The income threshold for Obamacare determines your eligibility for subsidies and cost assistance, impacting your access to affordable health insurance. At income-partners.net, we help you navigate these complexities, providing clarity on how income affects your healthcare options and connecting you with the right resources to maximize your benefits. Discover how strategic partnerships can further enhance your financial well-being and ensure you have access to quality healthcare through collaborative income strategies, fiscal planning resources and economic stability.

1. Understanding Obamacare and Income Thresholds

What Is The Income Threshold For Obamacare, and how does it affect your eligibility for financial assistance? The income threshold for Obamacare, officially known as the Affordable Care Act (ACA), determines whether you qualify for premium tax credits and cost-sharing reductions that can significantly lower your health insurance costs. Let’s explore the essentials of Obamacare income limits.

The ACA uses a metric called the Federal Poverty Level (FPL) to determine eligibility. This level is set annually by the U.S. Department of Health and Human Services. According to research from the University of Texas at Austin’s McCombs School of Business, understanding the FPL is critical for assessing your potential benefits under Obamacare.

-

Federal Poverty Level (FPL): The FPL serves as a benchmark for income eligibility. It varies based on household size, with higher levels for larger households.

-

Premium Tax Credits: These credits reduce your monthly health insurance premiums, making coverage more affordable. They are available to individuals and families with incomes between 100% and 400% of the FPL.

-

Cost-Sharing Reductions (CSR): These reductions lower your out-of-pocket expenses, such as deductibles, copayments, and coinsurance. CSRs are available to those with incomes between 100% and 250% of the FPL who enroll in a Silver plan.

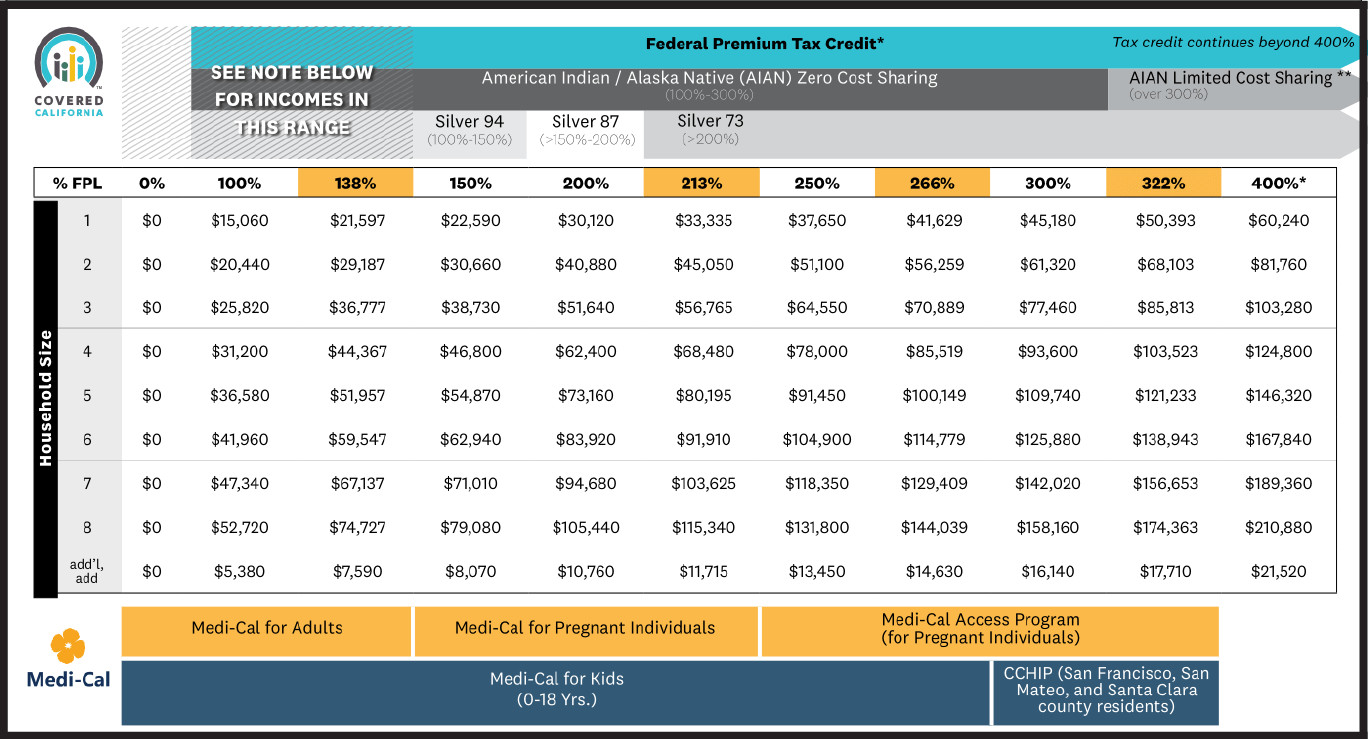

Chart showing program eligibility by federal poverty level

Chart showing program eligibility by federal poverty level

2. How the Federal Poverty Level (FPL) Impacts Your Obamacare Eligibility

How does the Federal Poverty Level (FPL) influence your Obamacare eligibility, and what are the specific income brackets you should be aware of? The Federal Poverty Level (FPL) plays a pivotal role in determining your eligibility for Obamacare subsidies and cost-sharing reductions. Let’s delve into the specifics of how the FPL impacts your access to affordable healthcare.

-

Calculating Your Income as a Percentage of FPL: To determine your eligibility, your household income is calculated as a percentage of the FPL. For instance, if the FPL for a single individual is $14,580, and your income is $29,160, your income is 200% of the FPL.

-

Eligibility Tiers Based on FPL:

- 100% to 400% FPL: Individuals and families in this income range are eligible for premium tax credits, which lower their monthly insurance premiums.

- 100% to 250% FPL: In addition to premium tax credits, those in this income bracket may also qualify for cost-sharing reductions (CSRs), which reduce out-of-pocket healthcare costs.

- Below 100% FPL: In most states, individuals with incomes below 100% of the FPL may qualify for Medicaid, which provides comprehensive healthcare coverage at little to no cost.

According to the Department of Health and Human Services (HHS), understanding these income tiers is vital for maximizing your benefits under Obamacare.

3. Understanding Modified Adjusted Gross Income (MAGI) for Obamacare

What is Modified Adjusted Gross Income (MAGI), and why is it crucial for determining your eligibility for Obamacare subsidies? Modified Adjusted Gross Income (MAGI) is a specific calculation used to determine your eligibility for Obamacare subsidies and cost-sharing reductions. It’s not just about your gross income; MAGI takes into account certain deductions and additions to provide a more accurate picture of your financial situation.

-

Definition of MAGI: MAGI is calculated from your Adjusted Gross Income (AGI) on your tax return, with a few key modifications. Specifically, MAGI includes:

- Adjusted Gross Income (AGI)

- Non-taxable Social Security benefits

- Tax-exempt interest income

- Foreign earned income and housing expenses

According to the IRS, understanding MAGI is essential for accurately determining your eligibility for healthcare subsidies.

How to Calculate Your MAGI

Calculating your MAGI involves a few simple steps:

- Start with your Adjusted Gross Income (AGI): This is your gross income minus certain deductions like student loan interest, IRA contributions, and alimony payments.

- Add back certain items: Add back any non-taxable Social Security benefits, tax-exempt interest income, and any foreign earned income or housing expenses.

Why MAGI Matters for Obamacare

MAGI is crucial for Obamacare because it provides a standardized way to assess income across different households, ensuring that subsidies and cost-sharing reductions are distributed fairly. This method is designed to be more accurate than simply looking at gross income.

4. Navigating Obamacare Income Limits During Pregnancy

How do Obamacare income limits change during pregnancy, and what resources are available to ensure pregnant women receive adequate healthcare? Navigating Obamacare income limits during pregnancy is essential for ensuring expectant mothers receive the comprehensive healthcare they need. During pregnancy, the income requirements for healthcare coverage may differ from the standard limits, providing additional support to pregnant women.

-

Expanded Eligibility for Pregnant Women:

- Medi-Cal: Pregnant women in California may qualify for Medi-Cal if their income falls between 138% and 213% of the poverty level. This ensures they receive comprehensive medical care throughout their pregnancy.

- Medi-Cal Access Program (MCAP): For those with slightly higher incomes, the Medi-Cal Access Program (MCAP) provides coverage for pregnant individuals with incomes between 213% and 322% of the poverty level.

-

Immediate Coverage: When applying for Medi-Cal during pregnancy, eligibility is often presumed while the application is being reviewed, allowing immediate access to necessary care.

According to the Affordable Care Act (ACA), all marketplace and Medicaid plans must provide coverage for pregnancy and childbirth, ensuring comprehensive care for expectant mothers.

Pregnant woman in California

Pregnant woman in California

5. Obamacare and Income Limits for Families with Children

How do Obamacare income limits affect families with children, and what resources are available to ensure children receive adequate healthcare coverage? Understanding Obamacare income limits for families with children is crucial for ensuring that all members of the family have access to quality healthcare. Different income thresholds apply to children, making it easier for them to qualify for coverage.

-

Children’s Eligibility for Medi-Cal:

- Income Threshold: In California, children may qualify for Medi-Cal if their family’s household income is 266% or less of the Federal Poverty Level (FPL). This threshold is higher than the one for adults, ensuring more children have access to healthcare.

- Age Requirement: To qualify, children must be under 19 years of age.

-

County Children’s Health Initiative Program (C-CHIP):

- Higher Income Families: For families with incomes greater than 266% and up to 322% of the FPL, the County Children’s Health Initiative Program (C-CHIP) offers healthcare coverage.

- Comprehensive Coverage: C-CHIP ensures that children from higher-income families also have access to necessary medical services.

6. How Seasonal Income Fluctuations Impact Obamacare Eligibility

How do seasonal income fluctuations affect Obamacare eligibility, and what steps can you take to ensure continuous coverage? Seasonal income fluctuations can significantly impact your eligibility for Obamacare subsidies. Understanding how these changes affect your income calculation is essential for maintaining continuous healthcare coverage.

-

Estimating Annual Income: When applying for Obamacare, you must estimate your annual income. If your income varies due to seasonal work, it’s crucial to make an accurate estimate to avoid discrepancies in your subsidies.

-

Reporting Income Changes: If your actual income deviates significantly from your estimate, you must report these changes to Obamacare. Significant changes can impact your eligibility for subsidies, and reporting them promptly can prevent overpayments or underpayments.

- Increased Income: If your income increases, your subsidy may decrease, and you may need to pay more for your monthly premiums.

- Decreased Income: If your income decreases, you may qualify for a higher subsidy, reducing your monthly premiums.

-

Avoiding Penalties: Failing to report income changes can lead to penalties or the need to repay excess subsidies when you file your taxes. Keeping your information up-to-date ensures you receive the correct amount of financial assistance.

7. Understanding Different Obamacare Plan Levels Based on Income

How do Obamacare plan levels vary based on income, and which plan is the best fit for your financial situation? Obamacare offers various plan levels designed to cater to different income levels and healthcare needs. Understanding these plan levels can help you choose the one that best fits your financial situation.

-

Plan Levels: Obamacare plans are divided into four main categories: Bronze, Silver, Gold, and Platinum. Each level offers a different balance between monthly premiums and out-of-pocket costs.

-

Bronze Plan:

- Premiums: Lowest

- Out-of-Pocket Costs: Highest

- Coverage: Covers about 60% of your healthcare costs

- Ideal For: Individuals who prioritize low monthly premiums and don’t anticipate needing frequent medical care.

-

Silver Plan:

- Premiums: Moderate

- Out-of-Pocket Costs: Moderate

- Coverage: Covers about 70% of your healthcare costs

- Ideal For: Individuals who qualify for cost-sharing reductions (CSRs), which lower out-of-pocket costs.

-

Gold Plan:

- Premiums: Higher

- Out-of-Pocket Costs: Lower

- Coverage: Covers about 80% of your healthcare costs

- Ideal For: Individuals willing to pay higher monthly premiums for lower out-of-pocket costs when they need medical care.

-

Platinum Plan:

- Premiums: Highest

- Out-of-Pocket Costs: Lowest

- Coverage: Covers about 90% of your healthcare costs

- Ideal For: Individuals who need frequent medical care and are willing to pay higher premiums to minimize out-of-pocket expenses.

-

-

Cost-Sharing Reductions (CSRs) and Silver Plans: If your income falls between 100% and 250% of the Federal Poverty Level (FPL), you may qualify for CSRs, which can significantly lower your out-of-pocket costs on a Silver plan. These reductions make Silver plans an attractive option for those who qualify.

8. What are Silver-Enhanced Plans and How Do They Work?

What are Silver-Enhanced plans, and how can they provide additional cost savings based on your income level? Silver-Enhanced plans are special types of Silver plans available through Obamacare that offer additional cost-sharing reductions (CSRs) based on your income. These plans can significantly reduce your out-of-pocket healthcare costs, making them an attractive option for eligible individuals.

-

Eligibility for Silver-Enhanced Plans: To qualify for Silver-Enhanced plans, your income must fall within specific ranges of the Federal Poverty Level (FPL):

- Silver Enhanced 94 Plan: Available to those with incomes between 138% and 150% of the FPL.

- Silver Enhanced 87 Plan: Available to those with incomes between 150% and 200% of the FPL.

- Silver Enhanced 73 Plan: Available to those with incomes between 200% and 250% of the FPL.

-

How Silver-Enhanced Plans Work: These plans provide lower deductibles, copayments, and coinsurance compared to standard Silver plans. The level of cost-sharing reduction varies depending on your income bracket, with higher subsidies available to those with lower incomes.

9. Providing Proof of Income for Your Obamacare Application

What documents are required to provide proof of income for your Obamacare application, and how can you ensure a smooth application process? Providing accurate and complete proof of income is crucial for a successful Obamacare application. The documents required may vary depending on your employment status and income sources.

-

For Employed Individuals:

- Pay Stubs: Provide recent pay stubs that show your year-to-date earnings.

- W-2 Forms: Include your W-2 forms from the previous year. If you don’t have these, a letter from your employer confirming your income can be used.

-

For Self-Employed Individuals:

- 1099 Forms: Gather 1099 forms from businesses or clients who paid you.

- Tax Returns: Include your most recent California income tax return, including all attachments and schedules.

- Income Statement: Provide a statement detailing your current year’s income and expenses.

- Bank Statements: Submit bank statements showing deposits related to your self-employed income.

-

Additional Income Sources:

- Social Security Benefits Letter: Include a benefits letter from the Social Security Administration.

- Pension or Retirement Income Documents: Provide documents confirming any pension or retirement income.

- Unemployment Benefits Documents: Submit documents confirming any unemployment benefits you received.

- Alimony Documents: Include legal documents or statements showing alimony you received.

- Investment Account Statements: Provide statements from your investment accounts showing dividends or interest received.

-

Tips for a Smooth Application Process:

- Submit Documents Promptly: Ensure all documents are submitted without delay.

- Ensure Clarity and Legibility: Make sure all documents are clear and legible.

- Complete All Fields: Fill out all necessary fields on multi-page documents.

10. Reporting Income Changes to Obamacare Mid-Year

Why is it important to report income changes to Obamacare mid-year, and how can you avoid potential penalties? Reporting income changes to Obamacare mid-year is essential to ensure you receive the correct amount of financial assistance. Failing to report these changes can lead to penalties or the need to repay excess subsidies when you file your taxes.

-

Reasons to Report Income Changes:

- Wage or Salary Changes: Report any increases or decreases in your wages or salary.

- Self-Employment Income Adjustments: Adjustments to your self-employment income should be reported promptly.

- Unemployment Benefits Changes: Changes to your unemployment benefits must be reported.

- One-Time Payments: Report any one-time payments like bonuses or inheritances.

-

How to Report Changes:

- Contact Obamacare Marketplace: Contact the Obamacare marketplace directly to report changes to your income.

- Provide Documentation: Be prepared to provide documentation to support the reported changes.

- Update Information Online: Update your information online through your Obamacare account.

-

Potential Consequences of Not Reporting:

- Overpayment of Subsidies: If your income increases and you don’t report it, you may receive excess subsidies that you’ll need to repay.

- Underpayment of Subsidies: If your income decreases and you don’t report it, you may miss out on additional financial assistance.

- Penalties: Failing to report income changes can result in penalties when you file your taxes.

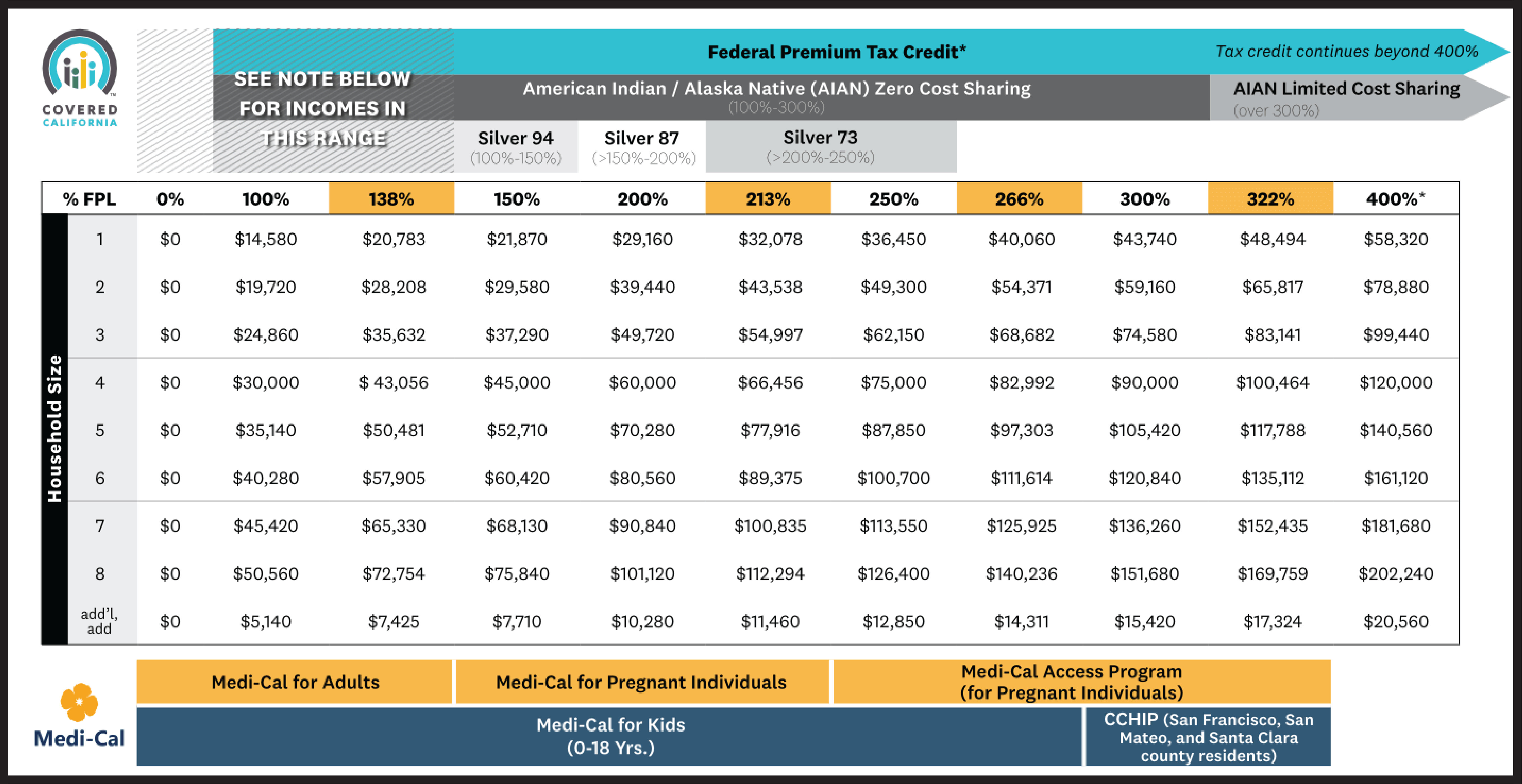

chart showing program eligibility by federal poverty level for 2023

chart showing program eligibility by federal poverty level for 2023

FAQ Section: Obamacare Income Thresholds

1. What is the income threshold to qualify for Obamacare in 2024?

The income threshold to qualify for Obamacare in 2024 ranges from 100% to 400% of the Federal Poverty Level (FPL), making premium tax credits available to those within this range.

2. How is my income calculated for Obamacare eligibility?

Your income for Obamacare eligibility is calculated using Modified Adjusted Gross Income (MAGI), which includes your Adjusted Gross Income (AGI) with certain additions like non-taxable Social Security benefits and tax-exempt interest income.

3. What happens if my income changes during the year?

If your income changes during the year, it’s essential to report these changes to Obamacare to ensure you receive the correct amount of financial assistance and avoid potential penalties.

4. Can pregnant women have different income limits for Obamacare?

Yes, pregnant women may have expanded income limits for healthcare coverage through programs like Medi-Cal and the Medi-Cal Access Program (MCAP), ensuring they receive comprehensive care during pregnancy.

5. Are there different income limits for children under Obamacare?

Yes, children may qualify for Medi-Cal with higher income limits than adults, ensuring more children have access to healthcare coverage.

6. What are Silver-Enhanced plans, and how do they help?

Silver-Enhanced plans are special types of Silver plans that offer additional cost-sharing reductions (CSRs) based on your income, reducing out-of-pocket healthcare costs for eligible individuals.

7. What documents do I need to provide as proof of income for my Obamacare application?

You may need to provide pay stubs, W-2 forms, 1099 forms, tax returns, bank statements, and other documents to verify your income for your Obamacare application.

8. How do seasonal income fluctuations affect my Obamacare eligibility?

Seasonal income fluctuations can impact your Obamacare eligibility, making it important to estimate your annual income accurately and report any significant changes to avoid discrepancies in your subsidies.

9. What should I do if my income exceeds the Obamacare limits?

If your income exceeds the Obamacare limits, you may still be able to purchase a plan through the marketplace, though you won’t qualify for premium tax credits or cost-sharing reductions.

10. Where can I find more information about Obamacare income thresholds and eligibility?

You can find more information about Obamacare income thresholds and eligibility on the official Obamacare website or through resources like income-partners.net, which offers guidance on navigating healthcare options and maximizing your financial benefits through strategic partnerships.

Are you looking to maximize your financial well-being and access affordable healthcare? Visit income-partners.net to explore strategic partnerships and collaborative income strategies that can enhance your access to quality healthcare. Discover how you can leverage our resources to navigate Obamacare income thresholds effectively and ensure you have the coverage you need. Contact us today to learn more about how we can help you achieve financial stability and healthcare security. Address: 1 University Station, Austin, TX 78712, United States. Phone: +1 (512) 471-3434.