Federal income tax was created in 1913 with the ratification of the 16th Amendment, granting Congress the power to levy taxes on income. Understanding its origins and impact is crucial for navigating today’s financial landscape and identifying potential partnership opportunities. At income-partners.net, we offer strategies and resources to help you understand this critical aspect of the U.S. financial system and explore innovative approaches to increase your income and build strategic alliances, including tax-efficient strategies, wealth management and financial planning.

1. The Genesis of Federal Income Tax: Understanding its Inception

The federal income tax in the United States wasn’t always a permanent fixture. Its story is rooted in historical necessity, political maneuvering, and the evolving needs of a growing nation.

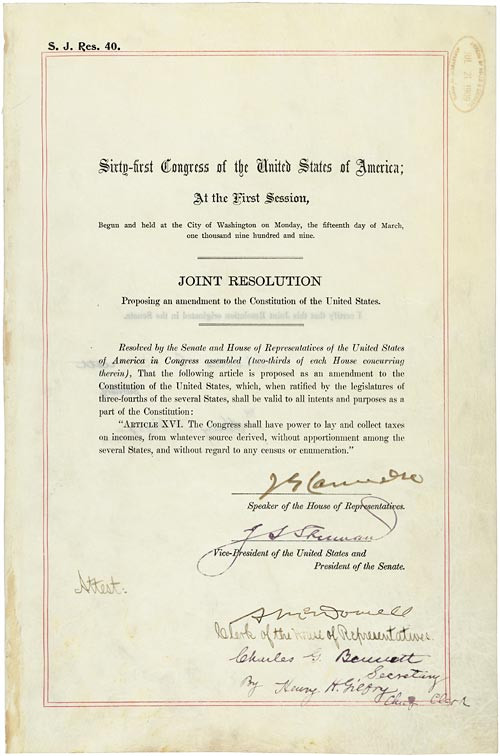

So, When Was Federal Income Tax Created? The answer lies in the ratification of the 16th Amendment to the U.S. Constitution in 1913. This amendment granted Congress the explicit power to levy and collect taxes on income, regardless of its source, without the need to apportion it among the states based on population.

The 16th Amendment, March 15, 1913; Ratified Amendments, 1795-1992; General Records of the United States Government; Record Group 11; National Archives.

The 16th Amendment, March 15, 1913; Ratified Amendments, 1795-1992; General Records of the United States Government; Record Group 11; National Archives.

1.1. A Look Back: Early Attempts at Income Tax

While the 16th Amendment marked the official establishment of federal income tax, it wasn’t the first time the U.S. government had experimented with this form of revenue generation.

- The Civil War Era: The first federal income tax was introduced during the Civil War in 1861 to finance the war effort. Congress imposed a flat 3% tax on incomes exceeding $800, later modifying it to include a graduated tax system. However, this tax was repealed in 1872 once the war’s financial demands subsided.

- The 1894 Tax Act: In 1894, Congress passed another income tax law, imposing a 2% tax on incomes over $4,000. Unfortunately, the Supreme Court swiftly struck down this act, deeming it unconstitutional.

1.2. The Road to the 16th Amendment

The need for a more stable and reliable source of federal revenue, coupled with growing public support for income tax, paved the way for the 16th Amendment.

- Populist Movement: The late 19th century witnessed the rise of the Populist movement, fueled by farmers and laborers who felt economically disadvantaged. They advocated for a graduated income tax to redistribute wealth and ease the financial burden on the working class.

- Progressive Era: The early 20th century saw the emergence of the Progressive Era, a period of social and political reform. Progressive leaders championed income tax as a means to fund social programs and regulate burgeoning industries.

- Political Maneuvering: In 1909, amidst debates over tariff legislation, Congress proposed a constitutional amendment authorizing income tax. Conservatives, believing it would never be ratified, surprisingly saw state legislatures across the nation ratify it, leading to its official adoption in 1913.

1.3. Initial Impact: A Gentle Start

Interestingly, in its early days, the federal income tax had a limited impact on the majority of Americans. Generous exemptions and deductions meant that less than 1% of the population actually paid income taxes in 1913, and even then, the rate was a mere 1% of net income.

2. The Enduring Legacy: Why Federal Income Tax Matters Today

The establishment of federal income tax through the 16th Amendment has had a profound and lasting impact on American society, shaping everything from government funding to economic policy.

2.1. Funding the Government:

Federal income tax is now the government’s largest single source of revenue, providing the financial backbone for essential public services and programs.

- Infrastructure: Taxes contribute significantly to the maintenance and development of roads, bridges, airports, and other critical infrastructure.

- Social Security and Medicare: A substantial portion of income tax revenue goes towards funding Social Security and Medicare, providing crucial benefits for retirees and those in need of medical care.

- National Defense: Taxes are essential for funding the military, protecting national security, and maintaining a strong defense force.

- Education: Federal income tax supports various educational programs, including grants, loans, and research initiatives.

2.2. Shaping Economic Policy:

The federal income tax system is a powerful tool for influencing economic activity and promoting social equity.

- Tax Incentives: The government can use tax incentives to encourage specific behaviors, such as investing in renewable energy, saving for retirement, or donating to charitable causes.

- Progressive Taxation: The progressive nature of the income tax system, where higher earners pay a larger percentage of their income in taxes, helps to reduce income inequality and fund social programs that benefit lower-income individuals and families.

- Economic Stabilization: During economic downturns, the government can use tax cuts or other tax-related measures to stimulate the economy and encourage spending and investment.

2.3. Navigating the Tax Landscape:

Understanding federal income tax is crucial for individuals and businesses alike.

- Tax Compliance: Filing taxes accurately and on time is a legal obligation. Understanding the tax code and available deductions and credits can help individuals and businesses minimize their tax liabilities.

- Financial Planning: Income tax considerations play a significant role in financial planning. Tax-advantaged investment accounts, such as 401(k)s and IRAs, can help individuals save for retirement while reducing their current tax burden.

- Business Decisions: Businesses must consider the tax implications of various decisions, such as choosing a business structure, investing in new equipment, or hiring employees.

3. Unveiling the Mechanics: How Federal Income Tax Works

The federal income tax system can seem complex, but understanding its basic mechanics can empower you to make informed financial decisions.

3.1. Taxable Income:

The first step in calculating your federal income tax is determining your taxable income, which is your adjusted gross income (AGI) less any deductions.

- Adjusted Gross Income (AGI): Your AGI is your gross income (wages, salaries, investment income, etc.) minus certain deductions, such as contributions to traditional IRAs, student loan interest payments, and self-employment taxes.

- Deductions: You can reduce your taxable income by claiming either the standard deduction or itemizing deductions. The standard deduction is a fixed amount that varies based on your filing status, while itemized deductions include expenses such as medical expenses, state and local taxes, and charitable contributions.

3.2. Tax Brackets and Rates:

The federal income tax system uses a progressive tax system, meaning that different portions of your income are taxed at different rates, according to tax brackets.

- Tax Brackets: Tax brackets are income ranges that are taxed at specific rates. For example, in 2023, the tax brackets for single filers ranged from 10% on income up to $10,950 to 37% on income over $578,125.

- Tax Rates: Each tax bracket is associated with a specific tax rate. Your income is taxed at the rate for the bracket it falls into. For example, if you are a single filer with a taxable income of $40,000, you would be taxed at 10% on the first $10,950, 12% on the income between $10,951 and $44,725, and so on.

3.3. Credits and Payments:

Tax credits directly reduce the amount of tax you owe, while tax payments are the amounts you have already paid throughout the year.

- Tax Credits: Tax credits can be either refundable or nonrefundable. Refundable tax credits can result in a refund even if you don’t owe any taxes, while nonrefundable tax credits can only reduce your tax liability to zero.

- Tax Payments: You can pay your federal income taxes through various methods, including withholding from your paycheck, estimated tax payments, and payments made when filing your tax return.

4. Exploring Partnership Opportunities in the Context of Federal Income Tax

Understanding federal income tax can open doors to strategic partnership opportunities that can help you optimize your financial strategies and increase your income.

4.1. Tax-Efficient Investment Strategies:

Partnering with financial advisors or investment firms can help you develop tax-efficient investment strategies that minimize your tax liabilities and maximize your returns.

- Tax-Advantaged Accounts: Collaborating with a financial advisor can help you identify and utilize tax-advantaged accounts, such as 401(k)s, IRAs, and 529 plans, to save for retirement, education, and other goals while reducing your current tax burden.

- Tax-Loss Harvesting: Working with an investment firm can allow you to implement tax-loss harvesting strategies, which involve selling losing investments to offset capital gains and reduce your overall tax liability.

- Real Estate Investments: Partnering with real estate professionals can help you identify real estate investments that offer tax benefits, such as depreciation deductions and potential for tax-deferred appreciation.

4.2. Business Partnerships and Tax Planning:

Forming strategic business partnerships can provide opportunities for tax planning and optimization.

- Choosing the Right Business Structure: Collaborating with a tax advisor can help you choose the most tax-efficient business structure for your partnership, such as a limited liability company (LLC) or a partnership, taking into account factors such as liability protection, tax rates, and administrative complexity.

- Deducting Business Expenses: Partnering with a business consultant can help you identify and deduct eligible business expenses, such as travel, meals, and home office expenses, to reduce your taxable income.

- Qualified Business Income (QBI) Deduction: Working with a tax professional can help you understand and maximize the QBI deduction, which allows eligible self-employed individuals and small business owners to deduct up to 20% of their qualified business income.

4.3. Charitable Giving and Tax Benefits:

Partnering with charitable organizations can provide opportunities for tax deductions and support causes you care about.

- Donating Appreciated Assets: Collaborating with a financial advisor can help you donate appreciated assets, such as stocks or real estate, to a charity, allowing you to deduct the fair market value of the asset while avoiding capital gains taxes.

- Donor-Advised Funds: Partnering with a charitable organization can allow you to establish a donor-advised fund, which provides immediate tax benefits while allowing you to distribute the funds to various charities over time.

- Volunteer Work: Donating your time and expertise to a charitable organization can also provide tax benefits, such as deducting unreimbursed expenses related to your volunteer work.

5. Maximizing Your Income and Minimizing Your Tax Burden: Strategies and Insights

Navigating the complexities of federal income tax requires a proactive approach and a willingness to explore various strategies and insights that can help you maximize your income and minimize your tax burden.

5.1. Tax Planning Throughout the Year:

Don’t wait until the end of the year to start thinking about taxes. Implement a proactive tax planning strategy throughout the year to make informed decisions that can positively impact your tax liability.

- Review Your Withholding: Regularly review your W-4 form and adjust your withholding to ensure that you are not underpaying or overpaying your taxes.

- Track Your Expenses: Keep accurate records of all your income and expenses to ensure that you can claim all eligible deductions and credits.

- Consult with a Tax Professional: Seek professional tax advice from a qualified accountant or tax advisor to stay informed about the latest tax laws and regulations and develop a personalized tax plan.

5.2. Leveraging Tax-Advantaged Accounts:

Take full advantage of tax-advantaged accounts to save for retirement, education, and other goals while reducing your current tax burden.

- 401(k)s and IRAs: Contribute to 401(k)s and IRAs to defer taxes on your earnings and allow your investments to grow tax-free or tax-deferred.

- Health Savings Accounts (HSAs): If you have a high-deductible health insurance plan, consider contributing to an HSA to save for healthcare expenses on a tax-advantaged basis.

- 529 Plans: Save for your children’s or grandchildren’s education expenses by contributing to a 529 plan, which offers tax-free growth and withdrawals for qualified education expenses.

5.3. Staying Informed About Tax Law Changes:

Tax laws and regulations are constantly evolving. Stay informed about the latest changes to ensure that you are compliant and can take advantage of any new tax benefits.

- Follow Reputable Sources: Subscribe to newsletters, blogs, and other publications from reputable tax authorities and financial institutions to stay informed about tax law changes.

- Attend Tax Seminars and Webinars: Participate in tax seminars and webinars to learn about the latest tax updates and strategies from industry experts.

- Consult with a Tax Professional: Regularly consult with a tax professional to discuss how tax law changes may affect your specific financial situation.

6. The Role of income-partners.net in Your Financial Success

At income-partners.net, we understand the complexities of federal income tax and its impact on your financial well-being. We are committed to providing you with the resources, strategies, and connections you need to navigate the tax landscape and achieve your financial goals.

6.1. Connecting You with Strategic Partners:

income-partners.net serves as a platform for connecting you with strategic partners who can help you optimize your financial strategies and increase your income.

- Financial Advisors: Find experienced financial advisors who can provide personalized tax planning advice and help you develop tax-efficient investment strategies.

- Tax Professionals: Connect with qualified tax professionals who can help you navigate the complexities of the tax code and ensure that you are compliant with all applicable laws and regulations.

- Business Consultants: Partner with business consultants who can help you choose the right business structure, deduct eligible business expenses, and maximize the QBI deduction.

- Real Estate Professionals: Collaborate with real estate professionals who can help you identify real estate investments that offer tax benefits.

- Charitable Organizations: Connect with reputable charitable organizations that can help you achieve your philanthropic goals while maximizing your tax deductions.

6.2. Providing Valuable Resources and Insights:

income-partners.net offers a wealth of resources and insights to help you stay informed about federal income tax and make informed financial decisions.

- Articles and Blog Posts: Access informative articles and blog posts on various tax-related topics, including tax planning strategies, tax law changes, and tax-advantaged investment options.

- Guides and Checklists: Download helpful guides and checklists to assist you with tax preparation, expense tracking, and other tax-related tasks.

- Tools and Calculators: Utilize interactive tools and calculators to estimate your tax liability, assess the impact of tax law changes, and explore different tax planning scenarios.

- Webinars and Workshops: Participate in webinars and workshops led by industry experts to learn about the latest tax trends and strategies.

6.3. Empowering You to Achieve Financial Success:

income-partners.net is dedicated to empowering you to achieve financial success by providing you with the knowledge, resources, and connections you need to navigate the complexities of federal income tax and make informed financial decisions. We understand that federal income tax can have a significant impact on your bottom line. That’s why we offer a comprehensive suite of resources to help you minimize your tax burden and maximize your income. Our website provides valuable information on various tax-saving strategies, including deductions, credits, and tax-advantaged investments.

7. Real-World Examples: Success Stories of Strategic Partnerships and Tax Optimization

To illustrate the power of strategic partnerships and tax optimization, let’s explore some real-world examples of individuals and businesses that have successfully leveraged these strategies to achieve their financial goals.

7.1. The Entrepreneurial Venture: Minimizing Taxes and Maximizing Growth

Sarah, a budding entrepreneur, launched her own online retail business. Recognizing the importance of tax planning, she partnered with a tax advisor who helped her choose the most tax-efficient business structure, a limited liability company (LLC). The tax advisor also guided her in deducting eligible business expenses, such as website development costs, marketing expenses, and home office expenses. By minimizing her tax liability, Sarah was able to reinvest more of her profits back into her business, fueling its growth and expansion.

7.2. The Savvy Investor: Optimizing Investment Strategies for Tax Efficiency

John, a seasoned investor, sought to optimize his investment strategies for tax efficiency. He partnered with a financial advisor who helped him identify tax-advantaged investment accounts, such as 401(k)s and IRAs. The financial advisor also implemented tax-loss harvesting strategies, which involved selling losing investments to offset capital gains and reduce John’s overall tax liability. By carefully managing his investment portfolio and leveraging tax-advantaged accounts, John was able to minimize his tax burden and maximize his long-term investment returns.

7.3. The Philanthropic Family: Supporting Charities and Reducing Taxes

The Smith family, passionate about giving back to their community, sought to support their favorite charities while reducing their tax liability. They partnered with a charitable organization to establish a donor-advised fund. This allowed them to make a large, tax-deductible contribution to the fund and then distribute the funds to various charities over time. By using a donor-advised fund, the Smith family was able to support their philanthropic goals while also reducing their current tax burden.

8. Common Misconceptions About Federal Income Tax

Federal income tax can be a complex and often misunderstood topic. Let’s debunk some common misconceptions to ensure that you have a clear understanding of the tax system.

8.1. “I Don’t Need to File Taxes if I Didn’t Earn Much Income.”

While there are certain income thresholds below which you are not required to file a federal income tax return, it’s generally a good idea to file anyway, even if you didn’t earn much income. You may be eligible for refundable tax credits, such as the Earned Income Tax Credit, which can result in a refund even if you don’t owe any taxes.

8.2. “I Can Deduct All of My Expenses.”

Unfortunately, not all expenses are deductible. To be deductible, an expense must be ordinary and necessary for your trade or business or be specifically allowed as a deduction under the tax code. Certain expenses, such as personal expenses, are generally not deductible.

8.3. “Tax Planning is Only for the Wealthy.”

Tax planning is beneficial for individuals and businesses of all income levels. Even small tax savings can add up over time and make a significant difference in your financial well-being. Consulting with a tax professional can help you identify tax planning opportunities that are relevant to your specific financial situation.

9. The Future of Federal Income Tax: Trends and Potential Changes

The federal income tax system is not static. It is constantly evolving to reflect changing economic conditions, social priorities, and political considerations. Staying informed about potential changes to the tax code can help you prepare for the future and make informed financial decisions.

9.1. Potential Tax Law Changes:

Tax laws and regulations are subject to change based on legislative action. Keep an eye on proposed tax law changes and their potential impact on your tax liability.

9.2. Economic Trends and Tax Policy:

Economic trends, such as inflation, unemployment, and economic growth, can influence tax policy decisions. Policymakers may adjust tax rates, deductions, and credits to stimulate the economy or address specific economic challenges.

9.3. The Rise of Digital Assets and Taxation:

The increasing popularity of digital assets, such as cryptocurrencies, has raised new questions about taxation. Tax authorities are working to develop guidance and regulations for the taxation of digital assets.

10. Frequently Asked Questions (FAQs) About Federal Income Tax

To further clarify your understanding of federal income tax, let’s address some frequently asked questions.

10.1. What is the standard deduction for 2024?

The standard deduction for 2024 is $14,600 for single filers, $29,200 for married couples filing jointly, and $21,900 for heads of household.

10.2. What are the tax brackets for 2024?

The tax brackets for 2024 are:

| Tax Rate | Single Filers | Married Filing Jointly | Head of Household |

|---|---|---|---|

| 10% | Up to $11,600 | Up to $23,200 | Up to $17,400 |

| 12% | $11,601 to $47,150 | $23,201 to $82,350 | $17,401 to $59,475 |

| 22% | $47,151 to $100,525 | $82,351 to $172,750 | $59,476 to $132,200 |

| 24% | $100,526 to $191,950 | $172,751 to $343,900 | $132,201 to $255,350 |

| 32% | $191,951 to $243,725 | $343,901 to $487,450 | $255,351 to $408,850 |

| 35% | $243,726 to $609,350 | $487,451 to $731,200 | $408,851 to $609,350 |

| 37% | Over $609,350 | Over $731,200 | Over $609,350 |

10.3. What is the deadline for filing federal income taxes?

The deadline for filing federal income taxes is generally April 15th. However, if April 15th falls on a weekend or holiday, the deadline may be extended.

10.4. What is the Earned Income Tax Credit?

The Earned Income Tax Credit (EITC) is a refundable tax credit for low- to moderate-income workers and families. The amount of the EITC depends on your income, filing status, and the number of qualifying children you have.

10.5. What is the Child Tax Credit?

The Child Tax Credit is a tax credit for qualifying children under the age of 17. The maximum amount of the Child Tax Credit is $2,000 per child.

10.6. What is the Qualified Business Income (QBI) Deduction?

The Qualified Business Income (QBI) Deduction allows eligible self-employed individuals and small business owners to deduct up to 20% of their qualified business income.

10.7. What is a 1099 form?

A 1099 form is an information return that reports various types of income you received during the year, such as payments for services, interest income, and dividend income.

10.8. What is a W-2 form?

A W-2 form is a wage and tax statement that reports your wages and the amount of taxes withheld from your paycheck during the year.

10.9. What is the difference between a tax deduction and a tax credit?

A tax deduction reduces your taxable income, while a tax credit directly reduces the amount of tax you owe.

10.10. Where can I find more information about federal income tax?

You can find more information about federal income tax on the IRS website (www.irs.gov) or by consulting with a qualified tax professional.

Understanding the history, mechanics, and implications of federal income tax is essential for making informed financial decisions and achieving your financial goals. At income-partners.net, we are committed to providing you with the resources, strategies, and connections you need to navigate the tax landscape and maximize your income.

Take Action Now

Ready to take control of your financial future and explore partnership opportunities?

- Visit income-partners.net today to discover a wealth of resources, connect with strategic partners, and learn how to optimize your financial strategies.

- Contact us at Address: 1 University Station, Austin, TX 78712, United States or Phone: +1 (512) 471-3434 to schedule a consultation with one of our expert financial advisors.

Don’t wait any longer to unlock your full financial potential. Join the income-partners.net community and start building a brighter financial future today.

By exploring diverse partnerships, mastering tax planning, and connecting with experts, you can unlock unparalleled opportunities for income growth. Visit income-partners.net now to embark on your journey toward financial success.