Do You Get All Your State Income Tax Back? The answer isn’t always straightforward, but income-partners.net can help you navigate the complexities of state income tax refunds and explore opportunities to increase your income. Understanding the factors that influence your refund, such as withholdings and deductions, is crucial for maximizing your financial well-being. Partnering with the right financial advisors and exploring various income streams can further enhance your financial standing, ensuring you not only understand your tax situation but also optimize your income potential.

1. Understanding State Income Tax Refunds

Do you get all your state income tax back? Not necessarily. Whether you receive a refund, and the amount, depends on your individual circumstances and how much state income tax you paid versus what you actually owed. A refund is essentially the difference between the tax you paid throughout the year (through withholdings or estimated tax payments) and your actual tax liability.

1.1 Factors Influencing Your State Income Tax Refund

Several factors determine whether you get a refund and its size. These include:

- Withholdings: The amount of state income tax withheld from your paycheck throughout the year.

- Estimated Tax Payments: Payments you make if you are self-employed, have significant investment income, or otherwise don’t have enough tax withheld.

- Deductions: Expenses that reduce your taxable income, such as itemized deductions (medical expenses, mortgage interest, charitable contributions) or the standard deduction.

- Credits: Direct reductions of your tax liability, such as credits for child care, education expenses, or energy-efficient home improvements.

1.2 Overpayment vs. Underpayment

If you overpaid your state income tax, you’ll receive a refund. Conversely, if you underpaid, you’ll owe additional tax. Aiming for a balance between overpayment and underpayment is generally ideal, as it avoids tying up your money unnecessarily while ensuring you meet your tax obligations.

2. How Withholdings Affect Your Refund

Do you get all your state income tax back if you have too much withheld? Yes, potentially, but it’s not the most efficient financial strategy. The more state income tax withheld from your paycheck, the larger your potential refund. However, this means you’re essentially giving the state an interest-free loan. Adjusting your withholdings can help you keep more money in your pocket throughout the year.

2.1 Adjusting Your Withholdings

You can adjust your state income tax withholdings by submitting a new W-4 form to your employer. This form allows you to claim allowances, which reduce the amount of tax withheld. Factors to consider when adjusting your withholdings include:

- Changes in Income: If your income has increased or decreased, you may need to adjust your withholdings.

- New Deductions or Credits: If you anticipate claiming new deductions or credits, you can reduce your withholdings.

- Life Events: Major life events such as marriage, divorce, or the birth of a child can impact your tax liability and require adjustments to your withholdings.

2.2 Using a Withholding Calculator

Many states offer online withholding calculators that can help you estimate your tax liability and determine the appropriate amount to withhold. These calculators take into account your income, deductions, and credits to provide a personalized withholding recommendation.

3. State Income Tax Deductions and Credits

Do you get all your state income tax back if you maximize deductions and credits? Maximizing eligible deductions and credits can significantly impact your state income tax liability and potentially increase your refund.

3.1 Common State Income Tax Deductions

Many states offer deductions similar to those available on the federal level, such as:

- Itemized Deductions: If your itemized deductions (medical expenses, mortgage interest, charitable contributions) exceed the standard deduction, you can itemize to reduce your taxable income.

- Student Loan Interest: You may be able to deduct student loan interest payments, subject to certain limitations.

- IRA Contributions: Contributions to traditional IRAs may be deductible, depending on your income and whether you are covered by a retirement plan at work.

- Health Savings Account (HSA) Contributions: Contributions to an HSA are generally deductible.

3.2 State-Specific Tax Credits

Many states offer tax credits tailored to their specific needs and priorities. These may include:

- Child Care Credit: A credit for expenses related to child care.

- Earned Income Tax Credit (EITC): A credit for low-to-moderate income workers and families.

- Education Credits: Credits for tuition and other education expenses.

- Energy-Efficient Home Improvement Credits: Credits for installing energy-efficient equipment in your home.

3.3 Researching Available Deductions and Credits

It’s crucial to research the specific deductions and credits available in your state, as they can vary significantly. State tax agencies typically provide detailed information on their websites.

4. Understanding Refundable vs. Non-Refundable Tax Credits

Do you get all your state income tax back even if you owe no taxes, thanks to refundable credits? Refundable tax credits can indeed result in a refund even if you owe no taxes. Understanding the difference between refundable and non-refundable credits is crucial for maximizing your tax benefits.

4.1 Refundable Tax Credits

Refundable tax credits can reduce your tax liability to zero, and if the credit amount exceeds your liability, you’ll receive the difference as a refund. Examples of refundable credits include the Earned Income Tax Credit (EITC) and the Additional Child Tax Credit.

4.2 Non-Refundable Tax Credits

Non-refundable tax credits can only reduce your tax liability to zero. If the credit amount exceeds your liability, you won’t receive the difference as a refund. Examples of non-refundable credits include the Child Tax Credit and education credits.

4.3 Maximizing Credit Usage

To maximize the benefits of tax credits, it’s essential to understand whether they are refundable or non-refundable and to plan your tax strategy accordingly.

5. State Income Tax Rates and Brackets

Do you get all your state income tax back depending on your tax bracket? While your tax bracket doesn’t directly determine whether you get a refund, it does influence your overall tax liability, which in turn affects the size of your refund or the amount you owe.

5.1 Progressive, Regressive, and Flat Tax Systems

States employ various income tax systems, including:

- Progressive Tax Systems: Tax rates increase as income increases.

- Regressive Tax Systems: Lower-income individuals pay a higher percentage of their income in taxes.

- Flat Tax Systems: All income is taxed at the same rate.

5.2 Impact of Tax Rates on Refund

Your state’s income tax rates and brackets determine how much tax you owe on your taxable income. Higher tax rates generally result in higher tax liabilities, while lower rates result in lower liabilities. Your refund is the difference between what you paid and what you owe, so tax rates indirectly affect your refund.

5.3 Researching Your State’s Tax System

Understanding your state’s income tax system is crucial for effective tax planning. State tax agencies provide detailed information on tax rates, brackets, and how they apply to your income.

6. Common Reasons for State Income Tax Refund Delays

Do you get all your state income tax back on time, or are there common delays? While states strive to process refunds promptly, delays can occur for various reasons. Knowing these reasons can help you anticipate and potentially avoid delays.

6.1 Errors on Your Tax Return

The most common reason for refund delays is errors on your tax return. These can include:

- Incorrect Social Security Numbers: Ensure that you have accurately entered your Social Security number and those of any dependents.

- Math Errors: Double-check all calculations to avoid math errors.

- Missing Information: Ensure that you have included all required information, such as W-2 forms and supporting documentation for deductions and credits.

6.2 Identity Theft and Fraud

States are increasingly vigilant about identity theft and fraud, which can lead to refund delays. If your return is flagged for potential fraud, it may undergo additional scrutiny.

6.3 Returns Under Review

Certain returns may be selected for manual review, which can delay the processing of your refund. This doesn’t necessarily mean there’s something wrong with your return, but it may require additional time for verification.

6.4 High Volume of Returns

During peak filing season (March, April, and May), state tax agencies may experience a high volume of returns, which can lead to processing delays. Filing early can help you avoid these delays.

6.5 How to Check Your Refund Status

Most states offer online tools to check your refund status. These tools allow you to track the progress of your refund and estimate when you can expect to receive it.

7. What To Do If Your Refund Is Less Than Expected

Do you get all your state income tax back as you expected, or is it sometimes less? If your refund is less than expected, there are several possible explanations.

7.1 Adjustments to Your Return

The state tax agency may have made adjustments to your return, such as disallowing a deduction or credit. You should receive a notice explaining these changes.

7.2 Offset for Debts

Your refund may have been offset to pay outstanding debts, such as unpaid taxes, child support, or student loans. You should receive a notice if this has occurred.

7.3 Errors in Your Calculations

You may have made errors in your calculations, leading to an incorrect refund amount. Review your return carefully to identify any potential errors.

7.4 Contacting the State Tax Agency

If you’re unsure why your refund is less than expected, contact the state tax agency for clarification. They can provide detailed information about any adjustments or offsets made to your return.

8. The Importance of Accurate Tax Filing

Do you get all your state income tax back more easily with accurate filing? Accurate tax filing is crucial for avoiding delays, penalties, and other issues.

8.1 Keeping Accurate Records

Maintain accurate records of all income, deductions, and credits. This will make it easier to prepare your tax return and support any claims you make.

8.2 Filing on Time

File your tax return by the due date to avoid penalties. If you need more time, request an extension.

8.3 Seeking Professional Assistance

If you’re unsure about any aspect of tax filing, seek professional assistance from a qualified tax advisor. They can help you navigate the complexities of state income tax laws and ensure that you’re taking advantage of all available deductions and credits.

9. Maximizing Your Income Through Strategic Partnerships

While understanding state income tax refunds is important, focusing on increasing your income can have a more significant impact on your financial well-being. Strategic partnerships can be a powerful tool for income growth.

9.1 Identifying Potential Partners

Look for partners who complement your skills and resources. Consider businesses or individuals with:

- Complementary Products or Services: Partnering with businesses that offer complementary products or services can expand your reach and customer base.

- Shared Target Markets: Partnering with businesses that target the same market can increase your visibility and generate new leads.

- Established Networks: Partnering with individuals or businesses with established networks can provide access to new opportunities.

9.2 Types of Strategic Partnerships

There are various types of strategic partnerships, including:

- Joint Ventures: A collaborative project between two or more businesses.

- Affiliate Marketing: Promoting another business’s products or services in exchange for a commission.

- Referral Programs: Exchanging referrals with other businesses.

- Strategic Alliances: A long-term partnership focused on achieving shared goals.

9.3 Benefits of Strategic Partnerships

Strategic partnerships can offer numerous benefits, such as:

- Increased Revenue: By expanding your reach and customer base, partnerships can lead to increased revenue.

- Reduced Costs: Sharing resources and expenses with partners can reduce costs.

- Access to New Markets: Partnerships can provide access to new markets and customers.

- Enhanced Expertise: Partnering with experts can enhance your knowledge and skills.

10. Finding Partnership Opportunities on Income-Partners.net

Do you get all your state income tax back, or do you seek better opportunities through income-partners.net? Instead of solely relying on tax refunds, income-partners.net offers a platform to explore diverse partnership opportunities and boost your income potential.

10.1 Navigating Income-Partners.net

Income-partners.net provides a user-friendly interface to discover and connect with potential partners.

10.2 Types of Partnerships Featured

Income-partners.net showcases various partnership categories, including:

- Strategic Alliances: Form long-term collaborations to achieve shared goals and expand market reach.

- Joint Ventures: Collaborate on specific projects, combining resources and expertise for mutual benefit.

- Referral Programs: Exchange customer referrals, earning commissions for successful leads.

- Affiliate Marketing: Promote partner products or services and earn commissions on sales.

- Distribution Partnerships: Expand your product distribution network through strategic alliances.

- Technology Partnerships: Integrate complementary technologies to enhance product offerings.

- Investment Partnerships: Connect with investors to fund new ventures and growth opportunities.

- Marketing Partnerships: Collaborate on marketing campaigns to increase brand awareness and customer acquisition.

10.3 Success Stories from Income-Partners.net

Numerous individuals and businesses have found success through income-partners.net. These success stories highlight the potential of strategic partnerships to drive income growth and achieve business goals.

10.4 How to Get Started

To get started with income-partners.net:

- Create a Profile: Showcase your skills, experience, and partnership interests.

- Browse Opportunities: Explore partnership opportunities that align with your goals.

- Connect with Partners: Reach out to potential partners and initiate discussions.

- Build Relationships: Cultivate strong relationships with your partners to ensure long-term success.

Remember, while maximizing your state income tax refund can provide a small financial boost, focusing on strategic partnerships and income growth can lead to more substantial and sustainable financial gains. Visit income-partners.net today to explore the possibilities and start building your path to financial success.

Address: 1 University Station, Austin, TX 78712, United States

Phone: +1 (512) 471-3434

Website: income-partners.net

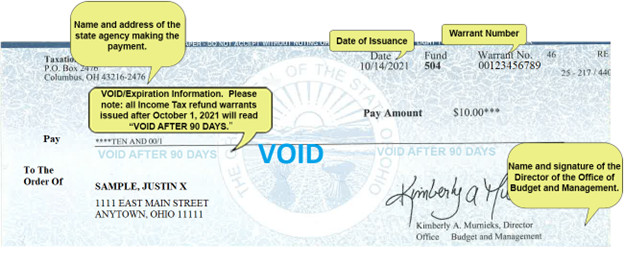

A graphic depicting a verifiable refund check, including the name and address of the state agency making the payment, date of issuance, warrant number, name and signature of the director of the Office of Budget and Management, and VOID/expiration information. Please note: all Income Tax refund warrants issued after October 1, 2021 will read VOID AFTER 90 DAYS

A graphic depicting a verifiable refund check, including the name and address of the state agency making the payment, date of issuance, warrant number, name and signature of the director of the Office of Budget and Management, and VOID/expiration information. Please note: all Income Tax refund warrants issued after October 1, 2021 will read VOID AFTER 90 DAYS

FAQ: State Income Tax Refunds

1. Do you get all your state income tax back if you overpay?

Yes, if you overpay your state income tax, you are generally entitled to a refund for the excess amount. The refund represents the difference between the amount you paid through withholdings or estimated payments and your actual tax liability for the year.

2. How do I check the status of my state income tax refund?

Most states offer online tools to check your refund status. You’ll typically need to provide your Social Security number, filing status, and the amount of your expected refund.

3. What if my state income tax refund is less than expected?

If your refund is less than expected, it could be due to adjustments made by the state tax agency, offsets for outstanding debts, or errors in your calculations. Contact the state tax agency for clarification.

4. Can I adjust my state income tax withholdings to get a bigger refund?

You can adjust your state income tax withholdings by submitting a new W-4 form to your employer. However, it’s generally better to aim for a balance between overpayment and underpayment, rather than intentionally overpaying to get a bigger refund.

5. What are some common state income tax deductions?

Common state income tax deductions include itemized deductions (medical expenses, mortgage interest, charitable contributions), student loan interest, IRA contributions, and HSA contributions.

6. Are state income tax credits refundable?

Some state income tax credits are refundable, meaning you can receive a refund even if you owe no taxes. Others are non-refundable, meaning they can only reduce your tax liability to zero.

7. How do state income tax rates affect my refund?

State income tax rates determine how much tax you owe on your taxable income. Higher tax rates generally result in higher tax liabilities, while lower rates result in lower liabilities, indirectly affecting your refund.

8. What if I didn’t receive my state income tax refund check?

If you haven’t received your refund check within a reasonable timeframe (e.g., 30 days), contact the state tax agency to request a reissue.

9. What is the deadline to file for a state income tax refund?

The deadline to file for a state income tax refund is typically four years from the original due date of the return.

10. Where can I find more information about state income tax refunds?

You can find more information about state income tax refunds on the website of your state’s tax agency or by consulting with a qualified tax advisor. You can also explore partnership opportunities to increase your income on income-partners.net.