Determining What Percentage Of Monthly Income Should Go To Car Payment is a crucial financial decision, and at income-partners.net, we’re here to help you make informed choices that align with your financial goals, fostering partnerships, and boosting your earning potential. Understanding this balance enables you to manage your finances effectively, paving the way for lucrative collaborations and income growth opportunities. By exploring smart budgeting strategies and effective money management, you can optimize your monthly expenses, including your car payment, and unlock pathways to successful partnerships and increased revenue streams.

Table of Contents

1. Understanding the Fundamentals

- 1.1. What is the 20/4/10 Rule for Car Buying?

- 1.2. Why is it Important to Budget for Car Payments?

- 1.3. How Does Your Credit Score Affect Your Car Payment Affordability?

2. Key Factors Influencing Your Car Payment Budget

- 2.1. Monthly Net Income: The Foundation of Your Budget

- 2.2. Essential Monthly Expenses: Accounting for Fixed and Variable Costs

- 2.3. Debt-to-Income Ratio (DTI): A Critical Indicator of Financial Health

- 2.4. Interest Rates and Loan Terms: Understanding the Long-Term Impact

3. Practical Guidelines for Determining Your Car Payment Percentage

- 3.1. The Conservative Approach: 10% or Less of Monthly Income

- 3.2. The Moderate Approach: 10-15% of Monthly Income

- 3.3. The Aggressive Approach: Over 15% of Monthly Income (Proceed with Caution)

4. Real-World Examples and Scenarios

- 4.1. Scenario 1: Young Professional in Austin, TX

- 4.2. Scenario 2: Business Owner with Variable Income

- 4.3. Scenario 3: Family with Multiple Financial Obligations

5. Strategies for Optimizing Your Car Payment

- 5.1. Negotiating a Lower Purchase Price

- 5.2. Increasing Your Down Payment

- 5.3. Refinancing Your Auto Loan

- 5.4. Improving Your Credit Score

- 5.5. Considering a More Affordable Vehicle

6. Alternatives to Buying a Car

- 6.1. Leasing: Weighing the Pros and Cons

- 6.2. Public Transportation and Ride-Sharing

- 6.3. Carpooling and Sharing Economy Options

7. Common Mistakes to Avoid

- 7.1. Ignoring the Total Cost of Ownership

- 7.2. Overestimating Affordability

- 7.3. Neglecting to Shop Around for the Best Rates

- 7.4. Disregarding the Impact of Depreciation

8. Expert Insights and Recommendations

- 8.1. Advice from Financial Advisors

- 8.2. Case Studies of Successful Budgeting

9. Leveraging Income-Partners.net for Financial Growth

- 9.1. Finding Strategic Partners to Increase Income

- 9.2. Building Collaborative Ventures for Financial Stability

- 9.3. Accessing Resources for Financial Planning and Management

10. Frequently Asked Questions (FAQs)

- 10.1. Is it better to buy a new or used car?

- 10.2. How does the length of my car loan affect my finances?

- 10.3. What is the best way to negotiate a lower car price?

- 10.4. Should I lease or buy a car?

- 10.5. How can I improve my credit score quickly?

- 10.6. What are the hidden costs of car ownership?

- 10.7. How does my car affect my income tax?

- 10.8. What percentage of my salary should I invest?

- 10.9. What should I consider other than my car payment?

- 10.10. How can income-partners.net help me manage my car expenses?

11. Conclusion: Balancing Car Payments with Financial Goals

1. Understanding the Fundamentals

Let’s delve into the basics of budgeting for car payments to ensure financial stability and identify opportunities for strategic partnerships. Understanding these fundamental aspects helps you to make informed decisions, paving the way for better financial health and collaborative ventures.

1.1. What is the 20/4/10 Rule for Car Buying?

The 20/4/10 rule is a guideline to help you buy a car responsibly. It suggests you put down at least 20% as a down payment, finance the car for no more than four years, and ensure that your total transportation costs, including car payments, insurance, and gas, don’t exceed 10% of your gross monthly income. Adhering to this rule can prevent financial strain and keep your car-related expenses manageable. This principle, when applied thoughtfully, enables you to allocate more resources towards building strategic partnerships and income-generating activities.

1.2. Why is it Important to Budget for Car Payments?

Budgeting for car payments is crucial because it helps you maintain financial discipline and avoid overspending. A car is often one of the most significant monthly expenses for many individuals and families. Without a clear budget, you risk allocating too much of your income to car payments, leaving less for other essential needs, investments, or business ventures. By planning ahead, you can ensure that your car payment aligns with your financial goals and supports your overall financial health, enabling you to pursue strategic partnerships and income-generating activities with confidence.

1.3. How Does Your Credit Score Affect Your Car Payment Affordability?

Your credit score plays a pivotal role in determining the interest rate you’ll receive on an auto loan. A higher credit score typically translates to lower interest rates, which can significantly reduce your monthly car payments and the total cost of the loan. Conversely, a lower credit score may result in higher interest rates, making the car less affordable over the loan term. Improving your credit score before applying for a car loan can save you thousands of dollars and make your car payment more manageable. Moreover, a strong credit profile can also open doors to strategic partnerships and investment opportunities, further enhancing your financial prospects.

A close-up of a credit score report, highlighting key factors like payment history and credit utilization

A close-up of a credit score report, highlighting key factors like payment history and credit utilization

2. Key Factors Influencing Your Car Payment Budget

Several factors influence your car payment budget, from your monthly net income to your debt-to-income ratio. Understanding these elements is essential for setting a realistic and sustainable car payment plan.

2.1. Monthly Net Income: The Foundation of Your Budget

Your monthly net income, or take-home pay after taxes and deductions, is the foundation of your car payment budget. It represents the actual amount of money you have available to spend each month. Accurately calculating your net income is the first step in determining how much you can realistically afford for a car payment without jeopardizing your financial stability. According to financial advisors, your car expenses should not exceed 15% of your monthly take-home pay. Knowing this figure helps you to better manage your cash flow and identify opportunities for strategic partnerships and investment.

2.2. Essential Monthly Expenses: Accounting for Fixed and Variable Costs

Essential monthly expenses include fixed costs like rent or mortgage payments, utilities, insurance, and loan repayments, as well as variable costs such as groceries, transportation, and healthcare. Accounting for these expenses is vital in determining how much disposable income you have left for a car payment. Underestimating your monthly expenses can lead to financial strain, making it difficult to meet your obligations. By carefully tracking and budgeting for all your expenses, you can ensure that your car payment fits comfortably within your financial framework. This diligence frees up resources that can be channeled into strategic partnerships and income-generating ventures.

2.3. Debt-to-Income Ratio (DTI): A Critical Indicator of Financial Health

Your debt-to-income ratio (DTI) is a percentage that represents the amount of your gross monthly income that goes toward paying debts, including credit cards, loans, and other obligations. Lenders use DTI to assess your ability to manage monthly payments. A lower DTI indicates that you have a healthy balance between debt and income, making you a more attractive borrower. Experts generally recommend a DTI of no more than 43% to ensure financial stability. Keeping your DTI in check will enable you to more effectively pursue strategic partnerships and capitalize on income-enhancing opportunities.

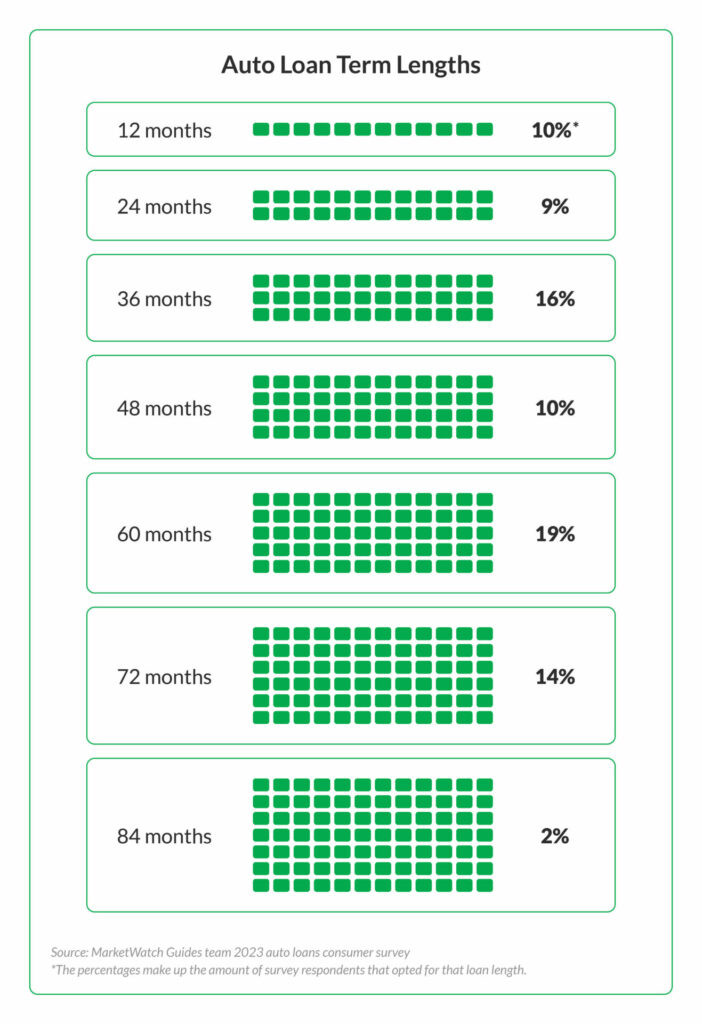

2.4. Interest Rates and Loan Terms: Understanding the Long-Term Impact

Interest rates and loan terms significantly impact the total cost of your car. A lower interest rate can save you thousands of dollars over the life of the loan, while a shorter loan term means higher monthly payments but less interest paid overall. Understanding these factors allows you to make informed decisions about financing your car. MarketWatch notes that longer loan terms, while offering lower monthly payments, increase the risk of ending up owing more on the loan than the vehicle is worth due to depreciation. Making wise choices regarding interest rates and loan terms can preserve capital that can be invested in strategic partnerships and growth initiatives.

3. Practical Guidelines for Determining Your Car Payment Percentage

To determine the appropriate percentage of your monthly income for a car payment, consider conservative, moderate, and aggressive approaches. Each approach offers varying levels of financial flexibility and risk.

3.1. The Conservative Approach: 10% or Less of Monthly Income

A conservative approach involves allocating 10% or less of your monthly income to car payments. This strategy provides a significant cushion for unexpected expenses and allows you to prioritize savings, investments, and strategic partnerships. Choosing this approach ensures that your car payment does not become a financial burden, freeing up resources for other essential needs and wealth-building activities. According to financial experts, limiting your car payment to 10% or less of your monthly income is a prudent way to maintain financial stability and pursue your long-term goals.

3.2. The Moderate Approach: 10-15% of Monthly Income

The moderate approach suggests dedicating 10-15% of your monthly income to car payments. This option strikes a balance between affordability and the ability to afford a more desirable vehicle. While it requires careful budgeting and monitoring of expenses, it still provides room for savings, investments, and unexpected costs. By staying within this range, you can enjoy a reliable car without compromising your overall financial health. This balanced approach can also enable you to effectively manage your resources while seeking strategic partnerships and income-generating opportunities.

3.3. The Aggressive Approach: Over 15% of Monthly Income (Proceed with Caution)

An aggressive approach entails allocating over 15% of your monthly income to car payments. While this may allow you to purchase a higher-end vehicle, it also carries a higher risk of financial strain. This approach leaves little room for unexpected expenses, savings, or investments and may limit your ability to pursue strategic partnerships. Financial advisors generally caution against this approach, especially for those with variable income or significant debt. If you choose this route, carefully assess your financial situation and ensure you have a solid plan to manage your expenses.

4. Real-World Examples and Scenarios

Consider these real-world examples to illustrate how different individuals can approach budgeting for car payments based on their unique financial situations.

4.1. Scenario 1: Young Professional in Austin, TX

Meet Sarah, a 28-year-old marketing specialist in Austin, TX, with a monthly net income of $4,000. Her essential monthly expenses, including rent, utilities, and groceries, total $2,500. Using the conservative approach (10% or less), Sarah should aim for a car payment of no more than $400. This allows her to save for a down payment, manage other financial obligations, and still invest in her career and potential business ventures through income-partners.net. A moderate approach (10-15%) would allow for a car payment between $400 and $600, providing more options but requiring tighter budgeting.

4.2. Scenario 2: Business Owner with Variable Income

John is a 45-year-old business owner with a variable monthly net income that averages around $7,000. His essential monthly expenses are approximately $3,500. Given the fluctuations in his income, John should lean towards a conservative approach. Limiting his car payment to 10% ($700) ensures that he can manage his finances during leaner months and still invest in his business growth and strategic partnerships through income-partners.net. An aggressive approach could put a strain on his finances during slower business periods.

4.3. Scenario 3: Family with Multiple Financial Obligations

Maria and David are a couple with two children, living in a suburban area. Their combined monthly net income is $8,000, and their essential monthly expenses, including mortgage, childcare, and groceries, amount to $5,000. With multiple financial obligations, they should adopt a moderate approach. Allocating 10-15% of their income to car payments would mean a budget of $800 to $1,200 per month. This range allows them to afford a reliable family vehicle while still contributing to savings, education funds, and potential investments with guidance from income-partners.net.

5. Strategies for Optimizing Your Car Payment

Optimizing your car payment involves several strategies, from negotiating a lower purchase price to refinancing your auto loan.

5.1. Negotiating a Lower Purchase Price

Negotiating the purchase price of a car can significantly reduce your monthly payments. Research the market value of the vehicle, compare prices from multiple dealerships, and be prepared to walk away if the dealer is unwilling to offer a reasonable price. According to Consumer Reports, negotiating aggressively can save you thousands of dollars on the purchase price. Lowering the purchase price reduces the loan amount and, consequently, your monthly payments. This strategy also frees up resources that can be directed towards strategic partnerships and investments through income-partners.net.

5.2. Increasing Your Down Payment

Increasing your down payment reduces the amount you need to borrow, resulting in lower monthly payments and less interest paid over the life of the loan. Aim for at least a 20% down payment to minimize the loan-to-value ratio. The more you put down, the less you’ll owe, and the more attractive you’ll be to lenders. This can result in a lower interest rate and better loan terms. Savings from reduced car payments can be reinvested into strategic partnerships and growth initiatives with support from income-partners.net.

5.3. Refinancing Your Auto Loan

Refinancing your auto loan involves replacing your existing loan with a new one, ideally at a lower interest rate. If your credit score has improved since you took out your original loan, or if interest rates have fallen, refinancing can save you a significant amount of money. Shop around for the best refinance rates and terms to ensure you get the most favorable deal. Saving on interest through refinancing can free up capital for investments and strategic partnerships facilitated by income-partners.net.

5.4. Improving Your Credit Score

Improving your credit score can lead to better loan terms and lower interest rates, making your car more affordable. Pay your bills on time, reduce your credit card balances, and avoid opening new credit accounts unnecessarily. A higher credit score demonstrates to lenders that you are a responsible borrower, increasing your chances of securing a favorable auto loan. With an improved credit score, you can allocate the savings from reduced car payments to strategic partnerships and entrepreneurial ventures through income-partners.net.

5.5. Considering a More Affordable Vehicle

Sometimes, the best way to optimize your car payment is to consider a more affordable vehicle. Opting for a used car or a less expensive model can significantly reduce your loan amount and monthly payments. Prioritize reliability and fuel efficiency over luxury features to save money in the long run. Savings from choosing a more affordable vehicle can be reinvested into strategic partnerships, business growth, and wealth-building opportunities with resources from income-partners.net.

6. Alternatives to Buying a Car

Explore alternatives to buying a car to determine if they align with your financial goals and lifestyle.

6.1. Leasing: Weighing the Pros and Cons

Leasing a car involves paying for the use of a vehicle over a specific period, typically two to three years, rather than owning it outright. Leasing generally results in lower monthly payments compared to buying, but you won’t build equity in the vehicle. At the end of the lease term, you must return the car or purchase it at its residual value. Leasing can be a good option if you prefer driving a new car every few years and don’t want to deal with the hassles of selling a used vehicle. However, it’s essential to consider the long-term costs and limitations of leasing. The money saved on lower monthly payments could be channeled into strategic partnerships and income-generating activities identified on income-partners.net.

6.2. Public Transportation and Ride-Sharing

Public transportation and ride-sharing services like Uber and Lyft can be cost-effective alternatives to owning a car, especially in urban areas. Using public transportation can save you money on car payments, insurance, gas, and maintenance. Ride-sharing services offer flexibility and convenience without the responsibilities of car ownership. These options can significantly reduce your transportation expenses, freeing up funds for strategic partnerships and wealth-building investments supported by income-partners.net.

6.3. Carpooling and Sharing Economy Options

Carpooling with colleagues or neighbors can help you save money on commuting costs while reducing traffic congestion and environmental impact. Sharing economy options, such as car-sharing services like Zipcar, provide access to vehicles when you need them without the financial burden of ownership. These collaborative solutions can significantly lower your transportation expenses, enabling you to invest more in strategic partnerships and financial growth opportunities facilitated by income-partners.net.

7. Common Mistakes to Avoid

Avoid these common mistakes when budgeting for a car to maintain financial stability and pursue strategic partnerships.

7.1. Ignoring the Total Cost of Ownership

Ignoring the total cost of ownership is a common mistake that can lead to unexpected expenses. Beyond the car payment, you must factor in insurance, gas, maintenance, repairs, and registration fees. According to AAA, the average cost of owning a new car can range from $600 to $1,000 per month, depending on the vehicle. Failing to account for these expenses can strain your budget and limit your ability to pursue strategic partnerships and income-generating activities.

7.2. Overestimating Affordability

Overestimating what you can afford is a critical mistake that can lead to financial distress. Just because a lender approves you for a certain loan amount doesn’t mean you can comfortably afford the payments. Accurately assess your income, expenses, and financial goals to determine a realistic car payment budget. Overextending yourself can jeopardize your financial stability and restrict your capacity to engage in strategic partnerships and business ventures through income-partners.net.

7.3. Neglecting to Shop Around for the Best Rates

Neglecting to shop around for the best rates can cost you thousands of dollars over the life of the loan. Compare interest rates from multiple lenders, including banks, credit unions, and online lenders, to ensure you get the most favorable terms. Even a small difference in interest rates can significantly impact your monthly payments and the total cost of the loan. Taking the time to shop around can free up capital for investments and strategic collaborations facilitated by income-partners.net.

7.4. Disregarding the Impact of Depreciation

Disregarding the impact of depreciation can lead to financial losses. Cars are depreciating assets, meaning their value decreases over time. Some vehicles depreciate faster than others, so research the depreciation rates of different models before making a purchase. Being aware of depreciation can help you make a more informed decision and avoid owing more on the loan than the car is worth. Understanding depreciation can preserve your capital and enable you to invest in strategic partnerships and wealth-building opportunities with resources from income-partners.net.

8. Expert Insights and Recommendations

Consider the following expert insights and recommendations to enhance your car payment budgeting and financial planning.

8.1. Advice from Financial Advisors

Financial advisors recommend following the 20/4/10 rule to ensure responsible car buying. They also advise creating a detailed budget, tracking your expenses, and prioritizing savings and investments. According to a survey by the Certified Financial Planner Board of Standards, 78% of financial advisors believe that budgeting is essential for achieving financial success. By seeking professional guidance, you can develop a comprehensive financial plan that includes car payments, savings goals, and strategies for pursuing strategic partnerships and income-generating ventures through income-partners.net.

8.2. Case Studies of Successful Budgeting

Case studies of successful budgeting highlight the importance of discipline, planning, and informed decision-making. For example, a study by the National Foundation for Credit Counseling found that individuals who participate in credit counseling are more likely to improve their credit scores, reduce their debt, and achieve their financial goals. By learning from these examples, you can implement effective budgeting strategies, optimize your car payment, and allocate resources to strategic partnerships and financial growth opportunities supported by income-partners.net.

9. Leveraging Income-Partners.net for Financial Growth

Discover how income-partners.net can help you find strategic partners, build collaborative ventures, and access resources for financial planning and management.

9.1. Finding Strategic Partners to Increase Income

Income-partners.net offers a platform to connect with strategic partners who can help you increase your income. Whether you’re looking for collaborators in marketing, sales, product development, or investment, the website provides a network of professionals and entrepreneurs seeking mutually beneficial partnerships. By leveraging these connections, you can diversify your income streams, expand your business reach, and achieve greater financial stability. Strategic partnerships can provide resources, expertise, and opportunities that accelerate your financial growth.

9.2. Building Collaborative Ventures for Financial Stability

Collaborative ventures are essential for achieving long-term financial stability. Income-partners.net facilitates the formation of collaborative ventures by connecting individuals and businesses with complementary skills and resources. These ventures can range from joint marketing campaigns to co-created products and services. By pooling resources and sharing risks, collaborative ventures can create new revenue streams and build a more resilient financial foundation. The website provides tools and resources to help you identify and establish successful collaborative partnerships.

9.3. Accessing Resources for Financial Planning and Management

Income-partners.net provides access to a wealth of resources for financial planning and management. The website offers articles, guides, and tools to help you budget effectively, manage your debt, and invest wisely. You can also find information on various financial topics, such as tax planning, retirement savings, and estate planning. These resources can empower you to make informed financial decisions, optimize your car payment, and allocate resources to strategic partnerships and wealth-building opportunities.

10. Frequently Asked Questions (FAQs)

Find answers to common questions about car payments, budgeting, and financial planning.

10.1. Is it better to buy a new or used car?

Whether it’s better to buy a new or used car depends on your priorities and financial situation. New cars come with the latest features and warranties, but they depreciate quickly. Used cars are more affordable and have lower insurance costs, but they may require more maintenance. Consider your budget, desired features, and risk tolerance to make the best decision.

10.2. How does the length of my car loan affect my finances?

The length of your car loan affects your monthly payments and the total interest paid. Shorter loan terms result in higher monthly payments but lower overall interest. Longer loan terms lead to lower monthly payments but higher total interest. Choose a loan term that balances affordability with the total cost of the loan.

10.3. What is the best way to negotiate a lower car price?

The best way to negotiate a lower car price is to research the market value, compare prices from multiple dealerships, and be prepared to walk away. Negotiate aggressively and focus on the out-the-door price, including all fees and taxes.

10.4. Should I lease or buy a car?

Whether you should lease or buy a car depends on your preferences and financial goals. Leasing offers lower monthly payments and the ability to drive a new car every few years. Buying builds equity and allows you to customize and keep the car for as long as you want.

10.5. How can I improve my credit score quickly?

You can improve your credit score quickly by paying your bills on time, reducing your credit card balances, and avoiding opening new credit accounts. Also, check your credit report for errors and dispute any inaccuracies.

10.6. What are the hidden costs of car ownership?

Hidden costs of car ownership include insurance, gas, maintenance, repairs, registration fees, and depreciation. Factor these expenses into your budget to get a realistic picture of the total cost of owning a car.

10.7. How does my car affect my income tax?

Your car can affect your income tax if you use it for business purposes. You may be able to deduct car expenses or take the standard mileage deduction. Consult a tax professional for personalized advice.

10.8. What percentage of my salary should I invest?

Financial advisors often recommend investing at least 15% of your salary to secure your financial future. Start early and increase your contributions over time to maximize the benefits of compounding.

10.9. What should I consider other than my car payment?

Other than your car payment, consider insurance, gas, maintenance, repairs, registration fees, and depreciation. Also, assess your overall financial goals and ensure your car payment aligns with your budget and priorities.

10.10. How can income-partners.net help me manage my car expenses?

Income-partners.net can help you manage your car expenses by providing resources for financial planning and connecting you with strategic partners to increase your income. By diversifying your income streams and building collaborative ventures, you can better afford your car payment and achieve greater financial stability.

11. Conclusion: Balancing Car Payments with Financial Goals

Balancing car payments with your financial goals requires careful budgeting, informed decision-making, and a strategic approach to financial planning. By understanding the key factors influencing your car payment budget, optimizing your expenses, and leveraging resources from income-partners.net, you can achieve financial stability and pursue your long-term goals. Remember to prioritize savings, investments, and strategic partnerships to build a solid financial foundation and achieve lasting success.

By integrating insights from financial experts, real-world scenarios, and practical strategies, you can make informed decisions about your car payment and overall financial health, empowering you to achieve your goals and build lasting partnerships through income-partners.net.