Does Farm Income Affect Social Security? Absolutely, farm income affects Social Security benefits. It’s vital to understand how your earnings impact your retirement funds. This article from income-partners.net explores the complexities of farm income and its effects on Social Security, guiding you towards strategic financial planning and partnership opportunities. Navigate the nuances of farm income, retirement planning, and strategic financial partnerships to secure your future with confidence. Explore partnership opportunities, retirement planning, and farm finances.

1. How Does Farming Impact Social Security Benefits?

Yes, farming can impact Social Security benefits. Your Social Security benefits can indeed be affected by farm income. As a farmer, your earnings from farming directly influence both your eligibility for and the amount of Social Security benefits you can receive. Understanding this connection is essential for effective retirement planning.

The Social Security Administration (SSA) looks at your work history and earnings to determine your benefits. When you’re self-employed, as many farmers are, you pay self-employment taxes, which go toward Social Security and Medicare. The amount of these taxes you pay is based on your net earnings from self-employment, meaning your profits after deducting business expenses.

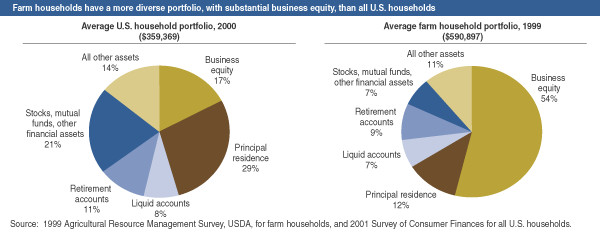

According to the USDA’s Economic Research Service, farm households often have diverse income streams, including off-farm employment, investments, and government payments. This diversity can influence how Social Security benefits are calculated. For example, if you have significant off-farm income, it could increase your overall earnings, potentially affecting your Social Security contributions and future benefits.

However, it’s important to note that if your farm income is low or if you experience losses, it could reduce your self-employment tax liability and potentially impact your future Social Security benefits. Therefore, careful financial planning and strategic partnerships, as explored on income-partners.net, are crucial for optimizing your income and retirement savings.

The interplay between farm income and Social Security is complex, but understanding the basics can help you make informed decisions about your financial future. Let’s delve deeper into the specifics of how farm income is assessed and how it influences your Social Security benefits.

2. What Types Of Farm Income Are Considered By Social Security?

Social Security considers various types of farm income. The Social Security Administration considers multiple types of farm income when determining your eligibility and benefit amount. Understanding which types of income are included is crucial for accurate financial planning.

The primary type of farm income considered by Social Security is your net earnings from self-employment. This includes profits from operating your farm, such as selling crops, livestock, and other agricultural products. It also encompasses income from renting out farmland, if you actively participate in the management or operation of the farm.

According to the Social Security Administration, net earnings from self-employment are calculated by subtracting your business expenses from your gross income. These expenses can include costs related to farming, such as seeds, fertilizer, equipment, labor, and other operating costs. The resulting net earnings are then subject to self-employment taxes, which contribute to your Social Security and Medicare coverage.

Additionally, Social Security may consider other forms of farm income, such as payments from government programs like the USDA’s Farm Service Agency (FSA). These payments can include subsidies, disaster assistance, and conservation incentives, which can impact your overall income and self-employment tax liability.

However, not all farm-related income is considered by Social Security. For example, if you passively rent out farmland without actively participating in its management, the rental income may not be subject to self-employment taxes. Similarly, capital gains from the sale of farm assets, such as land or equipment, may be treated differently than ordinary farm income.

Therefore, it’s essential to keep accurate records of all your farm income and expenses to determine your net earnings from self-employment accurately. Consulting with a tax advisor or financial planner can help you navigate the complexities of farm income and Social Security to optimize your retirement planning strategy. By understanding which types of farm income are considered by Social Security, you can make informed decisions about your business operations and financial future.

3. How Does Net Farm Income Affect Social Security Taxes?

Net farm income directly impacts Social Security taxes. Your net farm income directly influences the amount of Social Security taxes you owe. Understanding this relationship is vital for budgeting and financial planning.

Net farm income, which is your gross farm income minus deductible farm expenses, determines your self-employment tax liability. As a self-employed farmer, you’re responsible for paying both the employer and employee portions of Social Security and Medicare taxes, collectively known as self-employment taxes.

According to the Social Security Administration, the self-employment tax rate is 15.3%, consisting of 12.4% for Social Security (up to a certain earnings limit) and 2.9% for Medicare. This tax is applied to 92.35% of your net earnings from self-employment.

For example, if your net farm income is $50,000, you would multiply that amount by 0.9235 to arrive at your taxable base ($46,175). Then, you would multiply your taxable base by 0.153 to determine your self-employment tax liability ($7,065.70).

However, there are certain rules and considerations that can affect your self-employment tax liability. For instance, if your net earnings from self-employment are less than $400, you generally don’t have to pay self-employment taxes. Additionally, if you have both self-employment income and wages from employment, the amount of wages you earn can affect the amount of self-employment tax you owe.

Furthermore, you can deduct one-half of your self-employment taxes from your gross income when calculating your adjusted gross income (AGI) for income tax purposes. This deduction can help reduce your overall tax liability and potentially lower your taxable income.

Strategic partnerships and financial planning, such as those explored on income-partners.net, can help you optimize your net farm income and minimize your self-employment tax liability. By carefully managing your farm expenses, maximizing your income, and taking advantage of available deductions, you can reduce the impact of Social Security taxes on your overall financial situation.

4. Can Farm Losses Reduce My Social Security Taxes?

Yes, farm losses can reduce Social Security taxes. Farm losses can indeed reduce your Social Security taxes. When your farm expenses exceed your income, resulting in a net loss, this can lower your self-employment tax liability.

When you experience a net loss from your farming activities, you may be able to deduct that loss from other sources of income, such as wages or investment income, to reduce your overall taxable income. This can lower the amount of self-employment taxes you owe, as well as your income tax liability.

However, there are limitations and rules regarding the deductibility of farm losses. According to the IRS, you can generally deduct farm losses up to the amount of your other income. However, if your losses exceed your other income, you may be subject to certain limitations, such as the passive activity loss rules or the hobby loss rules.

The passive activity loss rules may apply if you’re not actively involved in the management or operation of your farm. In this case, your deductible losses may be limited to the amount of your passive income. The hobby loss rules may apply if your farming activities are not engaged in for profit. In this case, your deductible losses may be limited to the amount of your gross income from the activity.

Additionally, there are specific rules regarding the carryover of farm losses to future years. If you’re unable to deduct all of your farm losses in the current year, you may be able to carry them forward to future years and deduct them from your income in those years.

Strategic financial planning and risk management, as discussed on income-partners.net, are crucial for managing farm losses effectively. By implementing sound business practices, diversifying your income streams, and exploring available government programs and assistance, you can mitigate the impact of farm losses on your overall financial situation and minimize your Social Security tax liability.

Farm operators consider the future of the farm when contemplating retirement from farming

Farm operators consider the future of the farm when contemplating retirement from farming

5. How Does Farm Income Affect Social Security Benefits After Retirement?

Farm income can affect Social Security benefits after retirement. Your farm income can affect your Social Security benefits even after you retire. Understanding how your post-retirement income interacts with your benefits is essential for financial stability.

If you continue to earn income from farming after you start receiving Social Security benefits, it could potentially reduce your benefits, depending on your age and income level. The Social Security Administration has an earnings test that applies to beneficiaries who are younger than the full retirement age (FRA).

According to the SSA, if you’re younger than the FRA, your Social Security benefits may be reduced if your earnings exceed a certain limit. In 2024, that limit is $22,320 per year. For every $2 you earn above this limit, your Social Security benefits will be reduced by $1.

However, in the year you reach your FRA, a different rule applies. In this case, the earnings limit is higher ($59,520 in 2024), and for every $3 you earn above this limit, your Social Security benefits will be reduced by $1. Once you reach your FRA, the earnings test no longer applies, and you can earn any amount of income without affecting your Social Security benefits.

It’s important to note that only earned income, such as wages and self-employment income, is subject to the earnings test. Unearned income, such as investment income, pensions, and annuities, does not affect your Social Security benefits.

Furthermore, there are certain exceptions to the earnings test for self-employed individuals, such as farmers. According to the SSA, if your farming activities are considered a business and you materially participate in the operation of the farm, your earnings may be subject to the earnings test. However, if your farming activities are considered a hobby or a passive investment, your earnings may not be subject to the earnings test.

Strategic retirement planning, as explored on income-partners.net, is crucial for managing your farm income and Social Security benefits effectively. By carefully considering your age, income level, and the nature of your farming activities, you can make informed decisions about when to start receiving Social Security benefits and how to minimize the impact of the earnings test on your overall retirement income.

6. What Is The Social Security Retirement Earnings Test For Farmers?

The Social Security retirement earnings test applies to farmers. The Social Security retirement earnings test does indeed apply to farmers. This test can impact your benefits if you continue to work and earn income while receiving Social Security.

The earnings test is a rule that reduces Social Security benefits for individuals who are receiving benefits but have not yet reached their full retirement age (FRA) and have earnings above a certain limit. As mentioned earlier, for those under the FRA, Social Security benefits are reduced by $1 for every $2 earned above $22,320 in 2024. In the year an individual reaches FRA, benefits are reduced by $1 for every $3 earned above $59,520.

For farmers, this means that if you are receiving Social Security benefits but are still actively involved in farming and earning income above these limits, your benefits could be reduced. The Social Security Administration considers income from farming as earned income if you materially participate in the operation of the farm. Material participation means you are actively involved in the management or physical work of the farm.

However, there are some nuances for farmers. For instance, rental income from farmland may not be considered earned income if you are not materially participating in the farming operation. In such cases, the rental income would not be subject to the earnings test. It’s also important to understand that after reaching your full retirement age, the earnings test no longer applies, and you can earn any amount of income without affecting your Social Security benefits.

Strategic financial planning and consulting with experts, as encouraged by income-partners.net, can help farmers navigate the complexities of the earnings test. By understanding the rules and planning accordingly, you can optimize your Social Security benefits while continuing to work in agriculture.

7. How Can Farmers Minimize The Impact Of The Social Security Earnings Test?

Farmers can minimize the impact of the Social Security earnings test through strategic planning. There are several strategies farmers can employ to minimize the impact of the Social Security earnings test. Careful planning can help you maximize your benefits while continuing to work.

One common strategy is to reduce your earned income below the threshold by decreasing your work hours or shifting income to later years. This could involve postponing the sale of crops or livestock until after you reach your full retirement age.

Another strategy is to restructure your farming operation to reduce your material participation. For example, you could transition some of your responsibilities to a younger family member or hire a farm manager. If you are not materially participating, the income may not be considered earned income for Social Security purposes.

You can also explore different business structures, such as forming a limited liability company (LLC) or a corporation, which may offer opportunities to shift income or reduce your personal earned income. However, these strategies can be complex and may have tax implications, so it’s important to seek professional advice.

Additionally, it’s essential to keep accurate records of your income and expenses and to consult with a tax advisor or financial planner to ensure you’re taking advantage of all available deductions and credits. Strategic partnerships and financial planning, as facilitated by income-partners.net, can provide valuable insights and guidance in minimizing the impact of the Social Security earnings test on your retirement income.

Farm households save and invest for retirement

Farm households save and invest for retirement

8. What Happens If I Work And Receive Social Security At The Same Time?

Working while receiving Social Security can affect your benefits. Working while receiving Social Security benefits can affect the amount of your benefits, depending on your age and earnings. The impact varies depending on whether you are below, at, or above your full retirement age (FRA).

If you are below your FRA and work, your Social Security benefits may be reduced if your earnings exceed a certain limit. In 2024, the earnings limit is $22,320. For every $2 you earn above this limit, your Social Security benefits will be reduced by $1. This is designed to adjust benefits based on current income, assuming those who earn more need less support.

In the year you reach your FRA, a different rule applies. The earnings limit is higher ($59,520 in 2024), and for every $3 you earn above this limit, your Social Security benefits will be reduced by $1. This adjustment is less stringent than for those below FRA.

Once you reach your FRA, the earnings test no longer applies. You can earn any amount of income without affecting your Social Security benefits. This is a significant advantage, as it allows you to supplement your retirement income without penalty.

It’s important to note that the Social Security Administration (SSA) only counts earned income (such as wages or self-employment income) towards the earnings test. Income from investments, pensions, or annuities does not count.

The SSA will recalculate your benefit amount when you reach your FRA to account for months in which benefits were reduced due to earnings. This often results in a higher monthly benefit for the remainder of your retirement.

Strategic retirement planning, as promoted by income-partners.net, involves understanding these rules and making informed decisions about when to start receiving Social Security benefits and how much to work. Consulting with financial advisors can help you optimize your benefits and plan for a secure retirement.

9. Are There Resources Available To Help Farmers Understand Social Security?

Yes, many resources are available to help farmers understand Social Security. Farmers can access a variety of resources to understand Social Security benefits and how farm income affects them. Here are some valuable resources:

- The Social Security Administration (SSA): The SSA’s website (ssa.gov) provides comprehensive information on Social Security programs, including retirement, disability, and survivor benefits. You can find detailed guides, fact sheets, and calculators to estimate your benefits.

- USDA Economic Research Service (ERS): The USDA ERS offers research and analysis on farm household income, wealth, and retirement. Their publications can help you understand the broader economic context of farming and retirement planning.

- Tax Professionals: Certified Public Accountants (CPAs) and tax advisors specializing in agriculture can provide personalized advice on how farm income affects your Social Security taxes and benefits.

- Financial Planners: Financial planners can help you create a comprehensive retirement plan that takes into account your farm income, Social Security benefits, and other sources of income and assets.

- Extension Services: Local extension offices often provide workshops and resources on farm management, financial planning, and retirement.

- Farm Bureau: Farm Bureau organizations offer resources and advocacy for farmers, including information on Social Security and retirement planning.

- Online Forums and Communities: Online forums and communities for farmers can provide a platform to ask questions, share experiences, and learn from others.

By utilizing these resources, farmers can gain a better understanding of Social Security and make informed decisions about their retirement planning.

10. How Does Income-Partners.Net Help Farmers With Financial Planning And Social Security?

Income-partners.net assists farmers with financial planning and Social Security. Income-partners.net offers a unique platform for farmers seeking to optimize their financial planning and understand the intricacies of Social Security. Here’s how:

- Strategic Partnership Opportunities: Income-partners.net connects farmers with strategic partners who can provide financial expertise, investment advice, and business development support.

- Educational Resources: The website offers articles, guides, and webinars on topics such as retirement planning, tax optimization, and Social Security benefits.

- Personalized Financial Planning: Income-partners.net can connect you with financial advisors who specialize in working with farmers. These advisors can help you create a customized retirement plan that takes into account your farm income, Social Security benefits, and other financial goals.

- Networking Opportunities: The platform facilitates networking among farmers, financial professionals, and other industry experts, allowing you to learn from others’ experiences and best practices.

- Up-to-Date Information: Income-partners.net stays current with the latest changes in Social Security laws, tax regulations, and financial planning strategies, ensuring you have access to accurate and timely information.

Through these services, income-partners.net empowers farmers to make informed decisions about their financial future and maximize their Social Security benefits.

Conclusion

Understanding how farm income affects Social Security is crucial for farmers planning their financial future. Navigating the complexities of net farm income, self-employment taxes, and the Social Security earnings test requires careful planning and strategic partnerships. By leveraging resources like income-partners.net, farmers can optimize their retirement income and secure their financial well-being. Don’t navigate the complexities of farm income and Social Security alone; visit income-partners.net today to explore partnership opportunities, access expert financial guidance, and take control of your financial future. Visit income-partners.net to connect with experts and resources to enhance your financial stability. Secure your future with our expert advice and partnership opportunities.

FAQ Section

Q1: Does owning a farm affect my Social Security benefits?

Yes, owning a farm affects your Social Security benefits because your net earnings from self-employment (farming) determine your self-employment tax liability, which contributes to your Social Security coverage.

Q2: Can I receive Social Security benefits while still farming?

Yes, you can receive Social Security benefits while still farming, but your benefits may be reduced if your earnings exceed certain limits before you reach your full retirement age.

Q3: How does the Social Security earnings test apply to farmers?

The Social Security earnings test applies to farmers if they are under their full retirement age and their earned income (net earnings from farming) exceeds the annual limit set by the Social Security Administration.

Q4: What is considered earned income for farmers under Social Security?

Earned income for farmers includes net earnings from self-employment, such as profits from selling crops, livestock, and other agricultural products, as well as income from actively participating in managing or operating the farm.

Q5: Can farm losses reduce my Social Security benefits?

Farm losses can reduce your self-employment tax liability, potentially impacting your future Social Security benefits by lowering your overall contributions.

Q6: What resources are available for farmers to understand Social Security?

Farmers can access resources from the Social Security Administration (SSA), USDA Economic Research Service (ERS), tax professionals, financial planners, extension services, and farm bureau organizations to understand Social Security.

Q7: How does income-partners.net assist farmers with financial planning and Social Security?

Income-partners.net helps farmers by providing strategic partnership opportunities, educational resources, personalized financial planning services, networking opportunities, and up-to-date information on Social Security laws and financial strategies.

Q8: What happens to my Social Security benefits if I exceed the earnings limit while farming?

If you exceed the earnings limit before reaching your full retirement age, your Social Security benefits may be reduced by $1 for every $2 you earn above the annual limit.

Q9: Are there strategies to minimize the impact of the Social Security earnings test for farmers?

Strategies include reducing earned income below the threshold, restructuring the farming operation to reduce material participation, exploring different business structures, and consulting with a tax advisor or financial planner.

Q10: Does unearned income from farming affect my Social Security benefits?

Unearned income, such as passive rental income from farmland where you do not actively participate in management, generally does not affect your Social Security benefits.

Address: 1 University Station, Austin, TX 78712, United States.

Phone: +1 (512) 471-3434

Website: income-partners.net