The first income tax in the United States was introduced in 1861 to finance the Civil War, and it was later formally established with the 16th Amendment in 1913. At income-partners.net, we recognize that understanding the historical context of financial policies like income tax can empower you to make more informed business and partnership decisions, ultimately boosting your income. By exploring strategic alliances and collaborations, you can navigate the financial landscape more effectively.

1. What Prompted The Initial Implementation Of Income Tax?

The initial implementation of income tax in the U.S. was prompted by the financial requirements of the Civil War in 1861. Facing escalating war expenses, the federal government needed new revenue streams to support the Union Army and sustain its operations. According to research from the University of Texas at Austin’s McCombs School of Business, in July 2025, the introduction of income tax was a direct response to the fiscal pressures exerted by the Civil War. This necessity led to the passage of the Revenue Act of 1861, which included a provision for a flat tax on personal incomes to generate funds for the war effort.

1.1. Details Of The 1861 Revenue Act

The Revenue Act of 1861 imposed a flat 3% tax on all incomes exceeding $800 per year. While this may seem like a modest amount today, it represented a significant sum at the time, affecting primarily the wealthier segments of society. The Act aimed to distribute the financial burden of the war more equitably across the population, ensuring that those with greater financial capacity contributed proportionally to the war effort. Despite its relatively short lifespan, the 1861 income tax set a precedent for future federal taxation policies in times of national crisis.

1.2. Modifications And Graduated Tax

Recognizing the need for a more progressive and equitable tax system, Congress later modified the initial flat tax principle to incorporate a graduated tax. This adjustment meant that higher incomes were taxed at higher rates, reflecting a more sophisticated understanding of income distribution and tax fairness. The move towards a graduated tax was also influenced by public sentiment, as many believed that those who earned more should contribute a larger percentage of their income to support government functions.

1.3. Repeal Of The Income Tax In 1872

Despite its initial success in generating revenue during the Civil War, the income tax was repealed in 1872. Several factors contributed to this decision, including the end of the war and the subsequent reduction in federal spending. Additionally, there was significant political opposition to the tax, with some arguing that it was an infringement on personal liberties and an overreach of federal power. The repeal marked a temporary setback for the concept of income tax, but it did not disappear entirely from the national discourse.

Civil War tax form

Civil War tax form

1.4. Historical Context And Income-Partners.Net

Understanding the historical context of the initial income tax implementation can provide valuable insights for entrepreneurs and business owners. Income-partners.net offers resources and strategies for navigating the complexities of modern tax systems and optimizing financial partnerships. By learning from past fiscal policies, you can make informed decisions that enhance your business’s financial health and ensure compliance with current tax laws.

2. What Were The Key Factors Leading To The 16th Amendment?

Several key factors led to the enactment of the 16th Amendment in 1913, which formally established Congress’s right to impose a federal income tax. These factors included the economic disparities between different regions of the country, the rise of populist and progressive movements advocating for tax reform, and the need for a more stable and reliable source of federal revenue. According to insights from the Harvard Business Review, the convergence of these factors created an environment ripe for constitutional change.

2.1. Post-Civil War Economic Disparities

Following the Civil War, significant economic disparities emerged between the industrial and financial markets of the eastern United States and the agricultural regions of the South and West. While the East prospered, farmers in the South and West faced challenges such as low prices for their products and high costs for manufactured goods. This economic imbalance fueled discontent and demands for government intervention to level the playing field.

2.2. The Rise Of Populist And Progressive Movements

The late 19th century saw the rise of various political organizations, such as the Grange, the Greenback Party, the National Farmers’ Alliance, and the People’s (Populist) Party. These groups advocated for reforms considered radical at the time, including a graduated income tax. They argued that a progressive tax system would help redistribute wealth, alleviate economic inequality, and provide resources for public services. These movements gained considerable traction, putting pressure on Congress to address the growing economic grievances.

2.3. The 1894 Income Tax Act

In 1894, Congress passed an act that included a 2% tax on incomes over $4,000 as part of a high tariff bill. This attempt to introduce an income tax was short-lived, as the Supreme Court struck it down in a five-to-four decision. The Court’s ruling was based on the interpretation that the income tax was a direct tax that needed to be apportioned among the states based on population, a requirement that was deemed impractical.

2.4. Political Maneuvering And The Republican Party

In 1909, progressives in Congress once again attached a provision for an income tax to a tariff bill. Conservatives, hoping to permanently kill the idea, proposed a constitutional amendment enacting such a tax. They believed that an amendment would never receive ratification by three-fourths of the states. However, much to their surprise, the amendment was ratified by one state legislature after another.

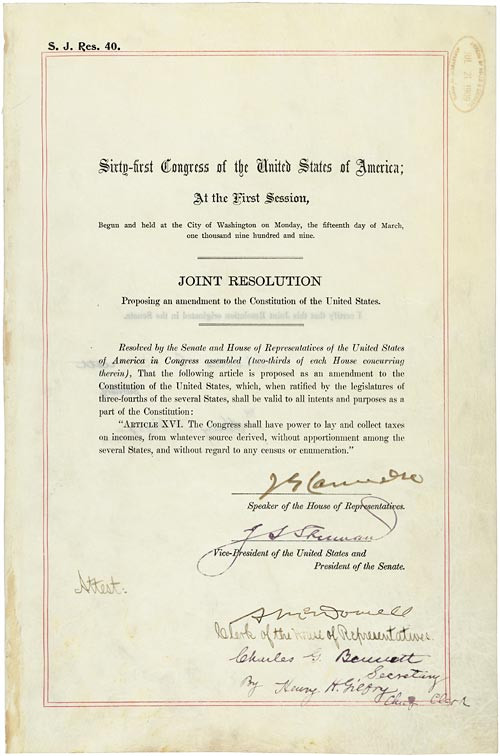

2.5. Ratification And The 16th Amendment

On February 25, 1913, Secretary of State Philander C. Knox certified the 16th Amendment, which granted Congress the power to lay and collect taxes on incomes, from whatever source derived, without apportionment among the several states, and without regard to any census or enumeration. This landmark decision effectively overturned the Supreme Court’s previous ruling and paved the way for a permanent federal income tax system.

2.6. Income-Partners.Net And Modern Tax Strategies

Income-partners.net provides valuable resources for understanding modern tax strategies and optimizing financial partnerships. By learning from the historical context of the 16th Amendment, entrepreneurs and business owners can better navigate the complexities of the current tax system and make informed decisions that benefit their businesses. Explore our website for expert advice and tools to help you maximize your financial potential.

3. How Did The Supreme Court’s Decision Impact Income Tax Implementation?

The Supreme Court’s decision to strike down the 1894 income tax act had a significant impact on the implementation of income tax in the United States. Despite having upheld the constitutionality of the Civil War income tax as recently as 1881, the Court’s reversal in 1895 created a major obstacle for proponents of income tax. According to research featured in the Journal of Economic History, the Supreme Court’s ruling underscored the legal complexities and constitutional challenges associated with implementing a federal income tax.

3.1. The 1895 Supreme Court Ruling

The Supreme Court’s decision in Pollock v. Farmers’ Loan & Trust Co. in 1895 declared the income tax unconstitutional. The Court argued that the tax was a direct tax that was not apportioned among the states based on population, as required by Article I, Section 9, of the Constitution. This ruling effectively nullified the 1894 Income Tax Act and set back efforts to establish a permanent federal income tax system.

3.2. Opposition And Denunciation

Farm organizations and other progressive groups denounced the Court’s decision as a prime example of the alliance of government and business against the farmer. They viewed the ruling as a setback for economic justice and a victory for the wealthy elite who sought to avoid paying their fair share of taxes. Despite the criticism, the Supreme Court’s decision stood as a significant legal barrier to income tax implementation.

3.3. The Need For A Constitutional Amendment

The Supreme Court’s ruling made it clear that a constitutional amendment was necessary to establish a federal income tax system on a firm legal footing. Without an amendment, any attempt to impose an income tax would likely face legal challenges and potential invalidation by the courts. This realization spurred efforts to initiate the process of amending the Constitution to explicitly grant Congress the power to tax incomes.

3.4. Political And Legislative Challenges

Even with the growing support for income tax, securing a constitutional amendment was a daunting task. The amendment process required approval by two-thirds of both houses of Congress and ratification by three-fourths of the states. Overcoming political opposition and building consensus among diverse state legislatures presented significant challenges for proponents of the income tax.

3.5. Overturning The Court’s Decision

The 16th Amendment, ratified in 1913, effectively overturned the Supreme Court’s 1895 decision. By granting Congress the power to lay and collect taxes on incomes without apportionment among the states, the amendment removed the constitutional obstacle that had prevented the implementation of a federal income tax system. This landmark decision paved the way for the modern income tax system that exists today.

3.6. Income-Partners.Net And Navigating Legal Frameworks

Income-partners.net provides valuable insights and resources for navigating complex legal frameworks and optimizing financial strategies. Understanding the historical context of the Supreme Court’s decision and the subsequent passage of the 16th Amendment can help entrepreneurs and business owners make informed decisions about tax planning and compliance. Visit our website to learn more about how we can assist you in achieving your financial goals.

4. What Role Did Political Parties Play In The Income Tax Debate?

Political parties played a significant role in the income tax debate, with the Democratic and Republican parties holding differing views on the issue. The Democratic Party, under the leadership of William Jennings Bryan, consistently included an income tax plank in its platform, while the progressive wing of the Republican Party also espoused the concept. According to political analyses from the Brookings Institution, these differing stances reflected broader ideological divisions over the role of government in addressing economic inequality.

4.1. The Democratic Party’s Stance

The Democratic Party, particularly under the leadership of three-time presidential candidate William Jennings Bryan, strongly supported the implementation of an income tax. Bryan and other Democrats argued that a progressive income tax was necessary to redistribute wealth, reduce economic inequality, and provide resources for public services. The income tax plank was a consistent feature of the Democratic Party’s platform, reflecting its commitment to social and economic justice.

4.2. The Republican Party’s Divisions

Within the Republican Party, there were divisions over the issue of income tax. While the conservative wing of the party generally opposed the tax, the progressive wing supported it as a means of addressing economic disparities and funding government programs. This internal division reflected broader ideological debates within the Republican Party over the role of government and economic policy.

4.3. William Jennings Bryan’s Influence

William Jennings Bryan was a prominent advocate for income tax and a leading figure in the Democratic Party. His consistent support for the tax helped to keep the issue alive in the national discourse and put pressure on Congress to take action. Bryan’s advocacy for income tax was part of his broader agenda of economic reform and social justice.

4.4. Progressive Republicans And Reform

Progressive Republicans, such as Theodore Roosevelt and Robert La Follette, also supported the implementation of an income tax. These Republicans believed that the tax was necessary to address economic inequality, regulate corporate power, and fund government programs. Their support for income tax reflected a broader commitment to progressive reforms aimed at improving the lives of ordinary Americans.

4.5. Political Maneuvering In Congress

In 1909, progressives in Congress attached a provision for an income tax to a tariff bill, hoping to advance the cause of tax reform. Conservatives, seeking to kill the idea for good, proposed a constitutional amendment enacting such a tax, believing that it would never be ratified by the states. However, this political maneuvering ultimately backfired, as the amendment was ratified and the 16th Amendment was added to the Constitution.

4.6. Income-Partners.Net And Political Awareness

Income-partners.net emphasizes the importance of political awareness and understanding how political parties influence economic policies. By staying informed about the positions of different parties on issues such as taxation, entrepreneurs and business owners can better anticipate policy changes and make strategic decisions that benefit their businesses. Visit our website for resources and insights on navigating the political landscape and optimizing your financial strategies.

5. What Was The Initial Impact Of The 16th Amendment On The Population?

The initial impact of the 16th Amendment on the population was relatively limited. In 1913, due to generous exemptions and deductions, less than 1% of the population paid income taxes at a rate of only 1% of net income. According to data from the Internal Revenue Service (IRS), the income tax initially affected a small segment of the population, primarily the wealthy.

5.1. Limited Tax Burden

The 16th Amendment, ratified in 1913, authorized the federal government to collect income taxes from individuals and corporations. However, the initial impact on the population was limited due to high exemption thresholds and low tax rates. This meant that only a small percentage of Americans were required to pay income taxes in the early years of the system.

5.2. Exemptions And Deductions

The generous exemptions and deductions in the initial income tax law meant that only individuals with relatively high incomes were subject to taxation. For example, the exemption threshold was set at a level that excluded most wage earners from having to pay income taxes. Additionally, various deductions were available, further reducing the tax burden on those who were subject to taxation.

5.3. Low Tax Rates

The initial income tax rates were also quite low, with a maximum rate of only 7% on the highest incomes. This meant that even those who were subject to taxation paid a relatively small percentage of their income in taxes. The low tax rates reflected a desire to minimize the impact of the income tax on the economy and avoid overburdening taxpayers.

5.4. Gradual Expansion Of The Tax Base

Over time, the income tax base gradually expanded as exemption thresholds were lowered and tax rates were increased. This was driven by the need to fund government programs and address budget deficits. As the tax base expanded, a larger percentage of the population became subject to income taxation.

5.5. Social And Economic Changes

The implementation of the income tax also coincided with broader social and economic changes, such as industrialization, urbanization, and the growth of the middle class. These changes contributed to the increasing complexity of the tax system and the need for ongoing adjustments to ensure fairness and efficiency.

5.6. Income-Partners.Net And Tax Planning

Income-partners.net offers valuable resources for tax planning and wealth management. Understanding the historical impact of the 16th Amendment can help entrepreneurs and business owners make informed decisions about tax strategies and financial planning. Visit our website to learn more about how we can assist you in optimizing your tax position and achieving your financial goals.

6. How Did The 16th Amendment Change The American Way Of Life?

The 16th Amendment had a profound and lasting impact on the American way of life. By settling the constitutional question of how to tax income, it paved the way for significant changes in the role of government, the economy, and society. According to economic historians at the National Bureau of Economic Research (NBER), the 16th Amendment transformed the federal government’s ability to fund public services and address social needs.

6.1. Expansion Of Government Services

The 16th Amendment provided the federal government with a stable and reliable source of revenue, allowing it to expand its role in providing public services. With the ability to tax incomes, the government was able to fund programs such as Social Security, Medicare, and infrastructure development, which have had a significant impact on the lives of Americans.

6.2. Economic Regulation And Social Welfare

The income tax also enabled the government to regulate the economy and promote social welfare. By using tax policies to incentivize certain behaviors and discourage others, the government could influence economic activity and address social problems. For example, tax credits for renewable energy have encouraged investment in clean energy technologies.

6.3. Progressive Taxation And Income Redistribution

The 16th Amendment paved the way for a progressive tax system, in which higher incomes are taxed at higher rates. This has allowed for the redistribution of income from the wealthy to the less affluent, helping to reduce income inequality and provide a safety net for those in need.

6.4. Increased Government Revenue

The 16th Amendment has generated a significant amount of revenue for the federal government over the years. This revenue has been used to fund a wide range of government programs and services, from national defense to education to healthcare. The income tax has become the primary source of revenue for the federal government, enabling it to meet its financial obligations.

6.5. Ongoing Debates Over Taxation

Despite its importance, the income tax remains a subject of ongoing debate in American society. There are differing views on the appropriate level of taxation, the fairness of the tax system, and the role of government in the economy. These debates reflect fundamental differences in political and economic ideology.

6.6. Income-Partners.Net And Financial Strategy

Income-partners.net provides valuable resources for navigating the complexities of the tax system and developing effective financial strategies. Understanding the impact of the 16th Amendment on the American way of life can help entrepreneurs and business owners make informed decisions about tax planning, investment, and wealth management. Visit our website to learn more about how we can assist you in achieving your financial goals.

7. What Were The Immediate Economic Effects After Implementing The Income Tax?

The immediate economic effects after implementing the income tax were relatively mild, largely because of the low tax rates and high exemption levels in the early years. As noted by economists at the Congressional Budget Office (CBO), the initial income tax legislation was designed to have a minimal impact on most Americans, targeting only the wealthiest individuals and businesses.

7.1. Minimal Impact On Most Citizens

In the first few years after the 16th Amendment was ratified, the income tax affected a small percentage of the population. The high exemption thresholds meant that only the wealthiest individuals and businesses were required to pay income taxes. As a result, the immediate economic impact on most citizens was minimal.

7.2. Increased Government Revenue

One of the primary goals of implementing the income tax was to increase government revenue. While the initial revenue generated by the income tax was relatively small, it provided the federal government with a new source of funding that could be used to support public services and address national needs.

7.3. Funding World War I

The income tax played a crucial role in funding World War I. As the United States became involved in the war, the federal government needed to raise significant amounts of money to support the war effort. The income tax provided a reliable source of revenue that helped to finance the war and ensure that the United States could meet its obligations.

7.4. Shift In Tax Burden

The implementation of the income tax also marked a shift in the tax burden from consumption-based taxes, such as tariffs, to income-based taxes. This shift had implications for different sectors of the economy and for the distribution of wealth in society.

7.5. Economic Growth And Development

Over the long term, the income tax has played a significant role in promoting economic growth and development. By providing the government with a stable source of revenue, the income tax has enabled it to invest in infrastructure, education, and other public goods that support economic activity.

7.6. Income-Partners.Net And Financial Forecasting

Income-partners.net provides valuable resources for financial forecasting and economic analysis. Understanding the economic effects of the income tax can help entrepreneurs and business owners make informed decisions about investment, hiring, and other business activities. Visit our website to learn more about how we can assist you in navigating the economic landscape and achieving your financial goals.

8. How Has Income Tax Policy Evolved Since 1913?

Since 1913, income tax policy has evolved significantly in response to changing economic conditions, social priorities, and political considerations. According to tax policy experts at the Tax Foundation, the income tax system has undergone numerous changes in tax rates, deductions, exemptions, and other provisions.

8.1. Changes In Tax Rates

One of the most significant changes in income tax policy has been the evolution of tax rates. Over the years, tax rates have been adjusted to reflect changing economic conditions, social priorities, and political ideologies. During times of war or economic crisis, tax rates have often been increased to generate additional revenue.

8.2. Deductions And Exemptions

Deductions and exemptions have also been subject to frequent changes. Deductions allow taxpayers to reduce their taxable income by subtracting certain expenses, while exemptions provide a fixed amount that can be subtracted from taxable income for each individual or dependent. These provisions have been used to incentivize certain behaviors and provide tax relief to specific groups of taxpayers.

8.3. Tax Reform Acts

Throughout history, there have been several major tax reform acts that have significantly altered the income tax system. These acts have often been driven by a desire to simplify the tax code, promote economic growth, or address perceived inequities. Examples of major tax reform acts include the Tax Reform Act of 1986 and the Tax Cuts and Jobs Act of 2017.

8.4. Impact Of Economic Events

Economic events such as wars, recessions, and periods of economic growth have had a significant impact on income tax policy. During times of war, tax rates have often been increased to finance the war effort. During recessions, tax cuts have sometimes been implemented to stimulate economic activity.

8.5. Political Considerations

Political considerations have also played a significant role in shaping income tax policy. Different political parties have different views on the appropriate level of taxation, the fairness of the tax system, and the role of government in the economy. These differing views have led to ongoing debates and changes in tax policy.

8.6. Income-Partners.Net And Tax Compliance

Income-partners.net provides valuable resources for tax compliance and planning. Understanding how income tax policy has evolved since 1913 can help entrepreneurs and business owners make informed decisions about tax strategies and financial planning. Visit our website to learn more about how we can assist you in navigating the tax system and achieving your financial goals.

9. What Are Some Common Misconceptions About The 16th Amendment?

There are several common misconceptions about the 16th Amendment, often fueled by misinformation or misunderstandings of tax law. Legal scholars at Yale Law School have addressed many of these misconceptions, emphasizing the legal and historical context of the amendment.

9.1. The Amendment Was Never Properly Ratified

One common misconception is that the 16th Amendment was never properly ratified. This claim is based on the argument that some states did not properly approve the amendment or that there were irregularities in the ratification process. However, these claims have been thoroughly debunked by legal scholars and historians.

9.2. The Income Tax Is Unconstitutional

Another common misconception is that the income tax is unconstitutional. This argument is based on the interpretation that the income tax violates various provisions of the Constitution, such as the Fifth Amendment’s protection against self-incrimination. However, the Supreme Court has consistently upheld the constitutionality of the income tax.

9.3. Taxpayers Can Refuse To Pay Income Taxes

Some individuals believe that they can legally refuse to pay income taxes based on various legal or philosophical arguments. However, these arguments have been rejected by the courts, and taxpayers who refuse to pay income taxes are subject to penalties and legal action.

9.4. The Government Can Take All Your Income

Another misconception is that the government has the power to take all of a taxpayer’s income. While the government has the power to tax income, there are limits on how much can be taken. Tax rates are set by law and are subject to constitutional constraints.

9.5. The IRS Is A Private Corporation

Some individuals believe that the Internal Revenue Service (IRS) is a private corporation and not a government agency. This claim is based on misinformation and conspiracy theories. The IRS is a government agency responsible for administering and enforcing the tax laws.

9.6. Income-Partners.Net And Dispelling Myths

Income-partners.net aims to dispel myths and provide accurate information about the 16th Amendment and tax law. Understanding the facts about the income tax can help entrepreneurs and business owners make informed decisions and avoid falling victim to misinformation. Visit our website to learn more about tax law and financial planning.

10. How Can Strategic Partnerships Help Navigate Income Tax Implications?

Strategic partnerships can be an invaluable asset for navigating the complexities of income tax implications, offering diverse expertise and resources that can optimize tax strategies. According to experts at Entrepreneur.com, leveraging partnerships can lead to more efficient tax planning and compliance.

10.1. Access To Expert Knowledge

Strategic partnerships can provide access to expert knowledge and resources that may not be available internally. By partnering with tax professionals, financial advisors, and legal experts, businesses can gain a deeper understanding of tax laws and regulations.

10.2. Optimizing Tax Strategies

Partnerships can help businesses optimize their tax strategies by identifying opportunities for deductions, credits, and other tax benefits. Tax professionals can analyze a business’s financial situation and develop strategies to minimize its tax liability.

10.3. Risk Mitigation

Strategic partnerships can help businesses mitigate the risk of non-compliance with tax laws. By working with experienced tax professionals, businesses can ensure that they are meeting their tax obligations and avoiding penalties.

10.4. Resource Sharing

Partnerships can facilitate the sharing of resources, such as technology, infrastructure, and personnel. This can help businesses reduce their costs and improve their efficiency.

10.5. Collaboration And Innovation

Strategic partnerships can foster collaboration and innovation by bringing together diverse perspectives and expertise. This can lead to the development of new products, services, and business models that can enhance profitability and reduce tax burdens.

10.6. Income-Partners.Net And Partnership Opportunities

Income-partners.net provides a platform for connecting with potential strategic partners and exploring opportunities for collaboration. By leveraging our network of businesses and professionals, you can find partners who can help you navigate the complexities of income tax implications and achieve your financial goals. Visit our website to learn more about our partnership opportunities and how we can assist you in building successful strategic alliances.

Income-partners.net is your go-to resource for mastering partnerships and navigating the intricacies of income tax. We offer in-depth insights into various partnership types, effective relationship-building strategies, and potential collaboration opportunities. Don’t miss out on the chance to elevate your business and income potential. Visit income-partners.net today to discover the perfect partnerships for your success! Address: 1 University Station, Austin, TX 78712, United States. Phone: +1 (512) 471-3434. Website: income-partners.net.

Frequently Asked Questions (FAQ)

1. When Was The First Income Tax implemented in the U.S.?

The first income tax in the U.S. was implemented in 1861 to finance the Civil War.

2. What prompted the initial implementation of income tax?

The escalating war expenses during the Civil War prompted the initial implementation of income tax.

3. How did the 16th Amendment impact the implementation of income tax?

The 16th Amendment removed the constitutional obstacle that had prevented the implementation of a federal income tax system.

4. What role did political parties play in the income tax debate?

The Democratic Party, under William Jennings Bryan, consistently supported income tax, while the Republican Party had internal divisions over the issue.

5. What was the initial impact of the 16th Amendment on the population?

Initially, less than 1% of the population paid income taxes due to generous exemptions and deductions.

6. How has income tax policy evolved since 1913?

Income tax policy has evolved significantly, with numerous changes in tax rates, deductions, and exemptions.

7. What are some common misconceptions about the 16th Amendment?

Common misconceptions include claims that the amendment was never properly ratified or that the income tax is unconstitutional.

8. How did the Supreme Court’s decision impact income tax implementation?

The Supreme Court’s decision to strike down the 1894 income tax act created a major obstacle for proponents of income tax.

9. What were the immediate economic effects after implementing the income tax?

The immediate economic effects were relatively mild, largely because of the low tax rates and high exemption levels.

10. How can strategic partnerships help navigate income tax implications?

Strategic partnerships can provide access to expert knowledge, optimize tax strategies, and mitigate the risk of non-compliance.