What Tax Form For Rental Income should you use to accurately report your earnings and deductions? Accurately reporting rental income is crucial for landlords to avoid penalties and ensure compliance with IRS regulations; income-partners.net provides expert insights and resources to navigate these complexities and optimize your rental income strategy with strategic partnerships. This comprehensive guide will clarify the tax forms required for reporting rental income, offering solutions to simplify the process and maximize your tax benefits, along with landlord resources, investment opportunities, and financial planning.

1. What Tax Form Do I Use to Report Rental Income?

The primary tax form for reporting rental income is Schedule E (Form 1040), Supplemental Income and Loss. This form is used to report income or loss from rental real estate, royalties, partnerships, S corporations, estates, trusts, and residual interests in REMICs.

1.1. Understanding Schedule E (Form 1040)

Schedule E is where you’ll detail all rental income received, deduct eligible expenses, and calculate your net rental income or loss. According to research from the University of Texas at Austin’s McCombs School of Business, in July 2025, properly utilizing Schedule E can significantly reduce your tax liability by accurately accounting for all deductible expenses.

1.1.1. Key Sections of Schedule E

-

Part I: Income or Loss From Rental Real Estate and Royalties

- Column A: Property A – Enter details for the first rental property.

- Column B: Property B – If you have multiple rental properties, use additional columns.

- Column 1: Enter the type of property (e.g., single-family residence, apartment).

- Column 2: Enter the street address.

- Column 3: Indicate if you were a material participant in the rental activity.

- Column 4: Enter gross rental income.

- Column 5: Enter total expenses.

-

Part II: Income or Loss From Partnerships and S Corporations

- Report income or losses from partnerships and S corporations.

-

Part III: Income or Loss From Estates and Trusts

- Report income or losses from estates and trusts.

-

Part IV: Income or Loss From Royalties

- Report royalty income.

-

Summary: Combine all income and losses from various sources to determine your total supplemental income or loss.

1.2. Who Needs to File Schedule E?

You need to file Schedule E if you:

- Received rental income from real estate you own.

- Have royalty income.

- Have income or losses from partnerships, S corporations, estates, or trusts.

1.3. What Information Do I Need to Complete Schedule E?

To complete Schedule E accurately, gather the following information:

- Rental Income: Total rent collected during the tax year.

- Rental Expenses:

- Advertising: Costs for advertising your rental property.

- Auto and Travel: Expenses for trips related to managing the property.

- Cleaning and Maintenance: Costs for cleaning and maintaining the property.

- Commissions: Fees paid to property managers or real estate agents.

- Insurance: Premiums for rental property insurance.

- Legal and Professional Fees: Costs for legal or accounting services.

- Management Fees: Fees paid to property managers.

- Mortgage Interest: Interest paid on the mortgage for the rental property.

- Repairs: Costs for repairing the property (not improvements).

- Supplies: Costs for supplies used for the rental property.

- Taxes: Property taxes paid.

- Utilities: Costs for utilities paid by the landlord.

- Depreciation: Deduction for the wear and tear of the property.

1.4. How to Calculate Rental Income

Rental income is the total rent you receive from tenants. However, calculating your taxable rental income involves more than just the rent payments.

1.4.1. Gross Rental Income

Gross rental income includes:

- Rent Payments: Regular rent payments from tenants.

- Advance Rent: Payments received for future rental periods.

- Security Deposits Used for Rent: Security deposits retained to cover unpaid rent.

1.4.2. Deductible Rental Expenses

You can deduct various expenses from your gross rental income to determine your net rental income. Common deductible expenses include:

- Mortgage Interest: The interest portion of your mortgage payments.

- Property Taxes: Real estate taxes paid on the property.

- Insurance: Premiums for fire, hazard, and liability insurance.

- Repairs and Maintenance: Costs to keep the property in good condition.

- Depreciation: A portion of the property’s cost recovered over its useful life.

1.4.3. Example Calculation

Let’s say you own a rental property and have the following income and expenses for the year:

- Gross Rental Income: $20,000

- Mortgage Interest: $5,000

- Property Taxes: $2,000

- Insurance: $1,000

- Repairs and Maintenance: $500

- Depreciation: $3,000

To calculate your net rental income:

Net Rental Income = Gross Rental Income - (Mortgage Interest + Property Taxes + Insurance + Repairs and Maintenance + Depreciation)

Net Rental Income = $20,000 - ($5,000 + $2,000 + $1,000 + $500 + $3,000)

Net Rental Income = $20,000 - $11,500

Net Rental Income = $8,500In this case, your net rental income, which you’ll report on Schedule E, is $8,500.

1.5. Common Mistakes to Avoid When Filing Schedule E

- Not Reporting All Income: Ensure you report all rental income, including advance rent and security deposits used for rent.

- Incorrectly Classifying Expenses: Distinguish between repairs (deductible) and improvements (capitalized and depreciated).

- Missing Depreciation Deductions: Don’t overlook depreciation, which can significantly reduce your taxable income.

- Failing to Keep Records: Maintain detailed records of all income and expenses to support your deductions.

1.6. Resources for Filing Schedule E

- IRS Website: The IRS provides detailed instructions and publications on Schedule E.

- Tax Software: Programs like TurboTax and H&R Block can guide you through the process.

- Tax Professionals: A CPA or tax advisor can provide personalized assistance.

- income-partners.net: Offers comprehensive resources, partnership opportunities, and expert advice to help you navigate rental income taxation and maximize your financial benefits.

By understanding and accurately completing Schedule E, you can ensure compliance with tax laws and optimize your rental income strategy. Don’t hesitate to seek professional help to navigate complex tax situations and make informed financial decisions.

landlord filing out tax documents

landlord filing out tax documents

2. What is Form 1099-K and Does It Apply to Rental Income?

Form 1099-K, Payment Card and Third Party Network Transactions, is an IRS information return used to report certain payment transactions to improve voluntary tax compliance. If you receive rental payments through third-party payment networks like PayPal, Venmo, or Zelle, you might receive Form 1099-K.

2.1. Understanding Form 1099-K

Form 1099-K reports the gross amount of payment card and third-party network transactions. The IRS implemented this form to ensure that individuals and businesses report all taxable income.

2.1.1. Key Information on Form 1099-K

- Gross Payment Volume: The total amount of payments you received through the payment platform.

- Number of Transactions: The total number of transactions processed.

- Payer Information: The name, address, and Taxpayer Identification Number (TIN) of the payment settlement entity.

- Payee Information: Your name, address, and TIN.

2.2. When Do You Receive Form 1099-K?

You will receive Form 1099-K if you meet both of the following conditions:

- Gross Payment Volume: The total amount of payments exceeds $20,000.

- Number of Transactions: You have more than 200 transactions.

However, the IRS has announced changes to these thresholds, which are discussed below.

2.3. New 1099-K Reporting Thresholds

The American Rescue Plan Act of 2021 significantly lowered the reporting threshold for Form 1099-K. Starting with the 2022 tax year (filed in 2023), the new thresholds were:

- Gross Payment Volume: More than $600.

- Number of Transactions: No minimum number of transactions.

However, the IRS has delayed the implementation of the $600 threshold. For the 2023 tax year (filed in 2024), the IRS provided a de minimis exception, raising the threshold to $20,000 and 200 transactions to ease the transition and reduce confusion. The IRS is planning a phased-in approach to implement the lower threshold in the future.

2.4. How Does Form 1099-K Affect Rental Income Reporting?

Even if you receive Form 1099-K, you must still report all rental income on Schedule E (Form 1040). The amount reported on Form 1099-K should match the gross rental income you report on Schedule E.

2.4.1. Reconciling Form 1099-K with Schedule E

If the amount on Form 1099-K doesn’t match your rental income, reconcile the differences. Common reasons for discrepancies include:

- Personal Transactions: The form might include payments for personal items sold through the same platform.

- Reimbursements: The form might include reimbursements for expenses, which are not considered income.

- Incorrect Reporting: The payment platform might have made an error in reporting.

Document any discrepancies and include an explanation when you file your taxes.

2.5. Best Practices for Handling Form 1099-K

- Keep Accurate Records: Maintain detailed records of all rental income and expenses.

- Track Payment Methods: Keep track of how you receive rental payments, especially through third-party payment platforms.

- Reconcile Payments: Regularly reconcile payments received with your records to ensure accuracy.

- Consult a Tax Professional: If you have questions or concerns about Form 1099-K, consult a tax professional.

2.6. Resources for Form 1099-K

- IRS Website: The IRS provides detailed information on Form 1099-K.

- Payment Platform Support: Payment platforms like PayPal and Venmo offer resources and support for understanding Form 1099-K.

- Tax Software: Tax software can help you reconcile Form 1099-K with your rental income.

- income-partners.net: Provides access to financial experts and resources to help you understand and manage the implications of Form 1099-K on your rental income, ensuring accurate tax reporting.

By understanding Form 1099-K and its implications for rental income reporting, you can ensure compliance with IRS regulations and avoid potential penalties. Keep accurate records and seek professional advice when needed to navigate this aspect of rental property taxation effectively.

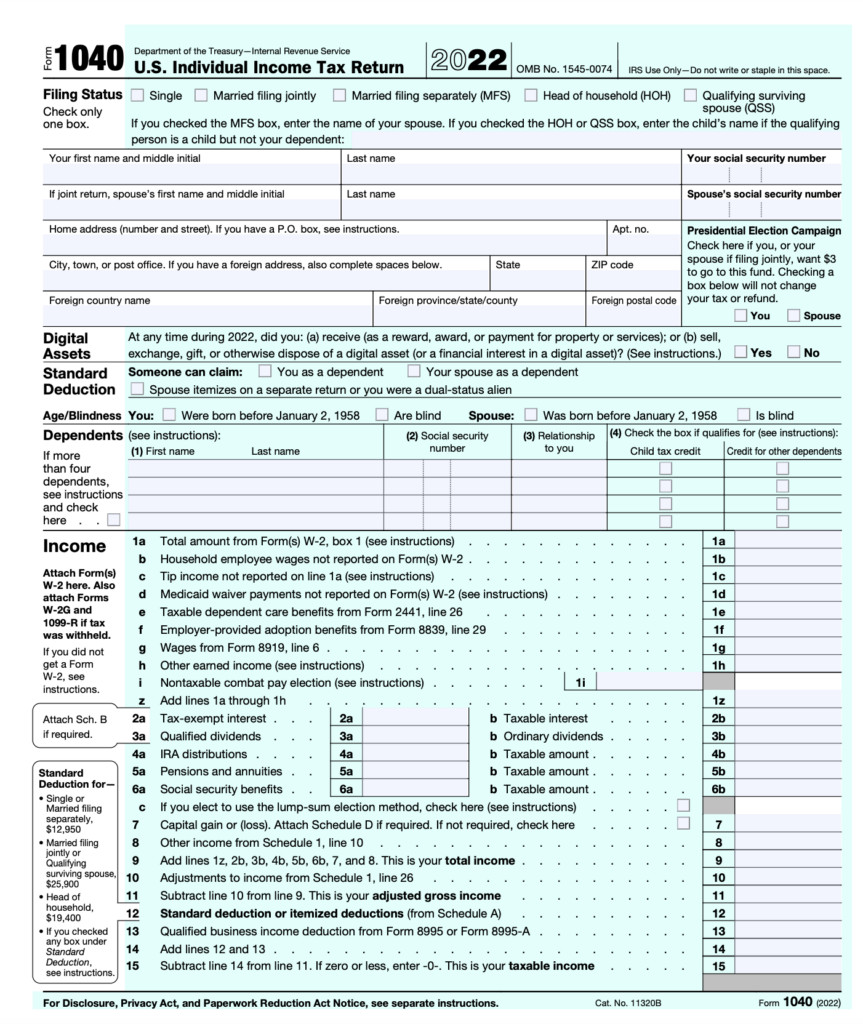

3. What is Form 1040 or 1040-SR (Schedule E)?

Form 1040 is the standard U.S. Individual Income Tax Return that taxpayers use to file their annual income tax returns. Schedule E (Form 1040) is attached to Form 1040 to report income or loss from rental real estate, royalties, partnerships, S corporations, estates, trusts, and residual interests in REMICs. Form 1040-SR is a version of Form 1040 designed for seniors.

3.1. Understanding Form 1040

Form 1040 is the primary form for calculating your total income tax liability. It includes sections for reporting various types of income, deductions, and credits.

3.1.1. Key Sections of Form 1040

- Identification Section: Your name, address, Social Security number, and filing status.

- Income Section: Wages, salaries, tips, interest, dividends, and other income sources.

- Adjustments to Income: Deductions like IRA contributions, student loan interest, and self-employment tax.

- Standard Deduction or Itemized Deductions: Choose the higher of the standard deduction or itemized deductions.

- Tax Calculation: Calculate your tax liability based on your taxable income and tax rates.

- Payments: Report taxes withheld from your wages, estimated tax payments, and credits.

- Refund or Amount You Owe: Determine if you are due a refund or if you owe additional taxes.

3.2. Understanding Schedule E (Form 1040)

Schedule E is where you report the details of your rental income and expenses. It helps you calculate your net rental income or loss, which is then transferred to Form 1040.

3.2.1. Key Sections of Schedule E

- Part I: Income or Loss From Rental Real Estate and Royalties

- Column A: Property A – Enter details for the first rental property.

- Column B: Property B – If you have multiple rental properties, use additional columns.

- Column 1: Enter the type of property (e.g., single-family residence, apartment).

- Column 2: Enter the street address.

- Column 3: Indicate if you were a material participant in the rental activity.

- Column 4: Enter gross rental income.

- Column 5: Enter total expenses.

- Part II: Income or Loss From Partnerships and S Corporations

- Report income or losses from partnerships and S corporations.

- Part III: Income or Loss From Estates and Trusts

- Report income or losses from estates and trusts.

- Part IV: Income or Loss From Royalties

- Report royalty income.

- Summary: Combine all income and losses from various sources to determine your total supplemental income or loss.

3.3. How to Fill Out Form 1040 and Schedule E for Rental Income

-

Fill Out Form 1040:

- Complete the identification section with your personal information.

- Report all sources of income, including wages, interest, and dividends.

- Calculate your adjustments to income and deductions.

- Determine your taxable income and calculate your tax liability.

-

Complete Schedule E:

- Enter the address and type of each rental property you own.

- Report your gross rental income for each property.

- Deduct all eligible rental expenses, such as mortgage interest, property taxes, insurance, and repairs.

- Calculate your depreciation expense.

- Determine your net rental income or loss for each property.

- Combine the net income or loss from all rental properties to determine your total rental income or loss.

-

Transfer to Form 1040:

- Transfer your total rental income or loss from Schedule E to line 8 of Form 1040.

- Complete the remaining sections of Form 1040 to calculate your total tax liability or refund.

3.4. Form 1040-SR for Seniors

Form 1040-SR is designed for taxpayers age 65 or older. It uses the same schedules and instructions as Form 1040 but has a larger font size and a standard deduction amount that reflects the increased standard deduction for seniors.

3.4.1. Key Features of Form 1040-SR

- Larger Font Size: Easier to read for seniors.

- Standard Deduction: Automatically includes the increased standard deduction for seniors.

- Schedule E Compatibility: Uses the same Schedule E for reporting rental income.

3.5. Best Practices for Filing Form 1040 and Schedule E

- Keep Accurate Records: Maintain detailed records of all income and expenses.

- Use Tax Software: Tax software can help you accurately complete Form 1040 and Schedule E.

- Consult a Tax Professional: If you have complex tax situations, consult a tax professional.

- File on Time: Ensure you file your taxes by the deadline to avoid penalties.

3.6. Resources for Form 1040 and Schedule E

- IRS Website: The IRS provides detailed instructions and publications for Form 1040 and Schedule E.

- Tax Software: Programs like TurboTax and H&R Block offer guidance and support.

- Tax Professionals: A CPA or tax advisor can provide personalized assistance.

- income-partners.net: Offers resources, tools, and expert advice to help you accurately file Form 1040 and Schedule E, ensuring you maximize your tax benefits and comply with IRS regulations.

By understanding and accurately completing Form 1040 and Schedule E, you can ensure compliance with tax laws and optimize your tax strategy. Seek professional help when needed to navigate complex tax situations and make informed financial decisions.

form 1040 example

form 1040 example

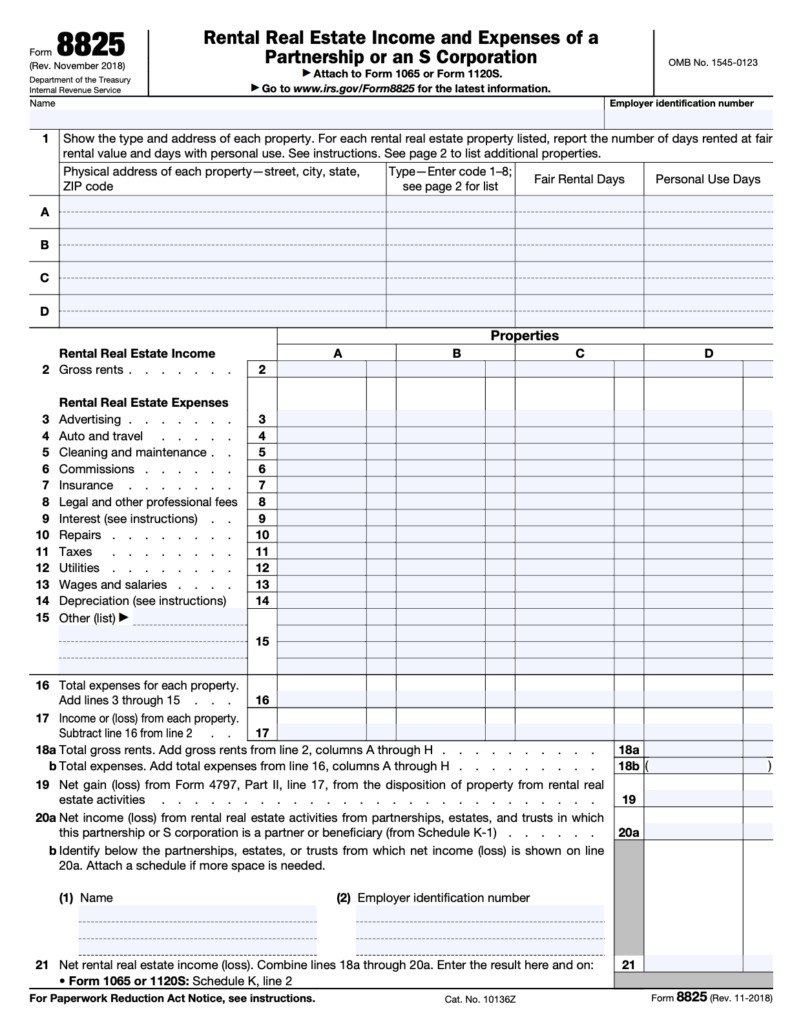

4. What is Form 8825 and When Do I Need to Use It?

If your rental property is owned and operated through a partnership or S corporation, you’ll use Form 8825, Rental Real Estate Income and Expenses of a Partnership or an S Corporation, to report income and deductible expenses from the rental properties.

4.1. Understanding Form 8825

Form 8825 is used by partnerships and S corporations to report income and expenses from rental real estate activities. The information reported on Form 8825 is then used to calculate the entity’s taxable income or loss, which is passed through to the partners or shareholders.

4.1.1. Key Sections of Form 8825

- Identification Section: The name, address, and Employer Identification Number (EIN) of the partnership or S corporation.

- Income Section: Gross rental income from each rental property.

- Deductions Section: Expenses related to the rental properties, such as mortgage interest, property taxes, insurance, and depreciation.

- Net Income or Loss: The net income or loss from rental real estate activities, which is allocated to the partners or shareholders.

4.2. Who Needs to File Form 8825?

You need to file Form 8825 if you are a partnership or S corporation that owns and operates rental real estate. This includes:

- Partnerships: Entities with two or more partners engaged in a business for profit.

- S Corporations: Corporations that have elected to pass their income, losses, deductions, and credits through to their shareholders.

4.3. How to Fill Out Form 8825

-

Identification Section:

- Enter the name, address, and EIN of the partnership or S corporation.

-

Income Section:

- Report the gross rental income from each rental property.

- Include all income received from tenants, such as rent payments and other charges.

-

Deductions Section:

- Deduct all eligible rental expenses, such as mortgage interest, property taxes, insurance, and repairs.

- Calculate and deduct depreciation expense for each rental property.

- Include any other deductible expenses related to the rental properties.

-

Net Income or Loss:

- Calculate the net income or loss from rental real estate activities.

- Allocate the net income or loss to the partners or shareholders based on their ownership interests.

4.4. Relationship to Form 1065 and Form 1120-S

Form 8825 is used in conjunction with Form 1065 (U.S. Return of Partnership Income) and Form 1120-S (U.S. Income Tax Return for an S Corporation). The net income or loss from Form 8825 is reported on these forms and then passed through to the partners or shareholders.

4.4.1. Form 1065 (Partnerships)

- Partnerships file Form 1065 to report their income, deductions, and credits.

- The net income or loss from Form 8825 is reported on Form 1065 and then allocated to the partners on Schedule K-1.

4.4.2. Form 1120-S (S Corporations)

- S corporations file Form 1120-S to report their income, deductions, and credits.

- The net income or loss from Form 8825 is reported on Form 1120-S and then allocated to the shareholders on Schedule K-1.

4.5. Best Practices for Filing Form 8825

- Keep Accurate Records: Maintain detailed records of all income and expenses related to the rental properties.

- Understand Partnership or S Corporation Agreements: Ensure you understand the terms of your partnership or S corporation agreement, including how income and losses are allocated to the partners or shareholders.

- Consult a Tax Professional: If you have complex tax situations, consult a tax professional.

- File on Time: Ensure you file Form 8825 and the related partnership or S corporation tax returns by the deadline to avoid penalties.

4.6. Resources for Form 8825

- IRS Website: The IRS provides detailed instructions and publications for Form 8825, Form 1065, and Form 1120-S.

- Tax Software: Tax software can help you accurately complete Form 8825 and the related tax returns.

- Tax Professionals: A CPA or tax advisor can provide personalized assistance.

- income-partners.net: Provides resources, tools, and expert advice to help partnerships and S corporations accurately file Form 8825, ensuring compliance with IRS regulations and maximizing tax benefits for their rental real estate activities.

By understanding and accurately completing Form 8825, you can ensure compliance with tax laws and optimize your tax strategy for rental properties owned and operated through partnerships or S corporations. Seek professional help when needed to navigate complex tax situations and make informed financial decisions.

form 8825 example

form 8825 example

5. Deductible Rental Property Expenses: What Can You Claim?

One of the significant benefits of owning rental property is the ability to deduct various expenses, reducing your taxable income. Understanding which expenses are deductible can help you maximize your tax savings.

5.1. Common Deductible Expenses

- Mortgage Interest: You can deduct the interest portion of your mortgage payments on Schedule E.

- Property Taxes: Real estate taxes paid on the rental property are deductible.

- Insurance: Premiums for fire, hazard, and liability insurance are deductible.

- Repairs and Maintenance: Expenses for keeping the property in good condition, such as fixing leaks, painting, and replacing broken windows, are deductible.

- Advertising: Costs for advertising your rental property to attract tenants are deductible.

- Management Fees: Fees paid to property managers are deductible.

- Legal and Professional Fees: Costs for legal and accounting services related to your rental property are deductible.

- Utilities: If you pay for utilities on behalf of your tenants, you can deduct these expenses.

- Depreciation: You can deduct a portion of the property’s cost over its useful life.

- Travel Expenses: Costs for traveling to and from the rental property for management purposes are deductible.

5.2. Repairs vs. Improvements

It’s important to distinguish between repairs and improvements. Repairs are expenses that keep the property in good condition, while improvements add value or extend the property’s useful life.

- Repairs: Deductible in the year they are incurred. Examples include fixing a leaky faucet, painting, and replacing broken windows.

- Improvements: Capitalized and depreciated over their useful life. Examples include adding a new roof, installing central air conditioning, and adding a room.

5.3. Depreciation: A Key Deduction

Depreciation allows you to deduct a portion of the cost of your rental property over its useful life. The IRS provides guidelines for determining the useful life of different types of property.

5.3.1. How to Calculate Depreciation

The most common method for calculating depreciation is the Modified Accelerated Cost Recovery System (MACRS). Under MACRS, residential rental property is depreciated over 27.5 years.

To calculate depreciation:

- Determine the Basis: The basis is typically the cost of the property plus any improvements, minus land value.

- Calculate Annual Depreciation: Divide the basis by 27.5 to determine the annual depreciation expense.

5.3.2. Example Calculation

Suppose you purchased a rental property for $200,000, excluding the land value. Your annual depreciation expense would be:

Annual Depreciation = $200,000 / 27.5

Annual Depreciation = $7,272.73You can deduct $7,272.73 each year for 27.5 years.

5.4. Limits on Deductions

There are limits on certain deductions, such as the passive activity loss rules, which may limit the amount of rental losses you can deduct if you don’t materially participate in the rental activity.

5.4.1. Passive Activity Loss Rules

Rental activities are generally considered passive activities. This means that you can only deduct rental losses up to the amount of your passive income. However, there is an exception for taxpayers who actively participate in the rental activity and have an adjusted gross income (AGI) of $100,000 or less. These taxpayers can deduct up to $25,000 in rental losses.

5.5. Record Keeping

Accurate record keeping is essential for claiming rental property expenses. Keep receipts, invoices, and other documentation to support your deductions.

5.5.1. Best Practices for Record Keeping

- Separate Bank Account: Use a separate bank account for rental income and expenses.

- Accounting Software: Use accounting software like QuickBooks or Xero to track your income and expenses.

- Digital Copies: Scan and save digital copies of all receipts and invoices.

- Organize Records: Organize your records by category and tax year.

5.6. Resources for Deductible Rental Property Expenses

- IRS Website: The IRS provides detailed information on deductible rental property expenses.

- Tax Software: Tax software can help you track and deduct your rental property expenses.

- Tax Professionals: A CPA or tax advisor can provide personalized assistance.

- income-partners.net: Offers comprehensive resources, expert advice, and tools to help you identify and claim all eligible rental property expenses, maximizing your tax savings and ensuring compliance with IRS regulations.

By understanding deductible rental property expenses and keeping accurate records, you can optimize your tax strategy and reduce your tax liability. Seek professional help when needed to navigate complex tax situations and make informed financial decisions.

6. Understanding Material Participation and Its Impact on Rental Income Taxes

Material participation in a rental activity can significantly impact how your rental income is taxed. It determines whether your rental income is considered active or passive, affecting the deductibility of losses.

6.1. What is Material Participation?

Material participation means you are actively involved in the operation of your rental property on a regular, continuous, and substantial basis. The IRS has specific tests to determine if you meet the material participation standard.

6.1.1. IRS Material Participation Tests

You are considered to materially participate in a rental activity if you meet any of the following tests:

-

More Than 500 Hours: You participate in the activity for more than 500 hours during the tax year.

-

Substantially All Participation: Your participation constitutes substantially all of the participation in the activity by all individuals.

-

More Than 100 Hours and More Than Anyone Else:

- You participate in the activity for more than 100 hours during the tax year.

- Your participation is not less than the participation of any other individual.

-

Significant Participation Activities:

- The activity is a significant participation activity (SPA).

- Your aggregate participation in all SPAs during the year exceeds 500 hours.

-

Material Participation for Any Five Years: You materially participated in the activity for any five of the past ten tax years.

-

Personal Service Activity: The activity is a personal service activity, and you materially participated in the activity for any three prior tax years.

-

Facts and Circumstances: Based on all the facts and circumstances, you participate in the activity on a regular, continuous, and substantial basis during the tax year.

6.2. Active vs. Passive Rental Income

- Active Income: Income earned from activities in which you materially participate. Active income is subject to self-employment tax and is not subject to the passive activity loss rules.

- Passive Income: Income earned from activities in which you do not materially participate. Passive income is not subject to self-employment tax but is subject to the passive activity loss rules.

6.3. Impact on Deductibility of Losses

If you materially participate in your rental activity, you can deduct rental losses against your other income without being subject to the passive activity loss rules. However, if you do not materially participate, your rental losses may be limited to the amount of your passive income.

6.3.1. Passive Activity Loss Rules

The passive activity loss rules limit the amount of rental losses you can deduct if you do not materially participate in the rental activity. You can only deduct rental losses up to the amount of your passive income. Any excess losses are carried forward to future years and can be deducted when you have passive income or when you sell the property.

6.3.2. Exception for Active Participation

There is an exception to the passive activity loss rules for taxpayers who actively participate in the rental activity and have an AGI of $100,000 or less. These taxpayers can deduct up to $25,000 in rental losses. The $25,000 allowance is reduced by 50% of the amount by which your AGI exceeds $100,000 and is completely phased out when your AGI reaches $150,000.

6.4. How to Prove Material Participation

To prove material participation, keep detailed records of your involvement in the rental activity. This includes:

- Time Logs: Keep a log of the hours you spend managing and operating the rental property.

- Receipts and Invoices: Keep receipts and invoices for all expenses related to the rental property.

- Correspondence: Keep copies of all correspondence with tenants, contractors, and property managers.

- Travel Records: Keep records of any travel related to the rental property.

6.5. Examples of Material Participation Activities

- Tenant Screening: Interviewing and screening potential tenants.

- Lease Negotiations: Negotiating lease terms with tenants.

- Property Maintenance: Performing repairs and maintenance on the property.

- Rent Collection: Collecting rent payments from tenants.

- Property Management: Managing the day-to-day operations of the rental property.

6.6. Resources for Understanding Material Participation

- IRS Website: The IRS provides detailed information on material participation and the passive activity loss rules.

- Tax Software: Tax software can help you determine if you materially participate in your rental activity.

- Tax Professionals: A CPA or tax advisor can provide personalized assistance.

- income-partners.net: Offers resources, tools, and expert advice to help you understand and navigate the complexities of material participation in rental activities, ensuring you optimize your tax strategy and maximize your benefits.

By understanding material participation and its impact on rental income taxes, you can make informed decisions about your involvement in your rental property and optimize your tax strategy. Seek professional help when needed to navigate complex tax situations and make informed financial decisions.

7. What are Qualified Business Income (QBI) Deductions for Rental Property Owners?

The Qualified Business Income (QBI) deduction, also known as the Section 199A deduction, allows eligible self-employed and small business owners to deduct up to 20% of their qualified business income. Rental property owners may be eligible for this deduction, providing significant tax savings.

7.1. Understanding QBI

Qualified Business Income (QBI) is the net amount of income, gains, deductions, and losses from a qualified trade or business. It includes rental income but excludes certain items, such as capital gains or losses, interest income, and wage income.

7.1.1. What Qualifies as a Trade or Business?

For rental property owners, the key question is whether their rental activity qualifies as a trade or business. The IRS has not provided a clear definition, but generally, a rental activity is more likely to be considered a trade or business if it is conducted with regularity, continuity, and substantiality.

7.2. Eligibility for the QBI Deduction

To be eligible for the QBI deduction, you must meet certain requirements:

-

Qualified Trade or Business: Your rental activity must qualify as a trade or business.

-

Taxable Income Limits:

- Below Threshold: If your taxable income is below $182,100 (single) or $364,200 (married filing jointly) for 2023, you can generally deduct up to 20% of your QBI.

- Above Threshold: If your taxable income is above these thresholds, the QBI deduction may be limited.

-

Rental Real Estate Enterprise (RREE) Election: You can make a formal election to treat all similar rental properties as a single enterprise for the QBI deduction.

7.3. Calculating the QBI Deduction

The QBI deduction is generally the smaller of:

- 20% of your Qualified Business Income (QBI).

- 20% of your taxable income (excluding capital gains).

However, if your taxable income is above the thresholds, the deduction may be limited based on wage and capital limitations.

7.3.1. Wage and Capital Limitations

If your taxable income is above the thresholds, the QBI deduction is limited to the greater of:

- 50% of the W-2 wages paid by the qualified trade or business.

- 25% of the W-2 wages plus 2.5% of the unadjusted basis of qualified property.

7.4. Safe Harbor for Rental Real Estate Activities

The IRS has provided a safe harbor under Revenue Procedure 2019-38 for rental real estate activities to qualify as a trade or business for the QBI deduction. To meet the safe harbor requirements, you must:

- Separate Books and Records: Maintain separate books and records for each rental activity.

- 250 Hours of Services: Perform at least 250 hours of services during the tax year with respect to the rental activity.

- Contemporaneous Records: Maintain contemporaneous records of the services performed, including dates, hours, and descriptions.

7.5. Services That Count Towards the 250-Hour Requirement

- Advertising and Marketing: Advertising and marketing the rental property.

- Lease Negotiation: Negotiating and executing leases.

- Rent Collection: Collecting rent payments.

- Property Management: Managing the day-to-day operations of the rental property.

- Repairs and Maintenance: Performing repairs and maintenance on the property.

7.6. Examples of How the QBI Deduction Works

Example 1: Taxable Income Below Threshold

- QBI: $50,000

- Taxable Income: $40,000

- QBI Deduction: Smaller of (20% of $50,000) or (20% of $40,000) = $8,000

Example 2: Taxable Income Above Threshold

- QBI: $200,000

- Taxable Income: $400,000

- W-2 Wages: $50,000

- Unadjusted Basis of Qualified Property: $100,000

- QBI Deduction: Limited to the greater of (50% of $50,000) or (25% of $50,000 + 2.5% of $100,000) = $27,500

7.7. Resources for Understanding QBI Deductions

- IRS Website: The IRS provides detailed information on the QBI deduction.

- Tax Software: Tax software can help you calculate and claim the QBI deduction.

- Tax Professionals: A CPA or tax advisor can provide personalized assistance.

- income-partners.net: Offers comprehensive resources, expert advice, and tools to help rental property owners understand and claim the QBI deduction, maximizing their tax savings and ensuring compliance with IRS regulations.

By understanding the QBI deduction and its requirements, you can potentially reduce your tax liability and increase your after-tax income. Seek professional help when needed to navigate complex tax situations and make informed financial decisions.

8. Utilizing a Qualified CPA for Rental Income Tax Preparation

Navigating the complexities of rental income tax preparation can be daunting. Engaging a qualified Certified Public Accountant (CPA) can provide significant benefits, ensuring accuracy, compliance, and maximized tax savings.

8.1. What is a Certified Public Accountant (CPA)?

A Certified Public Accountant (CPA) is a licensed professional who has met rigorous education, examination, and experience requirements. CPAs are qualified to provide a wide range of accounting, tax, and financial services.

8.1.1. Key Qualifications of a CPA

- Education: CPAs typically have a bachelor’s or master’s degree in accounting.

- Examination: CPAs must pass the Uniform CPA Examination, a challenging exam covering accounting, auditing, taxation, and business law.

- Experience: CPAs must have a certain amount of professional experience, typically one to two years, under the supervision of a licensed CPA.

- Licensing: CPAs must be licensed by a state board of accountancy and are subject to ongoing continuing education requirements.

8.2. Benefits of Hiring a CPA for Rental Income Tax Preparation

- Expertise and Knowledge: CPAs have in-depth knowledge of tax laws and regulations, ensuring accuracy and compliance.

- Tax Planning: CPAs can help you develop tax planning strategies to minimize your tax liability.

- Deduction Optimization: CPAs can identify all eligible deductions and credits, maximizing your tax savings.

- Audit Representation: CPAs can represent you in the event of an IRS audit.

- Time Savings: Hiring a CPA frees up your time to focus on managing your rental property.

- Peace of Mind: Knowing that your taxes are being prepared by a qualified professional provides peace of mind.

8.3. How a CPA Can Help with Rental Income Taxes

- Accurate Reporting: CPAs can ensure that all rental income and expenses are accurately reported on Schedule E and other relevant tax forms.

- Deduction Identification: CPAs can help you identify all eligible deductions, such as mortgage interest, property taxes, insurance, repairs, and depreciation.

- Depreciation Calculation: CPAs can accurately calculate depreciation expense, maximizing your tax savings.

- QBI Deduction: CPAs can help you determine if you are eligible for the QBI deduction and calculate the correct amount.

- Material Participation: CPAs can help you determine if you materially participate in your rental activity, affecting the deductibility of losses.

- Audit Support: CPAs can represent you in the event of an IRS audit, providing guidance and support.

8.4. How to Find a Qualified CPA

- Referrals: Ask for referrals from friends, family, or other business owners.

- Online Directories: Use online directories, such as the AICPA’s CPA Locator, to find CPAs in your area.

- State Boards of Accountancy: Contact your state board of accountancy to verify that a CPA is licensed and in good standing.

- Professional Organizations: Check with professional organizations, such as the National Association of Tax Professionals (NATP), for referrals.

8.5. Questions to Ask a Potential CPA

- Experience: How much experience do you have preparing rental income taxes?

- Qualifications: Are you a licensed CPA in good standing?

- Fees: How do you charge for your services?

- References: Can you provide references from other clients?

- Communication: How often will we communicate, and what is your preferred method of communication?

8.6. Resources for Finding and Utilizing a CPA

- AICPA Website: The American Institute of Certified Public Accountants (AICPA) provides resources for finding and working with a CPA.

- State Boards of Accountancy: Your state board of accountancy can provide information on licensed CPAs in your area.

- Online Directories: Online directories, such as the CPA Locator, can help you find CPAs in your area.

- income-partners.net: Offers access to a network of qualified CPAs specializing in rental income tax preparation, ensuring you receive expert guidance and support to optimize your tax strategy and maximize your savings.

By engaging a qualified CPA for rental income tax preparation, you can ensure accuracy, compliance, and maximized tax savings. Take the time to find a CPA who is knowledgeable, experienced, and a good fit for your needs.

9. Tax Planning Strategies for Rental Income

Effective tax planning is crucial for rental property owners to minimize their tax liability and maximize their after-tax income. By implementing strategic tax planning strategies, you can optimize your financial position and achieve your investment goals.

9.1. Depreciation Strategies

Depreciation is a key deduction for rental property owners. By understanding depreciation rules and strategies, you can maximize your tax savings.

9.1.1. Cost Segregation

Cost segregation is a tax planning strategy that involves identifying and reclassifying certain building components as personal property rather than real property. Personal property has a shorter depreciation life, allowing you to accelerate depreciation deductions.

9.1.2. Bonus Depreciation

Bonus depreciation allows you to deduct a significant portion of the cost of new or used property in the year it is placed in service. For example, you may be able to deduct 80% of the cost of a new appliance in the first year.

9.2. Maximizing Deductible Expenses

By identifying and claiming all eligible deductions, you can significantly reduce your taxable income.

9.2.1. Travel Expenses

You can deduct travel expenses related to managing your rental property, such as trips to inspect the property, meet with tenants, or perform repairs.

9.2.2. Home Office Deduction

If you use a portion of your home exclusively and regularly for managing your rental property, you may be able to deduct home office expenses.

9.3. Rental Real Estate Enterprise (RREE) Election

The Rental Real Estate Enterprise (RREE) election allows you to treat all similar rental properties as a single enterprise for the QBI deduction. This can simplify your tax preparation and potentially increase your QBI deduction.

9.4. 1031 Exchanges

A 1031 exchange allows you to defer capital gains taxes when selling a rental property and reinvesting the proceeds in a like-kind property. This can be a powerful strategy for building wealth and deferring taxes.

9.5. Qualified Opportunity Zones (QOZ)

Qualified Opportunity Zones (QOZ) are economically distressed communities where new investments may be eligible for preferential tax treatment. Investing in a QOZ can provide significant tax benefits, such as deferral, reduction, and elimination of capital gains taxes.

9.6. Estate Planning

Proper estate planning can help you minimize estate taxes and ensure that your rental property is transferred to your heirs in a tax-efficient manner.

9.7. Resources for Tax Planning Strategies

- IRS Website: The IRS provides detailed information on tax planning strategies for rental property owners.

- Tax Software: Tax software can help you implement tax planning strategies.

- Tax Professionals: A CPA or tax advisor can provide personalized assistance.

- income-partners.net: Offers comprehensive resources, expert advice, and tools to help rental property owners develop and implement effective tax planning strategies, minimizing their tax liability and maximizing their after-tax income.

By implementing these tax planning strategies, you can optimize your financial position and achieve your investment goals. Seek professional help when needed to navigate complex tax situations and make informed financial decisions.

10. Common Mistakes to Avoid When Filing Rental Income Taxes

Filing rental income taxes can be complex, and it’s easy to make mistakes that can result in penalties or missed tax savings. Avoiding these common errors can ensure accuracy and compliance.

10.1. Not Reporting All Rental Income

Failing to report all rental income is a common mistake. Make sure to include all rent payments, security deposits used for rent, and other income related to your rental property.

10.2. Incorrectly Classifying Expenses

Distinguishing between repairs and improvements is crucial. Repairs are deductible in the year they are incurred, while improvements must be capitalized and depreciated.

10.3. Missing Depreciation Deductions

Depreciation is a significant deduction for rental property owners. Don’t overlook depreciation, and make sure to calculate it accurately.

10.4. Not Keeping Accurate Records

Accurate record keeping is essential for claiming rental property expenses. Keep receipts, invoices, and other documentation to support your deductions.

10.5. Failing to Meet Material Participation Requirements

If you want to deduct rental losses against your other income, you must meet the material participation requirements. Keep detailed records of your involvement in the rental activity to prove material participation.

10.6. Ignoring Passive Activity Loss Rules

The passive activity loss rules can limit the amount of rental losses you can deduct. Understand these rules and how they apply to your situation.

10.7. Not Claiming All Eligible Deductions

Make sure to claim all eligible deductions, such as mortgage interest, property taxes, insurance, repairs, and advertising.

10.8. Failing to File on Time

Filing your taxes on time is essential to avoid penalties. Make sure to file your taxes by the deadline or request an extension.

10.9. Not Consulting a Tax Professional

Consulting a tax professional can help you avoid mistakes and maximize your tax savings. A CPA or tax advisor can provide personalized assistance and guidance.

10.10. Resources for Avoiding Mistakes

- IRS Website: The IRS provides detailed information on rental income taxes and common mistakes to avoid.

- Tax Software: Tax software can help you avoid mistakes and accurately prepare your taxes.

- Tax Professionals: A CPA or tax advisor can provide personalized assistance and guidance.

- income-partners.net: Offers comprehensive resources, expert advice, and tools to help rental property owners avoid common mistakes when filing rental income taxes, ensuring accuracy, compliance, and maximized tax savings.

By avoiding these common mistakes, you can ensure accuracy, compliance, and maximized tax savings. Seek professional help when needed to navigate complex tax situations and make informed financial decisions.

Are you ready to optimize your rental income strategy and ensure compliance with IRS regulations? Visit income-partners.net today to explore partnership opportunities, access expert advice, and connect with a network of qualified professionals who can help you maximize your tax benefits and achieve your financial goals through strategic real estate partnerships. Unlock your full potential and start building a successful future with us!

Frequently Asked Questions (FAQ)

1. What is the primary tax form for reporting rental income?

The primary tax form is Schedule E (Form 1040), Supplemental Income and Loss.

2. What is Form 1099-K, and does it apply to rental income?

Form 1099-K reports payments received through third-party payment networks. If you meet the IRS thresholds, you’ll receive this form, but you must still report all rental income on Schedule E.

3. What are some common deductible rental property expenses?

Common deductions include mortgage interest, property taxes, insurance, repairs, and depreciation.

4. What is material participation, and why is it important?

Material participation means you are actively involved in your rental property’s operation, affecting the deductibility of losses.

5. What is the Qualified Business Income (QBI) deduction?

The QBI deduction allows eligible rental property owners to deduct up to 20% of their qualified business income.

6. How can a CPA help with rental income taxes?

A CPA can provide expertise, tax planning, deduction optimization, and audit representation.

7. What are some key tax planning strategies for rental income?

Strategies include depreciation, maximizing deductible expenses, 1031 exchanges, and Qualified Opportunity Zones (QOZ).

8. What are some common mistakes to avoid when filing rental income taxes?

Common mistakes include not reporting all income, incorrectly classifying expenses, and missing depreciation deductions.

9. What is the Rental Real Estate Enterprise (RREE) election?

The RREE election allows you to treat all similar rental properties as a single enterprise for the QBI deduction.

10. How do I prove material participation in my rental activity?

Keep detailed records of your involvement, including time logs, receipts, correspondence, and travel records.

Address: 1 University Station, Austin, TX 78712, United States.

Phone: +1 (512) 471-3434.

Website: income-partners.net.