What Percent Of Income Should Be Car Payment? Ideally, your car payment should be no more than 10-15% of your monthly net income, according to financial experts at income-partners.net, ensuring it doesn’t strain your budget and allows for other financial goals. This guide provides a comprehensive approach to determining a sustainable car payment and maximizing your income potential through strategic partnerships.

1. Understanding the Golden Rule: The 10-15% Guideline

What percentage of your monthly income should you allocate to your car payment? A common rule of thumb suggests that your car payment should not exceed 10-15% of your monthly net income. But why this range?

The 10-15% guideline is rooted in sound financial planning principles. According to a study by the University of Texas at Austin’s McCombs School of Business, individuals who maintain their car payments within this range are more likely to achieve their long-term financial goals, such as saving for retirement or investing in income-generating assets.

Breaking Down the Rationale

- Financial Stability: Keeping your car payment within 10-15% of your net income ensures you have enough funds for other essential expenses, such as housing, utilities, food, and healthcare.

- Savings and Investments: A lower car payment frees up more money for savings and investments. This is crucial for building wealth and achieving financial independence.

- Unexpected Expenses: Life is full of surprises. A manageable car payment provides a buffer to handle unexpected expenses, such as medical bills or home repairs, without derailing your financial plan.

- Debt Management: Overextending yourself with a high car payment can lead to debt accumulation, which can be difficult to overcome. Sticking to the 10-15% guideline helps you avoid this pitfall.

Example Scenario

Let’s say your monthly net income is $5,000. According to the 10-15% rule, your car payment should ideally be between $500 and $750. This range allows you to comfortably afford your car while still having ample funds for other financial obligations and goals.

Example scenario with monthly net income and car payment range

Example scenario with monthly net income and car payment range

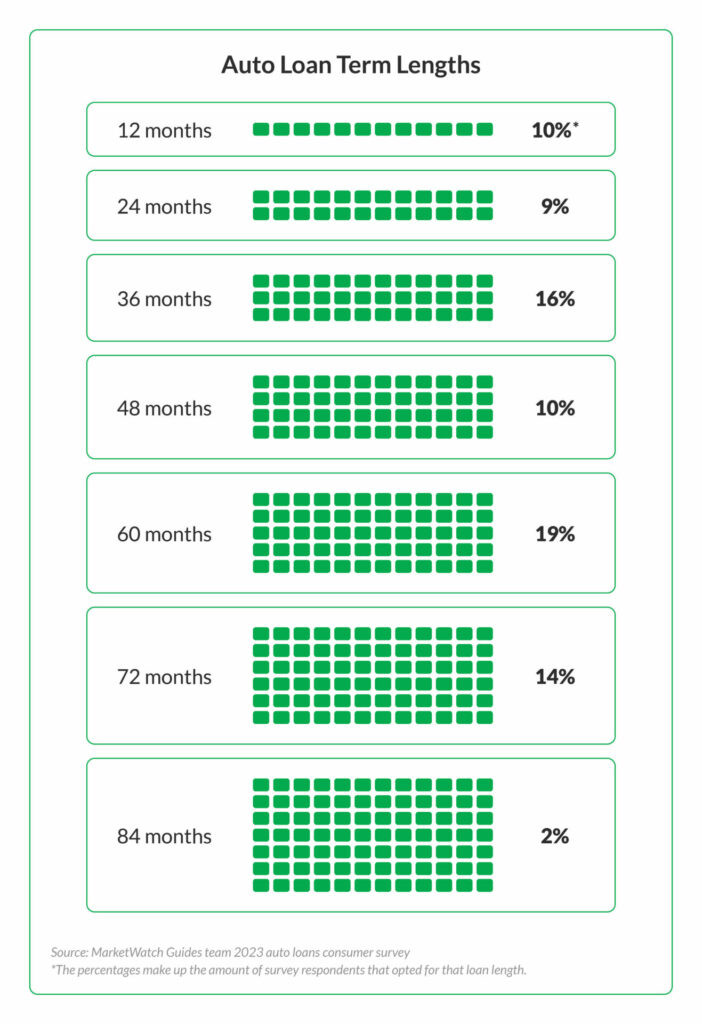

Alt text: Illustration showing auto term lengths and percentages of car owners from a 2023 survey.

2. The Comprehensive Approach: Beyond the Car Payment

While the 10-15% rule is a great starting point, it’s crucial to consider the total cost of car ownership when determining affordability. This includes not only the monthly payment but also expenses like insurance, fuel, maintenance, and repairs. Financial advisors at income-partners.net emphasize that a holistic view is essential for making informed decisions.

Identifying All Car-Related Expenses

- Car Payment: The principal and interest you pay each month on your auto loan or lease.

- Insurance: The cost of your auto insurance policy, which can vary depending on your coverage level, driving history, and location.

- Fuel: The amount you spend on gasoline or electricity to power your vehicle. This depends on your driving habits and the fuel efficiency of your car.

- Maintenance: Routine maintenance tasks such as oil changes, tire rotations, and filter replacements.

- Repairs: Unexpected repairs that may arise due to mechanical issues or accidents.

- Registration and Taxes: Annual registration fees and taxes associated with owning a vehicle.

Calculating the Total Cost of Ownership

To get an accurate picture of your car’s affordability, calculate the total cost of ownership by adding up all car-related expenses. For example, let’s say your monthly car payment is $500, your insurance costs $150, you spend $200 on fuel, and you budget $100 for maintenance and repairs. Your total monthly cost of car ownership would be $950.

The 20% Rule: A Safety Net

Many financial experts recommend that the total cost of car ownership should not exceed 20% of your monthly net income. This ensures you have enough room in your budget for other financial priorities and unexpected expenses.

3. Income Optimization: Strategies for Affording Your Dream Car

What can you do if your desired car payment exceeds the recommended guidelines? Instead of settling for a less desirable vehicle, consider optimizing your income through strategic partnerships. income-partners.net specializes in connecting individuals with opportunities to increase their income and achieve their financial goals.

Exploring Partnership Opportunities

- Strategic Alliances: Partner with complementary businesses to cross-promote products or services and generate new revenue streams.

- Joint Ventures: Collaborate with other entrepreneurs or companies on specific projects or ventures, sharing resources and profits.

- Affiliate Marketing: Promote other companies’ products or services on your website or social media channels and earn a commission for each sale or lead generated.

- Referral Programs: Partner with businesses that offer referral fees for new customers or clients you bring in.

- Freelance or Consulting Work: Leverage your skills and expertise to provide freelance or consulting services to businesses in need of specialized support.

Income-Partners.Net: Your Gateway to Financial Success

income-partners.net provides a comprehensive platform for individuals seeking to explore partnership opportunities and increase their income. The website offers a variety of resources, including:

- Partner Directory: A searchable database of potential partners across various industries.

- Partnership Guides: Expert advice and tips on how to identify, evaluate, and establish successful partnerships.

- Networking Events: Opportunities to connect with other entrepreneurs and business professionals in your area.

- Financial Planning Tools: Calculators and resources to help you manage your finances and track your progress towards your financial goals.

Address: 1 University Station, Austin, TX 78712, United States

Phone: +1 (512) 471-3434

Website: income-partners.net.

By leveraging the resources available at income-partners.net, you can increase your income and afford your dream car without sacrificing your financial stability.

4. The Impact of Loan Terms and Interest Rates

How do loan terms and interest rates affect your car payment? The length of your loan term and the interest rate you pay can significantly impact your monthly payment and the total cost of your car.

Loan Term: Short vs. Long

- Short-Term Loans: Offer lower interest rates and allow you to pay off your car faster, saving you money in the long run. However, they also come with higher monthly payments.

- Long-Term Loans: Provide lower monthly payments, making them more affordable in the short term. However, you’ll pay more interest over the life of the loan, increasing the total cost of your car.

Interest Rates: The APR Factor

The annual percentage rate (APR) is the interest rate you pay on your car loan, plus any fees or charges. A lower APR can save you thousands of dollars over the life of the loan.

Navigating the Trade-offs

When choosing a loan term and interest rate, it’s important to consider your individual financial situation and goals. If you can afford higher monthly payments, a short-term loan with a low APR is the best option. If you need lower monthly payments, a long-term loan may be more suitable, but be prepared to pay more interest over time.

Example scenario with monthly net income and car payment range

Alt text: The graph shows the relationship between auto loan term lengths and the percentage of car owners choosing them, based on a 2023 survey.

5. Leasing vs. Buying: Which is Right for You?

Should you lease or buy a car? Leasing and buying are two different ways to acquire a vehicle, each with its own advantages and disadvantages.

Leasing: Short-Term Affordability

Leasing involves renting a car for a fixed period, typically two to three years. Lease payments are generally lower than loan payments because you’re only paying for the depreciation of the car during the lease term.

Buying: Long-Term Ownership

Buying involves taking out a loan to purchase a car. Once you’ve paid off the loan, you own the car outright.

Making the Decision

The decision to lease or buy depends on your individual needs and preferences. Leasing is a good option if you want to drive a new car every few years and don’t mind making monthly payments indefinitely. Buying is a better choice if you want to own your car outright and keep it for a long time.

6. Down Payment Strategies: Reducing Your Loan Amount

How does a down payment impact your car payment? Making a down payment on your car can significantly reduce your loan amount and monthly payment.

The Benefits of a Down Payment

- Lower Monthly Payments: A larger down payment means you need to borrow less money, resulting in lower monthly payments.

- Reduced Interest Costs: A smaller loan amount means you’ll pay less interest over the life of the loan.

- Improved Loan Approval Odds: A down payment can increase your chances of getting approved for a car loan, especially if you have a less-than-perfect credit score.

How Much Should You Put Down?

As a general rule, aim to put down at least 20% of the car’s purchase price. This can significantly reduce your loan amount and monthly payment.

7. Credit Score Matters: Securing the Best Rates

Why is your credit score important when buying a car? Your credit score is a major factor in determining the interest rate you’ll pay on your car loan.

Credit Score Tiers

- Excellent Credit (750+): You’ll qualify for the lowest interest rates.

- Good Credit (700-749): You’ll still get competitive interest rates.

- Fair Credit (650-699): Your interest rates will be higher, but you can still get approved for a loan.

- Poor Credit (Below 650): You’ll likely pay very high interest rates, or you may have difficulty getting approved for a loan.

Improving Your Credit Score

If you have a low credit score, take steps to improve it before applying for a car loan. This may involve paying your bills on time, reducing your credit card balances, and disputing any errors on your credit report.

8. Negotiation Tactics: Getting the Best Deal

How can you negotiate the best price on a car? Negotiating the price of a car is an essential part of the car-buying process. With the right tactics, you can save thousands of dollars.

Research and Preparation

- Know the Market Value: Research the market value of the car you want to buy. Websites like Kelley Blue Book and Edmunds can provide valuable information.

- Get Pre-Approved for a Loan: Getting pre-approved for a car loan gives you leverage in negotiations. You’ll know exactly how much you can afford and what interest rate you qualify for.

- Shop Around: Don’t settle for the first offer you receive. Shop around at multiple dealerships to compare prices and find the best deal.

Negotiation Strategies

- Start Low: Make an initial offer that’s lower than what you’re willing to pay.

- Focus on the Out-the-Door Price: Pay attention to the total out-the-door price, including taxes, fees, and other charges.

- Be Willing to Walk Away: If the dealer isn’t willing to meet your price, be prepared to walk away. They may be more willing to negotiate if they think they’re going to lose a sale.

9. Fuel Efficiency: Saving Money at the Pump

What role does fuel efficiency play in car affordability? Fuel efficiency is an important factor to consider when buying a car. A fuel-efficient vehicle can save you a significant amount of money on gasoline over the life of the car.

Comparing Fuel Efficiency

The U.S. Department of Energy provides a detailed list of fuel economy figures as well as a comparison tool that allows you to check different vehicles’ annual fuel cost estimates.

Fuel-Efficient Options

Consider fuel-efficient options such as hybrid cars, electric vehicles, and small cars. These vehicles can significantly reduce your fuel costs.

10. Insurance Costs: Shopping for the Best Rates

How can you save money on car insurance? Car insurance is a necessary expense for all car owners. However, insurance rates can vary widely depending on your coverage level, driving history, and location.

Comparing Car Insurance Quotes

Shop around and compare car insurance quotes from multiple companies to find the best rates.

Factors Affecting Insurance Rates

- Driving History: A clean driving record will result in lower insurance rates.

- Coverage Level: Higher coverage levels will result in higher insurance rates.

- Location: Insurance rates vary by location.

- Vehicle Type: Some vehicles are more expensive to insure than others.

FAQ: Common Questions About Car Affordability

1. What is the 20/4/10 rule for buying a car?

The 20/4/10 rule suggests putting down 20% of the car’s price, financing for no more than 4 years, and ensuring that the total cost of car ownership doesn’t exceed 10% of your gross monthly income.

2. How do I calculate my affordable car payment?

Start with your monthly net income, subtract your essential expenses, and then allocate 10-15% of the remaining amount to your car payment.

3. Should I include insurance and fuel costs in my car budget?

Yes, include insurance, fuel, maintenance, and other car-related expenses to get a complete picture of your total car ownership cost.

4. Is it better to lease or buy a car?

Leasing offers lower monthly payments and the ability to drive a new car more often, while buying allows you to own the car outright after the loan is paid off. The best option depends on your financial goals and preferences.

5. How does a down payment affect my car payment?

A larger down payment reduces the loan amount, resulting in lower monthly payments and reduced interest costs.

6. What credit score is needed to get a good car loan rate?

An excellent credit score (750+) will get you the best interest rates, while a good credit score (700-749) will still qualify you for competitive rates.

7. How can I improve my credit score before buying a car?

Pay your bills on time, reduce your credit card balances, and dispute any errors on your credit report.

8. What are some negotiation tactics for buying a car?

Research the market value, get pre-approved for a loan, shop around, start with a low offer, focus on the out-the-door price, and be willing to walk away.

9. How does fuel efficiency impact car affordability?

A fuel-efficient vehicle can save you significant money on gasoline over the life of the car, reducing your overall cost of ownership.

10. How can income-partners.net help me afford my dream car?

income-partners.net provides resources and opportunities to increase your income through strategic partnerships, allowing you to afford your dream car without straining your budget.

Unlock Your Financial Potential with Income-Partners.Net

Ready to take control of your car payment and achieve your financial goals? Visit income-partners.net today to explore partnership opportunities, learn valuable financial planning strategies, and connect with a network of like-minded individuals. Discover the power of collaboration and start building a brighter financial future. Don’t wait – your dream car and financial freedom are within reach. Contact us today to learn more.