What Percentage Should Your Car Payment Be From Income? Ideally, your car payment should not exceed 10-15% of your monthly take-home pay, ensuring financial stability and flexibility to pursue partnership opportunities that boost your revenue with income-partners.net. By adhering to this guideline, you’ll maintain a healthy financial balance, enabling you to explore strategic alliances, investment ventures, and collaborative projects to maximize your earnings potential. Learn how to manage your debt-to-income ratio, affordable car ownership and improve your financial wellness.

1. How Much Car Can I Afford Based on My Income?

You can generally afford a car payment that aligns with 10–15% of your monthly take-home pay, which will ensure financial stability. If you earn $3,000 per month after taxes, your car payment should ideally range from $300 to $450. Staying within this range allows room for other essential expenses and investment opportunities. Let’s delve deeper into factors that will help determine affordability.

Understanding the Income-to-Car Payment Ratio

The ratio of your car payment to your income is a crucial metric in personal finance. A manageable car payment ensures you have enough funds for other financial goals. According to a financial advisor, “Keeping your car payment within a reasonable percentage of your income is vital for maintaining a healthy financial life.”

Setting a Realistic Monthly Car Budget

To set a realistic monthly car budget, start by calculating your total monthly take-home pay. This is your income after taxes and other deductions. Once you have this figure, you can determine the appropriate range for your car payment. For example, if your monthly take-home pay is $5,000, a 10–15% allocation would suggest a car payment between $500 and $750.

Factors to Consider Beyond the Car Payment

Beyond the car payment, there are additional factors to consider:

- Insurance: Car insurance costs can vary widely based on your location, driving history, and the type of vehicle.

- Fuel: Fuel costs depend on your driving habits and the fuel efficiency of the car.

- Maintenance: Routine maintenance such as oil changes, tire rotations, and other repairs can add up.

For example, someone living in Austin, TX, might find that their car insurance and fuel costs are higher than in other areas due to traffic and local prices. It’s essential to factor in these costs when determining affordability.

2. What Expenses Should I Include When Calculating Car Affordability?

When calculating car affordability, include all associated costs such as fuel, insurance, maintenance, and potential repairs, in addition to the car payment itself. This comprehensive approach ensures you have a clear picture of the true cost of owning a car. Not factoring in all expenses is one of the most frequent reasons for financial difficulties related to car ownership.

Comprehensive List of Car-Related Expenses

To get a realistic view of what you can afford, consider the following expenses:

- Car Payment: The monthly payment you make on your car loan or lease.

- Insurance: The monthly premium for your auto insurance policy.

- Fuel: The cost of gasoline or electricity to power your vehicle.

- Maintenance: Routine maintenance like oil changes, tire rotations, and inspections.

- Repairs: Unexpected repairs due to mechanical issues or accidents.

- Registration and Taxes: Annual fees for registering your vehicle and any applicable taxes.

Using Online Calculators for Accurate Estimates

Several online calculators can help you estimate these costs. Websites like Edmunds and Kelley Blue Book offer tools to calculate the total cost of ownership, including depreciation, insurance, and maintenance. These calculators provide a more accurate picture of the financial commitment involved.

Budgeting for Unexpected Car Repairs

It’s wise to set aside funds for unexpected car repairs. According to a study by AAA, the average cost of car repairs can range from $500 to $600 per year. Creating an emergency fund specifically for car-related issues can prevent you from derailing your budget when these expenses arise.

Illustration of several essential car maintenance items, with an emphasis on tires, oil changes, and brakes

Illustration of several essential car maintenance items, with an emphasis on tires, oil changes, and brakes

3. How Does My Credit Score Affect My Car Payment Affordability?

Your credit score significantly impacts your car payment affordability by influencing the interest rate you receive on your car loan. A higher credit score typically results in lower interest rates, making the car more affordable over the loan term. Conversely, a lower credit score can lead to higher interest rates, increasing your monthly payments and the total cost of the vehicle.

The Impact of Credit Score on Interest Rates

Your credit score is a numerical representation of your creditworthiness, ranging from 300 to 850. Lenders use this score to assess the risk of lending you money. A higher credit score indicates a lower risk, resulting in more favorable loan terms.

- Excellent Credit (750+): You’ll likely qualify for the lowest interest rates.

- Good Credit (700-749): You’ll receive competitive interest rates.

- Fair Credit (650-699): Interest rates will be higher, but still manageable.

- Poor Credit (Below 650): You’ll face the highest interest rates, making car ownership more expensive.

Strategies to Improve Your Credit Score

Improving your credit score can significantly reduce the cost of your car loan. Here are some strategies to boost your credit score:

- Pay Bills on Time: Payment history is a crucial factor in your credit score.

- Reduce Credit Card Balances: Aim to keep your credit utilization below 30%.

- Avoid Opening Too Many New Accounts: Opening multiple credit accounts in a short period can lower your score.

- Check Your Credit Report Regularly: Review your credit report for errors and dispute any inaccuracies.

Refinancing Your Car Loan for Better Terms

If you already have a car loan, refinancing can be a viable option to lower your interest rate and monthly payment. Refinancing involves taking out a new loan to pay off your existing car loan, ideally at a lower interest rate. This can save you a significant amount of money over the life of the loan.

4. Should I Buy a New or Used Car Based on My Income?

The decision to buy a new or used car based on your income depends on several factors, including your financial situation, priorities, and risk tolerance. A used car typically has a lower purchase price and slower depreciation, but it may come with higher maintenance costs. A new car offers the latest features and reliability, but it depreciates quickly and has a higher price tag.

Advantages and Disadvantages of Buying New

Advantages:

- Reliability: New cars come with warranties and are less likely to require immediate repairs.

- Latest Features: New cars offer the newest technology, safety features, and fuel efficiency.

- Customization: You can customize a new car with your preferred options and colors.

Disadvantages:

- Higher Purchase Price: New cars are more expensive than used cars.

- Rapid Depreciation: New cars depreciate significantly in the first few years.

Advantages and Disadvantages of Buying Used

Advantages:

- Lower Purchase Price: Used cars are more affordable, allowing you to save money upfront.

- Slower Depreciation: Used cars depreciate less rapidly than new cars.

- Lower Insurance Costs: Insurance rates are typically lower for used cars.

Disadvantages:

- Higher Maintenance Costs: Used cars may require more frequent repairs.

- Fewer Features: Older models may lack the latest technology and safety features.

- Uncertain History: You may not know the car’s full history, which could lead to unexpected problems.

Financial Planning for the Purchase

Before deciding, assess your financial situation. Calculate how much you can afford to spend on a car, considering all associated costs like insurance, fuel, and maintenance. If your budget is tight, a used car may be the more sensible choice. If you prioritize reliability and the latest features and can afford the higher price, a new car might be the better option.

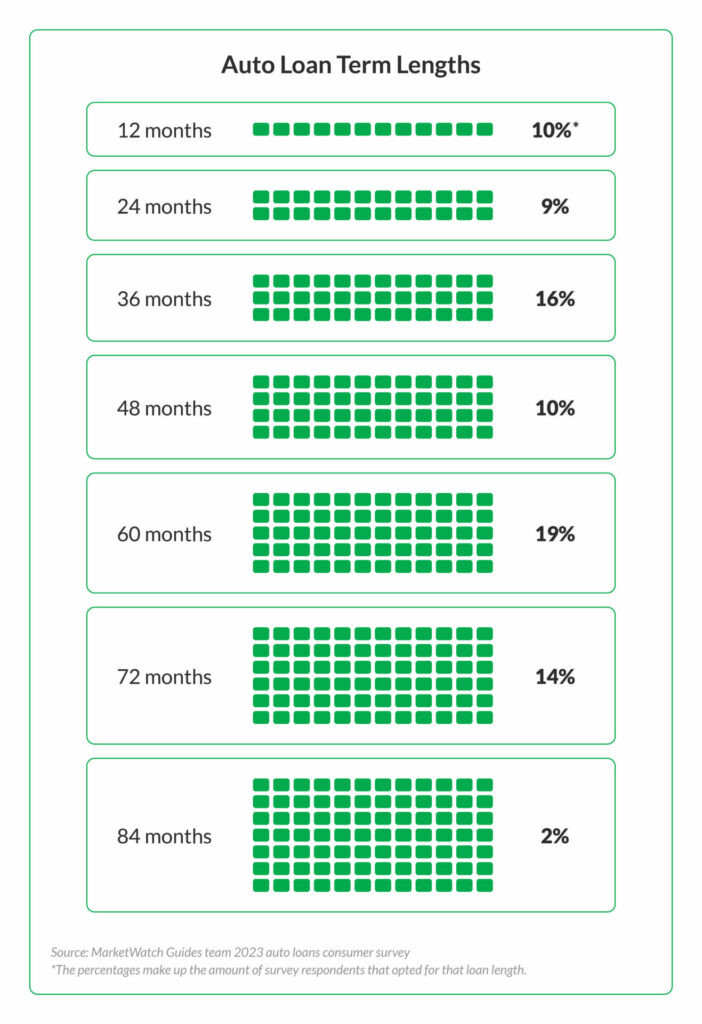

5. What Loan Term Length Should I Choose to Keep Payments Affordable?

Choosing the right loan term length is essential for keeping car payments affordable; shorter terms result in higher monthly payments but lower overall interest paid, while longer terms offer lower monthly payments but accumulate more interest over time. Balancing these factors helps you find a term that fits your budget and minimizes long-term costs.

Impact of Loan Term on Monthly Payments

The loan term is the length of time you have to repay the loan. Common car loan terms range from 24 to 72 months. The longer the term, the lower your monthly payment, but the more interest you’ll pay over the life of the loan.

Comparing Short-Term vs. Long-Term Loans

- Short-Term Loans (24-36 months):

- Pros: Higher monthly payments, lower overall interest, faster equity buildup.

- Cons: Higher monthly payments may strain your budget.

- Long-Term Loans (60-72 months):

- Pros: Lower monthly payments, easier to fit into your budget.

- Cons: Higher overall interest, slower equity buildup, risk of owing more than the car is worth.

Finding the Right Balance

To find the right balance, consider your budget and financial goals. If you want to pay off the car quickly and minimize interest, a short-term loan is a good option. If you need lower monthly payments to manage your budget, a long-term loan may be necessary. However, be aware of the increased interest costs and the risk of owing more than the car is worth.

6. How Does a Down Payment Affect My Car Payment Affordability?

A down payment significantly enhances car payment affordability by reducing the loan amount, leading to lower monthly payments and overall interest paid. A larger down payment also increases your equity in the vehicle from the start, decreasing the risk of owing more than the car is worth over time.

Benefits of a Larger Down Payment

Making a larger down payment offers several advantages:

- Lower Monthly Payments: Reducing the loan amount directly lowers your monthly payments.

- Reduced Interest: A smaller loan means less interest accrues over the loan term.

- Increased Equity: A larger down payment gives you more equity in the car from the beginning.

- Better Loan Terms: Lenders may offer better interest rates and terms with a larger down payment.

Determining the Ideal Down Payment Amount

The ideal down payment amount depends on your financial situation and the price of the car. A general guideline is to aim for at least 10% of the car’s purchase price. However, a larger down payment of 20% or more can provide even greater savings and financial benefits.

Strategies to Save for a Down Payment

Saving for a down payment requires planning and discipline. Here are some strategies to help you save:

- Create a Budget: Track your income and expenses to identify areas where you can save.

- Set a Savings Goal: Determine how much you need to save and set a realistic timeline.

- Automate Savings: Set up automatic transfers from your checking account to a savings account.

- Cut Unnecessary Expenses: Identify and eliminate non-essential expenses.

7. What Are the Best Negotiation Strategies for Lowering My Car Payment?

The best negotiation strategies for lowering your car payment involve thorough research, understanding the car’s value, and being prepared to walk away if the deal isn’t favorable. Negotiating the price, interest rate, and trade-in value separately can also lead to better terms and lower monthly payments.

Researching the Market Value of the Car

Before you start negotiating, research the market value of the car you’re interested in. Websites like Kelley Blue Book and Edmunds provide pricing information based on the car’s make, model, condition, and location. Knowing the market value gives you a benchmark for negotiations.

Negotiating the Price, Interest Rate, and Trade-In Value Separately

- Price: Focus on negotiating the car’s price before discussing financing options.

- Interest Rate: Shop around for the best interest rates from different lenders.

- Trade-In Value: Get an appraisal of your current car’s trade-in value from multiple sources.

Being Prepared to Walk Away

One of the most powerful negotiation tactics is being prepared to walk away from the deal if it doesn’t meet your needs. Dealers are often more willing to offer better terms if they know you’re not afraid to leave.

8. How Can I Balance Car Payments with Other Financial Goals?

Balancing car payments with other financial goals requires careful budgeting, prioritizing your goals, and making informed decisions about car affordability. By aligning your car payments with your broader financial plan, you can achieve stability and work towards long-term financial success.

Prioritizing Financial Goals

Start by identifying your financial goals, such as paying off debt, saving for retirement, buying a home, or starting a business. Prioritize these goals based on their importance and timeline. Make sure your car payment aligns with these priorities.

Creating a Detailed Budget

A detailed budget is essential for balancing car payments with other financial goals. Track your income and expenses to see where your money is going. Identify areas where you can cut back to free up funds for your car payment and other goals.

Automating Savings and Investments

Set up automatic transfers from your checking account to savings and investment accounts. Automating these transfers ensures you consistently save and invest, even when you’re busy.

9. What Are the Alternatives to Buying a Car to Save Money?

Alternatives to buying a car to save money include public transportation, carpooling, biking, and using ride-sharing services. These options can significantly reduce your transportation costs, freeing up funds for other financial goals and investment opportunities.

Utilizing Public Transportation

Public transportation, such as buses, trains, and subways, can be a cost-effective alternative to owning a car, especially in urban areas. Calculate the cost of a monthly transit pass and compare it to your car-related expenses.

Carpooling and Ride-Sharing Services

Carpooling with colleagues or neighbors can save you money on fuel and parking. Ride-sharing services like Uber and Lyft can be convenient for occasional trips, but they can be expensive if used frequently.

Biking and Walking

For shorter commutes, biking or walking can be a healthy and cost-effective alternative to driving. Investing in a good bike and safety equipment can be a worthwhile investment in your health and finances.

10. How Can Income-Partners.Net Help Me Increase My Income to Afford a Car?

Income-partners.net helps you increase your income to afford a car by connecting you with strategic partners and opportunities that boost your revenue streams. By joining our network, you gain access to collaborative projects, investment ventures, and expert advice tailored to maximize your earnings potential, making car ownership more achievable and financially sustainable.

Strategic Partnership Opportunities

Income-partners.net offers a platform to connect with like-minded professionals and businesses seeking strategic partnerships. These partnerships can lead to new revenue streams, business expansion, and increased profitability.

Investment Ventures and Collaborative Projects

Our network includes investors and entrepreneurs looking for collaborative projects and investment opportunities. By joining Income-partners.net, you can access these ventures and potentially earn additional income through equity, profit sharing, or other financial arrangements.

Expert Advice and Resources

Income-partners.net provides expert advice and resources to help you maximize your earnings potential. Our platform offers articles, guides, and tools to help you navigate the world of partnerships and investments.

Ready to find the perfect partnership opportunity? Visit income-partners.net today to explore strategic alliances, investment ventures, and collaborative projects to maximize your earnings potential. With the right partners, you can increase your income and achieve your financial goals. Contact us at Address: 1 University Station, Austin, TX 78712, United States. Phone: +1 (512) 471-3434, or visit our website at income-partners.net.

FAQ: Car Payment Affordability

-

What is the ideal percentage of my income that should go towards a car payment?

Ideally, your car payment should not exceed 10-15% of your monthly take-home pay to ensure financial stability. -

What expenses should I consider beyond the car payment when determining affordability?

Consider fuel, insurance, maintenance, repairs, registration fees, and taxes. -

How does my credit score affect my car payment affordability?

A higher credit score results in lower interest rates, making the car more affordable. -

Should I buy a new or used car based on my income?

If your budget is tight, a used car may be more sensible due to its lower purchase price and slower depreciation. -

What loan term length should I choose to keep payments affordable?

Balance the loan term based on your budget; shorter terms mean higher payments but lower overall interest. -

How does a down payment affect my car payment affordability?

A larger down payment reduces the loan amount, lowering monthly payments and overall interest. -

What are the best negotiation strategies for lowering my car payment?

Research the car’s value, negotiate price, interest rate, and trade-in value separately, and be prepared to walk away. -

How can I balance car payments with other financial goals?

Prioritize financial goals, create a detailed budget, and automate savings and investments. -

What are the alternatives to buying a car to save money?

Consider public transportation, carpooling, biking, and ride-sharing services. -

How can income-partners.net help me increase my income to afford a car?

income-partners.net connects you with strategic partners and opportunities to boost your revenue streams.