What Percentage Of Income Should Go To Car expenses? Ideally, aim to keep your total car expenses, including car payments, insurance, gas, and maintenance, below 15% of your monthly net income, providing a balance between transportation needs and financial well-being. At income-partners.net, we understand that striking this balance is key for entrepreneurs, business owners, investors, marketing experts and those seeking new business ventures, especially in thriving hubs like Austin, USA. Effective financial planning, including setting a realistic car budget, is crucial for maximizing your income and partnership opportunities.

1. Understanding the Golden Rule: The 15% Guideline

A common financial rule of thumb suggests allocating no more than 15% of your monthly net income to total car expenses. This includes your car payment, insurance, gas, and maintenance. Sticking to this guideline helps ensure your transportation costs don’t eat into your ability to invest, save, or pursue other business opportunities through platforms like income-partners.net.

Why 15%? The Rationale

The 15% guideline is designed to balance transportation needs with overall financial health. Here’s why it’s a good benchmark:

- Budget Flexibility: It leaves room for other essential expenses like housing, food, and healthcare.

- Investment Opportunities: Keeping car costs low frees up capital for investments, a key focus for our audience at income-partners.net.

- Savings and Emergency Funds: It allows you to build a financial cushion for unexpected events and long-term goals.

- Partnership Pursuits: By managing your finances wisely, you have more resources to explore and leverage partnership opportunities.

Breaking Down the 15%

While the 15% rule is a great starting point, it’s helpful to break it down further:

- Car Payment: This should ideally be the largest portion, but still manageable.

- Insurance: Shop around for the best rates to keep this cost down.

- Fuel: Consider fuel-efficient vehicles or alternative transportation methods.

- Maintenance: Regular maintenance can prevent costly repairs down the line.

For example, if your monthly take-home pay is $6,000, your total car expenses should ideally not exceed $900.

2. Calculate Your Monthly Car Payment: A Step-by-Step Approach

To calculate your monthly car payment effectively, start with your post-tax take-home pay, also known as net pay. This gives you a more realistic view of what you can afford compared to using your annual salary or gross pay. Deduct recurring expenses, bills, and other monthly budget items from your take-home pay to determine a safe, potential monthly payment range.

Gathering Your Financial Information

To start, gather the following:

- Wage or salary information

- Current bank statements

- Records of monthly and annual expenses

Using Net Pay for a Realistic Assessment

Net pay provides a clearer picture of your disposable income. Unlike gross pay, which doesn’t account for taxes and other deductions, net pay reflects the actual money you have available.

Accounting for Recurring Expenses

Deduct all recurring expenses from your net pay. This includes:

- Rent or mortgage payments

- Utilities

- Groceries

- Loan payments

- Credit card bills

- Entertainment

The remaining amount is what you can realistically allocate to car-related expenses.

Example Calculation

Let’s say your monthly net pay is $5,000. Your recurring expenses total $3,000. This leaves you with $2,000. According to the 15% rule, you should aim for total car expenses of no more than $750 per month.

3. MarketWatch Guidance: Factors to Consider for Financial Health

It’s crucial not to max out your budget. Unexpected financial strains can arise, so keep your anticipated monthly car payments within reasonable limits. Always maintain room in your budget for extra expenses.

Importance of Staying Within Reasonable Ranges

Staying within reasonable car payment ranges is vital for financial stability. Overextending yourself can lead to financial stress and limit your ability to pursue investment or partnership opportunities.

Allowing Room for Unexpected Expenses

Unexpected expenses are a part of life. Whether it’s a medical bill, home repair, or sudden job loss, having a financial cushion is essential. By keeping car payments manageable, you can better handle these unforeseen events.

Being Realistic About Loan Terms

Loan companies typically offer terms between 24 and 84 months for both used and new cars. Opting for a longer loan term can result in lower monthly payments, but you’ll pay more overall due to accumulated interest. Longer loan terms also increase the risk of owing more on the loan than the vehicle is worth, especially as a vehicle’s value decreases over time.

The Risk of Upside-Down Loans

Going upside-down on a loan means you owe more than the vehicle is worth. This can happen quickly if you choose a long loan term and the car depreciates faster than you pay it off. It’s important to weigh your options carefully before deciding which vehicle to purchase.

According to a study by the University of Texas at Austin’s McCombs School of Business in July 2025, consumers with longer loan terms are significantly more likely to find themselves in an upside-down loan situation.

4. Salary-Based Car Payment Guidelines: A Quick Reference Table

To provide a clear understanding of affordable car payments based on income, here’s a table outlining recommended monthly car payment limits based on your post-tax take-home pay:

| Monthly Take-Home Pay (Post-Tax) | Monthly Car Payments Should Not Exceed… |

|---|---|

| $1,500 | $150 to $225 per month |

| $3,000 | $300 to $450 per month |

| $4,500 | $450 to $675 per month |

| $6,000 | $600 to $900 per month |

| $7,500 | $750 to $1,125 per month |

| $9,000 | $900 to $1,350 per month |

This table provides a quick reference to help you gauge what is affordable based on your income, aligning with the principles of sound financial planning crucial for those seeking partnership opportunities on income-partners.net.

5. Beyond the Payment: Fuel and Insurance Costs

Before committing to a vehicle, factor in fuel and insurance costs. These expenses can significantly impact your overall car budget. Both costs are heavily influenced by your location, driving history, and the type of vehicle you choose.

Fuel Costs: Factors to Consider

- Vehicle Fuel Efficiency: Choose a fuel-efficient car to save on gas costs.

- Driving Habits: Aggressive driving can decrease fuel efficiency.

- Gas Prices: Monitor gas prices and plan your routes accordingly.

- Commute Length: Longer commutes will result in higher fuel costs.

Insurance Costs: Factors to Consider

- Driving History: A clean driving record can lower insurance premiums.

- Age and Gender: Younger drivers and males typically pay more for insurance.

- Location: Urban areas often have higher insurance rates than rural areas.

- Coverage Level: Higher coverage levels come with higher premiums.

Utilizing Resources for Estimation

The U.S. Department of Energy provides a detailed list of fuel economy figures and a comparison tool to check different vehicles’ annual fuel cost estimates. For auto insurance quotes, contact your agent or an insurance company. Comparing quotes can provide insights into potential expenses.

Keeping Total Costs Within Limits

When calculating your monthly car payment and related expenses, aim to keep the total costs to less than 20% of your monthly take-home pay. This ensures you have sufficient funds for other financial goals.

6. Loan Amount and Term Length: Making Informed Decisions

Once you’ve determined your affordable monthly payment, you can calculate how much you can borrow. The amount a lender will let you borrow hinges on several factors, including whether you’re buying a used or new car, your credit score, and your loan term.

Factors Affecting Loan Amount

- New vs. Used Car: New car loans generally have lower annual percentage rates (APRs) than used cars.

- Credit Score: Your credit score affects the APR on the loan and the amount the bank is willing to lend you.

- Loan Term: The loan term is the number of months you’ll have to pay off your auto loan.

Impact of Credit Score on Loan Terms

Your credit score plays a significant role in determining the interest rate you’ll receive on your car loan. A higher credit score typically results in a lower interest rate, saving you money over the life of the loan.

Choosing the Right Loan Term

Selecting the right loan term is essential. Longer loan terms can lower monthly payments, but you’ll pay more in interest over time. Shorter loan terms result in higher monthly payments but less overall interest.

Balancing Loan Terms with Financial Goals

Consider your financial goals when choosing a loan term. If you want to pay off the loan quickly and minimize interest, opt for a shorter term. If you need lower monthly payments to manage your budget, a longer term may be necessary.

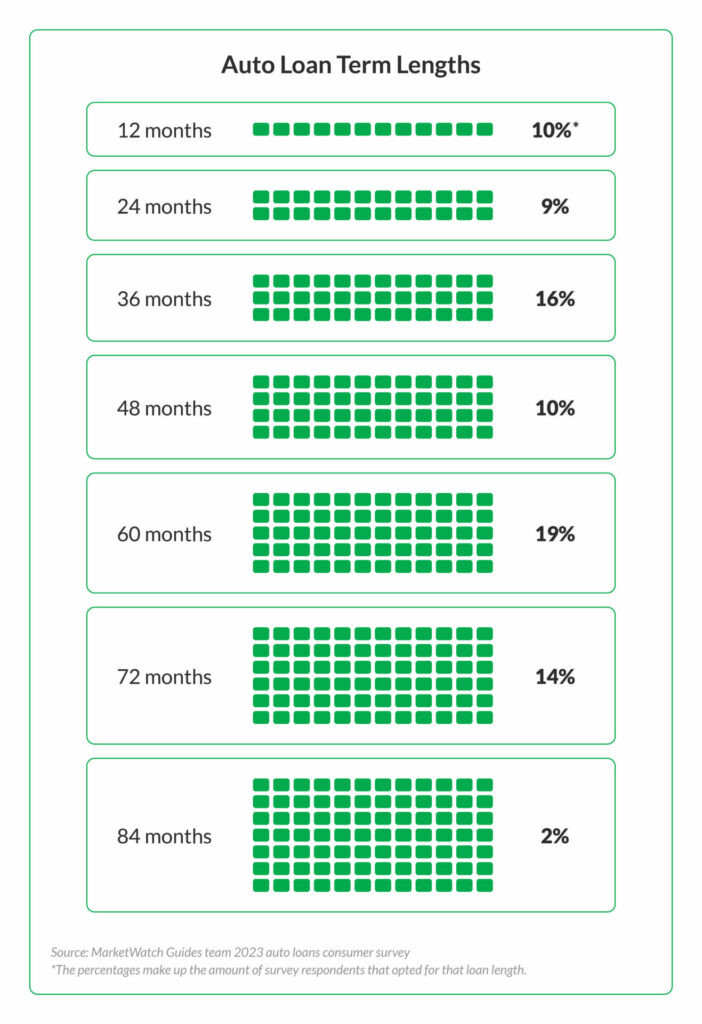

Illustration that shows seven auto term lengths and the percentages of car owners from our 2023 survey who chose those contract lengths

Illustration that shows seven auto term lengths and the percentages of car owners from our 2023 survey who chose those contract lengths

Illustration displaying seven auto term lengths with corresponding percentages from a 2023 survey illustrating consumer preferences in auto loan contracts.

7. Purchase Price: Beyond the Sticker Price

The total loan amount you calculated for your car might not be the final price you pay. When shopping for a car, consider factors beyond the sticker price. In most states, you’ll have to pay sales tax and fees, whether you buy a new or used car.

Sales Tax and Fees: Understanding the Costs

- Sales Tax: Sales tax rates vary by state, potentially reaching up to 12.9%.

- Registration Fees: Registration fees typically range from $50 to $300, though some states can be much more expensive.

- Documentation Fees: Documentation fees generally range between $100 and $500, depending on your state.

Strategies to Lower the Purchase Price

Making a down payment or trading in your old car can reduce the amount you need to borrow when purchasing a vehicle. These strategies can help lower your monthly payments and overall loan costs.

The Importance of Negotiation

Don’t hesitate to negotiate the purchase price. Dealerships often have room to lower the price, especially if you’re prepared to walk away.

8. Real-World Examples: Aligning Car Expenses with Income

To illustrate how different income levels can manage car expenses effectively, let’s consider a few real-world examples:

| Income Level | Monthly Net Income | Recommended Car Expense Limit (15%) | Example Scenario |

|---|---|---|---|

| Entry-Level | $3,000 | $450 | A young professional chooses a reliable used car with a monthly payment of $250, insurance of $100, and allocates $100 for gas and maintenance. |

| Mid-Career | $6,000 | $900 | A mid-career manager leases a new sedan for $500 per month, pays $150 for insurance, and budgets $250 for gas and maintenance. |

| Executive | $9,000 | $1,350 | An executive purchases a luxury SUV with a monthly payment of $800, pays $250 for comprehensive insurance, and budgets $300 for gas and maintenance. |

These examples demonstrate how individuals with varying income levels can align their car expenses with the 15% guideline, ensuring financial stability and the ability to pursue other opportunities.

9. Income-Partners.Net: Your Platform for Financial Growth

At income-partners.net, we understand the importance of managing your finances to maximize your income and partnership opportunities. Whether you’re an entrepreneur, business owner, investor, or marketing expert, our platform provides the resources and connections you need to succeed.

Leveraging Partnerships for Financial Success

Partnering with the right individuals and businesses can significantly boost your income and financial stability. Income-partners.net offers a diverse network of potential partners, allowing you to explore new ventures and expand your business.

Financial Planning Resources and Tools

Our website provides a range of financial planning resources and tools to help you manage your budget, make informed investment decisions, and achieve your financial goals.

Success Stories: How Partnerships Drive Growth

We feature success stories of individuals and businesses that have leveraged partnerships to achieve remarkable financial growth. These stories provide inspiration and practical insights for our users.

Income-partners.net is committed to helping you achieve financial success through strategic partnerships and sound financial management.

10. Call to Action: Explore Opportunities on Income-Partners.Net

Ready to take control of your financial future and explore lucrative partnership opportunities? Visit income-partners.net today to discover how you can connect with potential partners, access financial planning resources, and achieve your financial goals.

Connect with Potential Partners

Our platform makes it easy to find and connect with like-minded individuals and businesses. Whether you’re seeking investors, collaborators, or strategic partners, income-partners.net can help you build valuable relationships.

Access Financial Planning Resources

We offer a wealth of financial planning resources, including articles, guides, and tools, to help you manage your budget, make informed investment decisions, and achieve financial freedom.

Achieve Your Financial Goals

With the right partnerships and financial strategies, you can achieve your financial goals and build a secure future. Income-partners.net is your partner in this journey.

Don’t wait—start exploring the opportunities on income-partners.net today and take the first step toward financial success. Address: 1 University Station, Austin, TX 78712, United States. Phone: +1 (512) 471-3434.

Frequently Asked Questions (FAQ)

1. What is the 15% rule for car expenses?

The 15% rule suggests allocating no more than 15% of your monthly net income to total car expenses, including car payments, insurance, gas, and maintenance, ensuring balanced transportation and financial health.

2. Why is it important to use net pay instead of gross pay when calculating car affordability?

Using net pay provides a clearer picture of your disposable income, as it accounts for taxes and other deductions, reflecting the actual money available for car-related expenses.

3. What factors should I consider when determining fuel costs?

Consider vehicle fuel efficiency, driving habits, gas prices, and commute length to estimate fuel costs accurately.

4. How does my credit score affect my car loan?

A higher credit score typically results in a lower interest rate on your car loan, saving you money over the life of the loan.

5. What are some strategies to lower the purchase price of a car?

Making a down payment, trading in your old car, and negotiating the purchase price can lower the amount you need to borrow.

6. What are the risks of choosing a longer loan term for a car?

Longer loan terms can lead to paying more in interest over time and increase the risk of owing more on the loan than the vehicle is worth.

7. How can income-partners.net help me manage my finances and find partnership opportunities?

income-partners.net provides resources, tools, and a diverse network of potential partners to help you manage your budget, make informed investment decisions, and explore new business ventures.

8. What is the ideal percentage of income to allocate to car insurance?

While it varies, aiming for car insurance to be no more than 2-3% of your monthly net income is a good starting point, adjusting based on individual circumstances and coverage needs.

9. How often should I reassess my car budget?

You should reassess your car budget at least annually or whenever there are significant changes in your income, expenses, or financial goals.

10. Are there alternative transportation options to reduce car expenses?

Yes, consider public transportation, biking, walking, or carpooling to reduce fuel costs and wear and tear on your vehicle, potentially freeing up more of your income for other financial goals.