Bad debt expense, a crucial aspect of financial accounting, is indeed recorded on the income statement. Are you seeking to optimize your financial statements and forge strategic partnerships to boost revenue? At income-partners.net, we provide insights and strategies for managing bad debt and connecting with valuable business partners to enhance your financial health. Keep reading to explore practical methods for handling uncollectible accounts, minimizing financial losses, and cultivating successful partnerships. By leveraging strategic alliances and optimizing your financial processes, you can achieve sustainable growth and increased profitability.

1. Understanding Bad Debt Expense

Bad debt expense (BDE) represents the portion of a company’s accounts receivable that is deemed uncollectible and is subsequently written off. Accountants record bad debt as an expense under Sales, General, and Administrative expenses (SG&A) on the income statement. This entry reduces the value of receivables on the balance sheet, reflecting a more accurate picture of the company’s financial position.

1.1. Key Aspects of Bad Debt Expense

-

Accrual Accounting: Bad debt expense is primarily relevant under the accrual accounting system, where revenue is recognized when earned, regardless of when cash is received.

-

Not a Permanent Loss: Recording bad debt doesn’t necessarily mean the money is lost forever. The company retains the right to pursue collection if the customer’s financial situation improves.

-

Reversal of Revenue: The expense reverses previously recorded revenue when it becomes clear that payment will not be received.

1.2. Why Accrual Accounting Matters

Under accrual accounting, revenue is recognized before the cash arrives. According to the Generally Accepted Accounting Principles (GAAP), companies must follow the allowance method due to the matching principle. This can lead to complications if a customer fails to pay months after the sale. Bad debt expense is then used to reverse the recorded revenue in subsequent periods.

1.3. Cash-Based vs. Accrual Accounting

It’s important to note that bad debt expense is not applicable if you follow the cash-based method of accounting. In the cash method, revenue is only recorded when the payment is physically received. Therefore, if a credit sale becomes uncollectible, there’s no need to cancel out the receivable with a bad debt expense because the revenue was never initially recognized.

2. Common Causes of Bad Debt

Bad debt can arise from various factors, impacting businesses across different sectors. Understanding these causes can help companies take preventive measures.

-

Disagreements: Customers may refuse to pay due to dissatisfaction with the product or service quality.

-

Bankruptcy: Customers facing bankruptcy might be unable to fulfill their payment obligations.

-

Poor Communication: Misunderstandings about payment terms can arise when sales teams offer credit terms without consulting the accounts receivable (AR) department.

2.1. The Accounts Receivable Disconnect

One of the primary reasons for bad debt is the “Accounts Receivable Disconnect,” which refers to the communication gap between AR departments and their customers due to disconnected systems. This lack of communication can lead to misunderstandings and increased bad debt. As revealed in a Wakefield Research and Versapay survey, 85% of surveyed C-level executives reported that miscommunication between their AR department and customers resulted in customers not paying in full.

2.2. The Impact of Customer Experience

Customers are more likely to default on payments if they have a poor billing and payment experience. Improving customer experience is critical for minimizing bad debt. According to research, a streamlined and customer-centric billing process can significantly reduce the likelihood of non-payment.

3. Methods to Record Bad Debt Expense

There are two main methods for recording bad debt expenses in accounting statements: the direct write-off method and the allowance method. Each has its advantages and specific use cases.

- Direct Write-Off Method

- Allowance Method

3.1. Direct Write-Off Method

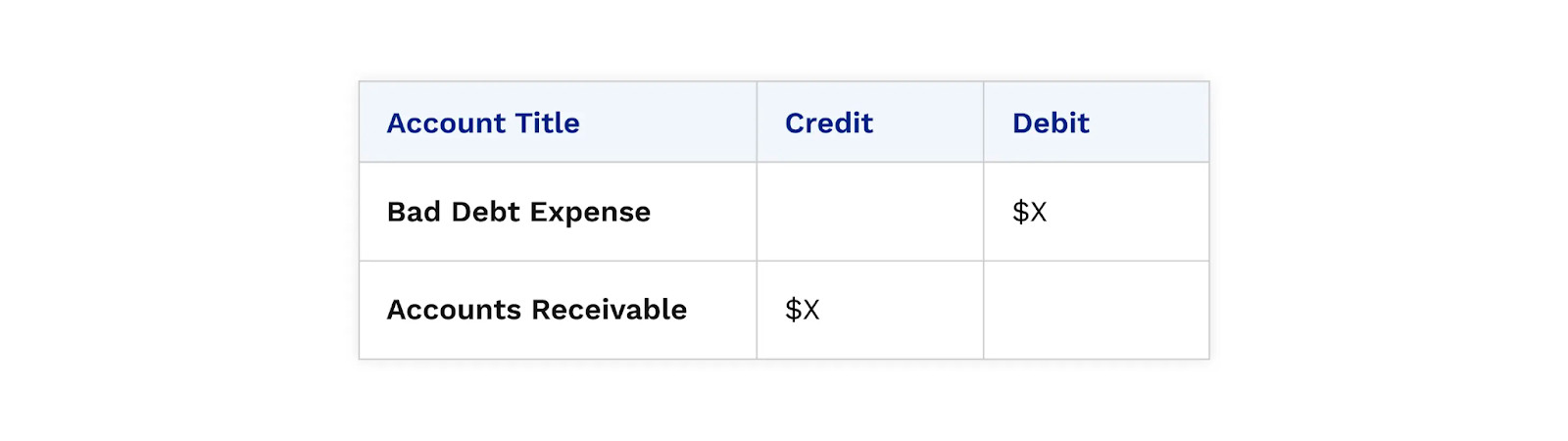

The direct write-off method involves immediately writing off a portion of the receivable account as bad debt when an invoice is deemed uncollectible. This method is straightforward, debiting bad debt expense and crediting accounts receivable.

Journal Entry Example

| Account | Debit | Credit |

|---|---|---|

| Bad Debt Expense | $X | |

| Accounts Receivable | $X | |

| To write off uncollectible account |

Bad debt expense journal entry using the direct write-off method

Bad debt expense journal entry using the direct write-off method

Advantages and Disadvantages

- Advantages: Simple and easy to implement.

- Disadvantages: Can misstate income if the write-off occurs in a different period from the initial sale.

This method is best suited for recording immaterial debts or when there are only a few uncollected invoices.

IRS Conditions for Write-Off

To satisfy the IRS’ conditions for writing off a debt, businesses must have:

- Firm evidence that the customer will not pay.

- Taken reasonable steps to collect the amount owed, such as contacting the customer or addressing disputes.

3.2. Allowance Method

The allowance method involves creating an allowance for doubtful accounts (AFDA) at the end of the fiscal year to estimate uncollectible amounts. This method aligns with the Generally Accepted Accounting Principles (GAAP) and the matching principle, which requires expenses and related revenue to be recorded in the same period.

Steps for Recording Bad Debt via the Allowance Method

- Create an AFDA journal account.

- Estimate AFDA at the end of the accounting period.

- Calculate actual bad debts.

This approach provides a more accurate representation of a company’s ability to collect invoices.

4. Estimating Bad Debt Expense Using the Allowance Method

Estimating bad debt expense under the allowance method can be done using three primary formulas: percentage of sales, percentage of accounts receivable, and accounts receivable aging.

- Percentage of Sales

- Percentage of Accounts Receivable

- Accounts Receivable Aging

These methods rely on historical averages of a business’s collections and are most effective when the underlying conditions are stable.

4.1. Conditions for Accurate Estimation

- Stable Customer Base: The customer base should remain relatively consistent.

- Stable Business Conditions: The business should not experience significant growth or decline.

- Steady Economic Conditions: The economic environment surrounding the industry should be stable.

4.2. Economic Cycle Considerations

Historical collection percentages can vary between economic cycles. Referencing past performance during different economic conditions can improve the accuracy of predictions.

4.3. Percentage of Sales Method

The percentage of sales method estimates bad debt based on a percentage of total credit sales.

Formula

Bad Debt Expense = Percentage of Sales Estimated Uncollectible × Actual Credit Sales

Example

- Historical Average Annual Credit Sales: $10,000,000

- Historical Average Uncollected Credit Sales: $500,000

- Historical Percentage of Uncollected Credit Sales: 5%

If actual credit sales for the current period are $12,000,000, the bad debt expense allowance would be:

BDE Allowance = 5% of $12,000,000 = $600,000

Accounting Treatment

- Income Statement: The adjustment value (calculated BDE allowance) is recorded.

- Balance Sheet: The existing AFDA balance from the previous year is added to the adjustment balance to find the ending balance.

4.4. Percentage of Receivables Method

This method estimates bad debt based on a percentage of the accounts receivable balance.

Formula

Bad Debt Expense = Percentage Receivables Estimated Uncollectible × Receivables Balance

Example

- Historical Average Accounts Receivable: $15,000,000

- Historical Cash Collected from Accounts Receivable: $1,200,000

- Historical Percentage of Uncollected Receivables: 8%

If the receivables balance for the current period is $18,000,000, the bad debt expense allowance would be:

BDE Allowance = 8% of $18,000,000 = $1,440,000

Accounting Treatment

- Balance Sheet: The calculated BDE allowance is the ending AFDA balance for the period.

- Income Statement: The adjustment value (the difference between the ending and starting AFDA balances) is recorded.

4.5. Accounts Receivable Aging Method

The accounts receivable aging method assigns a collection probability to each AR aging category. This method provides a more detailed estimation of uncollectible amounts.

Process

- Create an AR aging report.

- Assign a collection probability to each aging bucket.

- Calculate the bad debt allowance for each bucket.

- Sum the totals to find the ending balance.

Example of an Accounts Receivable Aging Report

| Aging Bucket | Receivables Balance | Collection Probability | Bad Debt Reserve |

|---|---|---|---|

| Current | $500,000 | 1% | $5,000 |

| 31-60 Days | $300,000 | 5% | $15,000 |

| 61-90 Days | $150,000 | 15% | $22,500 |

| Over 90 Days | $50,000 | 30% | $15,000 |

| Total | $1,000,000 | $57,500 |

The accounts receivable aging method offers an advantage because it gives accounts receivable teams a more exact basis for estimating their uncollectibles

The accounts receivable aging method offers an advantage because it gives accounts receivable teams a more exact basis for estimating their uncollectibles

Advantages and Disadvantages

- Advantages: Provides a more accurate estimate by considering the age of outstanding receivables.

- Disadvantages: Still relies on averages, and individual outstanding accounts can skew calculations.

5. Bad Debt Expense Calculator Overview

Using the allowance method, here’s an overview of calculating bad debt expense using the three methods:

| Method | Formula |

|---|---|

| Percentage of Sales | Percentage of Sales Estimated Uncollectible × Actual Credit Sales |

| Percentage of Receivables | Percentage of Outstanding Receivables Estimated Uncollectible × Receivables Balance |

| Aging Schedule | Percentage of Outstanding Receivables Estimated Uncollectible × Receivables Balance (for each aging bucket, summed) |

Based on data from previous years

Based on data from previous years

Maintaining consistency in the chosen method from year to year is crucial unless there’s a disclosed change in methods.

6. Minimizing Bad Debt Expense with Collaborative Accounts Receivable

Uncontrolled bad debt expenses can significantly impact a company’s profitability. Optimizing collections management is essential to minimizing these losses.

6.1. Collaborative AR Solutions

A collaborative accounts receivable solution, like Versapay, uses automation and cloud-based collaboration to align customers, sales, and AR teams. It enhances efficiency, accelerates cash flow, and significantly improves customer experience.

6.2. Benefits of Collaborative AR

-

More Transparent Communication: Facilitates clear communication between AR staff and customers, resolving issues like disputed invoice charges or missing remittance information.

-

Better Alignment Between Sales and AR: Provides sales teams with access to customer payment history, enabling more informed credit decisions.

-

Focus on Value-Added Work: Automates routine tasks, allowing AR teams to focus on strategic activities such as identifying causes of payment delays and understanding customer needs.

6.3. How Collaborative AR Minimizes Bad Debt

- Enhanced Communication: Collaborative AR streamlines communication, making it easier to address and resolve disputes. By offering a centralized platform for all interactions, it reduces misunderstandings and delays in payment. This leads to improved customer relationships and a reduced likelihood of non-payment.

- Improved Credit Decisions: Sales teams can access real-time payment data, allowing them to make better-informed decisions about credit terms. Understanding a customer’s payment behavior helps in setting appropriate credit limits and terms, which reduces the risk of extending credit to unreliable customers.

- Automated Processes: Automating invoicing, collections, payment processing, and cash application allows AR teams to focus on strategic tasks. This includes proactively addressing potential payment issues and engaging with customers to understand their needs and challenges.

6.4. Success Through Collaboration

Collaborative AR minimizes bad debt expense by fostering better customer relationships and reducing the likelihood of receivables becoming uncollectible. This approach not only improves financial outcomes but also strengthens customer loyalty.

7. Real-World Examples of Successful Partnerships

Several companies have successfully leveraged strategic partnerships to enhance their financial health and reduce bad debt. Here are a few notable examples:

7.1. Case Study 1: Technology Firm and Financial Institution

A technology firm partnered with a financial institution to offer flexible payment solutions to its customers. By providing financing options and payment plans, the technology firm reduced the risk of non-payment and improved customer satisfaction. The financial institution benefited from increased loan volume and access to a new customer base.

7.2. Case Study 2: Retail Chain and Marketing Agency

A retail chain collaborated with a marketing agency to improve customer engagement and loyalty. By implementing targeted marketing campaigns and personalized offers, the retail chain increased sales and reduced the likelihood of customers defaulting on payments. The marketing agency gained a valuable client and expanded its expertise in the retail sector.

7.3. Case Study 3: Manufacturing Company and Logistics Provider

A manufacturing company partnered with a logistics provider to streamline its supply chain and improve delivery times. By optimizing logistics and ensuring timely delivery, the manufacturing company reduced customer disputes and improved cash flow. The logistics provider secured a long-term contract and enhanced its reputation for reliability.

These examples highlight the potential of strategic partnerships to mitigate financial risks and drive business growth.

8. Actionable Strategies for Reducing Bad Debt

Implementing proactive strategies can significantly reduce bad debt and improve overall financial health.

8.1. Enhance Credit Policies

Develop clear and consistent credit policies that outline payment terms, credit limits, and collection procedures. Ensure that all customers are aware of these policies and that they are consistently enforced.

8.2. Improve Communication

Foster open and transparent communication with customers to address any concerns or disputes promptly. Provide multiple channels for customers to reach out with questions or issues, and ensure that customer service representatives are well-trained to handle inquiries effectively.

8.3. Implement Early Payment Incentives

Offer discounts or other incentives to customers who pay their invoices early. This can encourage timely payments and reduce the risk of late or non-payment.

8.4. Monitor Accounts Receivable

Regularly monitor accounts receivable to identify potential issues early on. Track payment trends, aging balances, and customer credit limits to detect any red flags and take corrective action promptly.

8.5. Leverage Technology

Utilize accounts receivable automation software to streamline invoicing, collections, and payment processing. These tools can help improve efficiency, reduce errors, and enhance visibility into accounts receivable performance.

9. Seeking Expert Advice and Resources

Navigating the complexities of bad debt and strategic partnerships requires expertise and access to reliable resources.

9.1. Consulting Services

Consider engaging with financial consultants or business advisors who specialize in accounts receivable management and strategic partnerships. These professionals can provide valuable insights and guidance tailored to your specific business needs.

9.2. Industry Associations

Join industry associations and networks to connect with peers, share best practices, and stay informed about the latest trends and developments in accounts receivable management and strategic partnerships.

9.3. Online Resources

Explore online resources such as industry publications, webinars, and case studies to expand your knowledge and learn from the experiences of other companies.

9.4. Income-Partners.net

Visit income-partners.net for a wealth of information on strategic partnerships, revenue enhancement, and financial optimization. Our platform offers valuable resources and insights to help you achieve your business goals.

10. Frequently Asked Questions (FAQs) About Bad Debt Expense

-

What is bad debt expense?

Bad debt expense is the portion of a company’s accounts receivable that is considered uncollectible and is written off as an expense. -

Where does bad debt expense appear on the income statement?

It is typically listed under Sales, General, and Administrative expenses (SG&A). -

Why is it important to record bad debt expense?

Recording bad debt expense provides a more accurate representation of a company’s financial health by reducing the value of accounts receivable on the balance sheet. -

What accounting method requires recording bad debt expense?

The accrual accounting method requires recording bad debt expense, as it recognizes revenue when earned, not when cash is received. -

What are the two methods to record bad debt expense?

The two methods are the direct write-off method and the allowance method. -

What is the direct write-off method?

The direct write-off method involves writing off a specific uncollectible account directly to bad debt expense when it is deemed uncollectible. -

What is the allowance method?

The allowance method involves estimating uncollectible accounts at the end of an accounting period and creating an allowance for doubtful accounts. -

What are the common methods for estimating bad debt expense under the allowance method?

The methods include the percentage of sales, percentage of accounts receivable, and accounts receivable aging. -

How does collaborative accounts receivable minimize bad debt expense?

Collaborative AR improves communication, aligns sales and AR teams, and automates routine tasks, allowing for more strategic focus on customer relationships and collection efforts. -

What steps can a company take to reduce bad debt expense?

Companies can enhance credit policies, improve communication, implement early payment incentives, monitor accounts receivable, and leverage technology.

Bad debt expense is a critical metric for evaluating financial health and collection effectiveness. It reflects the quality of customer relationships and the efficiency of accounts receivable management. Understanding and effectively managing bad debt expense can lead to improved profitability and sustainable business growth.

Ready to Transform Your Approach to Partnerships?

Don’t let uncollected debts hinder your business growth. Visit income-partners.net today to discover how strategic partnerships can enhance your financial health and drive revenue. Explore our resources, connect with potential partners, and start building a more prosperous future. Take the first step towards financial success by exploring the opportunities that await you at income-partners.net.

Address: 1 University Station, Austin, TX 78712, United States.

Phone: +1 (512) 471-3434.

Website: income-partners.net.