What percentage of your income should go towards your car payment? Determining the right amount is crucial for financial health, and at income-partners.net, we help you make informed decisions that align with your income goals. Discover the ideal percentage and strategies to ensure your car payment doesn’t derail your financial success, fostering lucrative partnerships along the way. Achieve financial balance and explore opportunities for revenue enhancement by understanding how to manage your car expenses effectively.

1. Understanding the Golden Rule: The 10-15-20 Rule

What percentage of your income should really be allocated to your car payment? As a general guideline, the 10-15-20 rule suggests that your car payment should not exceed 10% of your gross monthly income, your down payment should be at least 20% of the car’s value, and your loan term should be no longer than 36 months, although this may vary depending on individual circumstances. This rule helps ensure that your vehicle expenses remain manageable and don’t strain your budget.

1.1 Why is this rule important?

This rule is important because it sets a limit on how much of your income should go towards car expenses, helping you avoid financial strain. Sticking to the 10-15-20 guideline means you’re less likely to overextend yourself, leaving room for other financial priorities like savings, investments, and unexpected expenses. According to financial experts, adhering to these percentages can significantly reduce the risk of debt and financial instability.

1.2 How to Calculate Your Ideal Car Payment Percentage

Calculating your ideal car payment percentage is straightforward: divide your desired monthly car payment by your gross monthly income, then multiply by 100. Understanding this percentage allows you to compare it against recommendations and adjust your car-buying strategy accordingly.

Here’s a simple formula:

(Monthly Car Payment / Gross Monthly Income) x 100 = Car Payment PercentageFor example, if your gross monthly income is $5,000 and you’re aiming for a $500 car payment:

($500 / $5,000) x 100 = 10%This calculation ensures you stay within a reasonable range and prevent overspending.

1.3 Benefits of Staying Within the Recommended Percentage

Staying within the recommended percentage offers numerous benefits, including increased financial stability and flexibility. By keeping your car payment manageable, you can allocate more funds to investments, savings, and other financial goals.

- Financial Stability: Manageable car payments reduce the risk of falling behind on payments.

- Increased Savings: More money available for emergency funds, retirement, or other savings goals.

- Investment Opportunities: Extra capital to invest in income-generating assets and partnerships.

- Reduced Stress: Lower financial burdens lead to less stress and better overall well-being.

By adhering to these guidelines, you set yourself up for long-term financial success.

2. Determining Affordability: Key Factors

What determines how much you can actually afford for a car payment? Your financial comfort zone depends on factors like income, expenses, credit score, and loan terms.

2.1 Income and Expenses Analysis

Assess your monthly income and expenses to understand your budget constraints and how much you can allocate to car payments. Subtracting your total monthly expenses from your net income provides a clear picture of your disposable income.

- Calculate Net Income: Start by determining your net monthly income, which is your income after taxes and other deductions.

- List Fixed Expenses: Include all your fixed monthly expenses, such as rent or mortgage, utilities, insurance, and loan payments.

- Identify Variable Expenses: List variable expenses like groceries, gas, entertainment, and dining out.

- Calculate Total Expenses: Add your fixed and variable expenses to determine your total monthly expenses.

- Determine Disposable Income: Subtract your total expenses from your net income to find your disposable income.

This structured approach ensures you understand your financial capacity before committing to a car payment.

2.2 Credit Score Impact

Your credit score significantly influences the interest rate you’ll receive on a car loan, affecting your monthly payment and total cost. A higher credit score can secure lower interest rates, saving you thousands of dollars over the loan term.

| Credit Score Range | Interest Rate (New Car) | Interest Rate (Used Car) |

|---|---|---|

| 750+ (Excellent) | 4.00% | 4.50% |

| 700-749 (Good) | 5.00% | 5.50% |

| 650-699 (Fair) | 7.00% | 7.50% |

| Below 650 (Poor) | 9.00% | 9.50% |

These rates are approximate and can vary based on the lender and market conditions.

Credit score ratings and their impact on car loan rates

Credit score ratings and their impact on car loan rates

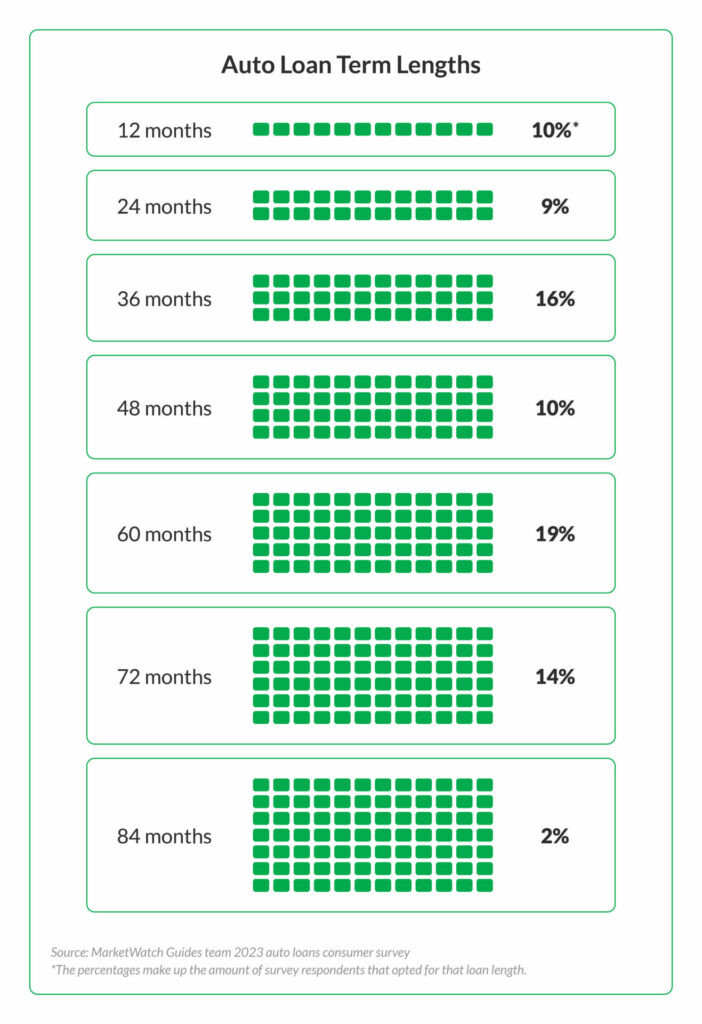

2.3 Loan Term Considerations

Consider the impact of loan term length on your monthly payment and overall interest paid. Shorter loan terms result in higher monthly payments but less interest paid over the life of the loan, while longer loan terms offer lower monthly payments but accumulate more interest.

| Loan Term (Months) | Monthly Payment | Total Interest Paid |

|---|---|---|

| 36 | $464.96 | $678.56 |

| 48 | $352.78 | $933.24 |

| 60 | $283.35 | $1,200.70 |

| 72 | $235.66 | $1,490.01 |

This table assumes a loan amount of $16,000 at an interest rate of 4.00%.

3. Practical Steps to Calculate Your Car Affordability

What are the steps to calculate how much car you can afford? Start by determining your monthly net income, calculating your monthly expenses, and setting a realistic budget for your car payment.

3.1 Step-by-Step Calculation

- Determine Net Income: Calculate your total monthly income after taxes and deductions.

- Calculate Monthly Expenses: Add up all your fixed and variable monthly expenses.

- Calculate Disposable Income: Subtract your total expenses from your net income to find your disposable income.

- Set Car Payment Budget: Allocate a percentage of your disposable income for your car payment, ideally no more than 10-15% of your gross monthly income.

- Factor in Additional Costs: Include expenses like car insurance, fuel, maintenance, and registration fees.

3.2 Tools and Calculators Available

Utilize online car affordability calculators to estimate your monthly payments and total costs based on your income, expenses, and credit score. These tools provide valuable insights and help you make informed decisions.

- Auto Loan Calculator: Estimates monthly payments based on loan amount, interest rate, and loan term.

- Car Affordability Calculator: Determines how much you can afford based on income and expenses.

- Total Cost of Ownership Calculator: Calculates the total cost of owning a car, including depreciation, insurance, and maintenance.

3.3 Real-Life Examples

Consider real-life examples of individuals with varying income levels and their approaches to car affordability. These case studies offer practical insights and demonstrate how to tailor your car-buying strategy to your specific financial situation.

-

Example 1: Single Professional

- Gross Monthly Income: $5,000

- Recommended Car Payment (10%): $500

- Strategy: Prioritize a reliable, fuel-efficient vehicle with low maintenance costs.

-

Example 2: Young Family

- Gross Monthly Income: $7,000

- Recommended Car Payment (15%): $1,050

- Strategy: Opt for a family-friendly SUV with good safety ratings and ample cargo space.

-

Example 3: Entrepreneur

- Gross Monthly Income: $10,000

- Recommended Car Payment (10%): $1,000

- Strategy: Choose a vehicle that balances professional appearance with practical needs for business travel.

These examples show how diverse individuals can navigate car affordability based on their unique circumstances.

4. Hidden Costs to Consider

What hidden costs should you consider when determining car affordability? Don’t forget to factor in car insurance, fuel costs, maintenance, and potential repair expenses.

4.1 Car Insurance

Research average car insurance rates based on your location, driving history, and vehicle type. Insurance premiums can significantly impact your overall car expenses.

| Factor | Impact on Insurance Rate |

|---|---|

| Location | Urban areas = higher |

| Driving History | Accidents/Tickets = higher |

| Vehicle Type | Sports cars = higher |

| Age | Younger drivers = higher |

| Coverage Level | More coverage = higher |

4.2 Fuel Costs

Estimate your monthly fuel costs based on your average driving distance and the fuel efficiency of your chosen vehicle. Use online tools to compare fuel costs for different models.

- Calculate Annual Mileage: Determine how many miles you drive annually.

- Find MPG: Look up the vehicle’s miles per gallon (MPG) rating.

- Calculate Gallons Used: Divide annual mileage by MPG to find gallons used per year.

- Determine Fuel Cost: Multiply gallons used by the average fuel price in your area.

- Calculate Monthly Cost: Divide annual fuel cost by 12 to find your monthly fuel expense.

4.3 Maintenance and Repairs

Budget for routine maintenance tasks like oil changes, tire rotations, and brake inspections. Also, set aside funds for unexpected repairs to avoid financial surprises.

- Routine Maintenance:

- Oil Changes: $50-$100 every 3,000-7,000 miles

- Tire Rotations: $25-$50 every 6,000-8,000 miles

- Brake Inspections: $50-$100 annually

- Unexpected Repairs:

- Battery Replacement: $100-$300

- Brake Replacement: $300-$800

- Transmission Repair: $2,000-$5,000

4.4 Depreciation

Understand the concept of depreciation and how it affects the value of your vehicle over time. New cars typically depreciate faster than used cars.

| Year | Depreciation |

|---|---|

| 1 | 20-30% |

| 2 | 10-15% |

| 3 | 8-12% |

| 4 | 6-10% |

| 5 | 5-8% |

These are average depreciation rates; actual rates can vary based on the vehicle’s make, model, and condition.

5. Strategies to Lower Your Car Payment

What strategies can you employ to lower your car payment? Negotiate the purchase price, increase your down payment, and consider a used car instead of a new one.

5.1 Negotiating the Purchase Price

Research fair market value for the vehicle you’re interested in and negotiate the price with the dealer. Be prepared to walk away if the terms don’t meet your budget.

- Research: Use sites like Kelley Blue Book and Edmunds to find the fair market value.

- Get Quotes: Obtain multiple quotes from different dealerships to leverage competitive pricing.

- Negotiate: Start with an offer below the fair market value and be prepared to negotiate.

- Walk Away: Don’t be afraid to walk away if the dealer doesn’t meet your terms.

5.2 Increasing Your Down Payment

Making a larger down payment reduces the loan amount and lowers your monthly payments. Aim for at least 20% of the vehicle’s purchase price.

| Down Payment | Loan Amount | Monthly Payment (60 months, 4% interest) |

|---|---|---|

| $2,000 | $14,000 | $257.94 |

| $4,000 | $12,000 | $221.26 |

| $6,000 | $10,000 | $184.55 |

5.3 Choosing a Used Car

Opting for a used car can save you money on the purchase price and insurance premiums. Conduct thorough inspections and research the vehicle’s history.

- Inspection: Have a mechanic inspect the car before purchasing.

- Vehicle History: Check the vehicle’s history report using services like Carfax or AutoCheck.

- Mileage: Consider cars with lower mileage for better reliability.

- Maintenance Records: Review maintenance records to assess the car’s upkeep.

5.4 Refinancing Options

Explore refinancing options to potentially lower your interest rate and monthly payment. Compare offers from different lenders to find the best terms.

- Check Credit Score: Ensure your credit score has improved since your original loan.

- Shop Around: Compare offers from multiple lenders to find the best interest rate.

- Calculate Savings: Use a refinancing calculator to estimate your potential savings.

- Apply for Refinancing: Submit your application and required documents.

6. Alternative Transportation Options

What alternative transportation options can you consider to avoid or minimize car payments? Think about public transportation, cycling, and carpooling.

6.1 Public Transportation

Utilize public transportation options like buses, trains, and subways to reduce your reliance on a personal vehicle. Calculate the cost savings compared to owning a car.

| Expense | Car Ownership | Public Transportation |

|---|---|---|

| Car Payment | $300 | $0 |

| Insurance | $150 | $0 |

| Fuel | $100 | $0 |

| Maintenance | $50 | $0 |

| Public Transit Pass | $0 | $100 |

| Total | $600 | $100 |

6.2 Cycling and Walking

Consider cycling or walking for short commutes and errands to save money on transportation costs and improve your physical health.

- Cost Savings: Eliminates fuel, maintenance, and parking costs.

- Health Benefits: Improves cardiovascular health and fitness.

- Environmental Impact: Reduces carbon footprint and pollution.

6.3 Carpooling and Ride-Sharing

Share rides with coworkers or neighbors to reduce your transportation expenses. Explore ride-sharing services like Uber and Lyft for occasional trips.

- Carpooling: Split fuel and parking costs with other commuters.

- Ride-Sharing: Convenient for occasional trips and eliminates the need for parking.

7. Expert Financial Advice

What do financial experts recommend regarding car payments? Financial advisors suggest prioritizing financial stability and avoiding excessive debt.

7.1 Quotes from Financial Advisors

- “Aim for a car payment that doesn’t exceed 10% of your gross monthly income to maintain financial flexibility.” – Dave Ramsey, Financial Expert

- “Consider the total cost of ownership, including insurance, fuel, and maintenance, when determining your car affordability.” – Suze Orman, Personal Finance Advisor

- “Focus on building a strong financial foundation before committing to a large car payment.” – Clark Howard, Consumer Advocate

7.2 Case Studies of Successful Financial Planning

Explore case studies of individuals who have successfully managed their car expenses and achieved financial stability. These stories provide inspiration and practical tips.

-

Case Study 1: Maria, Teacher

- Income: $4,000/month

- Strategy: Bought a used car, increased her down payment, and kept her car payment under 10% of her income.

-

Case Study 2: John, Engineer

- Income: $7,000/month

- Strategy: Negotiated a lower price on a new car, refinanced his loan, and used the savings to invest.

8. Resources for Further Information

Where can you find more resources for determining car affordability? Utilize online tools, financial planning websites, and expert advice to make informed decisions.

8.1 Online Tools and Calculators

- Auto Loan Calculator: Estimate monthly payments based on loan terms.

- Car Affordability Calculator: Determine how much car you can afford.

- Total Cost of Ownership Calculator: Calculate the total cost of owning a car.

8.2 Financial Planning Websites

- income-partners.net: Offers resources and tools for managing finances and partnering for success.

- NerdWallet: Provides financial advice and tools for managing debt and investments.

- The Balance: Offers articles and resources on personal finance topics.

8.3 Books and Publications

- “The Total Money Makeover” by Dave Ramsey: A comprehensive guide to financial planning and debt management.

- “The Automatic Millionaire” by David Bach: Offers strategies for automating your savings and investments.

- “Your Money or Your Life” by Vicki Robin and Joe Dominguez: A guide to achieving financial independence.

9. How Income-Partners.net Can Help

How can income-partners.net assist you in making informed car-buying decisions and enhancing your financial partnerships? We offer strategies, resources, and partnership opportunities to improve your financial health.

9.1 Strategies for Financial Success

Discover effective strategies for managing your car expenses and optimizing your financial partnerships with income-partners.net. Learn to balance your financial obligations while exploring opportunities for growth and collaboration.

9.2 Partnership Opportunities

Connect with potential partners through income-partners.net to explore collaborative opportunities that can boost your income and financial stability. By leveraging strategic alliances, you can achieve financial goals more efficiently.

9.3 Exclusive Resources and Tools

Access exclusive resources and financial tools on income-partners.net, designed to help you make informed decisions about car affordability and overall financial management.

10. Final Thoughts

What is the key takeaway regarding car affordability and income? Prioritize financial stability, make informed decisions, and leverage resources to ensure your car payment aligns with your financial goals.

10.1 Key Takeaways

- Aim for a car payment that doesn’t exceed 10-15% of your gross monthly income.

- Consider all associated costs, including insurance, fuel, and maintenance.

- Negotiate the purchase price and increase your down payment to lower your monthly payments.

- Explore alternative transportation options to reduce your reliance on a personal vehicle.

10.2 Call to Action

Ready to take control of your finances and explore lucrative partnership opportunities? Visit income-partners.net today to discover strategies, resources, and connections that can transform your financial future. Don’t wait—start building your path to financial success now!

FAQ: Managing Car Payments and Income

1. What is the ideal percentage of income for a car payment?

The ideal percentage for a car payment should be between 10% and 15% of your gross monthly income to ensure financial stability and flexibility. Staying within this range helps you avoid overextending your budget.

2. How do I calculate the percentage of my income that goes to my car payment?

To calculate the percentage, divide your monthly car payment by your gross monthly income, then multiply by 100, this provides a clear picture of how much of your income is allocated to your car payment.

(Monthly Car Payment / Gross Monthly Income) x 100 = Car Payment Percentage3. What factors should I consider when determining how much car I can afford?

When determining car affordability, consider your income, monthly expenses, credit score, interest rates, and additional costs like insurance, fuel, and maintenance. A comprehensive assessment of these factors is vital.

4. How does my credit score affect my car payment?

A higher credit score typically results in lower interest rates on your car loan, reducing your monthly payment and overall cost, so aim to improve your credit score before applying for a car loan.

5. What are some strategies to lower my car payment?

Strategies to lower your car payment include negotiating the purchase price, increasing your down payment, choosing a used car, and refinancing your loan, each of which can significantly reduce your financial burden.

6. Are there any hidden costs I should consider when buying a car?

Hidden costs to consider include car insurance, fuel costs, maintenance and repairs, and depreciation, planning for these costs ensures there are no surprises.

7. What alternative transportation options can help me avoid or minimize car payments?

Alternative transportation options include public transportation, cycling, walking, carpooling, and ride-sharing, these can significantly reduce or eliminate car payments.

8. How can income-partners.net help me make informed car-buying decisions?

income-partners.net offers strategies, resources, and partnership opportunities to improve your financial health, helping you make informed decisions about car affordability and overall financial management.

9. What do financial experts recommend regarding car payments and income?

Financial experts recommend prioritizing financial stability, avoiding excessive debt, and aiming for a car payment that doesn’t exceed 10-15% of your gross monthly income, so heed their advice.

10. Where can I find reliable online tools and calculators to help me determine car affordability?

You can find reliable online tools and calculators on websites like NerdWallet, The Balance, and income-partners.net, these resources provide valuable insights for car-buying decisions.

Address: 1 University Station, Austin, TX 78712, United States

Phone: +1 (512) 471-3434

Website: income-partners.net