The average household income in 1970 is a crucial benchmark for understanding economic trends and income inequality. At income-partners.net, we help you explore partnership opportunities to increase your income, and understanding historical income data provides valuable context. Income levels and income brackets changed dramatically and you can stay ahead of these trends by reading on to discover the key economic shifts that have influenced household finances over the decades with income-partners.net, where strategic partnerships can pave the way for enhanced financial prosperity.

1. What Was the Median Household Income in 1970?

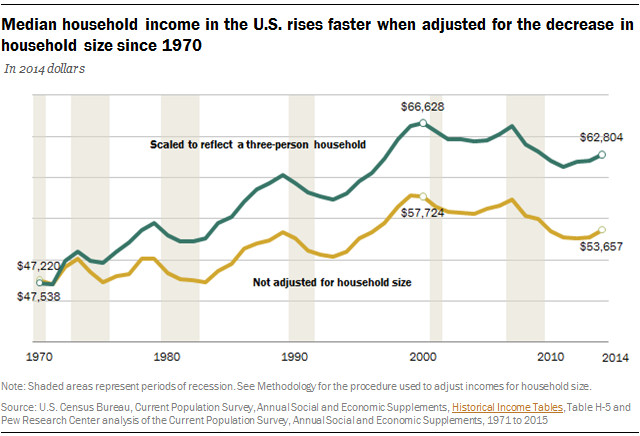

In 1970, the median household income in the United States was approximately $47,538. This figure, unadjusted for household size, provides a baseline for understanding economic conditions and standards of living at that time. However, when adjusted for household size, the median income was about $47,220, reflecting the financial resources available to a typical household. This adjustment is important because the average household size in 1970 was larger than it is today, affecting the overall economic well-being. Understanding these figures helps individuals and businesses assess economic trends and strategize for financial growth.

1.1 How Did Household Size Affect Income in 1970?

Household size significantly influenced the interpretation of income data in 1970. The average household consisted of 3.2 people, meaning that the median income had to support more individuals compared to later years. Adjusting for household size provides a more accurate view of the financial resources available per person. According to the U.S. Census Bureau, adjusting for household size, the median income increased to $62,804 in 2014 from $47,220 in 1970.

1.2 What Were the Income Trends for Different Income Tiers in 1970?

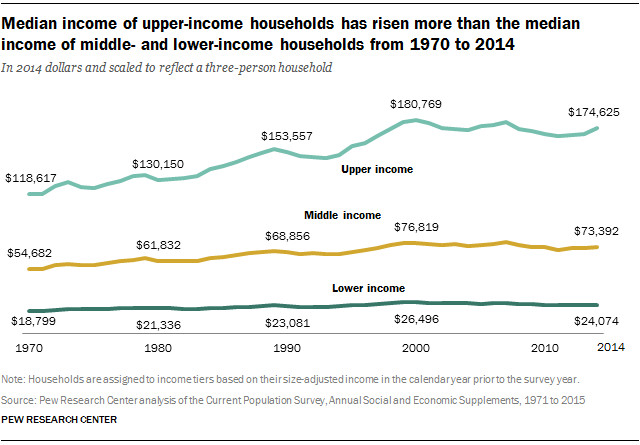

In 1970, income disparities were already evident across different income tiers. Upper-income households had a median income of about $118,617, while middle-income households had a median income of $54,682, and lower-income households had a median income of $18,799. These figures highlight the income gaps that existed and set the stage for understanding how these gaps have evolved over time.

2. How Did Household Income Change From 1970 to 2014?

From 1970 to 2014, household incomes experienced overall growth, but the extent of that growth varied across different income tiers. The median income for all households increased from $47,538 to $53,657, a rise of 13%. Adjusting for household size, the increase was even more significant, with median income rising from $47,220 to $62,804, a growth of 33%. This period also saw significant shifts in income distribution, with upper-income households experiencing the most substantial gains.

2.1 What Factors Contributed to Income Growth From 1970 to 2014?

Several factors contributed to income growth between 1970 and 2014, including technological advancements, increased educational attainment, and changes in the labor market. Technological advancements led to higher productivity and wages in many sectors. Increased educational attainment enabled more individuals to access higher-paying jobs. These factors, combined with shifts in economic policies, contributed to the overall rise in household incomes.

2.2 How Did Different Income Tiers Fare From 1970 to 2014?

From 1970 to 2014, upper-income households saw the most significant income growth, increasing by 47%, from $118,617 to $174,625. Middle-income households experienced a 34% increase, rising from $54,682 to $73,392, while lower-income households saw a 28% increase, growing from $18,799 to $24,074. These disparities highlight the growing income inequality during this period.

Median household income in the U.S. rises faster when adjusted for the decrease in household size since 1970

Median household income in the U.S. rises faster when adjusted for the decrease in household size since 1970

3. What Happened to Household Incomes Between 2000 and 2014?

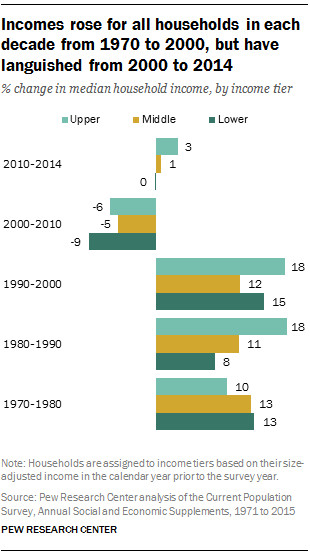

Between 2000 and 2014, household incomes generally declined, reversing some of the gains made in previous decades. This period was marked by two major economic recessions and slow recoveries, impacting households across all income tiers. The median income for middle-income households fell by 4%, from $76,819 to $73,392, while upper-income households saw a similar loss of 3%, decreasing from $180,769 to $174,625. Lower-income households experienced the most significant decline, with their income falling by 9%, from $26,496 to $24,074.

3.1 What Caused the Decline in Household Incomes From 2000 to 2014?

The decline in household incomes from 2000 to 2014 was primarily due to the economic downturns of 2001 and the Great Recession of 2007-2009. These recessions led to job losses, reduced wages, and decreased investment returns, affecting households across all income levels. According to economic analysts, the slow pace of economic recovery following these recessions further exacerbated the decline in household incomes.

3.2 How Did the Economic Downturns Affect Different Income Tiers?

The economic downturns disproportionately affected lower-income households, who experienced the largest percentage decline in income. While upper-income households also saw a decrease in income, their greater financial resources allowed them to weather the economic storms more effectively. Middle-income households faced increased financial strain as well, with many struggling to maintain their standard of living.

4. How Has Income Inequality Changed Since 1970?

Income inequality has significantly increased since 1970, with upper-income households capturing a larger share of the total household income. In 1970, upper-income households held 29% of the aggregate household income, while middle-income households held 62%. By 2014, the share held by upper-income households had risen to 49%, surpassing the 43% held by middle-income households. This shift highlights the growing concentration of wealth at the top of the income distribution.

4.1 What Factors Have Contributed to the Rise in Income Inequality?

Several factors have contributed to the rise in income inequality since 1970, including changes in tax policies, deregulation of industries, and the decline of labor unions. Tax policies have often favored upper-income individuals and corporations, leading to greater wealth accumulation. Deregulation has allowed for increased corporate profits, while the decline of labor unions has weakened the bargaining power of workers.

4.2 How Does the Distribution of Aggregate Income Look Today?

Today, the distribution of aggregate income is heavily skewed towards upper-income households. In 2014, upper-income households, comprising 21% of the adult population, held 49% of the aggregate income. Middle-income households, representing 50% of the adult population, held 43% of the income, while lower-income households, accounting for 29% of the adult population, held only 9% of the income. This unequal distribution underscores the significant income disparities in the United States.

Median income of upper-income households has risen more than the median income of middle- and lower-income households from 1970 to 2014

Median income of upper-income households has risen more than the median income of middle- and lower-income households from 1970 to 2014

5. How Does Household Income Affect Economic Mobility?

Household income plays a crucial role in determining economic mobility, the ability of individuals to move up or down the income ladder. Children from higher-income households tend to have better access to education, healthcare, and other resources that promote upward mobility. In contrast, children from lower-income households often face significant barriers to upward mobility, perpetuating income inequality across generations.

5.1 What Are the Barriers to Economic Mobility for Lower-Income Households?

Lower-income households face numerous barriers to economic mobility, including inadequate access to quality education, limited job opportunities, and lack of affordable healthcare. The quality of education in lower-income communities is often subpar, hindering academic achievement and future employment prospects. Limited job opportunities in these communities further restrict economic advancement.

5.2 How Can Policies Promote Greater Economic Mobility?

Policies that promote greater economic mobility include investing in early childhood education, increasing access to affordable healthcare, and raising the minimum wage. Early childhood education programs can provide children from lower-income households with a strong foundation for future success. Expanding access to affordable healthcare ensures that individuals can maintain their health and productivity.

6. What Is the Impact of Education on Household Income?

Education has a significant impact on household income, with higher levels of education generally leading to higher earnings. Individuals with a bachelor’s degree or higher typically earn significantly more than those with only a high school diploma. Education provides individuals with the skills and knowledge necessary to succeed in higher-paying jobs and industries.

6.1 How Does Educational Attainment Correlate With Income Levels?

Educational attainment is strongly correlated with income levels. According to the U.S. Bureau of Labor Statistics, individuals with a bachelor’s degree earn approximately 66% more than those with a high school diploma. Those with a professional or doctoral degree earn even more, further demonstrating the economic benefits of higher education.

6.2 What Types of Educational Investments Yield the Highest Returns?

Investments in STEM (Science, Technology, Engineering, and Mathematics) fields often yield the highest returns in terms of household income. STEM jobs are in high demand and typically offer higher salaries compared to other occupations. Additionally, investments in vocational training and apprenticeships can provide individuals with valuable skills for specific industries, leading to increased earnings.

7. How Do Demographic Factors Influence Household Income?

Demographic factors such as age, race, and gender significantly influence household income. Older individuals typically earn more than younger individuals, reflecting their greater experience and career advancement. However, racial and gender disparities persist, with women and minorities often earning less than their male and white counterparts.

7.1 How Do Age and Experience Affect Income?

Age and experience are positively correlated with income, up to a certain point. Individuals typically see their earnings increase as they gain more experience in their field. However, earnings may plateau or decline later in life as individuals approach retirement.

7.2 What Are the Racial and Gender Disparities in Household Income?

Significant racial and gender disparities exist in household income. According to the U.S. Census Bureau, women earn approximately 82 cents for every dollar earned by men. Similarly, racial minorities often earn less than their white counterparts, with the largest disparities seen among Black and Hispanic households.

8. What Role Do Government Policies Play in Shaping Household Income?

Government policies play a crucial role in shaping household income through taxation, social welfare programs, and labor regulations. Progressive tax policies can help redistribute income from higher-income to lower-income households, while social welfare programs provide a safety net for those in need. Labor regulations, such as minimum wage laws, can help ensure fair wages and working conditions.

8.1 How Do Tax Policies Impact Income Distribution?

Tax policies can have a significant impact on income distribution. Progressive tax systems, where higher-income individuals pay a larger percentage of their income in taxes, can help reduce income inequality. Tax credits and deductions can also provide targeted support to lower-income households.

8.2 What Is the Impact of Social Welfare Programs on Poverty and Income?

Social welfare programs, such as Supplemental Nutrition Assistance Program (SNAP) and Temporary Assistance for Needy Families (TANF), provide crucial support to low-income households, reducing poverty and improving income. These programs help ensure that individuals have access to basic necessities such as food, housing, and healthcare.

9. How Does Location Affect Household Income?

Location significantly impacts household income due to variations in cost of living, job markets, and industry concentrations. Areas with high costs of living, such as major metropolitan cities, often require higher incomes to maintain a comfortable standard of living. Regions with thriving job markets and concentrations of high-paying industries tend to offer better income opportunities.

9.1 What Are the Regional Variations in Household Income?

Significant regional variations exist in household income across the United States. States in the Northeast and West Coast typically have higher median household incomes compared to states in the South and Midwest. These variations reflect differences in economic conditions, industry concentrations, and cost of living.

9.2 How Does Urban vs. Rural Location Impact Income Opportunities?

Urban areas generally offer more diverse job opportunities and higher salaries compared to rural areas. However, the higher cost of living in urban areas can offset some of these advantages. Rural areas may offer lower living costs but often have fewer job opportunities and lower wages.

10. What Are the Strategies for Increasing Household Income?

There are several strategies individuals can use to increase their household income, including pursuing higher education, developing in-demand skills, and exploring entrepreneurial opportunities. Higher education and skill development can lead to better job opportunities and higher salaries. Entrepreneurship can provide individuals with the opportunity to create their own income streams and build wealth.

10.1 How Can Education and Skill Development Boost Earnings?

Investing in education and skill development is one of the most effective ways to boost earnings. Obtaining a college degree or pursuing vocational training can open doors to higher-paying jobs and industries. Developing in-demand skills, such as coding, data analysis, and project management, can also increase earning potential.

10.2 What Are the Benefits of Entrepreneurship for Income Generation?

Entrepreneurship offers the potential for significant income generation and wealth creation. Starting a business allows individuals to control their own income, pursue their passions, and build a valuable asset. While entrepreneurship involves risks, the rewards can be substantial for those who are successful.

Incomes rose for all households in each decade from 1970 to 2000, but have languished from 2000 to 2014

Incomes rose for all households in each decade from 1970 to 2000, but have languished from 2000 to 2014

11. What Are the Emerging Trends in Household Income and Wealth?

Several emerging trends are shaping household income and wealth, including the rise of the gig economy, increasing automation, and the growing importance of financial literacy. The gig economy offers new opportunities for income generation but also presents challenges in terms of job security and benefits. Increasing automation is transforming the labor market, requiring workers to adapt to new skills and technologies.

11.1 How Is the Gig Economy Reshaping Income Opportunities?

The gig economy is reshaping income opportunities by providing individuals with more flexible and diverse ways to earn money. However, it also presents challenges in terms of job security, benefits, and income stability. Workers in the gig economy often lack the protections and benefits of traditional employment, making it important to develop strategies for managing income and expenses.

11.2 What Is the Impact of Automation on Future Earnings?

Automation is expected to have a significant impact on future earnings, as many jobs are at risk of being replaced by machines and artificial intelligence. Workers will need to adapt to new skills and technologies to remain competitive in the labor market. Investing in education and training in areas such as technology, data analysis, and creative problem-solving will be crucial for future earnings.

12. How Can Financial Literacy Improve Household Income Management?

Financial literacy plays a crucial role in improving household income management by helping individuals make informed decisions about budgeting, saving, and investing. Understanding financial concepts and developing good financial habits can lead to greater financial stability and wealth accumulation.

12.1 What Are the Key Components of Financial Literacy?

Key components of financial literacy include budgeting, saving, investing, and debt management. Budgeting involves tracking income and expenses to ensure that spending is aligned with financial goals. Saving involves setting aside money for future needs, such as retirement or emergencies. Investing involves using money to purchase assets that have the potential to grow in value.

12.2 What Resources Are Available for Improving Financial Literacy?

Numerous resources are available for improving financial literacy, including online courses, workshops, and financial advisors. Many non-profit organizations and government agencies offer free or low-cost financial education programs. Additionally, financial advisors can provide personalized guidance on managing income, expenses, and investments.

13. What Are the Long-Term Implications of Income Trends on Society?

The long-term implications of income trends on society are significant, affecting social cohesion, economic stability, and overall well-being. Rising income inequality can lead to social unrest and political polarization. Economic instability can result from a lack of consumer demand and investment. Ensuring that all members of society have the opportunity to thrive is essential for a healthy and prosperous future.

13.1 How Does Income Inequality Affect Social Cohesion?

Income inequality can erode social cohesion by creating divisions between different income groups. When some members of society feel that they are not sharing in the benefits of economic growth, it can lead to resentment and distrust. Addressing income inequality is essential for building a more inclusive and equitable society.

13.2 What Policies Can Promote a More Equitable Distribution of Income?

Policies that can promote a more equitable distribution of income include progressive taxation, investments in education and job training, and strengthening social safety nets. Progressive taxation can help redistribute income from higher-income to lower-income households. Investments in education and job training can provide individuals with the skills and knowledge they need to succeed in the labor market.

14. How Can Partnerships Enhance Household Income?

Partnerships can significantly enhance household income by providing access to new opportunities, resources, and expertise. Whether it’s a business partnership, a strategic alliance, or a collaborative venture, working with others can unlock new income streams and accelerate financial growth. At income-partners.net, we specialize in connecting individuals and businesses with the right partners to achieve their financial goals.

14.1 What Types of Partnerships Are Most Effective for Income Growth?

Several types of partnerships can be effective for income growth, including joint ventures, strategic alliances, and referral partnerships. Joint ventures involve two or more parties pooling their resources to undertake a specific project or business activity. Strategic alliances involve ongoing collaboration between organizations to achieve shared goals.

14.2 How Can Income-Partners.net Facilitate Successful Partnerships?

Income-partners.net provides a platform for individuals and businesses to connect, collaborate, and build mutually beneficial partnerships. Our website offers resources, tools, and networking opportunities to help you find the right partners and structure successful partnerships. Whether you’re looking to start a new business, expand your existing operations, or simply increase your income, income-partners.net can help you achieve your goals.

Exploring income trends and understanding the factors that influence household income are essential for making informed financial decisions and building a secure future. By leveraging the resources and partnership opportunities available at income-partners.net, you can take control of your financial destiny and create a brighter future for yourself and your family.

15. What Are The Success Stories Of Income Growth Through Partnerships?

Many individuals and businesses have achieved remarkable income growth through strategic partnerships. These success stories highlight the power of collaboration, shared resources, and mutual goals. Whether it’s a small business partnering with a larger corporation or two entrepreneurs joining forces to launch a new venture, the possibilities are endless.

15.1 Case Study 1: Small Business and Corporate Partnership

A small business specializing in handmade crafts partnered with a large retail corporation to sell their products nationwide. This partnership provided the small business with access to a vast customer base and increased their sales exponentially. The corporation benefited from offering unique, high-quality products that enhanced their brand image.

15.2 Case Study 2: Two Entrepreneurs Launch a Startup

Two entrepreneurs with complementary skills and experience joined forces to launch a tech startup. One entrepreneur had expertise in software development, while the other had a background in marketing and sales. Together, they created a successful company that generated significant revenue and attracted venture capital funding.

16. What Tools And Resources Are Available On Income-Partners.Net To Help Find The Right Partner?

Income-partners.net offers a comprehensive suite of tools and resources to help individuals and businesses find the right partners for their income growth objectives. Our platform provides a user-friendly interface, advanced search capabilities, and detailed profiles to connect you with potential partners who align with your goals and values.

16.1 Advanced Search Functionality

Our advanced search functionality allows you to filter potential partners based on various criteria, such as industry, location, skills, and experience. This ensures that you find partners who are the best fit for your specific needs and objectives.

16.2 Detailed Partner Profiles

Each partner profile includes detailed information about their background, expertise, and partnership goals. This enables you to assess their suitability and compatibility before reaching out to initiate a conversation.

17. How Can You Create A Compelling Partnership Proposal?

Creating a compelling partnership proposal is essential for attracting the right partners and securing mutually beneficial agreements. Your proposal should clearly outline your goals, values, and the benefits of partnering with you. It should also demonstrate your expertise and commitment to the success of the partnership.

17.1 Defining Your Goals And Values

Clearly define your goals and values in your partnership proposal. This will help potential partners understand what you’re trying to achieve and whether you’re a good fit for their organization.

17.2 Demonstrating Expertise And Commitment

Demonstrate your expertise and commitment to the success of the partnership. Provide examples of your past achievements and highlight the skills and resources that you bring to the table.

18. How Do You Negotiate A Partnership Agreement?

Negotiating a partnership agreement is a critical step in establishing a successful partnership. It’s important to approach negotiations with a clear understanding of your goals and priorities, as well as a willingness to compromise and find mutually beneficial solutions.

18.1 Understanding Your Goals And Priorities

Before entering negotiations, take the time to understand your goals and priorities. What are you hoping to achieve through the partnership? What are you willing to compromise on, and what are your non-negotiables?

18.2 Seeking Mutually Beneficial Solutions

Approach negotiations with a collaborative mindset and a willingness to seek mutually beneficial solutions. The goal should be to create an agreement that benefits all parties involved, rather than trying to win at the expense of others.

19. How Can You Effectively Manage A Partnership?

Effective management is crucial for maintaining a successful partnership over the long term. This involves clear communication, mutual respect, and a commitment to achieving shared goals.

19.1 Maintaining Clear Communication

Maintain clear and open communication with your partners. This includes regular meetings, progress updates, and transparent discussions about any challenges or concerns.

19.2 Fostering Mutual Respect

Foster a culture of mutual respect and appreciation. Recognize and value the contributions of all partners, and be willing to listen to their perspectives and ideas.

20. What Are The Common Pitfalls To Avoid In Partnerships?

While partnerships can be highly beneficial, it’s important to be aware of the common pitfalls that can derail even the most promising ventures. Avoiding these mistakes can significantly increase your chances of success.

20.1 Lack Of Clear Communication

A lack of clear communication is one of the most common reasons why partnerships fail. Without open and honest communication, misunderstandings can arise, leading to conflict and distrust.

20.2 Misaligned Goals And Values

If partners have misaligned goals and values, it can be difficult to work together effectively. It’s important to ensure that all partners are on the same page from the outset and share a common vision for the partnership.

By understanding the economic context of household income in 1970 and leveraging the partnership opportunities available at income-partners.net, you can make informed decisions, build strategic alliances, and achieve your financial goals. Visit our website today to explore the possibilities and start your journey towards greater financial prosperity.

Navigating the complexities of income trends and understanding the dynamics of household finances is essential for anyone looking to improve their financial standing. Whether you’re a business owner seeking to expand your operations or an individual aiming to increase your income, income-partners.net offers the resources and connections you need to succeed. From historical data analysis to cutting-edge partnership strategies, we provide the tools and insights necessary to thrive in today’s economy. Join our community today and discover the power of strategic partnerships in achieving your financial goals. Remember the trends, learn from the past and create a better future.

FAQ Section

Q1: What Was The Average Household Income In 1970?

In 1970, the median household income in the United States was approximately $47,538, unadjusted for household size. When adjusted for household size, the median income was about $47,220. This provides a baseline for understanding economic conditions at that time.

Q2: How did household size affect income calculations in 1970?

Household size significantly influenced income data because the average household consisted of 3.2 people. Adjusting for household size gives a more accurate view of financial resources per person; when adjusted, the median income was around $47,220.

Q3: What were the income levels for different income tiers in 1970?

In 1970, upper-income households had a median income of approximately $118,617, middle-income households had $54,682, and lower-income households had $18,799, highlighting existing income disparities.

Q4: How did household incomes change between 1970 and 2014?

From 1970 to 2014, median income for all households increased from $47,538 to $53,657 (13% rise). Adjusting for household size shows a more significant increase, from $47,220 to $62,804 (33% growth), with upper-income households seeing the largest gains.

Q5: What caused the decline in household incomes between 2000 and 2014?

The decline in household incomes from 2000 to 2014 was mainly due to the economic recessions of 2001 and 2007-2009, which led to job losses, wage reductions, and decreased investment returns.

Q6: How has income inequality changed since 1970?

Income inequality has increased since 1970. By 2014, upper-income households held 49% of the aggregate household income, surpassing the 43% held by middle-income households.

Q7: What impact does education have on household income?

Education significantly impacts household income, with higher levels of education generally leading to higher earnings. For example, individuals with a bachelor’s degree typically earn more than those with only a high school diploma.

Q8: What role do government policies play in shaping household income?

Government policies shape household income through taxation, social welfare programs, and labor regulations, which can redistribute income, provide a safety net, and ensure fair wages.

Q9: How does location affect household income?

Location significantly impacts household income due to variations in cost of living, job markets, and industry concentrations. Urban areas often offer more job opportunities but also higher living costs.

Q10: What are effective strategies for increasing household income?

Effective strategies include pursuing higher education, developing in-demand skills, and exploring entrepreneurial opportunities, all of which can lead to better job prospects and higher earnings.

Visit income-partners.net to explore partnership opportunities and learn more about increasing your income through strategic alliances. Connect with us today to discover how you can achieve your financial goals through collaboration and innovation. Address: 1 University Station, Austin, TX 78712, United States. Phone: +1 (512) 471-3434. Website: income-partners.net.