Do Itemized Deductions Reduce Ordinary Income First? Yes, itemized deductions primarily reduce your ordinary income before being applied to capital gains. Understanding this principle can significantly impact your tax strategy, particularly when you’re aiming to optimize your income and explore partnership opportunities. At income-partners.net, we provide expert insights to help you navigate tax complexities and enhance your financial partnerships. We delve into how these deductions work, providing clear strategies for entrepreneurs, business owners, investors, marketing specialists, and product developers to maximize their tax efficiency.

1. Understanding Itemized Deductions and Ordinary Income

What are itemized deductions, and how do they relate to ordinary income?

Itemized deductions are specific expenses that taxpayers can claim on their tax returns to reduce their taxable income. These deductions, which include expenses like medical costs, state and local taxes (SALT), mortgage interest, and charitable contributions, directly lower your ordinary income before any capital gains considerations come into play. Understanding the intricacies of itemized deductions is crucial for effective tax planning.

1.1 What are Itemized Deductions?

Itemized deductions are expenses that you can subtract from your adjusted gross income (AGI) to lower your taxable income. Instead of taking the standard deduction, which is a fixed amount based on your filing status, you can choose to itemize if your eligible expenses exceed the standard deduction.

Key itemized deductions include:

- Medical Expenses: Costs exceeding 7.5% of your AGI.

- State and Local Taxes (SALT): Limited to $10,000 per household.

- Mortgage Interest: Interest paid on home loans.

- Charitable Contributions: Donations to qualified organizations.

1.2 What is Ordinary Income?

Ordinary income is income earned from regular sources, such as wages, salaries, tips, and business profits. This income is taxed at different rates based on your tax bracket, which is determined by your total taxable income.

1.3 How Itemized Deductions Impact Ordinary Income

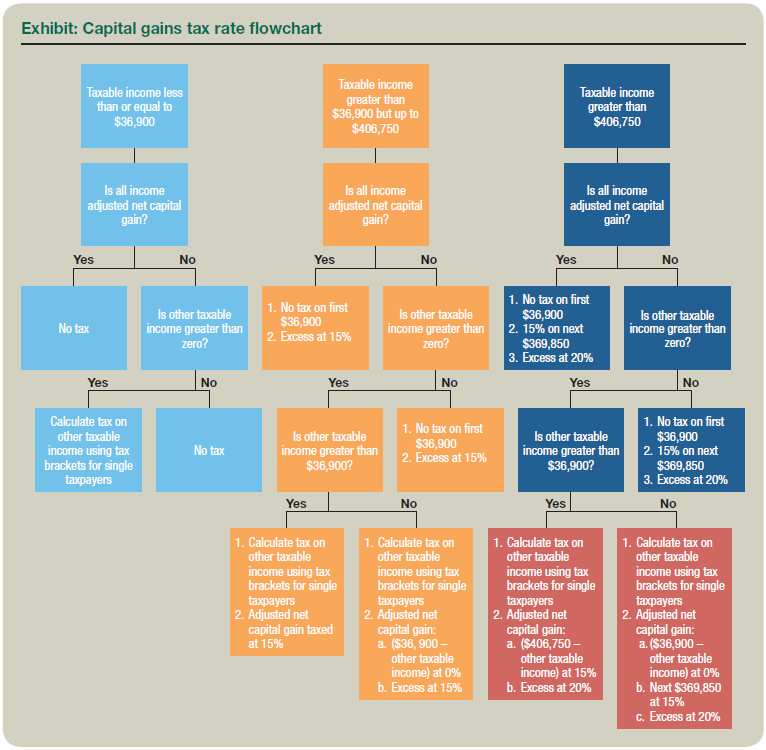

Itemized deductions directly reduce your ordinary income. By subtracting these deductions from your adjusted gross income (AGI), you arrive at a lower taxable income, which can result in a lower tax liability. The flowchart provided by the IRS illustrates this process, showing how deductions reduce your taxable income, which then affects the calculation of capital gains tax.

For example, if you have an AGI of $70,000 and itemized deductions totaling $15,000, your taxable income would be $55,000. This lower taxable income could potentially move you to a lower tax bracket, further reducing your tax liability.

Understanding the Flowchart

Understanding the Flowchart

2. The Priority of Ordinary Income Reduction

Why do itemized deductions reduce ordinary income before affecting capital gains?

Itemized deductions are applied to ordinary income first because the tax code prioritizes reducing income from regular sources before addressing capital gains. This approach helps to ensure that taxpayers receive the full benefit of their deductions against their most common forms of income.

2.1 IRS Guidelines on Deduction Application

The IRS guidelines clearly state that itemized deductions and personal exemptions first reduce other adjusted gross income (but not below zero) and then are applied against adjusted net capital gain. This means that if you have significant itemized deductions, they will first offset your ordinary income, potentially shielding some of your capital gains from taxation.

2.2 Impact on Capital Gains Tax Rates

The application of itemized deductions to ordinary income can indirectly affect the tax rates on your capital gains. Capital gains are taxed at different rates depending on your overall taxable income. By reducing your ordinary income with itemized deductions, you might lower your overall tax bracket, which can, in turn, affect the capital gains tax rate that applies to your investment income.

2.3 Strategies for Maximizing Tax Benefits

To maximize the tax benefits of itemized deductions, consider the following strategies:

- Bunching Deductions: If possible, concentrate deductible expenses in a single year to exceed the standard deduction threshold.

- Tax-Loss Harvesting: Offset capital gains with capital losses to reduce your overall tax liability.

- Consulting a Tax Professional: Seek advice from a tax professional to ensure you are taking advantage of all available deductions and credits.

3. Tax Implications for Capital Gains

How do itemized deductions and ordinary income interact to affect capital gains taxes?

The interplay between itemized deductions and ordinary income significantly influences the taxation of capital gains. By reducing ordinary income, itemized deductions can lower the overall tax burden, potentially shifting capital gains into lower tax brackets.

3.1 Understanding Capital Gains

Capital gains are profits from the sale of assets, such as stocks, bonds, and real estate. These gains are taxed differently from ordinary income, often at lower rates. There are two types of capital gains:

- Short-Term Capital Gains: Profits from assets held for one year or less, taxed at ordinary income rates.

- Long-Term Capital Gains: Profits from assets held for more than one year, taxed at preferential rates (0%, 15%, or 20%, depending on your income).

3.2 How Itemized Deductions Affect Capital Gains Rates

When itemized deductions reduce your ordinary income, they can indirectly affect the tax rate applied to your capital gains. Here’s how:

- Lowering Taxable Income: Itemized deductions decrease your taxable income, potentially moving you into a lower tax bracket.

- Impacting Capital Gains Rates: If your ordinary income is significantly reduced, more of your capital gains may be taxed at the 0% or 15% rate, rather than the 20% rate.

3.3 Examples of Tax Savings

Consider this scenario:

- Without Itemized Deductions: A taxpayer has $60,000 of ordinary income and $40,000 of long-term capital gains. The capital gains might be taxed at 15% or 20%, depending on their tax bracket.

- With Itemized Deductions: The same taxpayer has $60,000 of ordinary income but claims $15,000 in itemized deductions, reducing their taxable income to $45,000. This could shift the capital gains into a lower tax bracket, potentially resulting in a 0% or 15% tax rate on a portion of the gains.

4. Examples of Itemized Deductions in Action

Can you provide real-world examples of how itemized deductions work with capital gains?

Let’s explore a few examples to illustrate how itemized deductions can interact with capital gains in different scenarios.

4.1 Example 1: Single Taxpayer with Modest Income

A single taxpayer has $35,000 in ordinary income and $15,000 in adjusted net capital gains. Their itemized deductions total $8,000.

- Without Itemized Deductions: Taxable income is $50,000. The tax on ordinary income is calculated using the applicable tax brackets. A portion of the capital gains may be taxed at 15%.

- With Itemized Deductions: Taxable income is reduced to $42,000. The tax on ordinary income is lower, and a larger portion of the capital gains may qualify for the 0% rate.

4.2 Example 2: High-Income Taxpayer with Significant Capital Gains

A taxpayer has $500,000 in ordinary income and $200,000 in adjusted net capital gains. They have itemized deductions of $30,000.

- Without Itemized Deductions: Taxable income is $700,000. The capital gains are likely taxed at 20%.

- With Itemized Deductions: Taxable income is reduced to $670,000. While the capital gains are still likely taxed at 20%, the overall tax liability is reduced due to the lower taxable income.

4.3 Example 3: Business Owner with Fluctuating Income

A business owner has $80,000 in ordinary income one year and $40,000 the next. In both years, they have $20,000 in adjusted net capital gains. They can itemize deductions of $10,000 each year.

- Year 1:

- Without Itemized Deductions: Taxable income is $100,000.

- With Itemized Deductions: Taxable income is $90,000.

- Year 2:

- Without Itemized Deductions: Taxable income is $60,000.

- With Itemized Deductions: Taxable income is $50,000.

In both years, the itemized deductions reduce the taxable income, potentially affecting the tax rate on the capital gains.

Business Partnerships

Business Partnerships

5. Maximizing Tax Benefits Through Strategic Partnerships

How can strategic partnerships help in optimizing tax benefits related to itemized deductions and capital gains?

Strategic partnerships can play a crucial role in optimizing tax benefits. By collaborating with other businesses or individuals, you can leverage additional deductions, credits, and tax planning strategies to reduce your overall tax liability. At income-partners.net, we specialize in connecting you with partners who can enhance your tax optimization strategies.

5.1 Leveraging Business Expenses

Forming a partnership can allow you to pool resources and share business expenses, which can increase your deductible expenses. According to research from the University of Texas at Austin’s McCombs School of Business, collaborative ventures often lead to greater efficiency and cost savings, thus maximizing tax deductions.

5.2 Utilizing Pass-Through Entities

Partnerships, as pass-through entities, allow income and deductions to flow directly to the partners’ individual tax returns. This can be advantageous if you have significant deductions that can offset your share of the partnership’s income.

5.3 Strategic Investment Planning

Partnerships can also facilitate strategic investment planning. By pooling capital and expertise, partners can invest in assets that generate capital gains while also utilizing deductions to minimize the tax impact.

5.4 Examples of Partnership Benefits

Consider a scenario where two business owners form a partnership. One partner has significant business expenses that can be deducted, while the other has capital gains from investments. By combining their financial resources and tax planning strategies, they can optimize their overall tax benefits.

6. Common Misconceptions About Itemized Deductions

What are some common misunderstandings about how itemized deductions interact with ordinary income and capital gains?

There are several common misconceptions about itemized deductions and their impact on capital gains. Addressing these misunderstandings can help taxpayers make more informed decisions and optimize their tax planning.

6.1 Misconception 1: Itemized Deductions Only Benefit High-Income Earners

Many people believe that itemized deductions are only beneficial for high-income earners. However, this is not necessarily true. If your itemized deductions exceed the standard deduction for your filing status, you can benefit from itemizing, regardless of your income level.

6.2 Misconception 2: Itemized Deductions Directly Reduce Capital Gains Tax

While itemized deductions reduce your overall taxable income, they do not directly reduce the amount of capital gains tax you owe. Instead, they lower your ordinary income, which can indirectly affect the tax rate applied to your capital gains.

6.3 Misconception 3: Standard Deduction is Always Better

Some taxpayers assume that taking the standard deduction is always the best option. However, it’s essential to calculate your potential itemized deductions to determine whether they exceed the standard deduction. If they do, itemizing can result in a lower tax liability.

6.4 Misconception 4: All Expenses are Deductible

Not all expenses are deductible. The IRS has specific rules and limitations on what expenses can be claimed as itemized deductions. For example, there are limits on the amount of state and local taxes you can deduct.

6.5 Clearing Up the Confusion

To clear up these misconceptions, taxpayers should:

- Keep Accurate Records: Maintain detailed records of all potential deductible expenses.

- Calculate Both Options: Compare the standard deduction with itemized deductions to determine the most beneficial option.

- Seek Professional Advice: Consult with a tax professional to ensure they are taking advantage of all available deductions and credits.

7. How Tax Planning Can Minimize Capital Gains

What are some strategic tax planning techniques that can minimize the impact of capital gains taxes?

Strategic tax planning is essential for minimizing the impact of capital gains taxes. By implementing various techniques, taxpayers can reduce their tax liability and maximize their investment returns.

7.1 Tax-Loss Harvesting

Tax-loss harvesting involves selling investments at a loss to offset capital gains. This strategy can reduce your overall tax liability and potentially generate a tax deduction if your capital losses exceed your capital gains.

7.2 Investing in Tax-Advantaged Accounts

Investing in tax-advantaged accounts, such as 401(k)s and IRAs, can help you defer or eliminate capital gains taxes. These accounts offer various tax benefits, such as tax-deferred growth and tax-free withdrawals.

7.3 Qualified Opportunity Zones

Investing in Qualified Opportunity Zones (QOZs) can provide significant tax benefits, including the deferral or elimination of capital gains taxes. QOZs are designated areas with economic development needs, and investments in these zones can qualify for special tax incentives.

7.4 Charitable Donations

Donating appreciated assets, such as stocks, to a qualified charity can provide a double tax benefit. You can deduct the fair market value of the asset as a charitable contribution and avoid paying capital gains taxes on the appreciation.

7.5 Like-Kind Exchanges

Like-kind exchanges, also known as 1031 exchanges, allow you to defer capital gains taxes when exchanging one investment property for another similar property. This strategy can be particularly useful for real estate investors.

7.6 Example of Tax Planning Success

Consider a taxpayer who uses tax-loss harvesting to offset capital gains. By selling investments at a loss of $10,000, they can offset $10,000 of capital gains, resulting in a lower tax liability.

Tax Planning Success

Tax Planning Success

8. Navigating Tax Laws and Regulations

How can taxpayers stay informed about changes in tax laws and regulations that affect itemized deductions and capital gains?

Staying informed about changes in tax laws and regulations is crucial for effective tax planning. Tax laws are constantly evolving, and it’s essential to stay updated to ensure you are taking advantage of all available deductions and credits.

8.1 IRS Resources

The IRS provides numerous resources for taxpayers, including publications, forms, and online tools. The IRS website is a valuable source of information on tax laws, regulations, and updates.

8.2 Tax Professional

Consulting with a tax professional can provide personalized advice and guidance on tax planning. A tax professional can help you navigate the complexities of the tax code and ensure you are in compliance with all applicable laws and regulations.

8.3 Tax Software

Tax software programs can help you prepare and file your tax returns while also providing guidance on deductions and credits. These programs are often updated to reflect the latest tax laws and regulations.

8.4 Professional Organizations

Professional organizations, such as the American Institute of Certified Public Accountants (AICPA), provide resources and updates on tax laws and regulations. These organizations can be valuable sources of information for taxpayers and tax professionals alike.

8.5 Subscribing to Newsletters

Subscribing to tax newsletters and publications can help you stay informed about changes in tax laws and regulations. These newsletters often provide insights and analysis from tax experts.

8.6 Example of Staying Informed

Consider a taxpayer who subscribes to a tax newsletter and learns about a new deduction that they are eligible for. By staying informed, they can take advantage of this deduction and reduce their tax liability.

9. Case Studies of Successful Tax Optimization

Can you share some real-life case studies of how taxpayers have successfully optimized their tax situations using itemized deductions and capital gains strategies?

Examining real-life case studies can provide valuable insights into how taxpayers have successfully optimized their tax situations.

9.1 Case Study 1: Real Estate Investor

A real estate investor used a 1031 exchange to defer capital gains taxes on the sale of an investment property. By exchanging the property for a similar property, they were able to avoid paying capital gains taxes and continue growing their real estate portfolio.

9.2 Case Study 2: Business Owner

A business owner donated appreciated stock to a qualified charity. They were able to deduct the fair market value of the stock as a charitable contribution and avoid paying capital gains taxes on the appreciation.

9.3 Case Study 3: High-Income Earner

A high-income earner used tax-loss harvesting to offset capital gains. By selling investments at a loss, they were able to reduce their overall tax liability and minimize the impact of capital gains taxes.

9.4 Case Study 4: Family with High Medical Expenses

A family with high medical expenses itemized their deductions and reduced their taxable income significantly. By itemizing, they were able to lower their tax liability and free up more cash for other expenses.

9.5 Key Takeaways from the Case Studies

These case studies illustrate the importance of:

- Strategic Tax Planning: Implementing proactive tax planning strategies to minimize tax liability.

- Utilizing Deductions and Credits: Taking advantage of all available deductions and credits.

- Staying Informed: Staying updated on changes in tax laws and regulations.

10. Resources and Tools for Taxpayers

What resources and tools are available to help taxpayers understand and manage itemized deductions and capital gains?

Numerous resources and tools are available to help taxpayers understand and manage itemized deductions and capital gains.

10.1 IRS Website

The IRS website offers a wealth of information on tax laws, regulations, forms, and publications.

10.2 Tax Software

Tax software programs, such as TurboTax and H&R Block, can help you prepare and file your tax returns while also providing guidance on deductions and credits.

10.3 Tax Professionals

Consulting with a tax professional can provide personalized advice and guidance on tax planning.

10.4 Financial Advisors

Financial advisors can help you develop a comprehensive financial plan that includes tax planning strategies.

10.5 Online Calculators

Online calculators can help you estimate your tax liability and determine the potential impact of itemized deductions and capital gains.

10.6 Workshops and Seminars

Attending tax workshops and seminars can provide valuable insights and information on tax planning strategies.

FAQ About Itemized Deductions and Ordinary Income

1. What happens if my itemized deductions are less than the standard deduction?

If your itemized deductions are less than the standard deduction, you should take the standard deduction, as it will result in a lower taxable income.

2. Can I deduct expenses related to my business as itemized deductions?

No, business expenses are typically deducted on Schedule C of your tax return, not as itemized deductions.

3. How does the $10,000 SALT limit affect my itemized deductions?

The $10,000 SALT limit restricts the amount of state and local taxes you can deduct, including property taxes, income taxes, and sales taxes.

4. Can I deduct medical expenses for my dependents?

Yes, you can deduct medical expenses for your dependents if they meet certain criteria, such as being under age 19 or a full-time student under age 24.

5. How do I know if a charity is a qualified organization for deduction purposes?

You can use the IRS’s Tax Exempt Organization Search tool to verify if a charity is a qualified organization.

6. What records do I need to keep for itemized deductions?

You should keep receipts, canceled checks, and other documentation to support your itemized deductions.

7. Can I deduct student loan interest as an itemized deduction?

No, student loan interest is an above-the-line deduction, not an itemized deduction.

8. How do itemized deductions affect my adjusted gross income (AGI)?

Itemized deductions are subtracted from your adjusted gross income (AGI) to arrive at your taxable income.

9. What is the difference between a tax deduction and a tax credit?

A tax deduction reduces your taxable income, while a tax credit directly reduces the amount of tax you owe.

10. Where can I find the standard deduction amounts for the current tax year?

You can find the standard deduction amounts for the current tax year on the IRS website or in the instructions for Form 1040.

11. How does AMT affect itemized deductions?

The alternative minimum tax (AMT) can limit the benefits of certain itemized deductions. AMT also taxes adjusted net capital gain at the 0%, 15%, and 20% rates, with the applicable phaseouts as income increases. However, alternative minimum taxable income is often different from ordinary income, and AMT does feature graduated rates. At higher income levels, AMT will need to be calculated.

Conclusion

Understanding how itemized deductions reduce ordinary income first is crucial for effective tax planning. By strategically managing your deductions and capital gains, you can minimize your tax liability and maximize your financial success. Remember to stay informed about changes in tax laws and regulations and consult with a tax professional for personalized advice. At income-partners.net, we’re dedicated to providing you with the resources and partnerships you need to navigate the complexities of tax planning and achieve your financial goals.

Ready to take your tax optimization to the next level? Explore the diverse partnership opportunities at income-partners.net. Discover strategies to build effective relationships and connect with potential partners in the US, particularly in thriving hubs like Austin. Don’t miss out on the chance to boost your income and create profitable collaborations! Contact us today at Address: 1 University Station, Austin, TX 78712, United States. Phone: +1 (512) 471-3434.