Income Interview Questions and Case Studies Should I Expect?

To prepare for interviews, review the content on corporate banking, credit hedge funds, and distressed debt hedge funds, as the topics are similar.

Here are some sample questions:

- Markets: What is the current 10-year U.S. Treasury yield? What about gilts (U.K.), bunds (Germany), or Japanese government bonds (JGBs)?

- Bond Prices and Yields: What is the difference between Yield to Maturity, Yield to Call, and Yield to Worst, and how do you use them in practice? What factors might cause a bond’s price to change?

- Bond Math: How can you approximate the Yield to Maturity? What about duration and convexity? What does duration mean intuitively?

- Rates: Is the “risk-free rate” truly risk-free? If so, how could you still lose money by investing in a 10-year government bond in a “safe” country?

- Rate Changes: If interest rates are expected to rise over the next year, how would you structure your portfolio? Would investment-grade or high-yield bonds be more affected?

- Bond Types: How do corporate bonds differ from government bonds? How would you analyze them differently?

If you receive a case study, the task is likely to read 2-3 pages about a company and its bond issuances and then provide an investment recommendation on a specific issuance.

For high-yield or distressed bonds, they may also ask for a specific price target or a recommendation involving credit default swaps (CDS).

Since the default probability is very low for investment-grade bonds, much of the decision-making comes down to macro factors, relative value, and portfolio “fit.”

For example, a company might have a 5% bond due in 10 years and a 6% bond due in 1 year. Even though neither is likely to default, the 6% bond is not necessarily the better investment because:

- If you believe interest rates will drop substantially, you could earn a higher yield by buying the 5% bond, waiting for the rate drop, and selling it before maturity, as it’s more sensitive to interest rates.

- The 1-year maturity for the 6% bond is quite short and may not match your overall portfolio’s duration target.

You must also compare these issuances with those of similar companies. Is 5% or 6% a good deal? Can you find lower or higher yields in the market?

The most common mistake in these case studies is failing to pick a specific issuance to invest in, especially if the company has a wide range of bonds with different maturities.

8. What Are Fixed Income Research Salaries and Bonuses?

Salary and bonus data can be hard to come by, but for sell-side roles, expect a lower compensation compared to equity research. If ER Associates start with total compensation between $150,000 and $200,000, FI Associates might start in the $100,000 to $150,000 range. While some MD-level “Analysts” in equity research can earn $1 million+ from their base salary and bonus, the pay ceiling is generally lower in fixed income roles. Expect something more in the “mid-six-figures” range, although there are exceptions for top-performing groups and Analysts.

In buy-side fixed income research roles, Analysts can earn $300,000+ depending on the firm and their seniority, and the portfolio managers above them can earn significantly more, again depending on the firm type and performance.

9. What Are the Hours and Lifestyle Like in Fixed Income?

The hours in fixed income research are generally better than in equity research because you don’t need to follow earnings calls closely or issue new reports constantly. Because you cover so many more names, it’s more about forming an overall view of the market and your coverage universe.

Expect to work a more “normal” workweek, such as 50-55 hours, with spikes during significant events. At buy-side firms such as asset managers, many fixed income research professionals work 40-50 hours per week and experience relatively low stress levels.

10. What Are Potential Fixed Income Research Exit Opportunities?

Most research professionals aspire to work at hedge funds.

Hedge fund roles are more feasible if you focus on high-yield or distressed issuances because few HFs invest in investment-grade bonds, and the required skill sets differ. However, you’ll also compete with bankers from Leveraged Finance and Restructuring groups, making hedge funds not necessarily a “sure thing.”

Traders have a significant advantage when recruiting for global macro hedge funds, but you don’t have the same advantage when applying to credit-focused HFs.

Moving into equity research or investment banking is also possible, especially if you focus on groups where credit is essential (e.g., power & utilities, FIG, or industrials).

Distressed private equity is theoretically possible if you find a firm that operates more like a hedge fund, but it’s not especially likely.

The most likely outcome is that you’ll continue working in credit-related research roles at a bank or an asset manager.

Exits into traditional private equity, corporate development, and venture capital are unlikely due to the need for deal experience.

11. Is Fixed Income Research Worth It?

Here’s a summary of the pros and cons to help you decide if fixed income research is right for you:

Pros:

- The work can be more interesting than equity research, particularly if you cover high-yield or distressed issuances.

- It can be a good “second step” after a role like corporate banking, capital markets, or a credit rating agency if you want to improve your profile for buy-side roles.

- It can be very comfortable at the top, with senior-level staff earning in the mid-six-figures (or higher) with less stress than IB/PE-style jobs.

- You can transition to numerous other credit-related roles.

Cons:

- There is little turnover, meaning that recruiting has a high “luck” component.

- Exit opportunities exist but are narrower than IB/PE exits because you do not work on deals.

- The work can be repetitive, especially if you focus on investment-grade issuances.

- Compensation is often lower than in equity research and “equities in general,” although there is significant variance depending on the firm/fund type, performance, etc.

While fixed income research is often overlooked, it can be a rewarding career path. If you decide to pursue it, be prepared to stay in the field for a long time as you work your way up.

12. What are the Key Skills Required for a Fixed Income Analyst?

To excel as a fixed income analyst, you need a blend of technical and soft skills. According to Harvard Business Review, successful analysts are adaptable learners and problem-solvers. Essential skills include:

- Financial Modeling: Proficiency in building and interpreting financial models, particularly those focused on credit analysis and debt valuation.

- Credit Analysis: Understanding credit risk assessment, including evaluating financial ratios, debt covenants, and macroeconomic factors that can impact a company’s ability to repay its debt.

- Debt Agreement Interpretation: Ability to read and interpret complex legal documents like debt agreements to understand the terms and conditions of bond issuances.

- Macroeconomic Analysis: Knowledge of macroeconomic indicators and their impact on interest rates, inflation, and overall economic growth, which can affect bond prices.

- Communication Skills: Ability to communicate complex financial information clearly and concisely, both in writing and verbally, to clients and colleagues.

13. How Can Fixed Income Analysis Benefit Investors?

Fixed income analysis offers several benefits to investors, especially those looking for stability and income. Benefits include:

- Risk Management: Understanding the creditworthiness of bond issuers helps investors manage risk by avoiding potential defaults.

- Portfolio Diversification: Fixed income assets can provide diversification to an investment portfolio, reducing overall volatility.

- Income Generation: Bonds and other fixed income instruments can provide a steady stream of income through interest payments.

- Capital Preservation: In times of economic uncertainty, fixed income assets can act as a safe haven, preserving capital.

14. What are the Different Types of Bonds Analyzed by Fixed Income Analysts?

Fixed income analysts analyze a variety of bonds, each with its own characteristics and risk profile. Types of bonds analyzed include:

| Bond Type | Description |

|---|---|

| Government Bonds | Issued by national governments to fund public spending; generally considered low-risk, especially those issued by stable, developed countries. |

| Corporate Bonds | Issued by companies to fund operations or expansion; riskier than government bonds, with higher yields to compensate for the increased risk. |

| Municipal Bonds | Issued by state and local governments to finance public projects; often tax-exempt, making them attractive to investors. |

| High-Yield Bonds | Bonds with lower credit ratings (below investment grade); also known as junk bonds, offering higher yields to compensate for higher risk. |

| Investment-Grade Bonds | Bonds with higher credit ratings, indicating a lower risk of default; offer lower yields than high-yield bonds. |

15. What Role Does Technology Play in Fixed Income Analysis?

Technology has transformed fixed income analysis, enhancing efficiency and accuracy. Financial technology tools used include:

- Data Analytics Platforms: These platforms allow analysts to access and analyze large datasets quickly, identifying trends and patterns that would be difficult to spot manually.

- Financial Modeling Software: Software like Bloomberg Terminal and FactSet provide tools for building complex financial models, performing scenario analysis, and valuing debt instruments.

- Automated Trading Systems: These systems use algorithms to execute trades based on pre-defined criteria, improving efficiency and reducing transaction costs.

- AI and Machine Learning: AI and machine learning are increasingly used to predict credit risk, forecast interest rates, and identify investment opportunities in the fixed income market.

16. How Do Interest Rate Changes Affect Fixed Income Investments?

Interest rate changes have a significant impact on fixed income investments. According to economic principles, when interest rates rise, bond prices generally fall, and vice versa. This is because as interest rates increase, newly issued bonds offer higher yields, making existing bonds with lower yields less attractive.

Fixed income analysts closely monitor interest rate trends and use tools like duration and convexity to measure the sensitivity of bond prices to interest rate changes. They also analyze the yield curve, which plots the yields of bonds with different maturities, to forecast future interest rate movements and their potential impact on fixed income portfolios.

17. How Does Credit Rating Impact Fixed Income Analysis?

Credit rating is a critical factor in fixed income analysis. Credit rating agencies like S&P, Moody’s, and Fitch assess the creditworthiness of bond issuers, providing ratings that indicate the likelihood of default. Bonds with higher credit ratings are considered safer investments, while those with lower ratings are riskier.

Fixed income analysts use credit ratings as a starting point for their analysis, but they also conduct their own independent research to assess credit risk. They evaluate the issuer’s financial health, industry trends, and macroeconomic factors that could affect its ability to repay its debt.

18. How Does the Economy Affect the Role of a Fixed Income Analyst?

The economy plays a vital role in shaping the responsibilities and focus areas of a fixed income analyst. In periods of economic expansion, analysts may concentrate on identifying high-growth opportunities and assessing the potential for increased corporate borrowing. Conversely, during economic downturns, their focus shifts to risk management, assessing credit quality, and identifying safe-haven assets.

Economic indicators like GDP growth, inflation rates, and employment figures provide valuable insights for fixed income analysts. These indicators help them understand the overall health of the economy and forecast future trends, which can impact bond prices and yields.

19. How Can Income-Partners.net Help You Connect with Fixed Income Opportunities?

At income-partners.net, we understand the complexities of fixed income investing and the importance of finding the right opportunities. We offer a range of resources to help you connect with potential partners and investment opportunities in the fixed income market.

By joining our network, you can access:

- A diverse range of fixed income investment opportunities, including bonds, notes, and other debt instruments.

- A network of experienced fixed income analysts and portfolio managers who can provide valuable insights and guidance.

- Educational resources to help you better understand the intricacies of fixed income investing.

20. What are Some Current Trends in Fixed Income Analysis?

Several trends are shaping the future of fixed income analysis:

- ESG Investing: Environmental, social, and governance (ESG) factors are becoming increasingly important in fixed income analysis, with investors seeking bonds issued by companies with strong ESG credentials.

- Sustainable Investing: Focus on bonds that finance projects with positive environmental or social impacts, gaining traction among investors.

- Big Data and Analytics: The use of big data and advanced analytics techniques is transforming fixed income analysis, enabling analysts to process vast amounts of data and identify patterns and trends.

- Alternative Data Sources: Analysts are increasingly using alternative data sources, such as social media sentiment and satellite imagery, to gain insights into companies and industries.

FAQ: Fixed Income Analysts

- What is the primary goal of a fixed income analyst?

- The main goal is to evaluate the creditworthiness and risk associated with debt instruments and provide investment recommendations.

- What types of companies employ fixed income analysts?

- Fixed income analysts are employed by banks, asset management firms, hedge funds, and credit rating agencies.

- How does fixed income research differ from equity research?

- Fixed income research focuses on downside risk and debt analysis, while equity research focuses on growth potential.

- What are the key skills needed to become a fixed income analyst?

- Key skills include financial modeling, credit analysis, debt agreement interpretation, and macroeconomic analysis.

- What is the typical career path for a fixed income analyst?

- The career path often starts with an entry-level associate position, progressing to analyst, portfolio manager, or hedge fund manager.

- How do interest rate changes affect fixed income investments?

- Rising interest rates typically cause bond prices to fall, while falling interest rates cause bond prices to rise.

- What role does credit rating play in fixed income analysis?

- Credit ratings provide an initial assessment of credit risk, helping analysts and investors evaluate the likelihood of default.

- How does the economy affect the role of a fixed income analyst?

- The state of the economy influences the focus of fixed income analysts, shifting from growth opportunities during expansions to risk management during downturns.

- What are some current trends in fixed income analysis?

- Current trends include ESG investing, the use of big data and analytics, and the incorporation of alternative data sources.

- How can income-partners.net help you connect with fixed income opportunities?

- income-partners.net provides a network of experienced professionals, investment opportunities, and educational resources for fixed income investors.

Ready to explore the world of fixed income investing? Visit income-partners.net today to discover new opportunities, connect with potential partners, and take your investment strategy to the next level. Contact us at 1 University Station, Austin, TX 78712, United States, or call +1 (512) 471-3434 to learn more. Let income-partners.net be your guide to unlocking the potential of fixed income investments. Join us and start building profitable partnerships today.