What Percentage Of Income Should Go To Car Payments? A sensible car payment should ideally not exceed 10-15% of your monthly take-home income, according to income-partners.net. By ensuring you stay within this range, you’ll be better positioned to manage your finances effectively while also pursuing additional revenue streams through strategic business partnerships. Managing your debt-to-income ratio, considering your financial goals, and understanding the true cost of ownership are essential for financial stability.

Table of Contents

- Understanding the 10-15% Rule for Car Payments

- Why Is This Percentage Important?

- Factors That Influence the Affordable Percentage

- How to Calculate Your Ideal Car Payment Percentage

- What Happens If You Exceed the Recommended Percentage?

- Strategies to Reduce Your Car Payment Burden

- The Impact of Car Payments on Other Financial Goals

- Alternatives to Buying a Car

- The Role of Credit Score in Determining Affordability

- Frequently Asked Questions (FAQs)

1. Understanding the 10-15% Rule for Car Payments

How much of your income should really be allocated to car payments? As a general guideline, experts suggest that your total car expenses, including the car payment, insurance, and fuel, should not exceed 10-15% of your net monthly income. This rule helps ensure that your car remains an asset rather than a financial burden, allowing you to focus on income growth and strategic alliances, such as those you might find on income-partners.net.

This guideline provides a balanced approach to car ownership, promoting financial stability and enabling you to pursue other financial goals. Keeping your car expenses within this range frees up capital for investments, emergency savings, and partnership opportunities that can significantly boost your income. Remember, responsible financial planning involves considering all aspects of your financial life, not just the immediate satisfaction of owning a vehicle.

2. Why Is This Percentage Important?

Why is sticking to the 10-15% rule vital? This percentage is crucial because it helps maintain a healthy financial balance, preventing your car from becoming a financial burden. According to a study by the University of Texas at Austin’s McCombs School of Business in July 2025, individuals who keep their car expenses within this range are more likely to achieve their financial goals and less likely to face financial stress. This guideline allows for a more manageable budget, enabling you to explore various revenue-generating partnerships through platforms like income-partners.net.

Adhering to this rule ensures you have enough disposable income for other essential expenses such as housing, food, healthcare, and debt repayment. Moreover, it provides a buffer for unexpected costs and allows for savings and investments that can grow your wealth over time. By not overextending yourself on car payments, you maintain financial flexibility and are better positioned to take advantage of new opportunities.

3. Factors That Influence the Affordable Percentage

What factors determine the percentage of income you can realistically spend on car payments? Several elements influence the amount you can comfortably allocate to car payments, including your income, other debts, living expenses, and financial goals. A comprehensive understanding of these factors will help you determine a suitable budget for your car while maintaining financial health and exploring partnership opportunities on income-partners.net.

3.1. Income Level

How does your income level affect your car payment affordability? Higher incomes generally allow for a larger percentage to be allocated to car payments without causing financial strain. However, it’s still crucial to adhere to the 10-15% rule to avoid lifestyle inflation and ensure sufficient funds for savings, investments, and partnership ventures.

3.2. Existing Debts

How do existing debts impact your car payment budget? High levels of existing debt, such as student loans, credit card debt, or mortgage payments, reduce the amount you can comfortably spend on a car. Prioritize paying down high-interest debts before committing to a significant car payment to improve your financial health.

3.3. Living Expenses

How do your living expenses factor into your car payment decisions? High living expenses, such as rent, utilities, and groceries, leave less room for car payments. Assess your essential living costs to accurately determine what you can afford without compromising your financial stability.

3.4. Financial Goals

How do your financial goals influence your car payment strategy? Ambitious financial goals like buying a home, starting a business, or early retirement require careful budgeting. Keeping your car payments low can free up capital to invest and pursue these goals more effectively. Platforms like income-partners.net can provide avenues for generating additional income to support these objectives.

3.5. Location

How does your location affect your car affordability? The cost of living varies significantly by location. Urban areas with higher living costs may necessitate a lower percentage allocation to car payments compared to more affordable rural areas.

4. How to Calculate Your Ideal Car Payment Percentage

How do you accurately calculate your ideal car payment percentage? To calculate the ideal percentage, start by determining your net monthly income (after taxes). Then, multiply this number by 0.10 and 0.15 to find the range of recommended monthly car payments. Remember to include all associated costs, such as insurance and fuel, to get an accurate picture. Websites like income-partners.net can offer advice on managing your finances to accommodate these expenses.

Here’s a step-by-step guide:

- Calculate your net monthly income: This is your income after taxes and other deductions.

- Multiply by 0.10: This gives you the lower end of your recommended car payment range.

- Multiply by 0.15: This gives you the upper end of your recommended car payment range.

- Factor in additional costs: Include insurance, fuel, maintenance, and other car-related expenses.

- Adjust as needed: Based on your unique financial situation and goals, adjust the percentage to ensure it aligns with your overall financial plan.

Example:

- Net Monthly Income: $5,000

- Lower End (10%): $500

- Upper End (15%): $750

In this example, your total car expenses should ideally fall between $500 and $750 per month.

5. What Happens If You Exceed the Recommended Percentage?

What are the consequences of exceeding the recommended car payment percentage? Exceeding the 10-15% guideline can lead to financial strain, making it difficult to meet other financial obligations and goals. It may result in increased debt, reduced savings, and limited opportunities for investment or business partnerships. Addressing this issue promptly is vital to maintain financial stability and explore options for revenue growth, such as those available on income-partners.net.

5.1. Increased Financial Stress

How does exceeding the limit affect your stress levels? Higher car payments can lead to increased financial stress due to the constant pressure to meet monthly obligations. This stress can negatively impact your mental and physical health, affecting your overall quality of life.

5.2. Reduced Savings

Why is it important to maintain savings? Allocating too much income to car payments reduces the amount available for savings, hindering your ability to build an emergency fund or invest for the future.

5.3. Limited Investment Opportunities

How does this affect your investments? High car payments limit your ability to invest in opportunities that can grow your wealth, such as stocks, real estate, or business ventures.

5.4. Increased Debt

What happens when you have more debt? Exceeding the recommended percentage may force you to take on additional debt to cover other expenses, creating a cycle of debt that is difficult to break.

5.5. Missed Opportunities

Why does it matter to miss business opportunities? Overspending on a car can cause you to miss out on potential business partnerships or other income-generating opportunities due to lack of available capital. Exploring platforms like income-partners.net requires having the financial flexibility to invest in promising ventures.

6. Strategies to Reduce Your Car Payment Burden

How can you effectively reduce your car payment burden? Several strategies can help reduce your car payment burden, including refinancing your loan, making extra payments, and downsizing to a more affordable vehicle. Additionally, exploring avenues for increasing your income through strategic partnerships, such as those found on income-partners.net, can provide additional financial relief.

6.1. Refinance Your Loan

What are the benefits of refinancing? Refinancing your auto loan can potentially lower your interest rate and monthly payment. Shop around for the best rates and terms to ensure significant savings.

6.2. Make Extra Payments

How can extra payments help? Making extra payments, even small ones, can significantly reduce the loan term and the total interest paid over the life of the loan.

6.3. Downsize Your Vehicle

Why should you consider a smaller vehicle? Selling your current vehicle and purchasing a more affordable model can drastically reduce your car payment. Consider the long-term financial benefits of driving a less expensive car.

6.4. Increase Your Income

How can you increase your income? Finding additional sources of income, such as freelancing, starting a side business, or leveraging platforms like income-partners.net, can provide the extra funds needed to comfortably afford your car payment.

6.5. Negotiate Insurance Rates

How do you negotiate better rates? Regularly compare car insurance quotes from different providers to ensure you are getting the best possible rate. Bundling your insurance policies can also lead to significant savings.

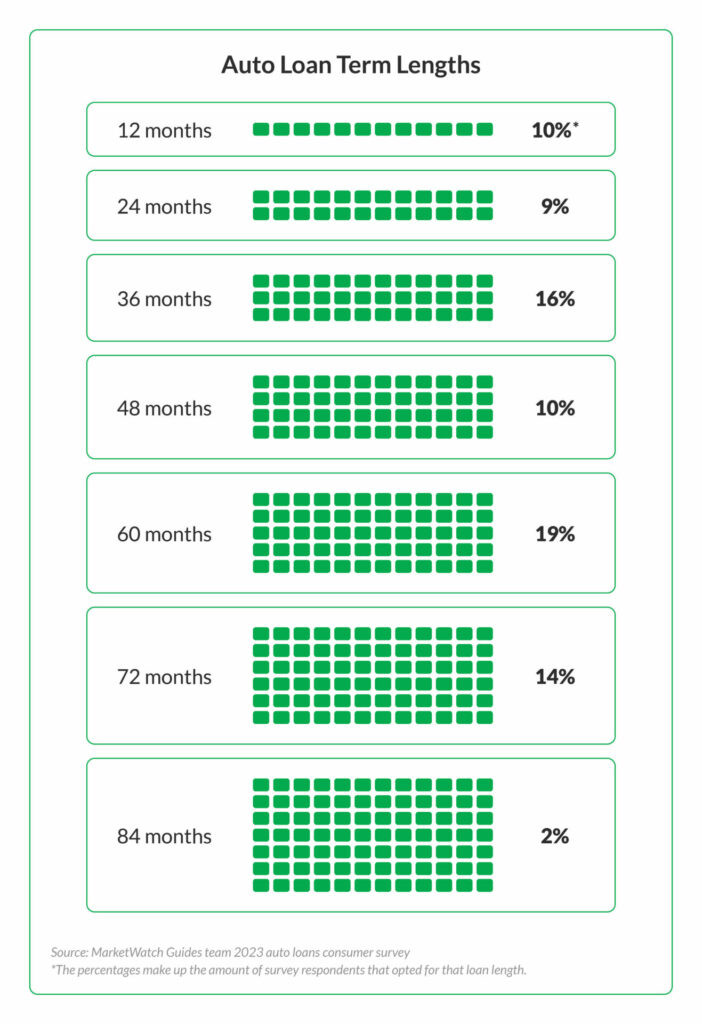

Illustration that shows seven auto term lengths and the percentages of car owners from our 2023 survey who chose those contract lengths

Illustration that shows seven auto term lengths and the percentages of car owners from our 2023 survey who chose those contract lengths

7. The Impact of Car Payments on Other Financial Goals

How do car payments affect your other financial goals? High car payments can significantly impact your ability to achieve other financial goals, such as buying a home, saving for retirement, or starting a business. By keeping your car expenses in check and exploring income-generating opportunities on platforms like income-partners.net, you can maintain progress towards your broader financial objectives.

7.1. Buying a Home

How does it affect home buying? High car payments can reduce the amount you qualify for on a mortgage, delaying or preventing you from buying a home. Lenders consider your debt-to-income ratio when approving mortgage applications.

7.2. Saving for Retirement

Why is retirement savings important? Allocating too much income to car payments can leave you with insufficient funds to save for retirement, jeopardizing your long-term financial security.

7.3. Starting a Business

How does it impact your business? High car payments can drain capital needed to start or grow a business, limiting your entrepreneurial potential. Platforms like income-partners.net can help offset these costs by providing partnership opportunities.

7.4. Paying Off Debt

What if you have other debts? Excessively high car payments can hinder your ability to pay off other debts, such as student loans or credit card balances, prolonging your debt repayment journey.

7.5. Building an Emergency Fund

Why do you need an emergency fund? Without an adequate emergency fund, unexpected expenses can force you to take on more debt or deplete your savings, setting you back financially.

8. Alternatives to Buying a Car

What alternatives are available if buying a car isn’t feasible? If buying a car stretches your budget too thin, several alternatives offer viable transportation solutions, including leasing, public transportation, carpooling, and ride-sharing services. Weighing these options can help you save money and explore alternative income streams through sites like income-partners.net.

8.1. Leasing

What are the pros and cons of leasing? Leasing a car typically involves lower monthly payments compared to buying, but it comes with mileage restrictions and no ownership at the end of the lease term.

8.2. Public Transportation

How does public transport help you save money? Utilizing public transportation, such as buses, trains, and subways, can significantly reduce your transportation costs, freeing up funds for other financial goals.

8.3. Carpooling

Why should you consider carpooling? Carpooling with coworkers or neighbors can help split commuting costs and reduce wear and tear on your vehicle.

8.4. Ride-Sharing Services

When should you use ride-sharing? Ride-sharing services like Uber and Lyft offer convenient transportation options without the costs of car ownership, making them ideal for occasional use.

8.5. Biking or Walking

Are biking and walking viable options? Biking or walking can be great options for short commutes, providing exercise while saving on transportation costs.

9. The Role of Credit Score in Determining Affordability

How does your credit score influence your car payment affordability? Your credit score plays a significant role in determining the interest rate you’ll receive on an auto loan, which directly affects your monthly car payment. A higher credit score translates to lower interest rates and more favorable loan terms, making car ownership more affordable. Conversely, a low credit score can result in higher interest rates, increasing your monthly payments and the total cost of the loan. Regularly checking and improving your credit score can lead to substantial savings over the life of the loan.

9.1. Impact on Interest Rates

How do interest rates affect your budget? A high credit score can secure lower interest rates, reducing the overall cost of the loan. According to Experian, borrowers with excellent credit scores (720 or higher) typically receive the best interest rates on auto loans.

9.2. Loan Approval

Why is loan approval important? A good credit score increases your chances of loan approval, while a poor credit score may result in denial or require a larger down payment.

9.3. Negotiating Power

How can you negotiate better terms? A strong credit history gives you more negotiating power with lenders, allowing you to secure better terms and conditions.

9.4. Long-Term Savings

What are the long-term benefits of a good credit score? Over the life of the loan, a better credit score can save you thousands of dollars in interest payments.

9.5. Credit Score Improvement

How do you improve your credit score? Improving your credit score involves paying bills on time, reducing your credit utilization ratio, and avoiding new debt. Regularly monitor your credit report for errors and take steps to correct them.

10. Frequently Asked Questions (FAQs)

What are some common questions about car payments and affordability? Here are some frequently asked questions to help you better understand how to manage your car payments effectively and achieve financial stability.

-

What is the ideal debt-to-income ratio for car payments?

The ideal debt-to-income ratio for car payments should be no more than 10-15% of your net monthly income.

-

Can I afford a car if my credit score is low?

It may be more challenging, but you can still get a car loan with a low credit score, though expect higher interest rates. Focus on improving your credit score before applying for a loan.

-

Should I include insurance and fuel costs when calculating affordability?

Yes, always include insurance, fuel, and maintenance costs when calculating how much you can afford for a car.

-

Is it better to lease or buy a car?

The best option depends on your financial situation and driving habits. Leasing usually has lower monthly payments, but buying builds equity.

-

How can I lower my car insurance costs?

Shop around for quotes, increase your deductible, and inquire about discounts to lower your car insurance costs.

-

What are the risks of a long-term car loan?

Long-term car loans can lead to higher interest payments and an increased risk of owing more than the car is worth.

-

How does my down payment affect my monthly payment?

A larger down payment reduces the amount you need to borrow, resulting in lower monthly payments.

-

What should I do if I can’t afford my car payments?

Contact your lender to discuss options like refinancing or loan modification. Consider selling the car and buying a more affordable model.

-

How often should I review my car payment budget?

Review your car payment budget at least once a year or whenever there are significant changes in your income or expenses.

-

Where can I find reliable advice on managing my car expenses?

Consult financial advisors, utilize online resources, and explore platforms like income-partners.net for expert advice on managing your car expenses effectively.

Navigating the world of car payments requires a balanced approach, blending financial prudence with strategic income growth. By adhering to the 10-15% rule and exploring partnership opportunities on platforms like income-partners.net, you can ensure your car remains a valuable asset rather than a financial burden.

Ready to take control of your finances and find the perfect partnerships to boost your income? Visit income-partners.net today to discover a wealth of resources, strategies, and opportunities to help you achieve your financial goals. Don’t let high car payments hold you back – explore how strategic alliances can pave the way to financial freedom. Contact us at Address: 1 University Station, Austin, TX 78712, United States. Phone: +1 (512) 471-3434 or visit our website to get started today.