Dealing with debt collectors can be stressful, especially when you’re unsure of your rights and obligations. If you’ve been contacted by Capio Partners Llc, it’s essential to understand who they are and how to effectively manage the situation. This guide provides a comprehensive overview of Capio Partners, a debt collection agency specializing in medical debt, and outlines the steps you can take to address your debt responsibly.

Concerned Man Looking at Bills

Concerned Man Looking at Bills

Understanding Capio Partners LLC

Capio Partners LLC operates as a third-party debt collection agency. Their primary focus is the recovery of outstanding medical debts. Established in 2008, Capio Partners is headquartered in Sherman, Texas, with additional offices in Lawrenceville, Georgia. They operate across the United States, purchasing debts from healthcare providers and then attempting to collect those debts from individuals.

Why is Capio Partners Contacting You?

If Capio Partners LLC is reaching out, it’s highly likely due to an unpaid medical bill. This could stem from various healthcare services, such as hospital treatments, ambulance services, or doctor’s visits. Healthcare providers often have internal processes for collecting payments. However, when these bills become overdue, they may choose to “charge off” the debt or sell it to a third-party agency like Capio Partners. This means Capio Partners now owns the debt and is responsible for pursuing collection. You are now hearing from them instead of the original medical facility because they have taken over the collection process for this debt.

Is Capio Partners LLC a Legitimate Company?

Yes, Capio Partners LLC is a legitimate debt collection agency. However, like many debt collectors, they have faced scrutiny and consumer complaints.

While not accredited by the Better Business Bureau (BBB), Capio Partners LLC does have a BBB profile. Currently, they hold a “B” rating. Their customer review rating on the BBB is low, at 1.16 out of 5 stars, based on nearly 500 complaints.

Furthermore, the Consumer Financial Protection Bureau (CFPB) data reveals over 1,200 complaints filed against Capio Partners LLC.

Common complaints against Capio Partners LLC include allegations of:

- Contacting individuals about debts they claim not to owe or debts that are not theirs.

- Failing to provide sufficient documentation or information to validate the debt, such as the original debt agreement or account details.

- Not furnishing consumers with legally required debt dispute information.

These complaints may indicate potential violations of the Fair Debt Collection Practices Act (FDCPA). The FDCPA is a federal law designed to protect consumers from abusive, deceptive, and unfair debt collection practices. It mandates that debt collectors provide a debt validation notice and outlines procedures for disputing debts.

It’s important to note that while these complaints are concerning, they may not represent the experience of every consumer who interacts with Capio Partners LLC.

Avoiding Scams Impersonating Capio Partners

While Capio Partners LLC is a real debt collection agency, be aware that scammers sometimes impersonate legitimate companies to defraud individuals. It’s crucial to recognize the warning signs of debt collection scams to protect yourself.

If you are contacted by someone claiming to be a debt collector, especially if it’s unexpected, always request debt validation before providing any personal information. Legitimate debt collectors should possess details about your debt account. Be particularly wary if they demand sensitive information like bank account details or your Social Security number upfront.

Do You Have to Pay Capio Partners LLC?

Whether you are legally obligated to pay Capio Partners LLC depends on the validity of the debt. The first step is to determine if you actually owe the debt they are attempting to collect. Have you received a debt validation notice from Capio Partners? This notice should detail the original creditor (the medical provider), the amount owed, and other relevant information about the debt.

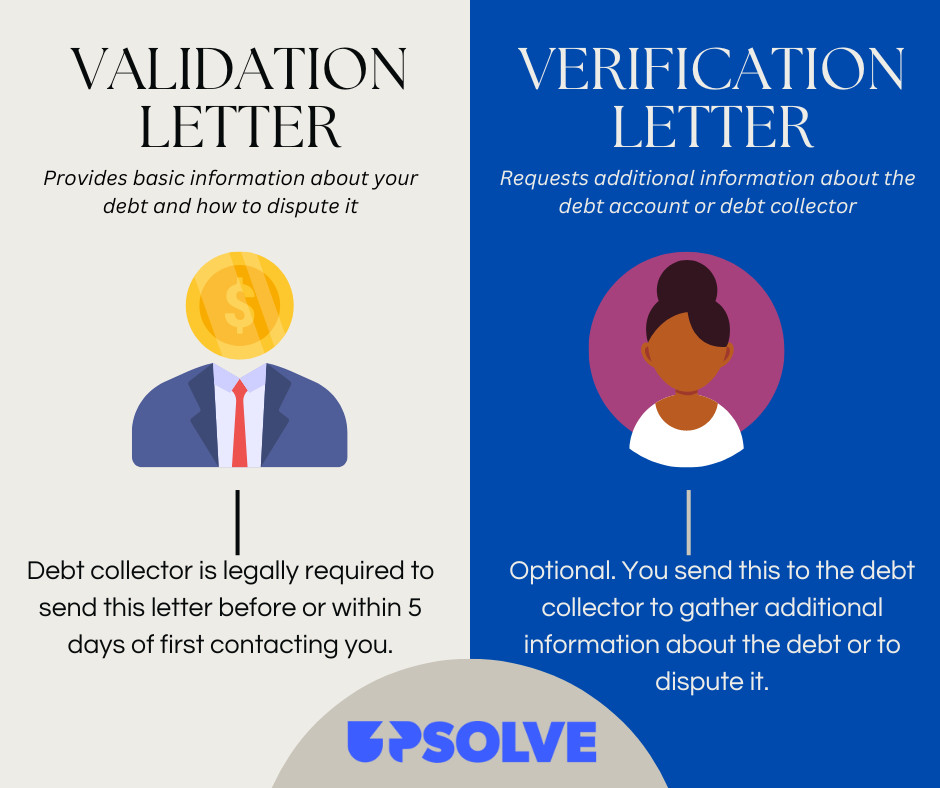

If you haven’t received a validation notice, or if you require more clarity about the debt, you should send them a debt verification letter.

Step 1: Sending a Debt Verification Letter to Capio Partners LLC

Under the FDCPA, debt collectors like Capio Partners LLC are legally required to send you a debt validation letter. This must be sent either before their initial contact or within five days of that first contact. This letter must inform you of your right to dispute the debt.

You have a 30-day window to dispute the debt from the date of the validation notice. If you formally dispute the debt within this timeframe, it should be noted on your credit report. Capio Partners LLC should cease collection activities, including phone calls, until they respond to your dispute and provide verification of the debt.

If you dispute the debt and Capio Partners LLC fails to verify it or does not respond to your dispute, they should halt collection efforts, and you may not be legally obligated to pay.

While the terms “debt dispute letter” and “debt verification letter” are sometimes used interchangeably, sending a verification letter can also be useful if you need more information beyond what was in the initial validation notice.

Key Difference:

- Debt Validation Letter: Legally required notice from the debt collector informing you of the debt and your dispute rights.

- Debt Verification Letter: A letter you send to the debt collector requesting further information and proof of the debt.

Step 2: Deciding Your Course of Action with Capio Partners LLC

Once Capio Partners LLC has validated the debt (or if you acknowledge the debt), you have several options:

- Dispute the Debt: If you believe the debt is inaccurate, doesn’t belong to you, or has already been paid.

- Negotiate a Debt Settlement: Attempt to pay a reduced amount to resolve the debt. You can also explore setting up a payment plan.

- Ignore the Debt: While an option, this is strongly discouraged due to potential negative consequences.

Let’s examine each option more closely.

Option 1: Disputing the Debt with Capio Partners LLC

Dispute the debt if you disagree with the amount Capio Partners LLC claims you owe, if the debt is not yours, or if you have already paid it (or your insurance has).

Instructions for disputing the debt are typically included in the debt validation letter. You can find detailed guidance in resources like “Guide To Disputing a Debt You Don’t Owe”.

When disputing a debt, it’s also prudent to check your credit report for inaccuracies. Errors on credit reports are common and can negatively impact your credit score. For medical debts specifically, there are particular considerations. According to the CFPB, medical debt under $500 should not appear on your credit report, regardless of its status.

The Fair Credit Reporting Act (FCRA) grants you the right to access your credit reports from Equifax, Experian, and TransUnion for free periodically. It also allows you to dispute any inaccuracies you find. Resources like “guide to disputing credit report errors” can assist you with this process.

Option 2: Negotiating a Debt Settlement with Capio Partners LLC

If you acknowledge the debt to Capio Partners LLC but cannot afford to pay the full amount, you can attempt to negotiate a debt settlement or establish a payment plan.

You can contact Capio Partners LLC by phone at (888) 502-0303. For settlement negotiations, it is generally recommended to put your offer in writing. You can utilize debt settlement agreement templates to draft your offer. It’s advisable to call and inquire about the correct mailing address for settlement proposals. You can also try negotiating over the phone, but always request any agreement in writing for your records.

How Debt Settlement Works with Capio Partners LLC

Debt collection agencies like Capio Partners LLC often purchase debts for significantly less than the original amount owed. This allows them some flexibility in negotiations. They may be willing to accept a settlement for a percentage of the total debt.

Debt settlement is a common practice. Collectors might agree to settle for amounts ranging from 40% to 60% of the original debt. For example, on a $1,000 medical bill, you could offer to pay $400 to settle the account. Be prepared for some back-and-forth negotiation.

More information on strategies for dealing with Capio Partners LLC can be found in guides like “Guide To Beating Capio Partners”.

Debts That Can Typically Be Negotiated

Past-due medical bills, credit card debt, and other unsecured consumer debts are generally negotiable. Debts secured by property, such as car loans or mortgages, are less likely to be negotiable because the lender has collateral they can repossess.

Student loans also have unique characteristics. Negotiating federal student loan debt is often difficult, but various student loan forgiveness programs have emerged in recent years that might offer relief.

Option 3: Ignoring the Debt from Capio Partners LLC (Not Recommended)

Ignoring Capio Partners LLC is generally not advisable. While it might seem like the easiest immediate option, it is unlikely to make the debt disappear and can lead to more significant problems.

Even if a medical debt is under $500 and shouldn’t impact your credit report, Capio Partners LLC may escalate their collection efforts if ignored. This could include initiating a debt collection lawsuit against you to seek a court order for wage garnishment. If a lawsuit occurs, you may incur additional costs in the form of court fees and legal expenses, increasing the total amount you owe.

In Conclusion: Addressing your debt with Capio Partners LLC proactively is the most responsible approach. Understanding your options to dispute or settle the debt allows you to take control of the situation and work towards resolving it.

Can Capio Partners LLC Sue You?

Yes, Capio Partners LLC has the legal right to sue you for unpaid debt. However, suing is often not the first course of action for debt collectors.

If Capio Partners LLC does pursue a lawsuit, you will be officially served with court documents, typically a summons and complaint. These documents will inform you that you are being sued and the reasons for the lawsuit.

If you are sued for debt, it is critical to respond to the lawsuit. Ignoring a debt collection lawsuit can lead to a default judgment against you. This allows Capio Partners LLC to pursue actions like wage garnishment to recover the debt.

If you are facing a debt collection lawsuit and need assistance responding, resources like SoloSuit can provide tools and guidance to help you draft an answer.

Summary: Dealing with Capio Partners LLC

Capio Partners LLC is a legitimate debt collection agency specializing in medical debt. If they contact you, prioritize debt validation. If the debt is valid and you owe it, explore payment plans or debt settlement. If you dispute the debt’s validity, take immediate steps to formally dispute it. While lawsuits are not always the first step, Capio Partners LLC can sue for unpaid debt, making it important to address their contact and take appropriate action.

Share Article [⬈]

Written By:

Upsolve’s content is created by a team of bankruptcy attorneys and finance professionals dedicated to providing up-to-date, informative, and helpful resources on debt and financial matters.

Concerned Man Looking at Bills

LinkedIn Jonathan Petts, co-founder and CEO of Upsolve, brings over a decade of experience in bankruptcy law. He holds an LLM in Bankruptcy from St. John’s University, has clerked for federal bankruptcy judges, and has worked at leading New York City law firms specializing in bankruptcy. Read more about Jonathan Petts