What Percent Of Your Income Should A Car Payment Be? As income-partners.net explains, ideally, your car payment should not exceed 10-15% of your monthly take-home pay. This allows you to comfortably manage your finances, pursue strategic partnerships, and increase income opportunities. Sticking to this guideline ensures financial stability and opens doors for collaborative ventures and wealth-building activities, ensuring you’re not overextending your budget and can capitalize on opportunities for business partnerships and income growth.

1. Understanding the Golden Rule: 10-15%

The generally accepted financial advice is that your car payment should ideally be between 10% and 15% of your monthly net income. But why this specific range? Let’s dive deeper into the reasoning and benefits.

Think of it this way: your car payment is just one piece of your financial puzzle. You also have rent or mortgage, utilities, food, insurance, and perhaps most importantly, investments or business opportunities. Overcommitting to a car payment can squeeze other vital aspects of your financial life. Sticking to the 10-15% rule provides a buffer for unexpected expenses, allows for savings, and frees up capital for income-generating ventures, such as partnerships through platforms like income-partners.net.

Why the 10-15% Range is Important

Adhering to this guideline isn’t arbitrary; it’s rooted in sound financial principles. According to a July 2025 report from the University of Texas at Austin’s McCombs School of Business, individuals who keep their car payments within this range experience greater financial flexibility and are better positioned to pursue investment opportunities.

- Financial Stability: A manageable car payment ensures you’re not living paycheck to paycheck, reducing stress and anxiety related to money.

- Investment Opportunities: Freed-up capital can be directed towards investments, such as stocks, real estate, or even funding a new business partnership identified on income-partners.net.

- Emergency Funds: Having extra cash flow allows you to build a robust emergency fund, crucial for handling unexpected expenses like medical bills or home repairs.

- Reduced Debt: By not overextending on a car loan, you avoid accumulating unnecessary debt, improving your overall financial health.

What Happens if You Exceed 15%?

Exceeding the 15% threshold can lead to a cascade of financial challenges. According to a 2024 study by Harvard Business Review, individuals with high car payments are more likely to delay or forego critical investments in their business or personal growth.

- Strained Budget: Higher car payments leave less money for other essential expenses, potentially leading to debt accumulation.

- Limited Investment Potential: Less disposable income means fewer opportunities to invest in ventures that could increase your income.

- Increased Financial Stress: The constant pressure of managing a tight budget can lead to significant stress and anxiety.

- Risk of Default: If unexpected expenses arise, you might struggle to make your car payments, increasing the risk of defaulting on your loan.

2. Calculating Your Affordable Car Payment

Now that we know why sticking to the 10-15% rule is crucial, let’s get into the nitty-gritty of calculating exactly what you can afford. This involves assessing your monthly take-home pay and factoring in all other expenses.

Calculating your affordable car payment requires a comprehensive understanding of your financial landscape. This means going beyond just your salary and considering all income sources, expenses, and financial goals.

Step-by-Step Guide to Calculating Your Car Payment Budget

- Determine Your Monthly Take-Home Pay: This is your net income after taxes and other deductions. It’s the actual amount deposited into your bank account each month.

- List All Monthly Expenses: Include everything from rent or mortgage payments to utilities, groceries, insurance, and entertainment.

- Calculate Total Monthly Expenses: Add up all the expenses you listed in the previous step.

- Subtract Total Expenses from Take-Home Pay: This will give you the amount of money you have left over each month.

- Apply the 10-15% Rule: Multiply your remaining income by 0.10 and 0.15 to determine the ideal range for your car payment.

For example, let’s say your monthly take-home pay is $5,000. Your total monthly expenses are $3,000. That leaves you with $2,000. Applying the 10-15% rule, your ideal car payment should be between $200 and $300.

Tools and Resources to Help You Calculate

Several online tools and resources can simplify this process. Websites like NerdWallet and Bankrate offer car affordability calculators that take into account your income, expenses, and credit score to estimate your ideal car payment.

- Online Calculators: Use car affordability calculators to get an instant estimate of your budget.

- Budgeting Apps: Apps like Mint and YNAB (You Need a Budget) help you track your income and expenses, providing a clear picture of your financial situation.

- Financial Advisors: Consider consulting a financial advisor for personalized advice tailored to your specific circumstances.

The Impact of Down Payment and Interest Rates

Your down payment and the interest rate on your car loan significantly impact your monthly payments. A larger down payment reduces the amount you need to borrow, leading to lower monthly payments. Similarly, a lower interest rate can save you thousands of dollars over the life of the loan.

- Down Payment Strategies: Aim for a down payment of at least 20% to reduce your loan amount and monthly payments.

- Credit Score Matters: A higher credit score qualifies you for lower interest rates, saving you money in the long run.

- Shop Around for Rates: Compare interest rates from multiple lenders to ensure you’re getting the best deal.

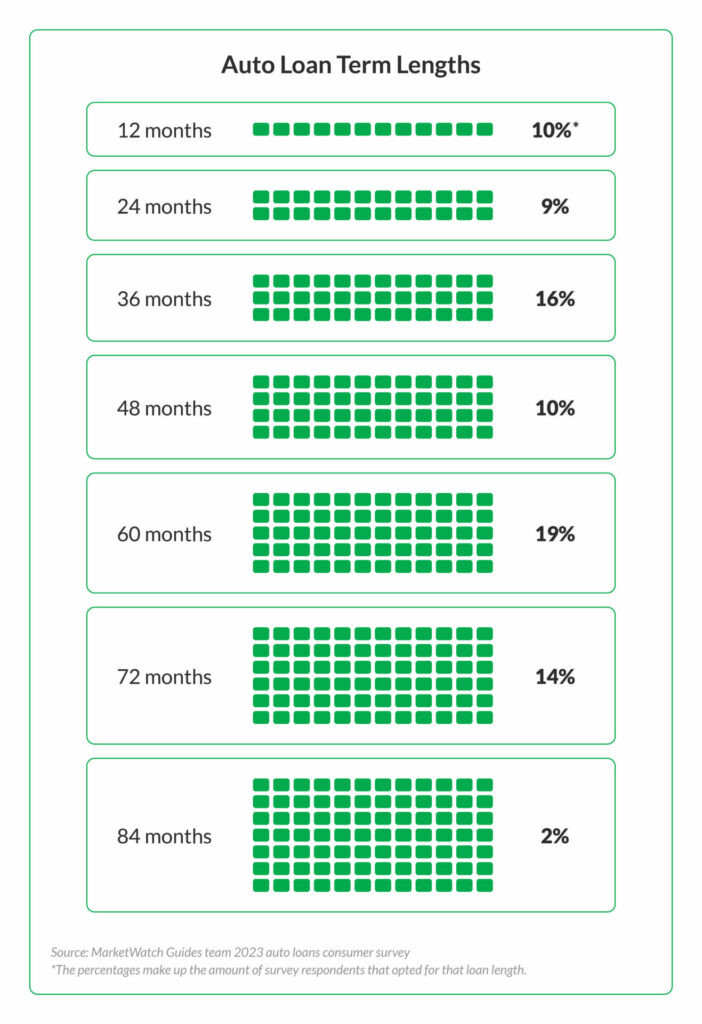

Calculation of Monthly Car Payment

Calculation of Monthly Car Payment

Alt Text: Illustration depicting auto loan term lengths and the distribution of choices among car owners in a 2023 survey, highlighting the popularity of a 60-month term.

3. Beyond the Payment: Hidden Costs of Car Ownership

It’s easy to focus solely on the monthly payment, but car ownership comes with a range of additional expenses that can quickly add up. Overlooking these costs can throw your budget off track and undermine your financial stability.

These hidden costs can significantly impact your budget and should be carefully considered when determining how much you can afford.

Fuel, Insurance, and Maintenance: The Big Three

- Fuel Costs: The price of gas can fluctuate significantly, impacting your monthly budget. Consider the fuel efficiency of the car you’re considering.

- Insurance Premiums: Car insurance rates vary based on your driving history, location, and the type of vehicle you own.

- Maintenance and Repairs: Regular maintenance, such as oil changes and tire rotations, is essential to keep your car running smoothly. Unexpected repairs can also be costly.

To illustrate, let’s consider a scenario: You budget $300 for a car payment, but forget to factor in gas ($150), insurance ($100), and maintenance ($50). Suddenly, your car costs you $600 a month, double your initial estimate.

Registration Fees, Taxes, and Other Incidentals

- Registration Fees: These are annual fees charged by your state to register your vehicle.

- Sales Tax: You’ll need to pay sales tax when you purchase the car.

- Property Taxes: Some states also charge annual property taxes on vehicles.

- Parking Fees: If you live in a city, parking fees can be a significant expense.

- Tolls: If you frequently drive on toll roads, factor these costs into your budget.

Strategies for Minimizing These Hidden Costs

- Choose Fuel-Efficient Vehicles: Opt for cars with good gas mileage to reduce your fuel costs.

- Shop Around for Insurance: Compare quotes from multiple insurance companies to find the best rates.

- Regular Maintenance: Keep your car well-maintained to prevent costly repairs.

- Consider Public Transportation: Use public transportation or carpool when possible to save on gas and parking fees.

- Negotiate Fees: Negotiate the purchase price and fees with the dealer to minimize your overall costs.

4. Leasing vs. Buying: Which is Right for You?

The decision to lease or buy a car has significant financial implications. Understanding the pros and cons of each option is crucial to making an informed decision that aligns with your financial goals.

Both leasing and buying have their advantages and disadvantages. The best choice depends on your individual circumstances, financial goals, and preferences.

The Pros and Cons of Leasing

Pros:

- Lower Monthly Payments: Lease payments are typically lower than loan payments because you’re only paying for the depreciation of the car during the lease term.

- Newer Car More Often: Leasing allows you to drive a new car every few years without the hassle of selling your old one.

- Warranty Coverage: Leased cars are usually covered by the manufacturer’s warranty, reducing the risk of unexpected repair costs.

Cons:

- Mileage Restrictions: Leases come with mileage limits, and you’ll be charged extra for exceeding them.

- No Ownership: You don’t own the car at the end of the lease term.

- Early Termination Fees: Ending a lease early can be expensive due to early termination fees.

- Wear and Tear Charges: You may be charged for excessive wear and tear on the car when you return it.

The Pros and Cons of Buying

Pros:

- Ownership: You own the car outright once you’ve paid off the loan.

- No Mileage Restrictions: You can drive as many miles as you want without incurring extra charges.

- Customization: You can customize the car to your liking without worrying about lease restrictions.

- Resale Value: You can sell the car later and recoup some of your investment.

Cons:

- Higher Monthly Payments: Loan payments are typically higher than lease payments.

- Depreciation: Cars depreciate over time, meaning their value decreases.

- Maintenance Costs: You’re responsible for all maintenance and repair costs once the warranty expires.

When Does Leasing Make Sense?

Leasing may be a good option if:

- You like driving a new car every few years.

- You drive fewer than the allotted miles per year.

- You don’t want to worry about maintenance and repair costs.

When Does Buying Make Sense?

Buying may be a better choice if:

- You want to own the car outright.

- You drive a lot of miles each year.

- You plan to keep the car for a long time.

- You like customizing your vehicle.

5. How to Negotiate the Best Car Deal

Negotiating a car deal can be intimidating, but with the right strategies, you can save thousands of dollars. The key is to be prepared, do your research, and be willing to walk away if you’re not getting a fair deal.

Negotiating effectively can significantly reduce the overall cost of your car, making it more affordable and freeing up funds for other investments.

Research, Research, Research

Before you even step into a dealership, do your homework. Know the market value of the car you’re interested in, as well as any incentives or rebates you may qualify for.

- Check Online Pricing: Use websites like Kelley Blue Book and Edmunds to research the market value of the car.

- Compare Prices: Get quotes from multiple dealerships to see who offers the best deal.

- Know Your Credit Score: Check your credit score to get an idea of the interest rates you qualify for.

Focus on the Out-the-Door Price

The “out-the-door” price is the total cost of the car, including taxes, fees, and any other charges. Focusing on this number ensures you’re not getting tricked by hidden fees.

- Ask for a Detailed Breakdown: Request a detailed breakdown of all costs included in the out-the-door price.

- Negotiate Each Item: Don’t be afraid to negotiate each item on the list, such as the vehicle price, fees, and trade-in value.

Don’t Be Afraid to Walk Away

One of the most powerful tools you have is the ability to walk away. If the dealer isn’t willing to meet your terms, be prepared to leave and take your business elsewhere.

- Set a Budget: Determine how much you’re willing to spend and stick to it.

- Be Patient: Don’t rush into a deal. Take your time and consider all your options.

- Shop Around: Visit multiple dealerships and compare offers before making a decision.

Leveraging income-partners.net for Financial Growth

While managing your car expenses wisely is crucial, don’t forget the importance of increasing your income to achieve financial freedom. This is where income-partners.net comes in. The platform offers a multitude of opportunities to connect with like-minded individuals, explore potential partnerships, and boost your earnings.

- Strategic Alliances: Finding the right partners can open doors to new markets, innovative ideas, and increased revenue streams.

- Diverse Opportunities: Whether you’re an entrepreneur, investor, or marketing expert, income-partners.net provides a diverse range of collaboration possibilities tailored to your skills and interests.

- Long-Term Growth: Building solid partnerships is not just about short-term gains; it’s about creating sustainable, long-term growth and financial stability.

By balancing smart budgeting with strategic partnership-building, you can achieve a level of financial success that goes beyond just making ends meet.

6. Real-Life Examples and Case Studies

To further illustrate the importance of staying within the 10-15% rule, let’s look at some real-life examples and case studies.

These examples highlight the impact of car payment decisions on overall financial health and the potential benefits of making smart choices.

Case Study 1: The Overextended Spender

John, a 30-year-old marketing manager, earned $6,000 per month after taxes. He loved cars and decided to lease a brand-new sports car with a monthly payment of $900, or 15% of his income. While he could technically afford the payment, he soon realized he was struggling to save for retirement or invest in other opportunities.

After a year, John felt stressed and financially constrained. He decided to downsize to a more affordable car with a payment of $400 per month. This freed up $500, which he invested in a promising partnership he found on income-partners.net. Within two years, his investment had doubled, significantly improving his financial situation.

Case Study 2: The Prudent Saver

Sarah, a 35-year-old entrepreneur, also earned $6,000 per month after taxes. She needed a reliable car for her business but was determined to stay within her budget. She purchased a used car for $15,000 with a down payment of $5,000. Her monthly payment was $200, or just over 3% of her income.

Sarah used the extra money to invest in her business and forge strategic alliances through income-partners.net. Her business thrived, and she was able to expand her operations and increase her income significantly.

Key Takeaways from These Examples

- Prioritize Financial Flexibility: Keeping your car payment low allows you to pursue other financial goals, such as investing and saving.

- Consider Long-Term Impact: Think about the long-term impact of your car payment on your overall financial health.

- Explore Alternative Options: Consider buying a used car or leasing a more affordable vehicle to save money.

- Invest in Income-Generating Opportunities: Use the money you save to invest in ventures that can increase your income, such as partnerships through income-partners.net.

7. Alternative Transportation Options

If you’re struggling to afford a car payment, consider alternative transportation options. These options can save you money and reduce your environmental impact.

Exploring these alternatives can significantly reduce your transportation costs and improve your financial well-being.

Public Transportation: Buses, Trains, and Subways

Public transportation is often the most affordable option, especially in urban areas. Many cities offer monthly passes that can save you even more money.

- Cost-Effective: Public transportation is typically cheaper than owning a car, especially when you factor in gas, insurance, and maintenance costs.

- Convenient: Many cities have extensive public transportation networks that can get you where you need to go.

- Environmentally Friendly: Public transportation reduces your carbon footprint and helps alleviate traffic congestion.

Cycling: A Healthy and Affordable Option

If you live in a bike-friendly city, cycling can be a great way to get around. It’s also a great form of exercise.

- Low Cost: Bicycles are relatively inexpensive, and maintenance costs are minimal.

- Healthy: Cycling is a great way to stay active and improve your physical health.

- Environmentally Friendly: Bicycles produce zero emissions.

Walking: The Simplest Solution

Walking is the simplest and most affordable form of transportation. If you live close to your work or other destinations, walking can be a great option.

- Free: Walking costs nothing.

- Healthy: Walking is a great way to stay active and improve your physical health.

- Environmentally Friendly: Walking produces zero emissions.

Ride-Sharing Services: Uber and Lyft

Ride-sharing services like Uber and Lyft can be convenient alternatives to owning a car, especially for occasional trips.

- Convenient: Ride-sharing services are available in most cities and can be summoned with a smartphone app.

- Flexible: You can use ride-sharing services only when you need them, avoiding the fixed costs of car ownership.

8. The Role of Credit Score in Car Affordability

Your credit score plays a significant role in determining the interest rate you’ll receive on a car loan. A higher credit score can save you thousands of dollars over the life of the loan.

Improving your credit score can significantly reduce the cost of borrowing money for a car and make it more affordable.

Understanding Credit Scores

A credit score is a numerical representation of your creditworthiness. It’s based on your credit history, including your payment history, outstanding debt, and credit utilization.

- Payment History: This is the most important factor in your credit score. Paying your bills on time is crucial.

- Outstanding Debt: The amount of debt you owe also affects your credit score. Keeping your debt levels low is important.

- Credit Utilization: This is the amount of credit you’re using compared to your total available credit. Keeping your credit utilization below 30% is recommended.

How Credit Score Impacts Interest Rates

Lenders use your credit score to assess the risk of lending you money. A higher credit score indicates a lower risk, so lenders will offer you lower interest rates.

- Lower Interest Rates: A higher credit score can save you thousands of dollars over the life of the loan.

- Better Loan Terms: Lenders may also offer you better loan terms, such as a longer repayment period or a lower down payment.

Tips for Improving Your Credit Score

- Pay Your Bills on Time: Make all your payments on time, every time.

- Reduce Outstanding Debt: Pay down your outstanding debt as quickly as possible.

- Keep Credit Utilization Low: Keep your credit utilization below 30%.

- Check Your Credit Report Regularly: Check your credit report for errors and dispute any inaccuracies.

- Become an Authorized User: If you have a friend or family member with good credit, ask them to add you as an authorized user on their credit card.

9. Financial Planning Beyond Car Ownership

While managing your car expenses is important, it’s just one piece of the financial puzzle. Comprehensive financial planning involves setting goals, creating a budget, and investing for the future.

Integrating car affordability into your overall financial plan ensures you’re making smart decisions that support your long-term goals.

Setting Financial Goals

- Short-Term Goals: These are goals you want to achieve within the next year, such as paying off debt or saving for a vacation.

- Mid-Term Goals: These are goals you want to achieve within the next five years, such as buying a home or starting a business.

- Long-Term Goals: These are goals you want to achieve in the distant future, such as retirement or financial independence.

Creating a Budget

A budget is a plan for how you’ll spend your money. It helps you track your income and expenses and ensures you’re saving enough to reach your financial goals.

- Track Your Income and Expenses: Use a budgeting app or spreadsheet to track your income and expenses.

- Identify Areas to Cut Back: Look for areas where you can reduce your spending.

- Allocate Funds for Savings and Investments: Make sure you’re allocating enough money to savings and investments.

Investing for the Future

Investing is essential for building wealth and achieving financial independence. Consider investing in stocks, bonds, real estate, or other assets.

- Start Early: The earlier you start investing, the more time your money has to grow.

- Diversify Your Investments: Don’t put all your eggs in one basket. Diversify your investments to reduce risk.

- Seek Professional Advice: Consider consulting a financial advisor for personalized investment advice.

Exploring Partnership Opportunities on income-partners.net

In addition to managing expenses and saving wisely, consider exploring partnership opportunities on income-partners.net to accelerate your financial growth.

- Connect with Potential Partners: Use the platform to connect with like-minded individuals and explore potential partnerships.

- Evaluate Opportunities Carefully: Carefully evaluate each opportunity to ensure it aligns with your financial goals.

- Negotiate Favorable Terms: Negotiate favorable terms to maximize your potential returns.

10. Expert Advice and Resources

Navigating the world of car affordability and financial planning can be complex. Seeking advice from experts and utilizing available resources can help you make informed decisions.

Leveraging expert advice and resources can empower you to make smart financial decisions and achieve your goals.

Financial Advisors: Personalized Guidance

Financial advisors can provide personalized guidance tailored to your specific circumstances and financial goals.

- Investment Advice: Financial advisors can help you develop an investment strategy that aligns with your risk tolerance and financial goals.

- Retirement Planning: They can also help you plan for retirement and ensure you have enough money to live comfortably.

- Debt Management: Financial advisors can help you develop a debt management plan to pay off your debts as quickly as possible.

Online Resources: Websites and Tools

Numerous websites and online tools can help you with car affordability and financial planning.

- NerdWallet: Offers car affordability calculators, credit score information, and financial planning advice.

- Bankrate: Provides interest rate comparisons, loan calculators, and financial news.

- Kelley Blue Book: Offers car pricing information and vehicle reviews.

- Edmunds: Provides car reviews, pricing information, and car-buying advice.

Books and Podcasts: Educational Resources

Books and podcasts can provide valuable insights into car affordability and financial planning.

- “The Total Money Makeover” by Dave Ramsey: Offers a step-by-step guide to getting out of debt and building wealth.

- “The Intelligent Investor” by Benjamin Graham: Provides timeless investment advice.

- “The Dave Ramsey Show” Podcast: Offers practical advice on money management and debt reduction.

Address: 1 University Station, Austin, TX 78712, United States

Phone: +1 (512) 471-3434

Website: income-partners.net

By leveraging these resources and seeking expert advice, you can make informed decisions about car affordability and financial planning, setting yourself up for long-term financial success. And remember, income-partners.net is here to help you connect with the right partners to boost your income and achieve your financial goals.

In conclusion, determining what percent of your income should a car payment be is a critical aspect of financial planning. Sticking to the recommended 10-15% guideline ensures financial stability, investment opportunities, and reduced stress. By carefully calculating your affordable payment, considering hidden costs, and exploring alternative transportation options, you can make informed decisions that align with your long-term financial goals. And don’t forget, income-partners.net offers valuable resources and partnership opportunities to help you increase your income and achieve financial independence. Visit income-partners.net today to explore potential collaborations, build strategic alliances, and take your financial success to the next level. Unlock your potential, connect with experts, and discover opportunities for business partnerships, wealth-building strategies, and increased income streams.

FAQ Section

Here are some frequently asked questions about car affordability:

1. What is the ideal percentage of my income that should go towards a car payment?

Ideally, your car payment should not exceed 10-15% of your monthly take-home pay to ensure financial stability and flexibility.

2. What factors should I consider when calculating my affordable car payment?

Consider your monthly take-home pay, all monthly expenses, down payment amount, and interest rates.

3. Are there any hidden costs of car ownership that I should be aware of?

Yes, hidden costs include fuel, insurance, maintenance, registration fees, and taxes.

4. Is it better to lease or buy a car?

It depends on your individual circumstances. Leasing offers lower monthly payments and newer cars more often, while buying allows for ownership and no mileage restrictions.

5. How can I negotiate the best car deal?

Research the market value of the car, focus on the out-the-door price, and be willing to walk away if you’re not getting a fair deal.

6. What role does my credit score play in car affordability?

A higher credit score qualifies you for lower interest rates, saving you money over the life of the loan.

7. What are some alternative transportation options to consider?

Consider public transportation, cycling, walking, and ride-sharing services like Uber and Lyft.

8. How can I improve my credit score?

Pay your bills on time, reduce outstanding debt, keep credit utilization low, and check your credit report regularly.

9. Why is financial planning important beyond car ownership?

Comprehensive financial planning helps you set goals, create a budget, and invest for the future, ensuring long-term financial success.

10. How can income-partners.net help me improve my financial situation?

income-partners.net provides opportunities to connect with potential partners, explore strategic alliances, and increase your income streams.