Individual income tax is a tax levied on your earnings, but how does it actually work? Individual income tax, as explored at income-partners.net, is a crucial aspect of financial planning and partnership opportunities, impacting your potential for increased earnings and business growth. Understanding this tax can unlock financial benefits, improve your tax strategy, and pave the way for strategic partnerships to boost your income.

1. How Does Individual Income Tax Work?

Individual income tax is a tax on a person’s earnings, including wages, salaries, and investment income, typically collected by federal and state governments. The U.S. operates under a progressive tax system, meaning higher income levels are taxed at higher rates.

In the United States, individual income taxes are imposed at both the federal and state levels. Numerous countries around the world also employ this form of taxation. The U.S. income tax is progressive, indicating that tax rates (the percentage of your income paid in taxes) rise as income increases. Income tax rates in the U.S. vary from 10% to 37%, based on specific income thresholds. These income ranges are referred to as tax brackets. All income within a particular bracket is taxed at the corresponding rate.

2024 Federal Income Tax Brackets and Rates

| Tax Rate | Single Filers | Married Filing Jointly | Heads of Households |

|---|---|---|---|

| 10% | $0 to $11,600 | $0 to $23,200 | $0 to $16,550 |

| 12% | $11,600 to $47,150 | $23,200 to $94,300 | $16,550 to $63,100 |

| 22% | $47,150 to $100,525 | $94,300 to $201,050 | $63,100 to $100,500 |

| 24% | $100,525 to $191,950 | $201,050 to $383,900 | $100,500 to $191,950 |

| 32% | $191,950 to $243,725 | $383,900 to $487,450 | $191,950 to $243,700 |

| 35% | $243,725 to $609,350 | $487,450 to $731,200 | $243,700 to $609,350 |

| 37% | $609,350 or more | $731,200 or more | $609,350 or more |

Source: Internal Revenue Service

This graduated-rate system, where each dollar above a threshold is taxed at a higher rate, leads to marginal tax rates. These rates reflect the additional tax paid for each extra dollar earned. Taxpayers often reduce their tax liability through deductions and credits. Common deductions include the standard deduction and itemized deductions. Credits like the Earned Income Tax Credit (EITC) and Child Tax Credit (CTC) also help reduce taxes. Many state tax codes offer similar deductions and credits.

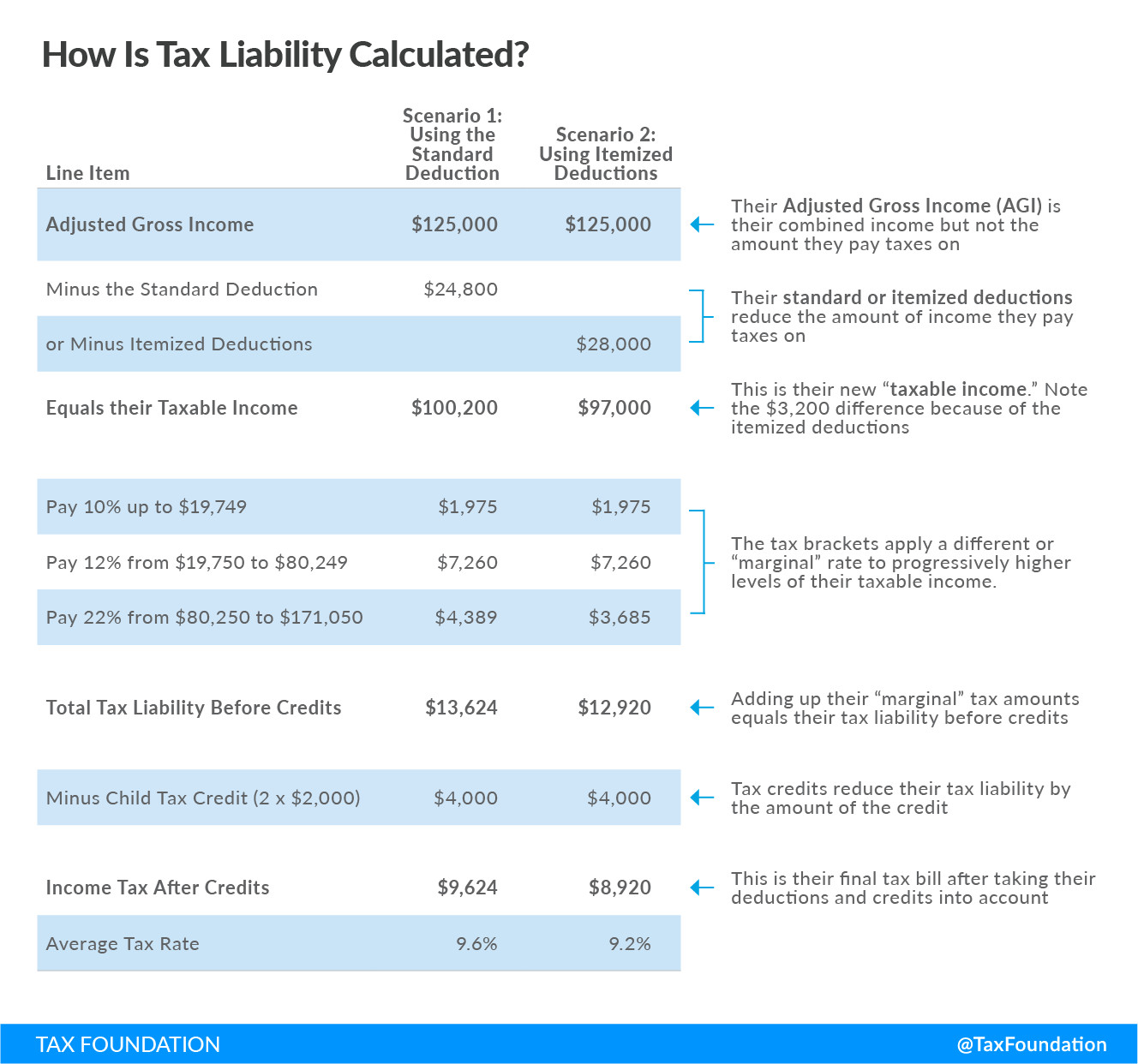

Tax Basics – How Is Tax Liability Calculated, adjusted gross income, average tax rate, child tax credit, earned income tax credit, individual income tax, itemized deduction, marginal tax rate, standard deduction, tax credit, tax deduction, taxable income

Tax Basics – How Is Tax Liability Calculated, adjusted gross income, average tax rate, child tax credit, earned income tax credit, individual income tax, itemized deduction, marginal tax rate, standard deduction, tax credit, tax deduction, taxable income

Understanding tax liability calculation, showcasing the impact of deductions and credits, and how they influence the final tax amount.

2. Who Is Required To Pay Federal Income Tax In The U.S.?

In the U.S., individuals who earn above a certain income threshold set by the IRS are required to pay federal income tax. The exact amount depends on filing status, age, and whether you can be claimed as a dependent.

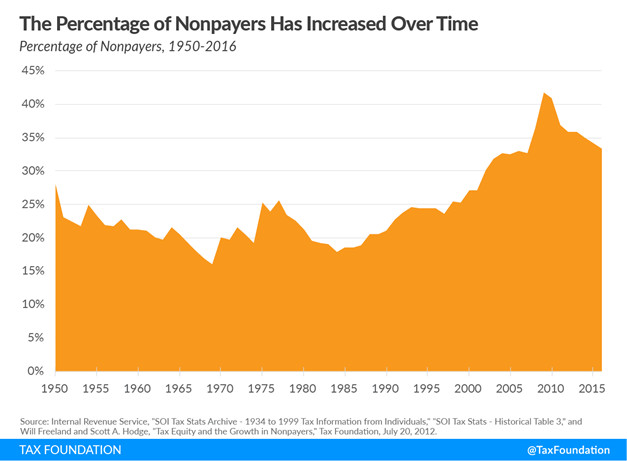

The progressive nature of the U.S. tax system means higher-income individuals pay a larger proportion of income taxes than lower-income individuals. Between 1950 and 2016, more U.S. taxpayers owed zero income taxes because of credits and deductions. The percentage of nonpayers increased from 28% in 1950 to 33.4% in 2016. The minimum percentage of nonpayers during this period was 16% in 1969, and the maximum was 41.7% in 2009.

The Percentage of Nonpayers Has Increased Over Time

The Percentage of Nonpayers Has Increased Over Time

Analysis of historical tax data showing the rise in the percentage of non-taxpayers over the years.

3. Why Is Understanding Individual Income Tax Important for Partnering to Increase Income?

Understanding individual income tax is crucial because it directly impacts your net earnings from partnerships, influencing financial planning and investment strategies. Effective tax management can significantly increase your profitability.

Navigating the complexities of income tax is essential for maximizing earnings and fostering successful partnerships. Consider these points:

- Financial Planning: Understanding tax implications enables you to make informed financial decisions, allocate resources effectively, and plan for future investments.

- Net Earnings: Knowledge of income tax helps you accurately calculate your net earnings after taxes, providing a clear view of your financial gains from partnerships.

- Investment Strategies: A strong grasp of tax laws allows you to develop tax-efficient investment strategies that minimize your tax liability and enhance your overall financial growth.

- Profitability: Effective tax management can significantly boost your profitability by reducing the amount of income paid in taxes, thus increasing your retained earnings.

According to a study by the University of Texas at Austin’s McCombs School of Business, businesses that prioritize tax planning and management experience an average of 15% higher profitability compared to those that do not.

4. What Are the Benefits of Understanding Individual Income Tax?

Understanding individual income tax allows you to optimize deductions, claim applicable credits, and structure your financial activities to minimize tax liabilities, ultimately leading to increased savings and investment opportunities.

There are several key advantages to understanding individual income tax:

- Optimizing Deductions: Knowledge of eligible deductions allows you to reduce your taxable income, leading to lower tax payments.

- Claiming Credits: Awareness of available tax credits enables you to further decrease your tax liability, providing additional financial relief.

- Financial Structuring: Understanding tax laws helps you structure your financial activities in a tax-efficient manner, minimizing your overall tax burden.

- Increased Savings: By minimizing tax liabilities, you can increase your savings and have more funds available for investments and other financial opportunities.

Income-partners.net provides valuable resources to help you navigate these benefits and make informed decisions about your income tax.

5. How Does Individual Income Tax Affect Different Income Levels?

The progressive tax system affects income levels differently, with higher earners paying a larger percentage of their income in taxes compared to lower earners, reflecting the principle of ability to pay.

The progressive tax system means that individuals with higher incomes pay a larger percentage of their income in taxes compared to those with lower incomes. This system reflects the principle of ability to pay, ensuring that those who can afford to contribute more to public services do so.

- Lower Income Levels: Individuals in lower income brackets benefit from lower tax rates, allowing them to retain a larger portion of their earnings for essential needs and savings.

- Middle Income Levels: Middle-income earners face moderate tax rates, balancing their contributions to public services with their financial obligations and investment opportunities.

- Higher Income Levels: Higher-income earners are subject to higher tax rates, contributing a larger share of their income to support public programs and services, while still having significant financial resources available.

This progressive structure helps fund essential government services and promotes a more equitable distribution of wealth across society.

6. How Can Partnering With Income-Partners.Net Help Me Manage My Individual Income Tax?

Partnering with income-partners.net provides access to expert advice, tools, and resources for optimizing your tax strategy, identifying beneficial deductions, and ensuring compliance with tax laws, ultimately maximizing your financial gains.

Partnering with income-partners.net can significantly enhance your ability to manage your individual income tax effectively. Here’s how:

- Expert Advice: Gain access to seasoned tax professionals who can provide personalized advice tailored to your financial situation and partnership activities.

- Optimized Tax Strategy: Develop a comprehensive tax strategy that aligns with your income goals, business structure, and investment plans.

- Deduction Identification: Discover eligible deductions and credits that can significantly reduce your tax liability and increase your net earnings.

- Compliance Assurance: Ensure full compliance with current tax laws and regulations, avoiding potential penalties and legal issues.

- Financial Maximization: Maximize your financial gains by leveraging tax-efficient strategies and optimizing your tax position.

Income-partners.net offers a range of resources and tools to support your tax management efforts, including webinars, articles, and personalized consultations.

Address: 1 University Station, Austin, TX 78712, United States

Phone: +1 (512) 471-3434

Website: income-partners.net

7. What Are Common Misconceptions About Individual Income Tax?

Common misconceptions include believing that all income is taxed at the highest marginal rate, not understanding available deductions and credits, and overlooking the impact of state income taxes on overall tax liability.

Many people hold misconceptions about individual income tax, which can lead to financial errors and missed opportunities. Here are some common misconceptions:

- All Income Taxed at Highest Rate: A common myth is that all income is taxed at your highest marginal rate. In reality, the progressive tax system means only the portion of income within each tax bracket is taxed at that specific rate.

- Ignoring Deductions and Credits: Many taxpayers fail to take advantage of available deductions and credits, such as those for education, healthcare, or charitable donations, resulting in a higher tax bill.

- Overlooking State Income Taxes: It’s important to consider state income taxes, which can significantly impact overall tax liability, especially in states with high income tax rates.

- Complexity and Professional Help: Some believe that individual income tax is too complex to understand, leading them to avoid seeking professional advice, which can help optimize their tax strategy.

By addressing these misconceptions, individuals can make informed decisions and optimize their tax planning for greater financial benefit.

8. What Strategies Can Individuals Use To Minimize Their Individual Income Tax?

Strategies to minimize individual income tax include maximizing retirement contributions, utilizing tax-advantaged investment accounts, claiming all eligible deductions and credits, and strategically timing income and expenses.

Individuals can employ several strategies to minimize their individual income tax liability. These strategies involve careful planning and understanding of tax laws:

- Retirement Contributions: Maximize contributions to tax-advantaged retirement accounts like 401(k)s and IRAs, which can reduce your taxable income while saving for retirement.

- Tax-Advantaged Investments: Utilize tax-advantaged investment accounts such as Health Savings Accounts (HSAs) and 529 plans to save on healthcare and education expenses, respectively.

- Eligible Deductions and Credits: Claim all eligible deductions and credits, including those for mortgage interest, student loan interest, and energy-efficient home improvements.

- Strategic Income and Expenses Timing: Strategically time income and expenses to shift income to lower tax years or accelerate deductions to higher tax years, optimizing your tax outcome.

By implementing these strategies, individuals can effectively minimize their tax burden and maximize their financial well-being.

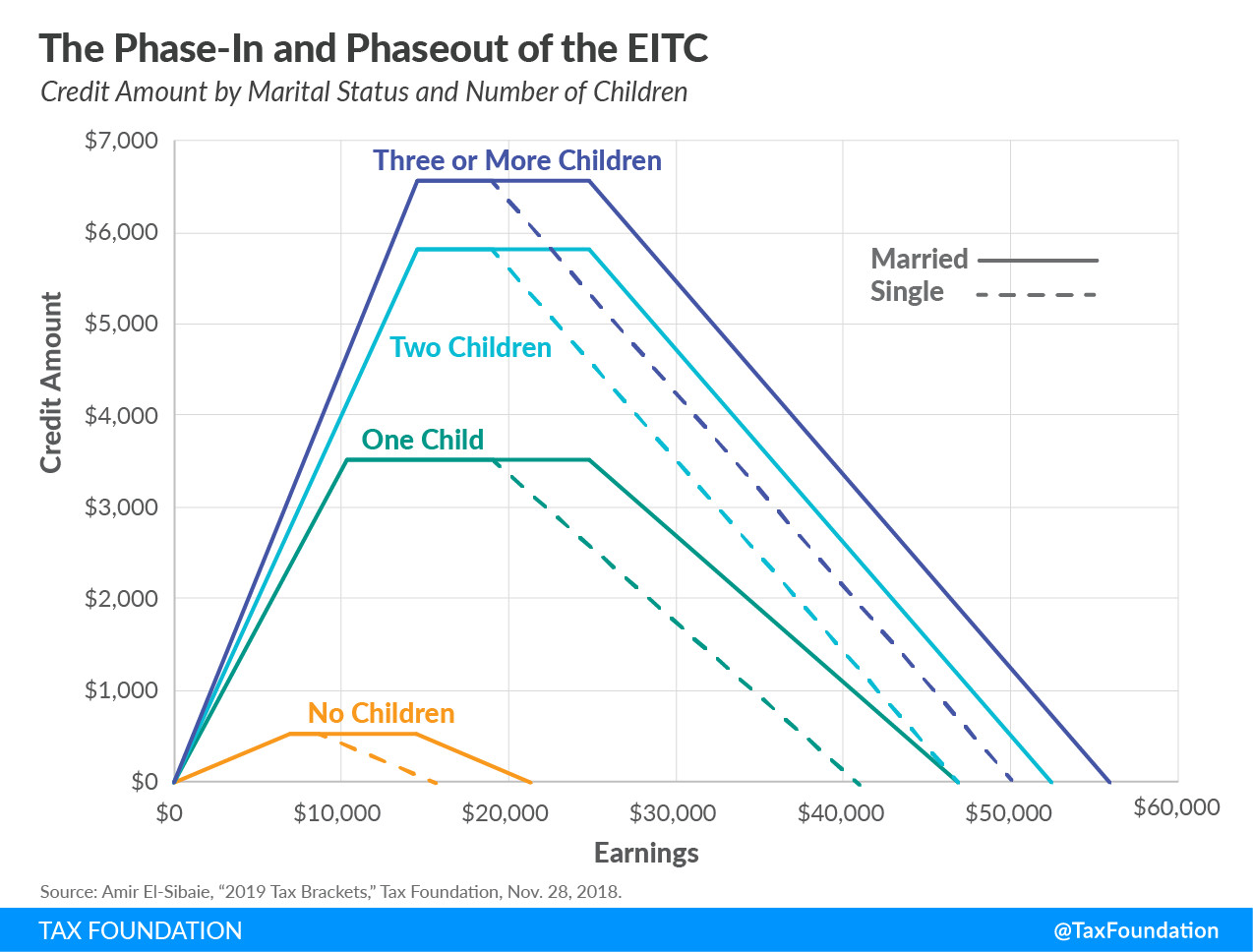

The Phase-In and Phaseout of the EITC Earned Income Tax Credit

The Phase-In and Phaseout of the EITC Earned Income Tax Credit

Understanding the Earned Income Tax Credit (EITC), including phase-in and phaseout ranges, to maximize its benefits for eligible taxpayers.

9. How Do State and Local Income Taxes Differ From Federal Income Taxes?

State and local income taxes vary significantly from federal income taxes in terms of rates, brackets, deductions, and credits, reflecting the unique fiscal policies and priorities of each state or locality.

State and local income taxes differ significantly from federal income taxes, as each state and locality sets its own tax policies to meet its specific fiscal needs. Here’s how they compare:

- Tax Rates: Federal income tax rates are uniform across the country, while state and local rates vary widely. Some states have no income tax, while others have progressive or flat tax systems with different rate structures.

- Tax Brackets: The number and width of tax brackets differ between federal, state, and local levels. Federal brackets are generally broader and more complex than those at the state and local levels.

- Deductions and Credits: States and localities offer different deductions and credits than the federal government. These may include deductions for property taxes, local charitable donations, or credits for specific local investments.

- Fiscal Policies: State and local tax policies reflect local priorities, such as funding education, infrastructure, or public services. These policies influence the types of taxes levied and how they are structured.

Understanding these differences is essential for accurate tax planning and compliance at all levels of government.

10. How Does Individual Income Tax Impact Business Partnerships and Opportunities?

Individual income tax impacts business partnerships by affecting the distribution of profits, the tax liabilities of partners, and the overall financial attractiveness of partnership ventures, necessitating careful tax planning and structuring.

Individual income tax significantly impacts business partnerships, influencing the distribution of profits and the financial outcomes for partners. Here’s how:

- Profit Distribution: The way profits are distributed among partners affects individual income tax liabilities. Partners must report their share of profits on their individual tax returns, regardless of whether the profits are actually distributed.

- Tax Liabilities: Each partner is responsible for paying individual income tax on their share of the partnership’s profits. Understanding these tax liabilities is crucial for financial planning and ensuring tax compliance.

- Partnership Structure: The structure of the partnership can impact tax liabilities. For example, limited partnerships and limited liability companies (LLCs) may offer different tax advantages compared to general partnerships.

- Financial Attractiveness: Effective tax planning can enhance the financial attractiveness of partnership ventures. Minimizing tax liabilities allows partners to retain more of their earnings, making the partnership more profitable.

Therefore, careful tax planning and structuring are essential for maximizing the benefits of business partnerships. According to Harvard Business Review, partnerships that prioritize tax efficiency often experience higher returns and greater financial stability.

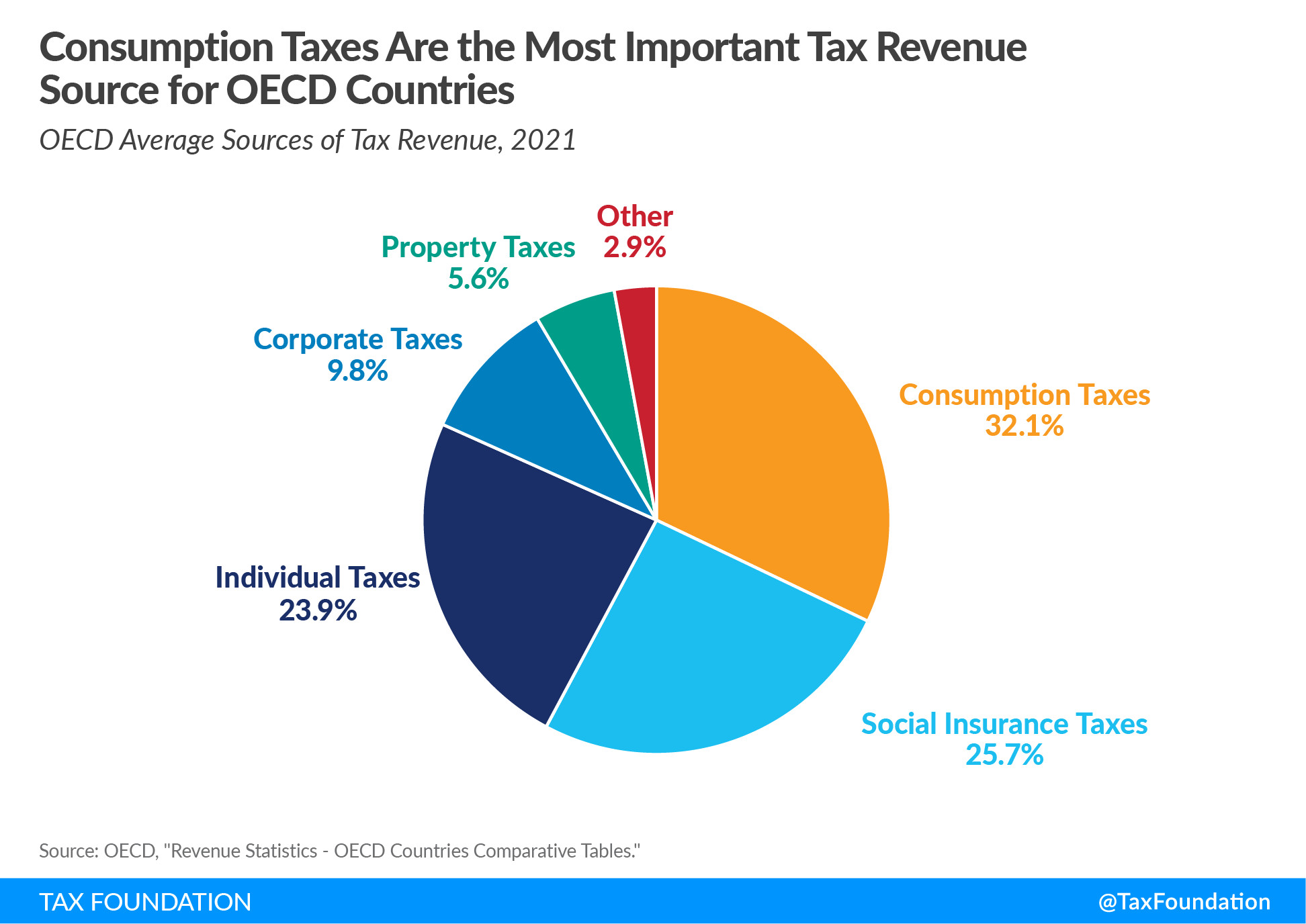

Compared to the OECD average, the United States relies more on individual income taxes. In 2021, OECD countries raised 23.9% of total tax revenue from individual income taxes. In the U.S., individual income taxes (federal, state, and local) were the primary source of tax revenue at 42.1%, exceeding the OECD average by over 18 percentage points.

US OECD rev2023 1

US OECD rev2023 1

Comparison of tax revenue sources between the U.S. and OECD countries, emphasizing the reliance on individual income taxes in the U.S.

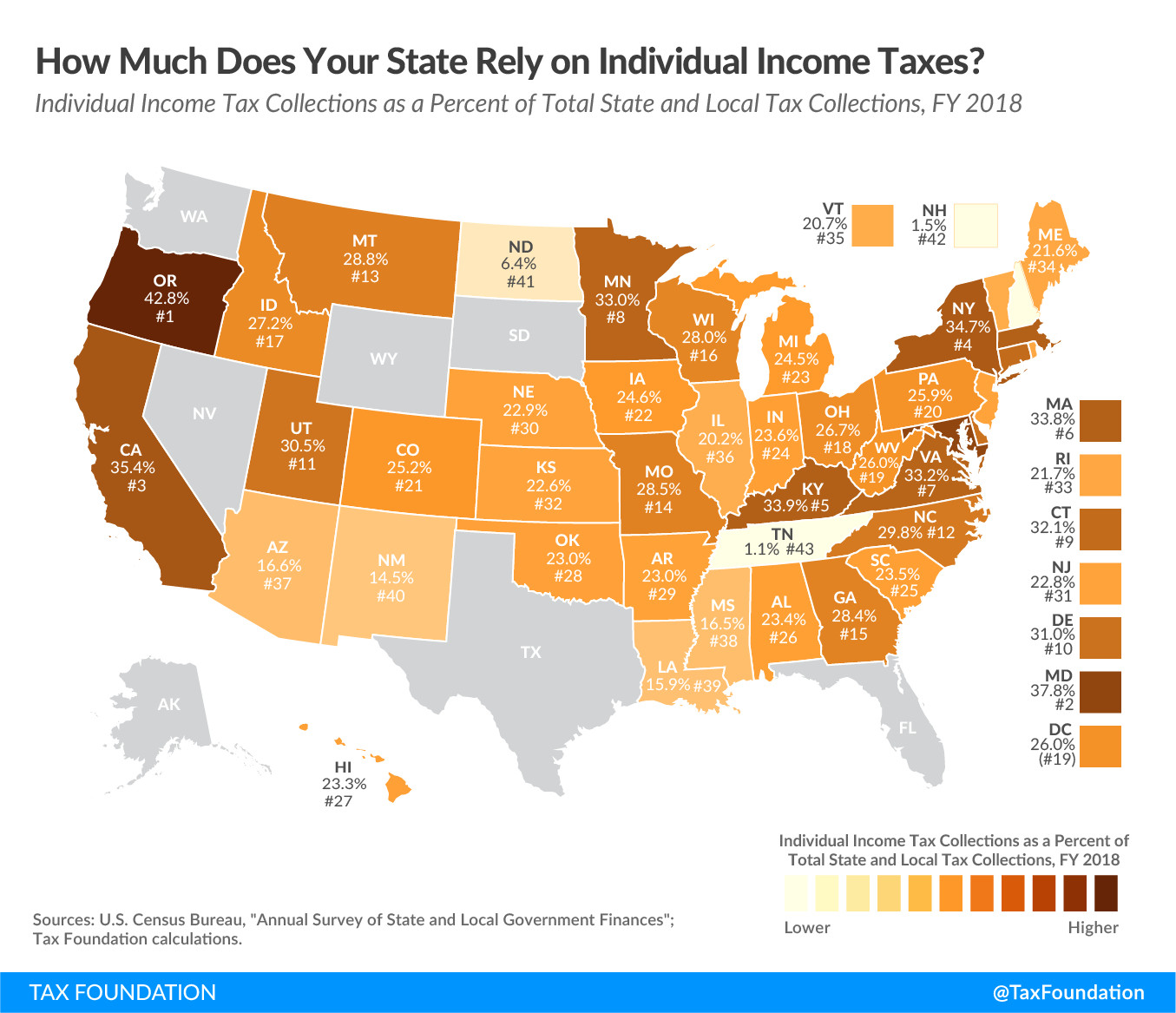

State and local governments also depend heavily on individual income tax, which comprised 22.8% of total U.S. state and local tax collections in fiscal year 2020. Reliance on income taxes varies significantly by state.

State tax reliance State income tax reliance. How much do states rely on income taxes To what extent does your state rely on individual income taxes 2021 01

State tax reliance State income tax reliance. How much do states rely on income taxes To what extent does your state rely on individual income taxes 2021 01

Visual representation of state tax reliance on individual income taxes, highlighting differences among states.

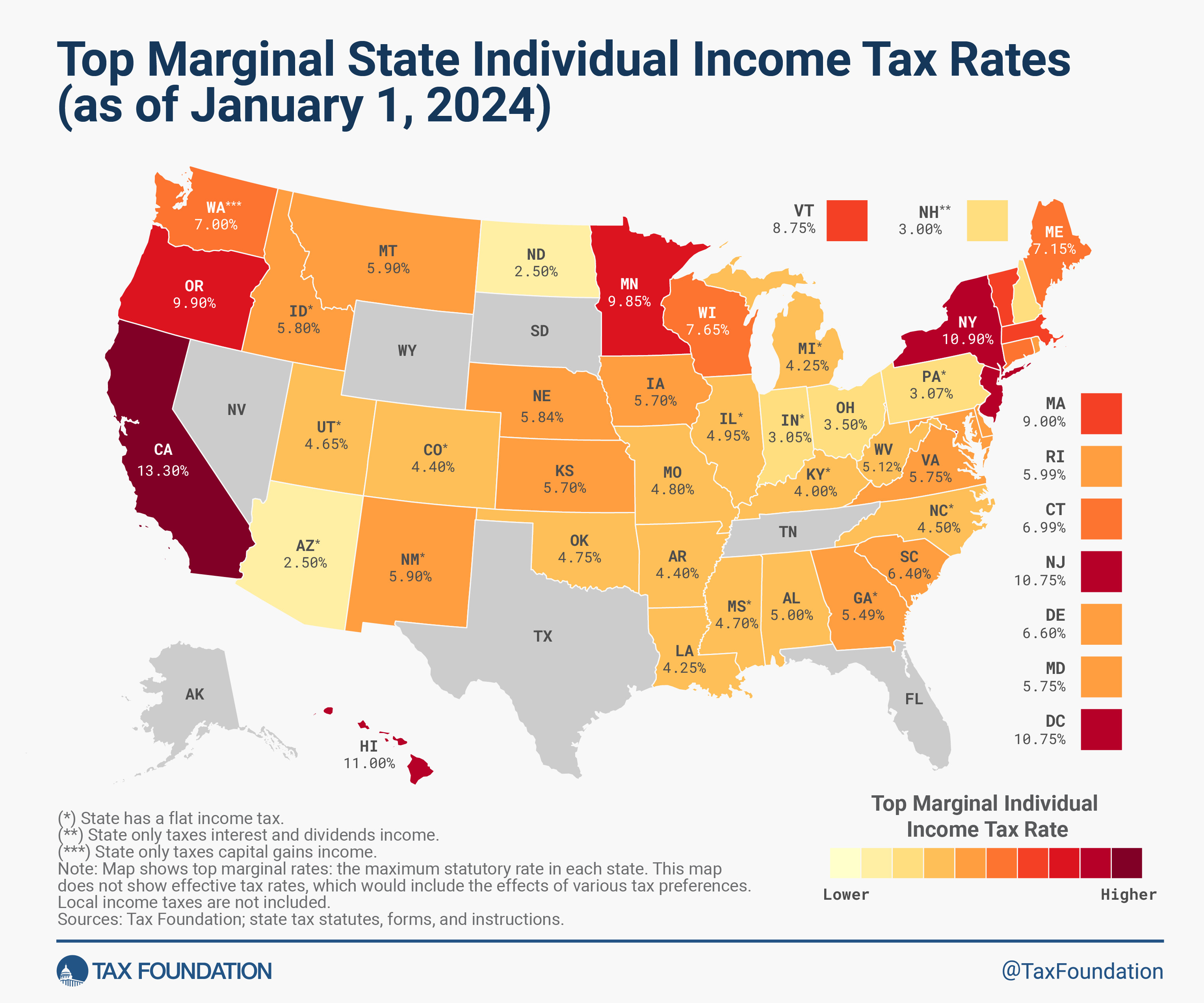

As of 2024, 43 states levy individual income taxes. Forty-one tax wage and salary income, while New Hampshire taxes dividend and interest income exclusively, and Washington taxes only capital gains income. Seven states levy no individual income tax.

Of the states taxing wages, 12 have single-rate tax structures, often called a flat tax, with one rate for all taxable income. Conversely, 29 states and the District of Columbia levy graduated-rate, progressive income taxes, with the number of brackets varying widely by state. Hawaii has 12 brackets, the most in the country.

Approaches to income taxes vary in other details as well. Some states double single-bracket widths for married filers to avoid a marriage penalty. Some states index tax brackets, exemptions, and deductions for inflation, while others do not. Some states tie their standard deductions and personal exemptions to the federal tax code, while others set their own or offer none at all.

2024 state income tax rates and states with no income tax

2024 state income tax rates and states with no income tax

Overview of state income tax rates and identification of states without income tax for 2024.

Ready to unlock the full potential of strategic partnerships and elevate your income? Visit income-partners.net now to explore diverse partnership opportunities, master effective relationship-building strategies, and connect with potential collaborators in the U.S. Don’t miss out on the chance to transform your financial future.

FAQ About Individual Income Tax

1. What is the difference between tax deductions and tax credits?

Tax deductions reduce your taxable income, while tax credits directly reduce the amount of tax you owe.

2. How do I determine my filing status?

Your filing status depends on your marital status and family situation, such as single, married filing jointly, or head of household.

3. What is the standard deduction for 2024?

The standard deduction for 2024 varies based on filing status, with specific amounts set by the IRS each year.

4. Are Social Security benefits taxable?

A portion of your Social Security benefits may be taxable, depending on your total income and filing status.

5. What is the difference between marginal and effective tax rates?

Marginal tax rate is the rate on your last dollar of income, while the effective tax rate is the total tax paid as a percentage of your total income.

6. Can I deduct contributions to a traditional IRA?

You may be able to deduct contributions to a traditional IRA, depending on your income and whether you are covered by a retirement plan at work.

7. What is the Earned Income Tax Credit (EITC)?

The EITC is a tax credit for low-to-moderate income working individuals and families.

8. How do I file my taxes?

You can file your taxes online, through the mail, or with the help of a tax professional.

9. What happens if I don’t file my taxes on time?

Failing to file taxes on time can result in penalties and interest charges.

10. Where can I find reliable information about individual income tax?

Reliable sources include the IRS website, tax professionals, and reputable financial websites like income-partners.net.