What Percent Of My Income Should Go To Car Payment? Generally, your car payment should ideally be no more than 10-15% of your monthly take-home pay, according to financial experts at income-partners.net. This range allows you to comfortably afford your vehicle without sacrificing other financial goals. This guide will give you actionable strategies to optimize your car expenses, explore partnership opportunities for additional income, and make financially sound decisions that align with your long-term prosperity.

Keep reading to discover strategies for smart budgeting, potential collaborations, and ways to boost your financial well-being. Discover how income diversification can ease financial strain.

1. Understanding the Golden Ratio: Car Payment vs. Income

Deciding what portion of your income should be allocated to car payments is a crucial financial decision. It’s not just about affordability but about maintaining a balanced financial life. Here’s how to determine the ideal percentage and why it matters.

1.1 The 10-15% Rule Explained

The 10-15% rule suggests that your total car expenses, including the car payment, insurance, and fuel, should not exceed 10-15% of your monthly net income.

- Example: If your monthly take-home pay is $4,000, your total car expenses should ideally stay within $400 to $600.

This guideline ensures that you have enough funds for other essential expenses like housing, food, utilities, and savings. According to a study by the University of Texas at Austin’s McCombs School of Business, individuals who adhere to this guideline report lower financial stress and higher savings rates.

1.2 Why This Percentage Matters

Sticking to this percentage helps in several ways:

- Financial Stability: It prevents you from overextending your budget, reducing the risk of debt.

- Savings and Investments: It allows you to allocate a significant portion of your income towards savings, investments, and emergency funds.

- Flexibility: It provides financial flexibility to handle unexpected expenses or changes in income.

1.3 Breaking Down Car-Related Expenses

When calculating the percentage of income for car payments, it’s important to include all related costs:

- Car Payment: The monthly amount you pay towards the loan.

- Insurance: The cost of your auto insurance policy.

- Fuel: The amount you spend on gasoline or electricity.

- Maintenance: Costs for regular servicing, oil changes, and tire rotations.

- Repairs: Unforeseen costs for fixing mechanical issues.

- Registration and Taxes: Annual fees for vehicle registration and property taxes.

1.4 Real-World Scenario

Consider a scenario where two individuals, Alex and Ben, each earn $5,000 per month after taxes.

- Alex spends 25% of his income ($1,250) on his car payment, insurance, and fuel.

- Ben spends 12% of his income ($600) on the same.

While Alex enjoys a more luxurious vehicle, he finds it challenging to save for retirement or handle unexpected expenses. Ben, on the other hand, has a comfortable savings buffer and can invest more aggressively.

1.5 Balancing Lifestyle and Affordability

Choosing a car is a personal decision that should align with your lifestyle and financial goals. Here’s how to strike a balance:

- Assess Your Needs: Determine whether you need a car for commuting, family, or recreational purposes.

- Consider Alternatives: Explore options like public transportation, carpooling, or biking if feasible.

- Set a Realistic Budget: Use the 10-15% rule to set a budget for car expenses.

- Shop Around: Compare prices, loan rates, and insurance quotes to find the best deals.

Person performing a car payment budget calculation

Person performing a car payment budget calculation

1.6 The Role of Down Payments

A significant down payment can substantially reduce your monthly car payments. Aim for at least 20% of the car’s purchase price to lower your loan amount and potentially secure a better interest rate. This approach aligns with advice from financial advisors who advocate for minimizing debt and maximizing equity.

1.7 Leasing vs. Buying

Deciding whether to lease or buy a car can impact your monthly expenses. Leasing typically involves lower monthly payments but doesn’t build equity. Buying, on the other hand, builds equity but may involve higher monthly payments and long-term costs.

1.8 Expert Insight

According to a report by Entrepreneur.com, “The key to financial success is aligning your expenses with your income.” This means understanding your income streams, setting clear financial goals, and making informed decisions about large purchases like cars.

1.9 Income-Partners.Net: Your Financial Ally

At income-partners.net, we understand the challenges of balancing financial responsibilities with lifestyle choices. We offer resources and partnership opportunities to help you increase your income and achieve financial stability. Whether you’re seeking strategic alliances or business ventures, our platform is designed to support your financial growth.

1.10 Making Informed Decisions

Deciding what percentage of your income should go to car payments requires careful consideration and planning. By following the 10-15% rule, understanding your expenses, and balancing lifestyle with affordability, you can make informed decisions that support your financial well-being.

2. Calculating Your Monthly Car Payment Potential

Determining how much you can afford for a car payment involves a detailed assessment of your income, expenses, and financial goals. Here’s a step-by-step guide to calculating your monthly car payment potential.

2.1 Gathering Financial Information

Start by collecting all necessary financial documents:

- Pay Stubs: To determine your post-tax take-home pay.

- Bank Statements: To track your monthly expenses.

- Credit Report: To understand your credit score and borrowing potential.

- Expense Records: Including bills, subscriptions, and other recurring costs.

2.2 Calculating Net Income

Your net income, or take-home pay, is the amount you receive after taxes and other deductions. This is the most accurate figure to use when calculating your car payment potential.

- Formula: Gross Income – Taxes – Deductions = Net Income

2.3 Listing Monthly Expenses

Create a comprehensive list of all your monthly expenses:

- Housing: Rent or mortgage payments.

- Utilities: Electricity, water, gas, and internet.

- Food: Groceries and dining out.

- Transportation: Public transportation costs or current car expenses.

- Insurance: Health, life, and other insurance premiums.

- Debt Payments: Credit cards, student loans, and other loans.

- Savings: Contributions to savings accounts or investment funds.

- Miscellaneous: Entertainment, personal care, and other discretionary spending.

2.4 Determining Disposable Income

Disposable income is the amount left after deducting all monthly expenses from your net income. This figure represents the funds available for discretionary spending, including car payments.

- Formula: Net Income – Monthly Expenses = Disposable Income

2.5 Applying the 10-15% Rule

Using the 10-15% rule, calculate the maximum amount you should allocate to car expenses:

- Lower Limit: Disposable Income x 0.10

- Upper Limit: Disposable Income x 0.15

2.6 Example Calculation

Let’s say your net income is $5,000 per month, and your monthly expenses total $3,000.

- Disposable Income: $5,000 – $3,000 = $2,000

- Lower Limit: $2,000 x 0.10 = $200

- Upper Limit: $2,000 x 0.15 = $300

Based on this calculation, your monthly car expenses should ideally stay between $200 and $300.

2.7 Considering Additional Costs

Remember to factor in additional car-related costs when determining your monthly payment:

- Insurance: Get quotes for auto insurance to estimate your monthly premiums.

- Fuel: Calculate your average monthly fuel costs based on your driving habits.

- Maintenance: Set aside funds for routine maintenance and potential repairs.

2.8 Using Online Calculators

Utilize online car affordability calculators to refine your estimates. These tools typically consider factors like loan term, interest rate, and down payment to provide a more accurate assessment of your monthly payments.

2.9 MarketWatch Guidance: Factors To Consider

As MarketWatch wisely advises, it’s crucial to not max out your budget. Financial strain can be mitigated by keeping anticipated monthly car payments within a reasonable range, ensuring there’s room for extra expenses.

2.10 Loan Terms and Interest Rates

The length of your loan term and the interest rate significantly impact your monthly payments. Longer loan terms result in lower monthly payments but higher overall costs due to accumulated interest. Shorter loan terms result in higher monthly payments but lower overall costs.

2.11 Credit Score Impact

Your credit score plays a vital role in determining the interest rate you’ll receive on your car loan. A higher credit score typically translates to lower interest rates, saving you money over the life of the loan.

2.12 Upside-Down Loans

Be cautious of longer loan terms that increase the risk of going upside-down on your loan. This occurs when you owe more on the loan than the car is worth, which can be problematic if you need to sell the car.

2.13 Income-Partners.Net: Boosting Your Income

If you find that your current income limits your car-buying options, consider exploring partnership opportunities with income-partners.net. By collaborating with strategic partners, you can increase your income and expand your financial capabilities.

2.14 Expert Insight

According to Harvard Business Review, “Strategic partnerships can drive revenue growth and increase market share.” By leveraging the expertise and resources of partners, you can unlock new income streams and achieve financial success.

2.15 Making Informed Decisions

Calculating your monthly car payment potential requires careful consideration of your income, expenses, and financial goals. By following these steps, you can make informed decisions that align with your financial well-being.

3. The Impact of Fuel and Insurance Costs

When budgeting for a car, it’s essential to consider fuel and insurance costs. These expenses can significantly impact your overall affordability. Here’s how to estimate these costs and incorporate them into your budget.

3.1 Estimating Fuel Costs

Fuel costs depend on factors such as your vehicle’s fuel efficiency, driving habits, and local gas prices.

- Vehicle Fuel Efficiency: Check the EPA fuel economy ratings for your desired vehicle.

- Driving Habits: Estimate your average monthly mileage.

- Gas Prices: Monitor local gas prices and factor in fluctuations.

3.2 Calculating Monthly Fuel Costs

Use the following formula to estimate your monthly fuel costs:

- (Monthly Mileage / Fuel Efficiency) x Gas Price = Monthly Fuel Cost

For example, if you drive 1,000 miles per month in a car that gets 25 miles per gallon, and the average gas price is $3.50 per gallon:

- (1,000 / 25) x $3.50 = $140

Your estimated monthly fuel cost would be $140.

3.3 Reducing Fuel Costs

Consider these strategies to reduce your fuel costs:

- Choose Fuel-Efficient Vehicles: Opt for cars with high fuel economy ratings.

- Maintain Your Vehicle: Regular maintenance improves fuel efficiency.

- Drive Efficiently: Avoid aggressive acceleration and braking.

- Carpool or Use Public Transportation: Reduce your reliance on your car.

3.4 Estimating Insurance Costs

Insurance costs vary based on factors such as your age, driving record, location, and vehicle type.

- Age and Driving Record: Younger drivers and those with accidents typically pay higher premiums.

- Location: Urban areas often have higher insurance rates due to increased risk.

- Vehicle Type: Expensive or high-performance cars usually cost more to insure.

3.5 Obtaining Insurance Quotes

Shop around and compare quotes from multiple insurance companies to find the best rates. Online comparison tools can help streamline this process.

3.6 Factors Affecting Insurance Premiums

Several factors can influence your insurance premiums:

- Coverage Level: Higher coverage levels result in higher premiums.

- Deductible: Choosing a higher deductible can lower your premiums.

- Discounts: Inquire about discounts for safe driving, bundling policies, or being a student.

3.7 Incorporating Fuel and Insurance into Your Budget

Add your estimated fuel and insurance costs to your monthly car payment to determine the total cost of owning a vehicle.

- Total Monthly Car Expenses = Car Payment + Fuel Costs + Insurance Costs

3.8 Real-World Example

Suppose your car payment is $300, your estimated fuel costs are $140, and your insurance premium is $100.

- Total Monthly Car Expenses = $300 + $140 + $100 = $540

Ensure that this total aligns with the 10-15% rule for your monthly net income.

3.9 MarketWatch Insight

MarketWatch suggests that when calculating your monthly car payment and related expenses, try to keep your total costs to less than 20% of your monthly take-home pay.

3.10 Income-Partners.Net: Financial Strategies

At income-partners.net, we provide financial strategies and partnership opportunities to help you manage and reduce your car-related expenses. By increasing your income, you can more comfortably afford your vehicle and other financial obligations.

3.11 Expert Insight

According to a study by the U.S. Department of Energy, choosing a fuel-efficient vehicle can save you thousands of dollars in fuel costs over the life of the car.

3.12 Making Informed Decisions

Estimating and managing fuel and insurance costs are crucial steps in budgeting for a car. By carefully considering these expenses and implementing strategies to reduce them, you can make informed decisions that support your financial well-being.

4. Understanding Loan Amounts and Terms

The amount you can borrow for a car loan and the terms of that loan significantly impact your monthly payments and overall costs. Here’s what you need to know about loan amounts and terms to make informed decisions.

4.1 Factors Affecting Loan Amounts

Several factors determine how much a lender is willing to lend you:

- Credit Score: A higher credit score typically results in a larger loan amount and better interest rates.

- Income: Lenders assess your income to ensure you can afford the monthly payments.

- Debt-to-Income Ratio (DTI): Lenders evaluate your DTI to determine your ability to manage additional debt.

- Down Payment: A larger down payment reduces the loan amount needed.

- Vehicle Type: New cars often qualify for larger loan amounts than used cars.

4.2 Impact of Credit Score

Your credit score is a critical factor in securing a car loan. Lenders use your credit score to assess your creditworthiness and determine the interest rate you’ll receive.

- Excellent Credit (750+): Qualifies for the lowest interest rates and largest loan amounts.

- Good Credit (700-749): Qualifies for favorable interest rates and loan terms.

- Fair Credit (650-699): May receive higher interest rates and stricter loan terms.

- Poor Credit (Below 650): May struggle to get approved or face very high interest rates.

4.3 Loan Terms Explained

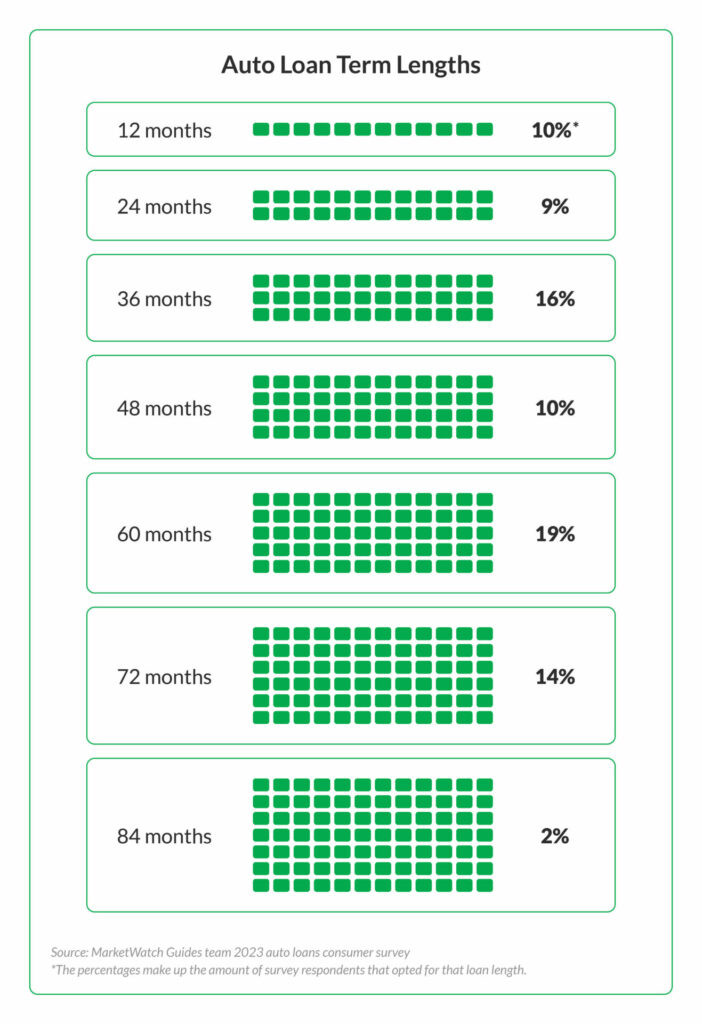

The loan term is the length of time you have to repay the loan. Common loan terms range from 24 to 72 months.

- Shorter Loan Terms (24-36 months): Higher monthly payments but lower overall interest costs.

- Longer Loan Terms (60-72 months): Lower monthly payments but higher overall interest costs.

4.4 Calculating Total Interest Paid

Use the following formula to estimate the total interest you’ll pay over the life of the loan:

- Total Interest = (Monthly Payment x Loan Term) – Loan Amount

For example, if you borrow $20,000 with a 60-month loan at a monthly payment of $400:

- Total Interest = ($400 x 60) – $20,000 = $4,000

You would pay $4,000 in interest over the life of the loan.

4.5 Choosing the Right Loan Term

Consider these factors when selecting a loan term:

- Budget: Determine how much you can comfortably afford each month.

- Interest Costs: Evaluate the total interest you’ll pay over the loan term.

- Vehicle Depreciation: Avoid longer loan terms that can lead to owing more than the car is worth.

4.6 Down Payments and Trade-Ins

Making a down payment or trading in your old car can reduce the loan amount needed, lowering your monthly payments and overall interest costs.

- Down Payment: Aim for at least 20% of the car’s purchase price.

- Trade-In Value: Research the value of your current car to negotiate a fair trade-in price.

4.7 Real-World Example

Consider two scenarios for a $25,000 car loan:

- Scenario 1: 36-Month Loan at 5% Interest

- Monthly Payment: $746.23

- Total Interest Paid: $1,864.28

- Scenario 2: 60-Month Loan at 5% Interest

- Monthly Payment: $471.77

- Total Interest Paid: $3,306.19

While the 60-month loan has lower monthly payments, it results in significantly higher interest costs.

4.8 Expert Insight

Nineteen percent of respondents in a 2023 consumer survey chose a 60-month loan term, making it the most popular choice, yet understanding the implications of this decision is crucial for financial health.

4.9 Income-Partners.Net: Enhancing Financial Capacity

At income-partners.net, we offer resources and partnership opportunities to help you improve your financial capacity and secure favorable loan terms. By increasing your income, you can qualify for better interest rates and manage your car payments more comfortably.

4.10 Harvard Business Review Insight

Harvard Business Review emphasizes the importance of understanding the financial implications of loan terms and interest rates when making purchasing decisions.

4.11 Making Informed Decisions

Understanding loan amounts and terms is crucial for making informed decisions about financing a car. By carefully considering these factors, you can choose a loan that aligns with your budget and financial goals.

5. Setting the Right Purchase Price

The purchase price of a car is a key factor in determining your monthly payments and overall affordability. Here’s how to set the right purchase price and negotiate a fair deal.

5.1 Researching Vehicle Prices

Start by researching the market value of the car you want to buy. Online resources like Kelley Blue Book and Edmunds can provide pricing data for new and used vehicles.

- New Cars: Check the manufacturer’s suggested retail price (MSRP) and look for incentives or rebates.

- Used Cars: Research the average selling price based on the car’s condition, mileage, and location.

5.2 Considering Additional Costs

Remember to factor in additional costs beyond the sticker price:

- Sales Tax: Varies by state and can add a significant amount to the purchase price.

- Registration Fees: Annual fees for registering your vehicle.

- Documentation Fees: Fees charged by the dealership for processing paperwork.

5.3 Calculating Total Purchase Price

Use the following formula to estimate the total purchase price:

- Total Purchase Price = Vehicle Price + Sales Tax + Registration Fees + Documentation Fees

5.4 Negotiating the Price

Negotiate the purchase price with the dealership to get the best possible deal. Be prepared to walk away if they don’t meet your budget.

- Do Your Homework: Research the car’s market value and come prepared with pricing data.

- Shop Around: Get quotes from multiple dealerships to compare prices.

- Be Assertive: Don’t be afraid to make a counteroffer and negotiate the price.

5.5 Factors Affecting Negotiation

Several factors can influence your ability to negotiate:

- Demand: High-demand vehicles may be harder to negotiate.

- Time of Year: Dealerships may be more willing to negotiate at the end of the month or year.

- Incentives: Take advantage of manufacturer incentives and rebates.

5.6 Making a Down Payment

A down payment can reduce the loan amount needed, lowering your monthly payments and overall interest costs.

- Aim for at least 20% of the car’s purchase price.

5.7 Trading In Your Old Car

Trading in your old car can offset the purchase price of the new car. Research the value of your current car to negotiate a fair trade-in price.

5.8 Avoiding Add-Ons

Be cautious of add-ons and extras that dealerships may try to sell you, such as extended warranties or paint protection. These can significantly increase the purchase price.

5.9 Real-World Example

Suppose you’re buying a car with a sticker price of $25,000. Sales tax is 6%, registration fees are $200, and documentation fees are $300.

- Sales Tax: $25,000 x 0.06 = $1,500

- Total Purchase Price: $25,000 + $1,500 + $200 + $300 = $27,000

Negotiating the price down to $24,000 would save you $60 in sales tax and lower your overall costs.

5.10 Expert Insight

Edmunds.com advises that understanding all fees and taxes associated with buying a car is crucial for setting a realistic budget and negotiating a fair price.

5.11 Income-Partners.Net: Empowering Financial Growth

At income-partners.net, we provide resources and partnership opportunities to help you increase your income and manage your car-related expenses effectively. By enhancing your financial stability, you can make confident decisions when buying a car.

5.12 Entrepreneur.com Insight

Entrepreneur.com emphasizes the importance of financial literacy and strategic planning when making significant purchases like cars.

5.13 Making Informed Decisions

Setting the right purchase price is essential for ensuring your car is affordable. By researching prices, negotiating effectively, and considering all associated costs, you can make informed decisions that align with your financial goals.

6. Leveraging Car Affordability Calculators

Car affordability calculators are valuable tools for estimating your monthly payments and determining how much car you can afford. Here’s how to use these calculators effectively and understand their results.

6.1 Understanding Car Affordability Calculators

These calculators use factors such as your income, expenses, loan term, interest rate, and down payment to estimate your monthly payments and the total cost of the loan.

6.2 Key Inputs for Calculators

To get accurate results, you’ll need the following information:

- Income: Your monthly net income (take-home pay).

- Expenses: Your total monthly expenses, excluding car-related costs.

- Loan Amount: The amount you plan to borrow.

- Loan Term: The length of the loan in months.

- Interest Rate: The annual interest rate on the loan.

- Down Payment: The amount you’ll pay upfront.

- Sales Tax: The sales tax rate in your state.

- Trade-In Value: The value of your current car if you plan to trade it in.

6.3 Using Online Calculators

Numerous online car affordability calculators are available. Some popular options include those from MarketWatch, Edmunds, and Kelley Blue Book.

6.4 Interpreting Calculator Results

The calculator will provide an estimate of your monthly payments and the total cost of the loan, including interest.

- Monthly Payment: The amount you’ll pay each month to repay the loan.

- Total Interest Paid: The total amount of interest you’ll pay over the life of the loan.

- Total Cost: The total cost of the car, including the purchase price, taxes, fees, and interest.

6.5 Adjusting Inputs for Different Scenarios

Experiment with different inputs to see how they affect your monthly payments and overall costs. For example, try increasing your down payment or shortening the loan term.

6.6 Incorporating Additional Costs

Remember to factor in additional car-related costs that the calculator may not include, such as insurance, fuel, and maintenance.

6.7 Real-World Example

Suppose you use a car affordability calculator and enter the following information:

- Income: $5,000 per month

- Expenses: $3,000 per month

- Loan Amount: $20,000

- Loan Term: 60 months

- Interest Rate: 5%

The calculator estimates your monthly payment at $377.42 and the total interest paid at $2,645.20.

6.8 Expert Insight

MarketWatch’s auto loan calculator can help you determine the monthly payment and total cost of a car loan, using factors like loan term, down payment, and interest rate.

6.9 Income-Partners.Net: Supporting Financial Planning

At income-partners.net, we provide resources and partnership opportunities to help you enhance your financial planning and make informed decisions about car ownership. By increasing your income, you can manage your car payments more comfortably.

6.10 Harvard Business Review on Financial Tools

Harvard Business Review emphasizes the importance of using financial tools and calculators to make informed decisions about large purchases like cars.

6.11 Making Informed Decisions

Car affordability calculators are valuable tools for estimating your monthly payments and determining how much car you can afford. By using these calculators effectively and understanding their results, you can make informed decisions that align with your budget and financial goals.

7. Exploring Partnership Opportunities for Income Growth

One of the most effective ways to afford a car without straining your finances is to increase your income. Exploring partnership opportunities can provide additional income streams and enhance your financial stability.

7.1 Types of Partnership Opportunities

Several types of partnerships can boost your income:

- Strategic Alliances: Collaborating with businesses that complement your skills and resources.

- Joint Ventures: Partnering with another company to undertake a specific project.

- Affiliate Marketing: Promoting other companies’ products or services and earning a commission on sales.

- Referral Programs: Earning rewards for referring new customers to businesses.

7.2 Benefits of Partnerships

Partnerships offer numerous benefits:

- Increased Income: Additional income streams can help you afford car payments and other expenses.

- Expanded Reach: Access to new markets and customers through your partners.

- Shared Resources: Leveraging partners’ resources, expertise, and networks.

- Reduced Risk: Sharing the risks and costs associated with new ventures.

7.3 Finding Partnership Opportunities

Here are some strategies for finding partnership opportunities:

- Networking: Attend industry events, join professional organizations, and connect with potential partners online.

- Online Platforms: Use platforms like LinkedIn to identify businesses and individuals who align with your goals.

- Industry Research: Research companies in your industry that may be open to collaboration.

- Income-Partners.Net: Explore partnership opportunities on our platform, designed to connect you with strategic allies.

7.4 Building Successful Partnerships

Follow these steps to build successful partnerships:

- Define Your Goals: Clearly outline what you hope to achieve through the partnership.

- Identify Potential Partners: Look for businesses and individuals with complementary skills and resources.

- Establish Clear Agreements: Create written agreements that outline the terms of the partnership, including responsibilities, compensation, and duration.

- Communicate Effectively: Maintain open and transparent communication with your partners.

- Evaluate Results: Regularly assess the partnership’s performance and make adjustments as needed.

7.5 Real-World Example

Consider a marketing consultant who partners with a web development agency. The consultant provides marketing expertise, while the agency provides website design and development services. Together, they can offer comprehensive solutions to clients and increase their income.

7.6 Expert Insight

According to Harvard Business Review, strategic partnerships can drive revenue growth and increase market share by leveraging the expertise and resources of multiple organizations.

7.7 Income-Partners.Net: Your Partner in Growth

At income-partners.net, we are committed to helping you find and build successful partnerships. Our platform offers a range of resources and opportunities to connect you with strategic allies and boost your income.

7.8 Entrepreneur.com on Collaboration

Entrepreneur.com emphasizes the importance of collaboration and strategic alliances in today’s competitive business environment.

7.9 Making Informed Decisions

Exploring partnership opportunities is a strategic way to increase your income and afford your car payments more comfortably. By following these steps and leveraging resources like income-partners.net, you can build successful partnerships that drive financial growth.

8. Strategies for Smart Car Budgeting

Creating a smart car budget involves careful planning and mindful spending. Here are some strategies to help you manage your car expenses effectively and stay within your financial limits.

8.1 Setting Clear Financial Goals

Start by defining your financial goals. Do you want to save for retirement, pay off debt, or build an emergency fund? Understanding your goals will help you prioritize your spending and make informed decisions about car ownership.

8.2 Creating a Detailed Budget

Develop a detailed budget that outlines your income and expenses. Track your spending to identify areas where you can cut back and allocate more funds towards car payments.

8.3 Prioritizing Needs vs. Wants

Distinguish between your needs and wants when it comes to car ownership. Do you need a new car, or would a used car suffice? Can you live with a more affordable model instead of a luxury vehicle?

8.4 Reducing Car-Related Expenses

Implement strategies to reduce your car-related expenses:

- Shop Around for Insurance: Compare quotes from multiple insurance companies to find the best rates.

- Maintain Your Vehicle: Regular maintenance can prevent costly repairs and improve fuel efficiency.

- Drive Efficiently: Avoid aggressive acceleration and braking to save on fuel.

- Carpool or Use Public Transportation: Reduce your reliance on your car and save on fuel and maintenance costs.

8.5 Building an Emergency Fund

Create an emergency fund to cover unexpected car repairs or other financial emergencies. Aim to save at least three to six months’ worth of living expenses.

8.6 Avoiding Impulse Purchases

Resist the temptation to make impulse purchases when shopping for a car. Stick to your budget and prioritize your needs over your wants.

8.7 Paying Off Debt

Pay off high-interest debt, such as credit card balances, to free up more funds for car payments. Consider consolidating your debt or using a balance transfer card to lower your interest rates.

8.8 Real-World Example

Consider a family that wants to buy a new car but also wants to save for their children’s college education. They create a detailed budget, prioritize their needs, and find ways to reduce their car-related expenses. They also explore partnership opportunities to increase their income and achieve their financial goals.

8.9 Expert Insight

According to financial experts, creating a detailed budget and setting clear financial goals are essential steps for managing your finances effectively and achieving long-term financial success.

8.10 Income-Partners.Net: Empowering Financial Stability

At income-partners.net, we are dedicated to helping you achieve financial stability and manage your car expenses effectively. Our platform offers resources and partnership opportunities to support your financial growth and empower you to make informed decisions.

8.11 Harvard Business Review on Budgeting

Harvard Business Review emphasizes the importance of budgeting and financial planning for achieving financial success and managing expenses effectively.

8.12 Making Informed Decisions

Creating a smart car budget involves careful planning, mindful spending, and a commitment to achieving your financial goals. By implementing these strategies and leveraging resources like income-partners.net, you can manage your car expenses effectively and stay within your financial limits.

9. Maximizing Income Through Diversification

Diversifying your income streams is a powerful strategy for increasing your overall income and affording your car payments more comfortably. Here’s how to maximize your income through diversification.

9.1 Exploring Multiple Income Streams

Consider pursuing multiple income streams to enhance your financial stability:

- Freelancing: Offer your skills and services on a freelance basis.

- Consulting: Provide expert advice and guidance to businesses.

- Investing: Invest in stocks, bonds, real estate, or other assets.

- Rental Income: Rent out a spare room or property.

- Online Business: Start an online store or blog and generate income through sales or advertising.

9.2 Leveraging Your Skills and Talents

Identify your skills and talents and find ways to monetize them. Can you teach a class, write articles, or design websites?

9.3 Investing in Education and Training

Invest in education and training to enhance your skills and increase your earning potential. Take online courses, attend workshops, or pursue a degree in a high-demand field.

9.4 Building a Passive Income

Create passive income streams that generate revenue with minimal effort:

- Write and Sell an Ebook: Create and sell digital products online.

- Create and Sell Online Courses: Develop online courses and earn recurring revenue from enrollments.

- Affiliate Marketing: Promote other companies’ products and earn commissions on sales.

9.5 Real-World Example

Consider an individual who works a full-time job but also earns income through freelancing, investing, and renting out a spare room. By diversifying their income streams, they can afford their car payments more comfortably and achieve their financial goals.

9.6 Expert Insight

According to financial experts, diversifying your income streams is a key strategy for building wealth and achieving financial security.

9.7 Income-Partners.Net: Connecting You With Opportunities

At income-partners.net, we provide resources and partnership opportunities to help you diversify your income streams and enhance your financial stability. Our platform connects you with strategic allies and provides the support you need to succeed.

9.8 Entrepreneur.com on Income Diversification

Entrepreneur.com emphasizes the importance of income diversification for managing risk and achieving long-term financial success.

9.9 Making Informed Decisions

Maximizing your income through diversification is a strategic way to afford your car payments and achieve your financial goals. By exploring multiple income streams, leveraging your skills and talents, and building passive income, you can enhance your financial stability and enjoy a more secure financial future.

10. Financial Tools and Resources

Leveraging financial tools and resources can greatly assist in making informed decisions about car payments and overall financial health.

10.1 Online Budgeting Tools

Utilize online budgeting tools like Mint, YNAB (You Need A Budget), or Personal Capital to track income, expenses, and savings goals.

10.2 Car Affordability Calculators

Use online car affordability calculators to estimate monthly payments based on loan amounts, interest rates, and loan terms.

10.3 Credit Score Monitoring Services

Monitor your credit score regularly using services like Credit Karma or Experian to identify potential issues and improve your creditworthiness.

10.4 Financial Advisory Services

Consider consulting with a financial