Federal income tax is primarily a progressive tax, meaning higher income earners pay a larger percentage of their income in taxes. Let’s delve deeper into what this means for you, especially if you’re aiming to boost your income through strategic partnerships, a goal we at income-partners.net are passionate about. We will discuss how it works, its impact, and strategies to manage it effectively while maximizing your opportunities for income growth through successful collaborations.

1. Understanding The Basics: What Exactly Is Federal Income Tax?

Federal income tax in the United States is a tax on earned income. This includes wages, salaries, tips, and self-employment earnings.

1.1. How Does Federal Income Tax Work?

The federal income tax system operates on a progressive tax bracket system. This means that as your income increases, the rate at which you are taxed also increases, but only for the portion of your income that falls into the higher tax bracket. The IRS (Internal Revenue Service) sets these tax brackets each year, adjusting them for inflation.

1.2. Key Components of Federal Income Tax

- Gross Income: This is your total income before any deductions or adjustments.

- Adjusted Gross Income (AGI): This is your gross income minus certain deductions like contributions to traditional IRAs, student loan interest, and health savings account (HSA) contributions.

- Taxable Income: This is your AGI minus either the standard deduction or itemized deductions, plus any qualified business income (QBI) deduction. Your tax liability is based on your taxable income.

1.3. Standard Deduction vs. Itemized Deductions

Taxpayers can choose to take the standard deduction, which is a set amount based on their filing status, or they can itemize deductions. Itemized deductions include expenses like medical expenses, state and local taxes (SALT), mortgage interest, and charitable contributions. You should choose whichever option results in a lower tax liability.

2. Why Is Federal Income Tax Considered A Progressive Tax?

Federal income tax is considered progressive due to its graduated tax rate system. Higher income earners pay a larger percentage of their income in taxes compared to lower income earners.

2.1. Tax Brackets Explained

The US federal income tax system uses tax brackets, which are income ranges taxed at different rates. For example, in 2024 (taxes filed in 2025), there are seven federal income tax brackets: 10%, 12%, 22%, 24%, 32%, 35%, and 37%. Your income is taxed at the rate of each bracket it falls into.

Example: Let’s say you are single and have a taxable income of $50,000 in 2024. The first $11,600 is taxed at 10%, the income between $11,601 and $47,150 is taxed at 12%, and the remaining income between $47,151 and $50,000 is taxed at 22%.

2.2. Marginal Tax Rate vs. Effective Tax Rate

It’s crucial to understand the difference between the marginal tax rate and the effective tax rate.

- Marginal Tax Rate: This is the tax rate you pay on your next dollar of income. It’s the rate of the highest tax bracket you fall into.

- Effective Tax Rate: This is the actual percentage of your total income that you pay in taxes. It is calculated by dividing your total tax liability by your total income.

Example: If your taxable income is $100,000, your marginal tax rate might be 22%, but your effective tax rate could be lower, say 18%, because not all of your income is taxed at 22%.

2.3. Historical Perspective on Progressive Taxation

The concept of progressive taxation has been around for centuries, with roots in ancient Greece and Rome. In the US, the modern federal income tax system was established in 1913 with the 16th Amendment to the Constitution. Over time, the tax rates and brackets have changed significantly, reflecting economic conditions and policy priorities.

3. What Are The Different Types of Federal Taxes?

Besides federal income tax, there are other types of federal taxes you should be aware of, especially as you explore income-generating partnerships.

3.1. Social Security and Medicare Taxes

Also known as FICA (Federal Insurance Contributions Act) taxes, these are payroll taxes that fund Social Security and Medicare. Employees and employers each pay a portion of these taxes.

- Social Security: The tax rate is 6.2% on earnings up to a certain wage base (e.g., $168,600 in 2024).

- Medicare: The tax rate is 1.45% on all earnings.

3.2. Federal Unemployment Tax (FUTA)

FUTA is a payroll tax paid by employers to fund unemployment benefits for workers who lose their jobs. The FUTA tax rate is 6.0% on the first $7,000 of each employee’s wages. However, most employers receive a credit of up to 5.4%, reducing the effective FUTA tax rate to 0.6%.

3.3. Excise Taxes

Excise taxes are taxes on specific goods or services, such as gasoline, alcohol, tobacco, and certain manufactured products. These taxes are often included in the price of the product and are paid by the manufacturer or retailer.

3.4. Estate and Gift Taxes

These taxes are imposed on the transfer of property from a deceased person to their heirs (estate tax) or on gifts made during a person’s lifetime (gift tax). The estate tax applies to estates above a certain threshold (e.g., $13.61 million in 2024), and the gift tax applies to gifts exceeding the annual gift tax exclusion (e.g., $18,000 per recipient in 2024).

4. How Federal Income Tax Affects Businesses And Partnerships

Understanding how federal income tax impacts businesses and partnerships is essential for effective financial planning and strategic decision-making, especially when you’re leveraging opportunities at income-partners.net.

4.1. Taxation of Partnerships

Partnerships are generally not subject to federal income tax at the entity level. Instead, the profits and losses of the partnership are passed through to the partners, who report them on their individual tax returns. This is known as pass-through taxation.

Each partner receives a Schedule K-1, which details their share of the partnership’s income, deductions, and credits. Partners then pay income tax on their share of the partnership’s profits at their individual tax rates.

4.2. Taxation of Corporations

Corporations, on the other hand, are subject to corporate income tax. This means the corporation pays tax on its profits before distributing any dividends to shareholders. When shareholders receive dividends, they may also have to pay tax on this income, resulting in double taxation.

The corporate tax rate is currently a flat 21%. However, some small businesses may choose to be taxed as S corporations, which allows them to avoid double taxation by passing through their profits and losses to their shareholders, similar to partnerships.

4.3. Tax Implications of Different Business Structures

The choice of business structure can have significant tax implications. For example:

- Sole Proprietorship: The business income is reported on the owner’s individual tax return, and the owner is also subject to self-employment tax.

- Limited Liability Company (LLC): An LLC can choose to be taxed as a sole proprietorship, partnership, S corporation, or C corporation, depending on its needs and circumstances.

- S Corporation: This structure allows the business to pass through its profits and losses to its shareholders while avoiding self-employment tax on the portion of profits that are considered a return on investment.

- C Corporation: This structure is subject to corporate income tax and may be suitable for larger businesses that need to raise capital.

4.4. Deductions and Credits for Businesses

Businesses can take various deductions and credits to reduce their taxable income. Some common deductions include:

- Business Expenses: These include expenses like rent, utilities, salaries, advertising, and travel.

- Depreciation: This allows businesses to deduct the cost of assets over their useful life.

- Qualified Business Income (QBI) Deduction: This allows eligible self-employed individuals, partnerships, and S corporation shareholders to deduct up to 20% of their qualified business income.

Tax credits, such as the research and development (R&D) tax credit and the work opportunity tax credit (WOTC), can also help businesses reduce their tax liability.

5. Strategies For Managing Federal Income Tax Effectively

Managing your federal income tax effectively is crucial for maximizing your financial well-being. Here are some strategies to consider:

5.1. Maximize Deductions and Credits

Take advantage of all eligible deductions and credits to reduce your taxable income. This includes itemizing deductions if they exceed the standard deduction, contributing to tax-deferred retirement accounts, and claiming eligible tax credits.

Example: Contributing to a traditional IRA or 401(k) can reduce your taxable income, while claiming credits like the Child Tax Credit or Earned Income Tax Credit can directly reduce your tax liability.

5.2. Tax-Advantaged Investments

Invest in tax-advantaged accounts like 401(k)s, IRAs, and HSAs to reduce your current and future tax liability. These accounts offer tax benefits such as tax-deferred growth, tax-deductible contributions, or tax-free withdrawals.

Example: Investing in a Roth IRA can provide tax-free withdrawals in retirement, while contributing to a health savings account (HSA) can allow you to pay for medical expenses with tax-free dollars.

5.3. Tax Planning Throughout the Year

Don’t wait until the end of the year to think about taxes. Engage in tax planning throughout the year to identify opportunities to reduce your tax liability. This includes estimating your income and deductions, adjusting your withholding or estimated tax payments, and making strategic financial decisions.

Example: If you anticipate a significant increase in income, consider increasing your estimated tax payments to avoid underpayment penalties.

5.4. Consult with a Tax Professional

Consider consulting with a qualified tax professional who can provide personalized advice based on your individual circumstances. A tax professional can help you navigate the complex tax laws, identify tax-saving opportunities, and ensure you are in compliance with IRS regulations.

Example: A tax professional can help you determine the most tax-efficient business structure, plan for major life events like marriage or divorce, and represent you in case of an audit.

6. Common Mistakes To Avoid When Filing Federal Income Tax

Filing your federal income tax return accurately and on time is essential to avoid penalties and interest. Here are some common mistakes to avoid:

6.1. Incorrect Filing Status

Choosing the wrong filing status can result in a higher tax liability. Make sure you choose the correct filing status based on your marital status and other factors. The most common filing statuses are:

- Single

- Married Filing Jointly

- Married Filing Separately

- Head of Household

- Qualifying Widow(er)

6.2. Overlooking Deductions and Credits

Many taxpayers overlook eligible deductions and credits, resulting in a higher tax liability. Make sure you review all possible deductions and credits to minimize your taxes.

Example: Common deductions include student loan interest, medical expenses, and charitable contributions, while common credits include the Child Tax Credit, Earned Income Tax Credit, and education credits.

6.3. Math Errors

Math errors are a common mistake that can lead to inaccuracies on your tax return. Double-check all calculations to ensure they are correct. Using tax preparation software can help minimize math errors.

6.4. Failure to Report All Income

Failing to report all income can result in penalties and interest. Make sure you report all sources of income, including wages, salaries, tips, self-employment income, investment income, and rental income.

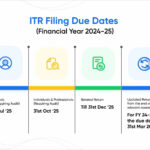

6.5. Missing the Filing Deadline

Missing the filing deadline can result in penalties and interest. The regular filing deadline is typically April 15, but you can request an extension if you need more time to file. However, an extension to file is not an extension to pay, so you should still pay any estimated taxes by the original deadline.

7. The Future Of Federal Income Tax: Potential Changes And Reforms

The federal income tax system is subject to ongoing debate and potential reforms. Here are some potential changes to watch for:

7.1. Tax Rate Changes

Tax rates and brackets can change due to legislation or economic conditions. Keep an eye on potential changes to tax rates, as they can significantly impact your tax liability.

Example: The Tax Cuts and Jobs Act of 2017 made significant changes to the tax rates and brackets, which are set to expire at the end of 2025 unless Congress acts to extend them.

7.2. Deduction and Credit Changes

Deductions and credits can also change due to legislation. Some deductions and credits may be expanded, while others may be phased out or eliminated.

Example: The standard deduction was significantly increased by the Tax Cuts and Jobs Act of 2017, but it is also set to revert to pre-2018 levels at the end of 2025.

7.3. Simplification Efforts

There have been ongoing efforts to simplify the tax code, making it easier for taxpayers to understand and comply with the tax laws. Simplification efforts could include reducing the number of tax brackets, eliminating certain deductions and credits, and making the tax filing process easier.

7.4. Impact of Economic Conditions

Economic conditions, such as inflation and unemployment, can also impact the tax system. Tax laws may be adjusted to address economic challenges and provide relief to taxpayers.

Example: During the COVID-19 pandemic, Congress enacted several tax relief measures, such as the Economic Impact Payments (stimulus checks) and expanded unemployment benefits.

8. How To Find Partners To Grow Your Income And Navigate Taxes

At income-partners.net, we specialize in connecting individuals and businesses to create synergistic partnerships that drive revenue growth. We also offer guidance on navigating the tax implications of these partnerships.

8.1. Identifying Potential Partners

Start by identifying potential partners who complement your skills, resources, and goals. Look for partners who bring unique expertise, access to new markets, or complementary products and services.

Example: A marketing consultant might partner with a web design agency to offer comprehensive digital marketing solutions to clients.

8.2. Building Strong Relationships

Building strong, trusting relationships with your partners is essential for long-term success. Communicate openly, establish clear expectations, and treat your partners with respect.

Example: Regularly scheduled meetings, transparent communication, and mutual support can help foster strong relationships.

8.3. Structuring Partnerships for Tax Efficiency

Work with a tax professional to structure your partnerships in a way that minimizes your tax liability. This may involve choosing the right business structure, allocating profits and losses effectively, and taking advantage of eligible deductions and credits.

Example: A partnership agreement can specify how profits and losses are allocated among partners, which can have significant tax implications.

8.4. Utilizing Income-Partners.Net Resources

Leverage the resources available at income-partners.net to find potential partners, learn about partnership strategies, and access tax-related information. Our platform offers a wealth of information and tools to help you succeed.

Example: Browse our directory of potential partners, read our articles on partnership best practices, and consult with our tax experts.

9. Real-Life Examples Of Successful Income-Generating Partnerships

To inspire you, here are some real-life examples of successful income-generating partnerships:

9.1. Software Company and Marketing Agency

A software company partners with a marketing agency to promote its products and services. The marketing agency provides expertise in digital marketing, content creation, and social media management, while the software company provides cutting-edge technology. This partnership helps both companies reach new customers and grow their revenue.

9.2. Restaurant and Local Farm

A restaurant partners with a local farm to source fresh, high-quality ingredients. The restaurant can offer customers unique dishes made with locally sourced ingredients, while the farm can sell its produce directly to the restaurant. This partnership supports local agriculture and enhances the restaurant’s reputation.

9.3. Real Estate Agent and Mortgage Broker

A real estate agent partners with a mortgage broker to offer clients comprehensive real estate services. The real estate agent helps clients find and purchase properties, while the mortgage broker helps them secure financing. This partnership streamlines the home-buying process and provides clients with a seamless experience.

9.4. Freelancer and Virtual Assistant

A freelancer partners with a virtual assistant to manage administrative tasks and client communications. The virtual assistant handles tasks like scheduling appointments, managing emails, and invoicing clients, allowing the freelancer to focus on their core skills and grow their business.

10. Frequently Asked Questions (FAQ) About Federal Income Tax

Here are some frequently asked questions about federal income tax:

10.1. What is the difference between a tax deduction and a tax credit?

A tax deduction reduces your taxable income, while a tax credit directly reduces your tax liability.

10.2. How do I determine my filing status?

Your filing status is determined by your marital status and other factors. Common filing statuses include single, married filing jointly, married filing separately, head of household, and qualifying widow(er).

10.3. What is the standard deduction for 2024?

The standard deduction for 2024 depends on your filing status. For example, the standard deduction for single filers is $14,600, while the standard deduction for married filing jointly is $29,200.

10.4. How do I itemize deductions?

To itemize deductions, you must complete Schedule A of Form 1040. Common itemized deductions include medical expenses, state and local taxes, mortgage interest, and charitable contributions.

10.5. What is the deadline for filing federal income tax?

The regular filing deadline is typically April 15, but you can request an extension if you need more time to file.

10.6. How do I pay my federal income tax?

You can pay your federal income tax online, by mail, or by phone. The IRS offers several payment options, including direct pay, electronic funds transfer, and credit or debit card.

10.7. What happens if I don’t pay my taxes on time?

If you don’t pay your taxes on time, you may be subject to penalties and interest. The penalty for failure to pay is typically 0.5% of the unpaid taxes for each month or part of a month that the taxes remain unpaid, up to a maximum of 25%.

10.8. How do I request an extension to file my taxes?

You can request an extension to file your taxes by completing Form 4868, Application for Automatic Extension of Time to File U.S. Individual Income Tax Return. The extension gives you an additional six months to file your return, but it does not extend the time to pay your taxes.

10.9. What is the difference between an employee and an independent contractor?

An employee is someone who works under the control and direction of an employer, while an independent contractor is someone who is self-employed and provides services to clients. The IRS has specific guidelines for determining whether someone is an employee or an independent contractor.

10.10. How do I handle a tax audit?

If you are selected for a tax audit, it’s important to cooperate with the IRS and provide all requested documentation. You may also want to consult with a tax professional to represent you during the audit.

By understanding the ins and outs of federal income tax and leveraging strategic partnerships, you can effectively manage your taxes and maximize your income-generating potential. Remember to visit income-partners.net to explore more opportunities and resources to help you achieve your financial goals.

Address: 1 University Station, Austin, TX 78712, United States. Phone: +1 (512) 471-3434. Website: income-partners.net.

Ready to take control of your financial future? Visit income-partners.net today to discover partnership opportunities, learn strategies for building strong relationships, and access expert tax advice. Don’t wait – start building your path to financial success now!