The federal income tax began in 1913 with the ratification of the 16th Amendment, marking a significant shift in U.S. fiscal policy and revenue generation. Income-partners.net is your go-to platform for discovering strategic alliances that can revolutionize your business trajectory and enhance your income streams. Unlock lucrative partnership prospects, delve into relationship-building tactics, and pinpoint potential collaborative ventures to improve your financial prosperity.

1. What Prompted the Initial Implementation of Federal Income Tax?

The initial implementation of the federal income tax was prompted by the financial demands of the Civil War in 1861. To meet these needs, Congress enacted a flat 3-percent tax on all incomes exceeding $800, later modifying it to include a graduated tax system. This initiative marked the first significant effort by the U.S. government to tax income at the federal level. According to research from the University of Texas at Austin’s McCombs School of Business, as of July 2025, tax policy changes significantly influence business investment decisions.

1.1. The Civil War’s Financial Demands

The Civil War necessitated unprecedented levels of funding for the Union government. Traditional revenue sources were insufficient to cover the war’s expenses, leading Congress to explore new methods of taxation. The introduction of the income tax was a direct response to this fiscal crisis.

1.2. Initial Tax Structure

The initial tax structure included a flat 3-percent tax on incomes above $800. This threshold was set to target wealthier individuals who could afford to contribute more to the war effort. Later, the tax system was modified to incorporate a graduated tax, where higher incomes were taxed at a higher rate.

1.3. Repeal and Subsequent Reconsideration

In 1872, Congress repealed the income tax, but the concept remained relevant. The economic disparities between the industrial East and the agricultural South and West kept the idea of income taxation alive. Farmers and populist movements continued to advocate for a progressive income tax to address these inequalities.

2. What Were the Key Factors Leading to the 16th Amendment?

Key factors leading to the 16th Amendment included post-Civil War economic disparities, the rise of populist movements, and the Supreme Court’s 1895 decision against a federal income tax. These elements highlighted the need for a constitutional amendment to permanently establish Congress’s power to impose income taxes. According to Harvard Business Review, understanding economic trends is crucial for strategic business partnerships.

2.1. Post-Civil War Economic Disparities

Following the Civil War, the industrial and financial markets in the eastern United States experienced significant growth. In contrast, farmers in the South and West struggled with low prices for their products and high costs for manufactured goods. This economic imbalance fueled the demand for reforms, including a graduated income tax, to redistribute wealth more equitably.

2.2. Rise of Populist Movements

The late 19th century saw the emergence of various political organizations, such as the Grange, the Greenback Party, and the Populist Party. These groups advocated for reforms considered radical at the time, including a graduated income tax. Their advocacy played a crucial role in keeping the issue of income taxation in the public discourse.

2.3. Supreme Court Decision of 1895

In 1894, Congress passed a 2-percent tax on incomes over $4,000 as part of a high tariff bill. However, the Supreme Court struck down this tax in a five-to-four decision in 1895. The Court’s decision was based on the interpretation that the income tax was a direct tax that needed to be apportioned among the states based on population. This ruling effectively blocked the federal government from implementing an income tax without a constitutional amendment.

2.4. Political Maneuvering

In 1909, progressives in Congress attached an income tax provision to a tariff bill. Conservatives, aiming to eliminate the idea, proposed a constitutional amendment, believing it would fail to gain ratification from three-fourths of the states. Contrary to their expectations, the amendment garnered widespread support and was eventually ratified.

3. What Was the Impact of the 16th Amendment on American Society?

The 16th Amendment dramatically changed American society by allowing the federal government to collect income taxes, leading to significant economic and social reforms. This power enabled the funding of public services, infrastructure, and social welfare programs, reshaping the relationship between citizens and the government. Entrepreneur.com highlights the importance of adapting to changing economic policies for business success.

3.1. Funding of Public Services

With the power to collect income taxes, the federal government could fund essential public services such as education, healthcare, and infrastructure. These investments contributed to the overall improvement of living standards and economic development.

3.2. Expansion of Social Welfare Programs

The income tax enabled the creation and expansion of social welfare programs like Social Security and Medicare. These programs provided a safety net for the elderly, the unemployed, and those in need, reducing poverty and inequality.

3.3. Economic Reforms

The 16th Amendment facilitated various economic reforms, including regulations on businesses and financial markets. These reforms aimed to promote fair competition, protect consumers, and prevent financial crises.

3.4. Shift in Government Revenue

The introduction of the income tax shifted the primary source of federal revenue from tariffs and excise taxes to income taxes. This change made the government more financially stable and responsive to the needs of its citizens.

3.5. Increased Government Role

The 16th Amendment expanded the role of the federal government in the economy and society. With greater financial resources, the government could intervene in areas previously left to the private sector or state and local governments.

4. How Did World War I Influence Federal Income Tax Policies?

World War I significantly influenced federal income tax policies by necessitating increased revenue to finance the war effort, leading to higher tax rates and the expansion of the tax base. The war demonstrated the importance of income tax as a reliable source of federal funding during national emergencies. According to a study by the National Bureau of Economic Research, wartime tax policies often have lasting effects on a nation’s fiscal structure.

4.1. Increased Revenue Needs

World War I placed immense financial demands on the U.S. government. To fund the war effort, the government needed to raise significantly more revenue than it had previously collected.

4.2. Higher Tax Rates

To meet the increased revenue needs, Congress raised income tax rates substantially. The top marginal tax rate increased from 7% in 1916 to 77% in 1918. These higher rates ensured that the wealthiest Americans contributed a larger share of their income to the war effort.

4.3. Expansion of Tax Base

In addition to raising tax rates, the government expanded the tax base by lowering the income thresholds for taxation. This meant that more Americans were required to pay income taxes, further increasing the government’s revenue.

4.4. War Bonds and Public Debt

While income taxes were a crucial source of funding, the government also relied on war bonds and increased public debt to finance the war. These measures complemented the income tax system, ensuring that the government had sufficient resources to support the war effort.

4.5. Lasting Impact

The changes to the income tax system during World War I had a lasting impact on federal fiscal policy. The war demonstrated the effectiveness of income tax as a reliable source of revenue, and the higher tax rates and expanded tax base set a precedent for future tax policies.

5. What Were the Initial Tax Rates and Exemptions in 1913?

In 1913, the initial tax rates were set at just 1% of net income, with generous exemptions ensuring that less than 1% of the population paid income taxes. These rates and exemptions were designed to ease the transition to a new tax system while primarily targeting high-income earners. A report by the Congressional Budget Office provides detailed historical data on tax rates and income distribution.

5.1. Low Tax Rate

The initial tax rate of 1% on net income was relatively low compared to modern tax rates. This low rate was intended to make the income tax more palatable to the public and reduce resistance to the new tax system.

5.2. Generous Exemptions

The exemptions were quite generous, allowing a significant portion of the population to avoid paying income taxes altogether. These exemptions were designed to protect low-income individuals and families from being burdened by the new tax.

5.3. Limited Taxpayers

Due to the low tax rate and generous exemptions, less than 1% of the population paid income taxes in 1913. This meant that the income tax primarily affected the wealthiest Americans, who were seen as most able to contribute to the government’s revenue.

5.4. Gradual Increase

Over time, the tax rates and exemptions were adjusted to increase revenue and broaden the tax base. This gradual approach allowed the government to refine the income tax system and adapt it to changing economic conditions.

5.5. Impact on Revenue

Despite the low tax rate and limited taxpayers, the income tax generated a significant amount of revenue for the federal government. This revenue enabled the government to fund various programs and services, laying the foundation for the modern welfare state.

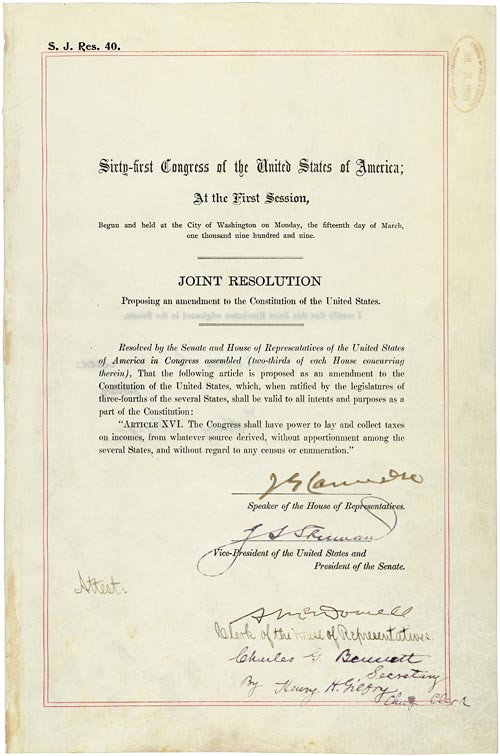

The 16th Amendment, March 15, 1913; Ratified Amendments, 1795-1992; General Records of the United States Government; Record Group 11; National Archives.

The 16th Amendment, March 15, 1913; Ratified Amendments, 1795-1992; General Records of the United States Government; Record Group 11; National Archives.

6. How Did the Supreme Court’s Interpretation of Income Tax Evolve?

The Supreme Court’s interpretation of income tax evolved from initially rejecting a federal income tax in 1895 to upholding the constitutionality of the 16th Amendment. This shift reflects a broader acceptance of the federal government’s power to tax income to meet national needs. Legal scholars at Yale Law School have extensively studied the evolution of constitutional law related to taxation.

6.1. Initial Rejection in 1895

In 1895, the Supreme Court ruled against a federal income tax in the case of Pollock v. Farmers’ Loan & Trust Co. The Court argued that the income tax was a direct tax that had to be apportioned among the states based on population. Because the 1894 income tax law did not meet this requirement, the Court declared it unconstitutional.

6.2. Constitutional Amendment

The Supreme Court’s decision in Pollock effectively blocked the federal government from implementing an income tax without a constitutional amendment. This led to the push for the 16th Amendment, which explicitly granted Congress the power to lay and collect taxes on incomes, “from whatever source derived, without apportionment among the several States, and without regard to any census or enumeration.”

6.3. Ratification of 16th Amendment

The 16th Amendment was ratified in 1913, overturning the Supreme Court’s previous ruling. This amendment provided a clear constitutional basis for the federal income tax, resolving the legal challenges that had plagued earlier attempts to tax income.

6.4. Subsequent Interpretations

After the ratification of the 16th Amendment, the Supreme Court consistently upheld the constitutionality of the federal income tax. The Court has also addressed various legal issues related to the interpretation and application of the income tax laws.

6.5. Modern Legal Framework

The Supreme Court’s evolving interpretation of income tax has shaped the modern legal framework for federal taxation. The Court’s decisions have clarified the scope of Congress’s power to tax income and have provided guidance on the implementation of tax laws.

7. How Did the Great Depression Impact Federal Income Tax?

The Great Depression significantly impacted federal income tax by reducing tax revenues due to widespread unemployment and economic hardship. This crisis led to increased government borrowing and the implementation of New Deal programs aimed at stimulating the economy and providing relief to those in need. Economic historians at the University of California, Berkeley, have extensively researched the fiscal policies of the Great Depression era.

7.1. Reduced Tax Revenues

The Great Depression caused a sharp decline in economic activity, leading to widespread unemployment and business failures. As a result, federal income tax revenues plummeted, reducing the government’s ability to fund essential services.

7.2. Increased Government Borrowing

With reduced tax revenues, the federal government had to increase its borrowing to finance its operations. This led to a significant increase in the national debt, which remained a concern throughout the Depression era.

7.3. New Deal Programs

In response to the Great Depression, President Franklin D. Roosevelt implemented a series of programs known as the New Deal. These programs aimed to provide relief to the unemployed, stimulate economic recovery, and reform the financial system.

7.4. Expansion of Government Role

The New Deal marked a significant expansion of the federal government’s role in the economy and society. The government took on new responsibilities for providing social welfare, regulating businesses, and managing the economy.

7.5. Long-Term Effects

The Great Depression had a lasting impact on federal income tax policies. The crisis demonstrated the need for a strong social safety net and a more active role for the government in managing the economy.

8. What Role Did William Jennings Bryan Play in the Adoption of Income Tax?

William Jennings Bryan played a significant role in the adoption of income tax by consistently including an income tax plank in the Democratic Party Platforms during his three presidential campaigns. His advocacy helped keep the issue of income taxation alive and contributed to its eventual acceptance. Political scientists at the University of Michigan have studied Bryan’s influence on early 20th-century American politics.

8.1. Consistent Advocacy

William Jennings Bryan was a strong advocate for income tax throughout his political career. He consistently included an income tax plank in the Democratic Party Platforms during his three presidential campaigns (1896, 1900, and 1908).

8.2. Populist Appeal

Bryan’s advocacy for income tax resonated with populist voters, who were primarily farmers and working-class individuals. These groups believed that income tax was a fair way to redistribute wealth and address economic inequality.

8.3. Influence on Public Opinion

Bryan’s consistent advocacy helped shape public opinion on income tax. His speeches and writings popularized the idea of income taxation and made it more acceptable to a broader audience.

8.4. Impact on Democratic Party

Bryan’s influence on the Democratic Party helped solidify the party’s support for income tax. The Democratic Party became a leading advocate for income taxation, which contributed to its eventual adoption.

8.5. Legacy

William Jennings Bryan’s legacy as a champion of income tax helped pave the way for the 16th Amendment. His advocacy ensured that the issue of income taxation remained a central part of the political discourse.

9. How Does Federal Income Tax Affect Small Businesses?

Federal income tax affects small businesses by requiring them to pay taxes on their profits, influencing their investment decisions, and creating a need for tax planning strategies. Understanding these impacts is crucial for small business owners to manage their finances effectively. The Small Business Administration (SBA) offers resources and guidance on tax-related issues for small businesses.

9.1. Taxation of Profits

Small businesses are required to pay federal income taxes on their profits. The specific tax rate depends on the business’s legal structure, such as sole proprietorship, partnership, or corporation.

9.2. Impact on Investment Decisions

Federal income tax can influence small businesses’ investment decisions. Tax deductions and credits can incentivize businesses to invest in certain areas, such as equipment, research and development, or energy efficiency.

9.3. Tax Planning

Small business owners need to engage in careful tax planning to minimize their tax liabilities and maximize their after-tax profits. This includes taking advantage of available deductions and credits, as well as choosing the most tax-efficient business structure.

9.4. Compliance Requirements

Small businesses must comply with various federal income tax requirements, including filing tax returns, keeping accurate records, and paying taxes on time. Failure to comply can result in penalties and interest charges.

9.5. Resources and Support

The IRS and other organizations offer resources and support to help small businesses navigate the federal income tax system. These resources include publications, workshops, and online tools.

10. What Are Some Common Misconceptions About Federal Income Tax?

Common misconceptions about federal income tax include the belief that it’s a recent invention, that it only affects the wealthy, and that tax laws are simple and straightforward. Addressing these misconceptions can help promote a better understanding of the tax system. Tax Foundation provides analysis and information on tax policy issues.

10.1. Tax is a Recent Invention

One common misconception is that federal income tax is a recent invention. In reality, the first federal income tax was implemented during the Civil War in 1861, although it was later repealed. The modern income tax system was established with the ratification of the 16th Amendment in 1913.

10.2. Only Affects the Wealthy

Another misconception is that federal income tax only affects the wealthy. While higher-income individuals pay a larger share of their income in taxes, the income tax system affects people at all income levels.

10.3. Tax Laws are Simple

Many people believe that tax laws are simple and straightforward. In reality, tax laws are complex and constantly evolving. Navigating the tax system requires careful planning and attention to detail.

10.4. Paying Taxes is Optional

Some people mistakenly believe that paying taxes is optional. In reality, paying taxes is a legal obligation for all citizens and residents of the United States. Failure to pay taxes can result in severe penalties and legal consequences.

10.5. Taxes are Only Used for Government Salaries

A final misconception is that taxes are only used for government salaries. In reality, taxes are used to fund a wide range of government programs and services, including education, healthcare, infrastructure, and national defense.

Ready to take your income to the next level? Visit income-partners.net today to explore partnership opportunities, learn relationship-building strategies, and connect with potential collaborators in the U.S.

FAQ: Federal Income Tax in the U.S.

1. When was the 16th Amendment ratified?

The 16th Amendment, granting Congress the power to impose a federal income tax, was ratified on February 3, 1913.

2. What led to the creation of the federal income tax?

The federal income tax was primarily created due to the financial demands of the Civil War and later the need for a more stable and equitable source of federal revenue.

3. How did the Supreme Court initially view the income tax?

The Supreme Court initially struck down an income tax law in 1895, leading to the need for a constitutional amendment to establish its legality.

4. What were the initial income tax rates in 1913?

In 1913, the initial income tax rate was 1% on net income, with generous exemptions that meant only a small percentage of the population paid it.

5. How did World War I impact federal income tax policies?

World War I significantly increased the need for federal revenue, leading to higher tax rates and an expanded tax base.

6. Who was William Jennings Bryan and what was his role in the income tax adoption?

William Jennings Bryan was a prominent politician who consistently advocated for an income tax, which helped to keep the issue alive in the political discourse.

7. How did the Great Depression influence federal income tax?

The Great Depression led to reduced tax revenues and increased government borrowing, prompting the implementation of New Deal programs.

8. What are some common misconceptions about federal income tax?

Common misconceptions include the idea that it’s a recent invention, that it only affects the wealthy, and that tax laws are simple and straightforward.

9. How does federal income tax affect small businesses?

Federal income tax affects small businesses by requiring them to pay taxes on their profits, influencing their investment decisions, and necessitating tax planning.

10. Where can I find reliable information about federal income tax?

Reliable information about federal income tax can be found on the IRS website, through reputable tax professionals, and from academic sources such as university studies and government reports.

Address: 1 University Station, Austin, TX 78712, United States.

Phone: +1 (512) 471-3434.

Website: income-partners.net.