Navigating tax season can feel like decoding a secret language, especially when it comes to understanding your W-2 form. If you’re asking, “Where do I find my gross income on my W-2?” you’re not alone. At income-partners.net, we help you decipher your W-2 and understand how to calculate your gross income, empowering you to make informed financial decisions and explore potential income-boosting partnerships. Let’s explore how to find this number and what it signifies for your overall financial picture, including exploring partnership opportunities, income streams, and strategic alliances.

1. What Exactly Is a W-2 Form and Why Is It Important?

A W-2 form, officially known as the “Wage and Tax Statement,” is a crucial document you receive from your employer each year. It summarizes your earnings and the total taxes withheld from your paycheck during the year. Understanding your W-2 is vital for accurately filing your taxes, claiming deductions, and planning your financial future. It’s not just a piece of paper; it’s a key to understanding your income and tax obligations.

1.1. Key Components of a W-2 Form

The W-2 form contains several boxes, each providing specific information about your earnings and taxes. Here’s a breakdown of the most important ones:

- Box 1: Federal Income Tax Withheld: This shows the total amount of federal income tax withheld from your paychecks.

- Box 2: Social Security Tax Withheld: This displays the amount of Social Security tax withheld.

- Box 3: Medicare Tax Withheld: This indicates the amount of Medicare tax withheld.

- Box 5: State Income Tax Withheld: This shows the total amount of state income tax withheld (if applicable).

- Box 15: Employer’s State ID Number: This is the state identification number assigned to your employer.

- Boxes 12a through 12d: These boxes report various types of compensation and benefits, such as 401(k) contributions, health savings account (HSA) contributions, and other pre-tax deductions.

1.2. Why Accuracy Matters

Ensuring the accuracy of your W-2 is paramount. Errors can lead to delays in processing your tax return, potential audits, and incorrect tax liabilities. Always compare your W-2 with your own payroll records or pay stubs to verify the information. If you spot a discrepancy, promptly contact your employer’s payroll department to request a corrected form (W-2c). According to the Internal Revenue Service (IRS), it is your responsibility to ensure that the information on your tax return matches the information reported on your W-2.

1.3. W-2 and Financial Planning

Beyond tax filing, your W-2 is a valuable tool for financial planning. It provides a clear snapshot of your annual income, allowing you to track your earnings, budget effectively, and set financial goals. Understanding your income also opens doors to exploring various income-boosting opportunities, such as side hustles, investments, and strategic partnerships. At income-partners.net, we provide resources and connections to help you leverage your income and explore new avenues for financial growth.

2. Decoding Gross Income: What It Really Means

Gross income is your total earnings before any deductions for taxes, benefits, or other withholdings. It’s the initial figure that represents your compensation from your employer. Understanding your gross income is essential because it serves as the baseline for calculating your taxable income and determining your overall financial health.

2.1. Gross Income vs. Net Income

It’s important to differentiate between gross income and net income. Gross income is your earnings before deductions, while net income (or “take-home pay”) is what remains after taxes, insurance premiums, retirement contributions, and other deductions are subtracted. While net income reflects your immediate spending power, gross income provides a more comprehensive view of your earning potential.

2.2. Why Gross Income Matters

Gross income plays a significant role in various financial calculations and decisions:

- Tax Planning: Your gross income is used to determine your eligibility for certain tax deductions and credits.

- Loan Applications: Lenders often use gross income to assess your ability to repay loans, such as mortgages or auto loans.

- Financial Planning: Understanding your gross income helps you create realistic budgets, set financial goals, and track your progress.

- Investment Strategies: Knowing your gross income can influence your investment decisions, as it provides insight into your capacity to save and invest.

2.3. Impact on Financial Opportunities

Your gross income level can significantly impact the types of financial opportunities available to you. Higher gross income may qualify you for better interest rates on loans, access to premium investment products, and opportunities to explore more sophisticated financial strategies. At income-partners.net, we help you understand how your income level can unlock new possibilities for financial growth and partnership opportunities.

3. The Tricky Part: Why Gross Income Isn’t Directly on Your W-2

You might expect to find your gross income clearly labeled on your W-2, but it’s not always the case. The W-2 primarily reports taxable wages, which are your gross income minus certain pre-tax deductions. This can be confusing, but there’s a logical reason for it: the IRS is primarily concerned with the income that is subject to taxation.

3.1. Understanding Taxable Wages

Taxable wages are the portion of your income that is subject to federal, state, and local income taxes. These wages are calculated by subtracting pre-tax deductions from your gross income. Common pre-tax deductions include:

- 401(k) Contributions: Contributions to a traditional 401(k) retirement plan are deducted from your gross income before taxes are calculated.

- Health Insurance Premiums: If you pay for health insurance premiums on a pre-tax basis, these amounts are deducted from your gross income.

- Flexible Spending Account (FSA) Contributions: Contributions to an FSA for medical or dependent care expenses are also deducted pre-tax.

- Health Savings Account (HSA) Contributions: Similar to FSAs, HSA contributions are deducted from your gross income.

- Commuter Benefits: Pre-tax deductions for transportation expenses, such as public transit or parking, reduce your taxable wages.

3.2. The Exception to the Rule

In rare cases, your gross income might match the amount reported in Box 1 (Federal Wages) of your W-2. This occurs only if you have no pre-tax deductions. For most employees, however, pre-tax deductions are common, making it necessary to calculate gross income using the methods described below.

3.3. IRS Perspective

The IRS focuses on taxable income because that’s what determines your tax liability. While gross income is a valuable metric for personal financial planning, it’s not the primary figure used for tax calculations. Understanding this distinction is crucial for navigating your W-2 and accurately reporting your income.

4. Step-by-Step Guide: Calculating Your Gross Income from Your W-2

While your gross income isn’t explicitly stated on your W-2, you can easily calculate it using the information provided. Here’s a step-by-step guide to help you determine your gross income:

4.1. The Basic Formula

The fundamental formula for calculating gross income from your W-2 is:

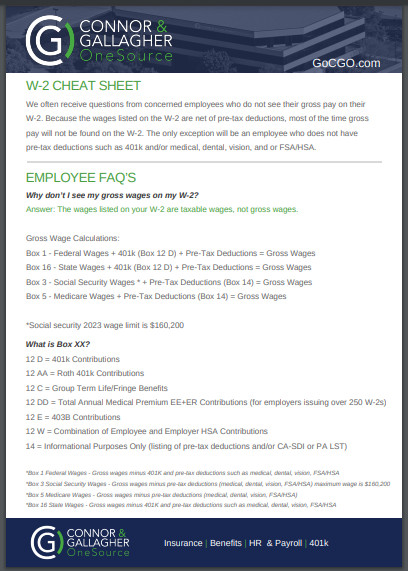

Gross Income = Box 1 (Federal Wages) + Total Pre-Tax Deductions

4.2. Identifying Pre-Tax Deductions

Locate Box 12 on your W-2. This section reports various types of compensation and benefits, including pre-tax deductions. Common codes you might find in Box 12 include:

- Code D: 401(k) contributions

- Code E: 403(b) contributions

- Code DD: Total cost of employer-sponsored health coverage

- Code W: Health Savings Account (HSA) contributions

For each code, note the corresponding amount reported in the adjacent box.

4.3. Summing Up Pre-Tax Deductions

Add up all the amounts reported in Box 12 that represent pre-tax deductions. For example, if you have contributions to a 401(k) (Code D) and an HSA (Code W), you would add those two amounts together.

4.4. Calculating Gross Income

Add the total pre-tax deductions you calculated in the previous step to the amount reported in Box 1 (Federal Wages). The result is your gross income for the year.

Example:

- Box 1 (Federal Wages): $60,000

- Box 12, Code D (401(k) contributions): $5,000

- Box 12, Code W (HSA contributions): $2,000

Gross Income = $60,000 + $5,000 + $2,000 = $67,000

4.5. Alternative Calculation Methods

You can also use other boxes on your W-2 to verify your gross income calculation:

- State Wages (Box 16): Similar to Box 1, Box 16 reports your state wages, which are also net of pre-tax deductions. You can add pre-tax deductions to this amount to estimate your gross income.

- Social Security Wages (Box 3) and Medicare Wages (Box 5): These boxes report wages subject to Social Security and Medicare taxes, respectively. Adding pre-tax deductions to these amounts can also provide an estimate of your gross income. Keep in mind that Social Security wages are subject to an annual limit ($160,200 in 2023), so this method may not be accurate for high-income earners.

4.6. Accuracy Checks

To ensure the accuracy of your calculation, compare your estimated gross income with your pay stubs or payroll records. Your pay stubs should show your gross income for each pay period, as well as all deductions. Multiplying your gross income per pay period by the number of pay periods in the year should give you a similar result to the calculation based on your W-2.

W-2 Cheat Sheet

W-2 Cheat Sheet

5. Understanding Box 12 Codes: A Comprehensive Guide

Box 12 of your W-2 is a treasure trove of information about various types of compensation, benefits, and deductions. Each item is identified by a specific code, which can seem like alphabet soup at first glance. Understanding these codes is essential for accurately calculating your gross income and understanding your overall compensation package.

5.1. Common Box 12 Codes and Their Meanings

Here’s a breakdown of some of the most common Box 12 codes you might encounter:

| Code | Description | Significance |

|---|---|---|

| A | Uncollected Social Security or RRTA tax on tips | Indicates that your employer was unable to collect the full amount of Social Security or Railroad Retirement Tax Act (RRTA) tax on your tips. |

| B | Uncollected Medicare tax on tips | Indicates that your employer was unable to collect the full amount of Medicare tax on your tips. |

| C | Taxable cost of group-term life insurance over $50,000 | Represents the taxable value of employer-provided group-term life insurance coverage exceeding $50,000. |

| D | Elective deferrals to a 401(k) cash or deferred arrangement | Indicates the amount you contributed to a traditional 401(k) plan. |

| E | Elective deferrals to a 403(b) tax-sheltered annuity | Indicates the amount you contributed to a 403(b) plan, which is common for employees of non-profit organizations and schools. |

| F | Elective deferrals to a 408(k)(6) SEP plan | Indicates the amount you contributed to a Simplified Employee Pension (SEP) plan. |

| G | Elective deferrals and employer contributions (including non-elective deferrals) to a 457(b) deferred compensation plan | Indicates contributions to a 457(b) plan, which is common for employees of state and local governments. |

| H | Elective deferrals to a 501(c)(18)(D) tax-exempt organization plan | Indicates contributions to a specific type of tax-exempt organization plan. |

| AA | Roth 401(k) contributions | Indicates the amount you contributed to a Roth 401(k) plan. |

| BB | Roth 403(b) contributions | Indicates the amount you contributed to a Roth 403(b) plan. |

| DD | Cost of employer-sponsored health coverage | Represents the total cost of employer-sponsored health coverage, including both your contributions and your employer’s contributions. |

| EE | Designated Roth contributions under a section 457(b) plan | Indicates Roth contributions to a 457(b) plan. |

| FF | Permitted benefits under a qualified cash or deferred arrangement or CODA | Indicates certain benefits under a qualified cash or deferred arrangement. |

| GG | Aggregate deferrals under section 402(g) exceed $20,500 | Indicates that your total elective deferrals exceeded the annual limit. |

| HH | Aggregate deferrals under section 402(g) exceed $20,500 | Indicates that your total elective deferrals exceeded the annual limit. |

| W | Employer contributions to a health savings account (HSA) | Indicates the amount your employer contributed to your HSA. |

5.2. How Box 12 Codes Affect Gross Income Calculation

When calculating your gross income, it’s essential to include any pre-tax deductions reported in Box 12. Common pre-tax deductions that should be added back to Box 1 wages include contributions to traditional 401(k) plans (Code D), 403(b) plans (Code E), and health savings accounts (Code W). Roth contributions (Codes AA and BB) are not pre-tax deductions, so they should not be included in the gross income calculation.

5.3. Deciphering Complex Scenarios

In some cases, your W-2 might include multiple entries in Box 12, or the descriptions might be unclear. If you’re unsure about the meaning of a particular code or how it affects your gross income calculation, consult with your employer’s payroll department or a tax professional. They can provide clarification and ensure that you’re accurately reporting your income.

6. Common Mistakes to Avoid When Calculating Gross Income

Calculating your gross income from your W-2 seems straightforward, but it’s easy to make errors if you’re not careful. Avoiding these common mistakes can save you time, prevent inaccuracies on your tax return, and ensure you have a clear understanding of your financial situation.

6.1. Overlooking Pre-Tax Deductions

One of the most frequent errors is failing to account for all pre-tax deductions. Be sure to carefully review Box 12 of your W-2 and include all relevant codes and amounts in your calculation.

6.2. Including Post-Tax Deductions

It’s important to distinguish between pre-tax and post-tax deductions. Only pre-tax deductions should be added back to Box 1 wages when calculating gross income. Post-tax deductions, such as Roth 401(k) contributions or after-tax contributions to a health savings account, should not be included.

6.3. Misinterpreting Box 12 Codes

Box 12 codes can be confusing, and misinterpreting them can lead to inaccurate calculations. If you’re unsure about the meaning of a particular code, consult with your employer’s payroll department or a tax professional.

6.4. Ignoring Other Income Sources

Your W-2 only reports income from your employer. If you have other sources of income, such as self-employment income, investment income, or rental income, you’ll need to account for those separately when calculating your total gross income for the year.

6.5. Not Reconciling with Pay Stubs

To ensure accuracy, it’s always a good idea to reconcile your W-2 with your pay stubs or payroll records. Your pay stubs should show your gross income for each pay period, as well as all deductions. Comparing these records can help you identify any discrepancies and ensure that you’re accurately reporting your income.

7. The Role of Gross Income in Strategic Partnership Planning

Understanding your gross income is not just about taxes; it’s also a critical factor in planning strategic partnerships. Your income level can influence the types of partnerships you pursue, the resources you can invest, and the potential returns you can expect.

7.1. Assessing Your Financial Capacity

Your gross income provides a clear picture of your financial capacity, which is essential when evaluating potential partnership opportunities. It helps you determine how much capital you can invest, the level of risk you can tolerate, and the resources you can dedicate to the partnership.

7.2. Identifying Complementary Partners

Knowing your income level can also help you identify complementary partners. For example, if you have a high income but limited time, you might seek partners who can provide the time and expertise you lack. Conversely, if you have limited income but valuable skills or resources, you might look for partners who can provide financial backing.

7.3. Negotiating Partnership Terms

Your gross income can also influence the terms of your partnership agreement. Partners with higher incomes may be able to negotiate more favorable terms, such as a larger share of the profits or greater control over decision-making.

7.4. Leveraging Income-Boosting Partnerships

Strategic partnerships can be a powerful way to boost your income and achieve your financial goals. By collaborating with others who have complementary skills, resources, or networks, you can create new income streams, expand your business, and accelerate your financial growth.

7.5. Finding Partnership Opportunities at income-partners.net

At income-partners.net, we connect individuals with diverse backgrounds and income levels to create mutually beneficial partnerships. Whether you’re looking for a strategic alliance, a joint venture, or a simple referral partnership, we can help you find the right fit. Our platform provides resources and tools to help you identify potential partners, assess their suitability, and negotiate partnership agreements that align with your financial goals.

Address: 1 University Station, Austin, TX 78712, United States. Phone: +1 (512) 471-3434. Website: income-partners.net.

8. Maximizing Income Through Strategic Alliances

Strategic alliances can be a game-changer when it comes to maximizing your income. These partnerships involve collaborating with other businesses or individuals to achieve shared goals, such as increasing revenue, expanding market reach, or developing new products or services.

8.1. Identifying Synergistic Opportunities

The key to a successful strategic alliance is identifying synergistic opportunities where the combined efforts of the partners create greater value than they could achieve individually. This might involve partnering with a company that has a complementary product or service, a strong distribution network, or access to a new market.

8.2. Types of Strategic Alliances

There are various types of strategic alliances, each with its own advantages and disadvantages:

- Joint Ventures: In a joint venture, two or more companies pool their resources to create a new entity that pursues a specific project or business opportunity.

- Marketing Alliances: Marketing alliances involve collaborating on marketing campaigns, cross-promotions, or co-branded products to reach a wider audience.

- Technology Alliances: Technology alliances involve sharing technology, intellectual property, or research and development resources to create new innovations.

- Supply Chain Alliances: Supply chain alliances involve collaborating on supply chain management, logistics, or procurement to reduce costs and improve efficiency.

8.3. Benefits of Strategic Alliances

Strategic alliances can offer numerous benefits, including:

- Increased Revenue: By combining resources and expertise, partners can generate more revenue than they could achieve individually.

- Expanded Market Reach: Alliances can provide access to new markets, customers, and distribution channels.

- Reduced Costs: Sharing resources and expertise can lower costs and improve efficiency.

- Innovation: Collaborating on research and development can lead to new products, services, and technologies.

- Risk Mitigation: Sharing risks and rewards can reduce the financial burden on each partner.

8.4. Building Successful Alliances

To build a successful strategic alliance, it’s important to:

- Clearly Define Goals: Establish clear goals and objectives for the alliance.

- Choose the Right Partners: Select partners who have complementary skills, resources, and values.

- Establish Clear Roles and Responsibilities: Define each partner’s roles, responsibilities, and contributions.

- Create a Formal Agreement: Develop a formal agreement that outlines the terms of the alliance, including profit sharing, decision-making, and dispute resolution.

- Communicate Effectively: Maintain open and transparent communication between partners.

8.5. income-partners.net: Your Gateway to Strategic Alliances

income-partners.net is your go-to resource for finding and building strategic alliances. Our platform connects you with potential partners who have the skills, resources, and networks you need to achieve your income goals. We provide tools and resources to help you identify synergistic opportunities, assess potential partners, and negotiate alliance agreements that align with your financial objectives.

9. Unlocking Passive Income Streams Through Partnerships

Passive income is income that requires minimal effort to earn and maintain. It’s a powerful way to build wealth and achieve financial freedom. Partnerships can be an excellent way to create passive income streams, allowing you to leverage the skills, resources, and networks of others.

9.1. Types of Passive Income Partnerships

There are several types of partnerships that can generate passive income:

- Affiliate Marketing Partnerships: In an affiliate marketing partnership, you promote another company’s products or services and earn a commission on each sale generated through your unique referral link.

- Real Estate Partnerships: Real estate partnerships involve investing in rental properties with other individuals. You can earn passive income from rental income, while your partners handle property management and maintenance.

- Content Creation Partnerships: Content creation partnerships involve collaborating with other creators to produce and distribute content, such as blog posts, videos, or podcasts. You can earn passive income from advertising revenue, sponsorships, or affiliate marketing.

- Licensing Partnerships: Licensing partnerships involve granting another company the right to use your intellectual property, such as a patent, trademark, or copyright. You can earn passive income from royalties or licensing fees.

9.2. Benefits of Passive Income Partnerships

Passive income partnerships offer numerous benefits:

- Diversification: Passive income streams can diversify your income and reduce your reliance on a single source of income.

- Scalability: Passive income streams can be scaled up without requiring significant additional effort.

- Flexibility: Passive income streams provide greater flexibility and freedom in your work life.

- Wealth Building: Passive income streams can accelerate your wealth building and help you achieve financial independence.

9.3. Finding the Right Passive Income Partnerships

To find the right passive income partnerships, it’s important to:

- Identify Your Interests and Skills: Choose partnerships that align with your interests and skills.

- Research Potential Partners: Research potential partners to ensure they are reputable and reliable.

- Evaluate the Potential for Passive Income: Assess the potential for passive income based on the market demand, commission rates, or royalty fees.

- Establish Clear Agreements: Establish clear agreements that outline the terms of the partnership, including profit sharing, responsibilities, and dispute resolution.

9.4. income-partners.net: Your Partner in Passive Income

income-partners.net is your trusted resource for finding and building passive income partnerships. Our platform connects you with potential partners who have the skills, resources, and networks you need to generate passive income streams. We provide tools and resources to help you identify lucrative opportunities, assess potential partners, and negotiate partnership agreements that align with your financial goals.

10. Expanding Business Reach Through Collaborative Ventures

Collaborative ventures are partnerships where businesses pool their resources, expertise, and networks to achieve a shared objective, such as expanding market reach, developing new products or services, or entering new geographic areas. These ventures can be a powerful way to accelerate growth and achieve greater success than businesses could achieve individually.

10.1. Types of Collaborative Ventures

There are various types of collaborative ventures:

- Joint Marketing Ventures: Joint marketing ventures involve collaborating on marketing campaigns, cross-promotions, or co-branded products to reach a wider audience and increase brand awareness.

- Joint Product Development Ventures: Joint product development ventures involve collaborating on the development of new products or services, sharing technology, intellectual property, or research and development resources.

- Joint Distribution Ventures: Joint distribution ventures involve collaborating on distribution channels, logistics, or supply chain management to reach new markets and reduce costs.

- Strategic Alliances: Strategic alliances are broader partnerships that involve collaborating on various aspects of the business, such as marketing, product development, or distribution.

10.2. Benefits of Collaborative Ventures

Collaborative ventures offer numerous benefits:

- Increased Market Reach: Ventures can provide access to new markets, customers, and distribution channels.

- Enhanced Innovation: Collaborating on research and development can lead to new products, services, and technologies.

- Reduced Costs: Sharing resources and expertise can lower costs and improve efficiency.

- Risk Mitigation: Sharing risks and rewards can reduce the financial burden on each partner.

- Competitive Advantage: Ventures can provide a competitive advantage by combining the strengths of multiple businesses.

10.3. Identifying the Right Ventures

To identify the right collaborative ventures, it’s important to:

- Define Your Objectives: Establish clear objectives for the venture, such as expanding market reach, developing new products, or reducing costs.

- Assess Your Strengths and Weaknesses: Identify your business’s strengths and weaknesses to determine what you can contribute to the venture and what you need from a partner.

- Research Potential Partners: Research potential partners to ensure they have complementary skills, resources, and values.

- Evaluate the Potential for Success: Assess the potential for success based on market demand, competition, and the partners’ ability to work together effectively.

10.4. income-partners.net: Your Partner in Expansion

income-partners.net is your trusted resource for finding and building collaborative ventures that expand your business reach. Our platform connects you with potential partners who have the skills, resources, and networks you need to achieve your growth objectives. We provide tools and resources to help you identify synergistic opportunities, assess potential partners, and negotiate venture agreements that align with your business goals.

Unlocking your income potential through strategic partnerships is within reach. Discover the possibilities at income-partners.net today.

FAQ: Finding Your Gross Income on Your W-2

Here are some frequently asked questions about finding your gross income on your W-2 form:

1. Is my gross income listed directly on my W-2?

No, your gross income is not directly listed on your W-2 form. The W-2 primarily reports taxable wages, which are your gross income minus certain pre-tax deductions.

2. Where can I find my taxable wages on my W-2?

Your taxable wages are reported in Box 1 of your W-2 form, labeled as “Federal Wages.”

3. What are pre-tax deductions, and how do they affect my gross income calculation?

Pre-tax deductions are amounts deducted from your gross income before taxes are calculated. Common examples include contributions to traditional 401(k) plans, health insurance premiums, and health savings account (HSA) contributions. To calculate your gross income, you need to add back these pre-tax deductions to your taxable wages (Box 1).

4. How do I find my pre-tax deductions on my W-2?

Pre-tax deductions are typically reported in Box 12 of your W-2, with specific codes indicating the type of deduction. Common codes include “D” for 401(k) contributions, “E” for 403(b) contributions, and “W” for HSA contributions.

5. What is the formula for calculating gross income from my W-2?

The formula for calculating gross income from your W-2 is: Gross Income = Box 1 (Federal Wages) + Total Pre-Tax Deductions.

6. What should I do if I have multiple entries in Box 12 of my W-2?

If you have multiple entries in Box 12, add up all the amounts that represent pre-tax deductions. Then, add the total to the amount reported in Box 1 to calculate your gross income.

7. Are Roth 401(k) contributions pre-tax deductions?

No, Roth 401(k) contributions are not pre-tax deductions. They are made with after-tax dollars, so they should not be included in the gross income calculation.

8. How can I verify the accuracy of my gross income calculation?

To verify the accuracy of your gross income calculation, compare your estimated gross income with your pay stubs or payroll records. Your pay stubs should show your gross income for each pay period, as well as all deductions.

9. What should I do if I find an error on my W-2?

If you find an error on your W-2, promptly contact your employer’s payroll department to request a corrected form (W-2c).

10. Where can I find more information about W-2 forms and gross income calculations?

You can find more information about W-2 forms and gross income calculations on the IRS website or by consulting with a tax professional. Additionally, income-partners.net offers resources and tools to help you understand your W-2 and explore income-boosting partnership opportunities.

Ready to take control of your income and explore exciting partnership opportunities? Visit income-partners.net today and start building your financial future!