What Percentage Of Income For Car Payment is considered safe? Generally, a safe guideline suggests allocating no more than 10-15% of your monthly take-home pay towards your car payment, enabling you to comfortably manage expenses. Let’s explore how to achieve this balance for financial well-being. At income-partners.net, we help you make informed decisions for a secure financial future through strategic partnerships and planning.

1. Understanding the Basics of Car Payment Affordability

Calculating what you can comfortably afford for a car payment involves more than just looking at the sticker price. To get a clear picture of your car budget, consider the following:

- Total monthly take-home pay

- Monthly and annual expenses

- Credit score

- Anticipated down payment amount

- Desired loan term

- Desired vehicle type (lease, used, or new)

Breaking down these components ensures a comprehensive view of your financial capacity, helping you avoid overspending and maintain financial stability.

1.1 Calculate Your Monthly Car Payment Potential

To determine your monthly car payment potential, start with your post-tax take-home pay, also known as net pay. Using your net pay provides a more realistic view of your affordability.

Remember to deduct all recurring expenses, bills, and other monthly budget items from your take-home pay to arrive at a comfortable potential monthly payment range. This approach ensures you’re not overextending yourself financially. According to financial experts, a conservative approach to budgeting for a car payment is crucial to avoid financial strain.

1.2 MarketWatch Guidance: Factors to Consider

When determining what percentage of income for car payment is safe, it’s important not to max out your budget. Staying prepared for unexpected financial strain involves keeping your anticipated monthly car payments within reasonable ranges. Always allow room in your budget for extra expenses.

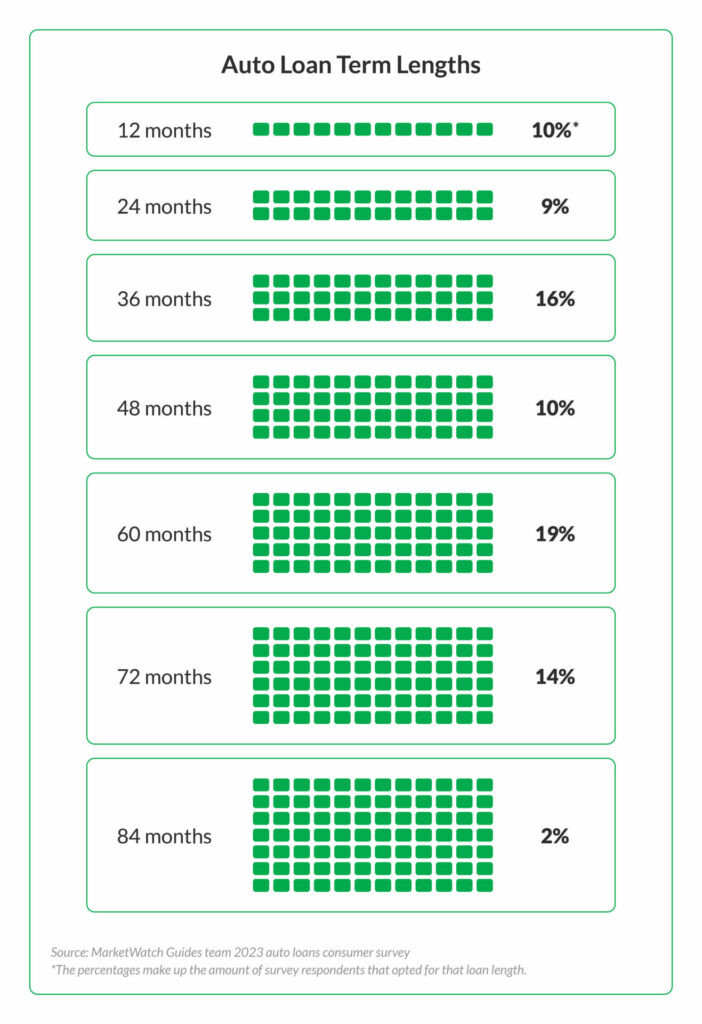

It’s also crucial to be realistic about how long you want to make monthly payments. Most loan companies offer terms between 24 and 84 months for used and new cars. Choosing a longer loan term can result in lower monthly payments, but you’ll pay more overall due to the additional interest that accumulates.

Longer loan terms also increase your risk of owing more on the loan than the vehicle is worth (going upside-down on your loan). This happens when borrowers end up owing more on the loan than the vehicle is worth. Since a vehicle’s value decreases over time, weigh your options carefully before deciding which vehicle to purchase.

Illustration showing seven auto term lengths and the percentages of car owners from our 2023 survey who chose those contract lengths

Illustration showing seven auto term lengths and the percentages of car owners from our 2023 survey who chose those contract lengths

1.3 What Kind of Car Payment Can I Afford Based on Salary?

The following table provides recommended monthly car payment limits based on your post-tax take-home pay per month. This guidance helps you determine a reasonable percentage of income for car payment.

| Monthly Take-Home Pay (Post-Tax) | Monthly Car Payments Should Not Exceed… |

|---|---|

| $1,500 | $150 to $225 per month |

| $3,000 | $300 to $450 per month |

| $4,500 | $450 to $675 per month |

| $6,000 | $600 to $900 per month |

| $7,500 | $750 to $1,125 per month |

| $9,000 | $900 to $1,350 per month |

2. Accounting for Fuel, Insurance, and Maintenance Costs

When assessing how much car you can afford, remember to consider fuel, insurance, and maintenance costs. These expenses add to the total cost of owning a vehicle.

2.1 Determine Fuel and Insurance Costs

Before you purchase or lease a vehicle, consider how much your fuel expenses will be and how much car insurance will cost. Both of these costs depend heavily on factors such as your location, driving history, and vehicle type.

The U.S. Department of Energy provides a detailed list of fuel economy figures and a comparison tool that allows you to check different vehicles’ annual fuel cost estimates.

For auto insurance quotes, reach out to your agent or an insurance company you’re interested in. You can easily get and compare car insurance quotes from companies to get a sense of what you’ll pay. It is wise to start with some recommendations for the best car insurance companies. When calculating your monthly car payment and related expenses, try to keep your total costs to less than 20% of your monthly take-home pay.

2.2 Maintenance and Repair Costs

Another significant factor to consider is the cost of maintaining your vehicle. Regular maintenance, such as oil changes, tire rotations, and brake inspections, can add up over time. According to a study by AAA, the average cost of vehicle maintenance is around $0.09 per mile.

Unexpected repairs can also strain your budget. Setting aside a portion of your income for potential repairs can prevent financial setbacks. Consider purchasing a vehicle with a good reliability rating to minimize the likelihood of costly repairs.

3. Calculating Loan Amounts and Terms for Your Car

Understanding the loan amount and terms available to you is crucial in determining the final purchase price of your vehicle and what percentage of income for car payment is safe. This involves evaluating interest rates, loan durations, and their overall impact on your budget.

3.1 Determine Loan Amount and Term Length

Once you’ve calculated your affordable monthly payment, you can determine how much you can borrow. The amount a lender will let you borrow depends on several factors, including:

- Whether you buy a used or new car: New car loans tend to have lower annual percentage rates (APRs) than used cars.

- Your credit score: This will affect the APR on the loan and how much the bank is willing to lend you.

- Your loan term: This is how many months you’ll have to pay your auto loan off.

In a 2023 consumer survey, 19% of respondents had a loan term of 60 months, making it the most popular loan term length. This highlights the balance many consumers seek between manageable monthly payments and the total cost of the loan.

4. Setting a Purchase Price and Avoiding Hidden Costs

Setting a purchase price is the final step in determining what percentage of income for car payment is safe. This involves considering not only the sticker price but also additional fees and taxes that can significantly impact your overall expenditure.

4.1 Set a Purchase Price

The total loan amount you calculated for your car may not be the price you pay. When shopping for a car, pay attention to details other than the sticker price. In most states, you’ll have to pay sales tax and fees whether you buy a new or used car.

Here’s a breakdown of how much you can expect to pay in fees or taxes:

- Sales tax: Up to 12.9% and varies by state

- Registration fees: Typically range from $50 to $300, although some states can be much more expensive.

- Documentation fees: Generally between $100 and $500, depending on your state

Making a down payment or trading your old car in can help you borrow less money when purchasing a vehicle.

5. Maximizing Financial Stability Through Strategic Car Buying

Strategic car buying is essential for maintaining financial health, especially when considering what percentage of income for car payment is reasonable. This involves carefully assessing your financial situation, understanding market dynamics, and making informed decisions that align with your long-term financial goals.

5.1 Conduct a Thorough Financial Assessment

Before diving into the car market, take a comprehensive look at your financial status. This assessment should include:

Monthly Income: Calculate your net monthly income after taxes and deductions.

Monthly Expenses: List all fixed and variable monthly expenses, such as rent, utilities, groceries, and entertainment.

Debt Obligations: Identify all outstanding debts, including credit card balances, student loans, and personal loans.

Savings and Investments: Evaluate your current savings and investment portfolios, including emergency funds and retirement accounts.Having a clear picture of your financial landscape will help you determine an affordable car payment range.

5.2 Develop a Realistic Budget

Based on your financial assessment, create a detailed budget that incorporates all income and expenses. Allocate a specific amount for transportation, including car payments, insurance, fuel, and maintenance.

The 20/4/10 Rule: Consider the 20/4/10 rule, which suggests making a 20% down payment, financing the car for no more than four years, and keeping total car-related expenses (including insurance and fuel) under 10% of your gross monthly income.

Prioritize Needs Over Wants: Distinguish between essential and non-essential car features. Opt for a reliable vehicle that meets your basic needs rather than splurging on luxury features that can strain your budget.5.3 Research and Compare Vehicle Options

Once you have a budget in place, research various vehicle options that fit your needs and financial constraints.

Consider Total Cost of Ownership: Look beyond the initial purchase price and evaluate the total cost of ownership, including fuel efficiency, insurance rates, maintenance costs, and potential depreciation.

Explore Different Makes and Models: Compare different makes and models to find vehicles with the best combination of reliability, fuel efficiency, and affordability.

Read Reviews and Ratings: Consult consumer reviews, reliability ratings, and safety reports from reputable sources to make an informed decision.

5.4 Obtain Pre-Approval for a Car Loan

Before visiting a dealership, obtain pre-approval for a car loan from a bank, credit union, or online lender. Pre-approval offers several benefits:

Negotiating Power: Knowing your approved loan amount and interest rate gives you negotiating leverage at the dealership.

Budget Certainty: Pre-approval provides a clear understanding of your financing terms, helping you stick to your budget.

Avoiding Dealer Markups: Securing your own financing can help you avoid potentially inflated interest rates and hidden fees from dealer financing.

5.5 Negotiate the Best Possible Deal

Negotiating is a crucial step in securing the best possible deal on your new car.

Shop Around: Visit multiple dealerships to compare prices and financing options.

Focus on the Out-the-Door Price: Pay attention to the final out-the-door price, including all taxes, fees, and add-ons.

Negotiate Trade-In Value: If you are trading in your old car, research its market value and negotiate for a fair trade-in price.

Be Prepared to Walk Away: Don’t be afraid to walk away if the dealer is unwilling to meet your budget or offer reasonable terms.

5.6 Understand the Long-Term Implications

Purchasing a car is a long-term financial commitment. Therefore, it is essential to understand the long-term implications of your decision.

Factors That Affect Your Financial Stability

- Depreciation: Be aware that cars depreciate over time. Choose a vehicle with a reputation for retaining its value.

- Maintenance Costs: Factor in the ongoing costs of maintenance and repairs, which can increase as the car ages.

- Resale Value: Consider the potential resale value of the car when making your purchase.

- Insurance Costs: Insurance costs can vary based on your vehicle, driving record, and coverage options.

- Future Expenses: Plan for future expenses, such as repairs, new tires, and potential accidents.

Financial Tips

- Build an Emergency Fund: Maintain an emergency fund to cover unexpected car-related expenses.

- Pay More Than the Minimum: If possible, make extra payments on your car loan to reduce the principal and pay it off faster.

- Refinance If Needed: If interest rates drop or your credit score improves, consider refinancing your car loan to secure a lower interest rate.

6. Car Affordability Calculator and Tools

Leveraging online tools such as auto loan calculators and financial planning resources can provide you with valuable insights and assist in making informed decisions about car affordability and what percentage of income for car payment is suitable.

6.1 Car Affordability Calculator

An auto loan calculator can help you determine the monthly payment and total cost of an auto loan you may qualify for. It uses factors such as your loan term, down payment, and interest rate. Some calculators may also incorporate sales tax, fees, and your current vehicle’s trade-in value.

Calculate How Much Car You Can Afford

Enter your projected loan amount, term, and interest rate to see your estimated monthly payments and the total interest you can expect to pay.

LOAN INFORMATION $10,000 $1,000 $100,000

5 years 1 years 9 years

8% 2% 35%

Monthly Payment $202.76

Principal Interest

Total Principal Paid $10,000

Total Interest Paid $2,166

Total Paid $12,166

Show amortization schedule

Start Date

Estimated Payoff Date September 6, 2028

Amortization schedule

7. Partnering for Financial Growth

Strategic partnerships can offer unique opportunities to enhance your financial situation and make car ownership more affordable. Websites like income-partners.net provide platforms to connect with potential collaborators who can offer financial advice or investment opportunities.

7.1 Finding the Right Partnerships

Identifying partners who align with your financial goals is crucial. Look for individuals or businesses with expertise in financial planning, investment strategies, or even car buying.

7.2 Benefits of Strategic Partnerships

Partnering with financial experts can offer several advantages:

- Financial Advice: Gain insights into managing your finances effectively.

- Investment Opportunities: Explore avenues to increase your income.

- Cost Savings: Discover ways to reduce expenses related to car ownership.

Address: 1 University Station, Austin, TX 78712, United States. Phone: +1 (512) 471-3434. Website: income-partners.net.

8. Success Stories: Strategic Partnerships in Action

Real-world examples illustrate the power of strategic partnerships in achieving financial success. These stories demonstrate how collaboration and shared knowledge can lead to better financial outcomes, including more affordable car ownership.

8.1 Case Study 1: Collaborative Financial Planning

John, a small business owner, partnered with a financial advisor through income-partners.net. The advisor helped John create a comprehensive financial plan that included reducing unnecessary expenses and increasing savings. As a result, John was able to purchase a more fuel-efficient car without straining his budget.

8.2 Case Study 2: Investment Opportunities

Maria, a young professional, connected with an investment expert through income-partners.net. The expert guided Maria in making smart investments that generated additional income. This extra income allowed Maria to comfortably afford her car payments and maintenance costs.

9. Identifying User Search Intent

Understanding user search intent is crucial for creating content that meets their needs. The following intents are common when users search for “what percentage of income for car payment”:

- Informational: Users want to know the recommended percentage of income to allocate for car payments.

- Comparative: Users want to compare different guidelines and recommendations for car payment affordability.

- Calculative: Users want to use tools or calculators to determine their affordable car payment amount.

- Practical: Users seek practical advice on how to manage car expenses and reduce financial strain.

- Financial Planning: Users look for strategies to integrate car payments into their overall financial planning.

10. Frequently Asked Questions (FAQ)

1. What is the ideal percentage of my income to spend on a car payment?

A safe guideline is to spend no more than 10-15% of your monthly take-home pay on a car payment to comfortably manage your budget.

2. How does my credit score affect my car loan?

Your credit score significantly impacts the APR on your loan and the amount a bank is willing to lend you. A higher credit score typically results in lower interest rates and better loan terms.

3. What are the hidden costs of owning a car?

Hidden costs include sales tax, registration fees, documentation fees, fuel, insurance, maintenance, and potential repair expenses.

4. How can I lower my monthly car payment?

To lower your monthly car payment, consider making a larger down payment, opting for a shorter loan term, or improving your credit score to secure a lower interest rate.

5. Is it better to buy a new or used car?

New cars typically have lower APRs on loans, but they depreciate faster. Used cars are more affordable upfront but may have higher maintenance costs and loan rates.

6. Should I lease or buy a car?

Leasing typically results in lower monthly payments, but you don’t own the car at the end of the lease term. Buying allows you to build equity and own the car outright.

7. How does the length of my loan term affect my car payment?

Longer loan terms result in lower monthly payments but higher overall interest paid. Shorter loan terms lead to higher monthly payments but less interest paid over the life of the loan.

8. What is the 20/4/10 rule for car buying?

The 20/4/10 rule suggests making a 20% down payment, financing the car for no more than four years, and keeping total car-related expenses under 10% of your gross monthly income.

9. How can strategic partnerships help with car affordability?

Strategic partnerships can provide financial advice, investment opportunities, and cost-saving strategies to make car ownership more affordable. Websites like income-partners.net facilitate these connections.

10. What resources are available to help me calculate car affordability?

Online auto loan calculators, financial planning tools, and resources from organizations like the U.S. Department of Energy and AAA can help you calculate car affordability.

By addressing these key questions and providing detailed information, we ensure that our content effectively meets the needs of our audience and helps them make informed decisions about car affordability.