Taxable income is the foundation upon which your tax obligations are calculated, and understanding what it includes is crucial for effective financial planning and maximizing your partnership opportunities; income-partners.net offers resources to help you navigate this complex topic. This guide explores the components of taxable income, deductions, and exemptions, equipping you with the knowledge to optimize your financial strategy and identify potential income-boosting partnerships. Dive in to discover how to leverage this knowledge for your financial success, with insights tailored for entrepreneurs, investors, and business professionals seeking to thrive in the US market, especially in bustling hubs like Austin, all while building lucrative partnerships.

1. What Exactly is Included in Taxable Income?

Taxable income refers to the portion of your gross income that is subject to taxation by federal, state, and local governments; this includes wages, salaries, tips, investment income, and business profits, but after certain deductions and exemptions are applied. Understanding what constitutes taxable income is essential for accurately calculating your tax liability and exploring strategies to minimize it through smart financial partnerships.

To elaborate, taxable income is not simply the total amount of money you earn in a year. It’s a refined figure arrived at by subtracting certain deductions and exemptions from your gross income. Let’s break down the components:

-

Gross Income: This is the starting point. It includes all income you receive, such as wages, salaries, bonuses, commissions, investment income (dividends, interest), rental income, royalties, and business profits. Even income from sources like gambling winnings or digital assets is included.

-

Above-the-Line Deductions: These deductions are subtracted from your gross income to arrive at your Adjusted Gross Income (AGI). Common above-the-line deductions include contributions to traditional IRAs, student loan interest payments, and alimony payments (for divorce agreements finalized before 2019).

-

Adjusted Gross Income (AGI): This is your gross income minus above-the-line deductions. AGI is an important figure because it’s used to determine eligibility for certain tax credits and deductions.

-

Below-the-Line Deductions: After calculating your AGI, you can choose to either take the standard deduction or itemize your deductions. The standard deduction is a fixed amount that depends on your filing status (single, married filing jointly, etc.). Itemized deductions include expenses like medical expenses (above a certain percentage of AGI), state and local taxes (SALT, up to a limit), mortgage interest, and charitable contributions.

-

Taxable Income: This is the final figure upon which your tax liability is calculated. It’s your AGI minus either the standard deduction or your total itemized deductions.

Example:

Let’s say you’re a single entrepreneur in Austin, Texas.

- Gross Income: $150,000 (from your business)

- Above-the-Line Deductions: $5,000 (traditional IRA contributions)

- AGI: $145,000

- Standard Deduction (2024): $14,600 (for single filers)

- Taxable Income: $130,400

In this scenario, your tax liability would be based on the $130,400 of taxable income. Understanding these components allows you to strategically plan your finances and potentially reduce your tax burden.

2. How Do Wages and Salaries Factor Into Taxable Income?

Wages and salaries are fundamental components of taxable income, representing compensation received for services performed as an employee. Employers typically withhold federal and state income taxes, as well as Social Security and Medicare taxes, from each paycheck. Understanding how these withholdings impact your overall tax liability is crucial for effective financial planning, and income-partners.net can connect you with experts who can provide personalized guidance.

Let’s delve deeper into how wages and salaries are taxed:

- Tax Withholding: When you start a new job, you fill out a W-4 form, which tells your employer how much federal income tax to withhold from your paycheck. The amount withheld depends on factors like your filing status, the number of dependents you claim, and whether you have other sources of income.

- State Income Tax: Most states also have income taxes, and your employer will withhold state income tax based on your state’s withholding rules.

- Social Security and Medicare Taxes: These taxes, also known as FICA taxes, are also withheld from your paycheck. In 2024, the Social Security tax rate is 6.2% on wages up to $168,600, and the Medicare tax rate is 1.45% on all wages.

- Form W-2: At the end of each year, your employer will send you a W-2 form, which summarizes your earnings and the amount of taxes withheld from your paychecks. You’ll use this form to file your tax return.

Strategic Considerations for Wages and Salaries:

- Adjusting Your Withholding: If you find that you’re consistently owing money when you file your tax return, you may want to adjust your W-4 form to increase the amount of tax withheld from your paycheck. Conversely, if you’re consistently getting a large refund, you may want to decrease your withholding.

- Tax-Advantaged Retirement Plans: Contributing to tax-advantaged retirement plans like 401(k)s or traditional IRAs can reduce your taxable income in the year you make the contribution.

- Employee Benefits: Take advantage of employee benefits like health insurance, flexible spending accounts (FSAs), and health savings accounts (HSAs), as these can help reduce your taxable income or pay for qualified expenses with pre-tax dollars.

Example:

Imagine you’re a marketing manager in Austin earning an annual salary of $80,000.

- Federal Income Tax Withholding: Approximately $8,000 (this can vary based on your W-4 form)

- State Income Tax Withholding (Texas has no state income tax): $0

- Social Security Tax Withholding: $4,960 (6.2% of $80,000)

- Medicare Tax Withholding: $1,160 (1.45% of $80,000)

Your taxable income from wages would be $80,000 minus any deductions you’re eligible for, such as contributions to a 401(k) or HSA. By understanding these withholdings and exploring available deductions, you can optimize your tax strategy and potentially increase your take-home pay.

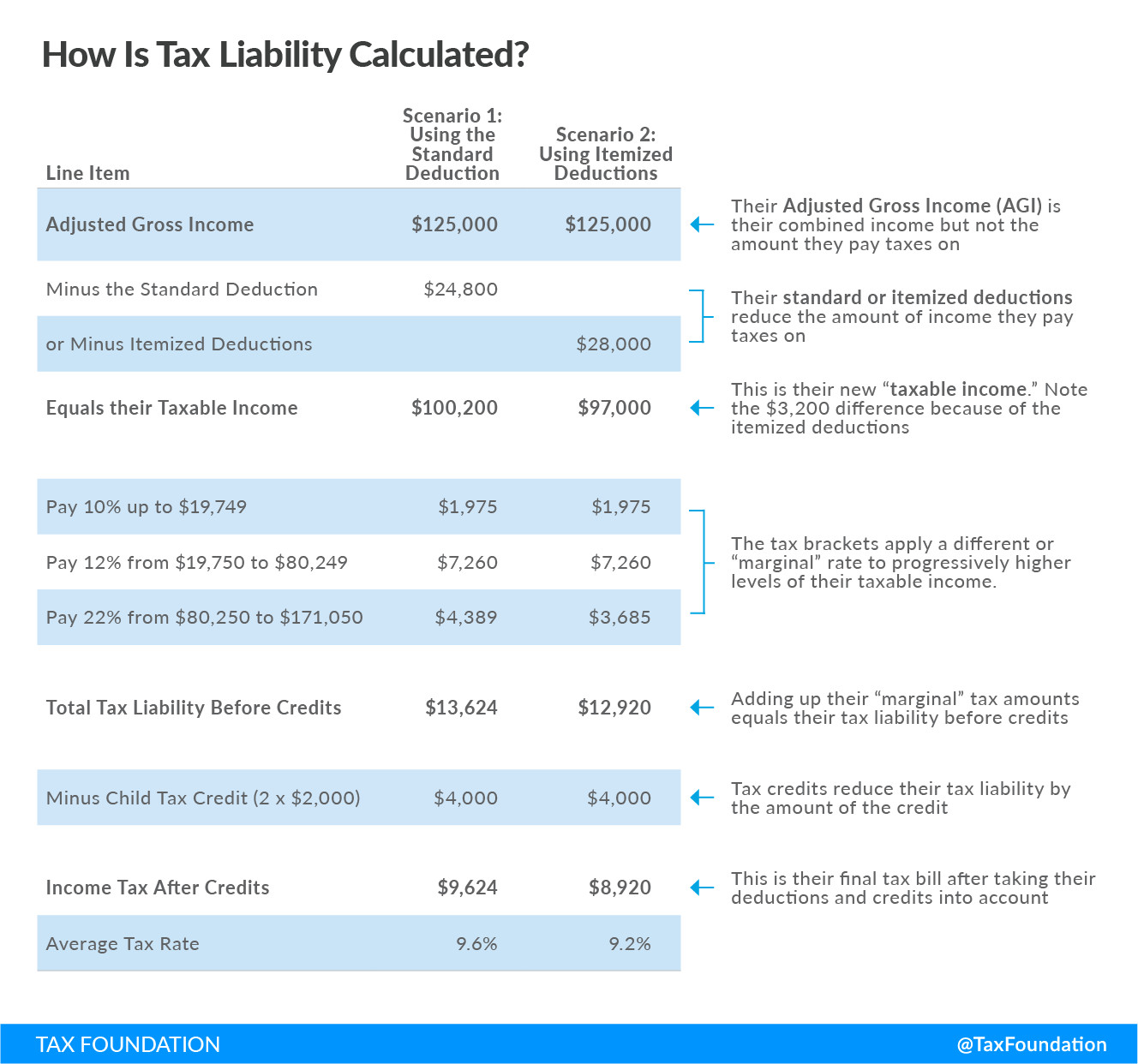

Tax Basics – How Is Tax Liability Calculated, adjusted gross income, average tax rate, child tax credit, earned income tax credit, individual income tax, itemized deduction, marginal tax rate, standard deduction, tax credit, tax deduction, taxable income

Tax Basics – How Is Tax Liability Calculated, adjusted gross income, average tax rate, child tax credit, earned income tax credit, individual income tax, itemized deduction, marginal tax rate, standard deduction, tax credit, tax deduction, taxable income

3. What About Investment Income: Is It Taxable?

Investment income, encompassing dividends, interest, capital gains, and rental income, is generally considered taxable, but the specific tax treatment varies depending on the type of investment and how long it’s held. Strategic investment planning, potentially with guidance from partners found on income-partners.net, is essential for minimizing your tax liability while maximizing returns.

Here’s a breakdown of how different types of investment income are taxed:

- Dividends: Dividends are payments made by corporations to their shareholders. They can be classified as either qualified or non-qualified dividends.

- Qualified Dividends: These are taxed at lower capital gains rates, which are generally lower than ordinary income tax rates. To qualify, the stock must be held for a certain period.

- Non-Qualified Dividends: These are taxed at your ordinary income tax rate.

- Interest: Interest income is earned from savings accounts, bonds, and other interest-bearing investments. It’s generally taxed at your ordinary income tax rate.

- Capital Gains: Capital gains are profits from the sale of assets, such as stocks, bonds, or real estate.

- Short-Term Capital Gains: These are profits from assets held for one year or less and are taxed at your ordinary income tax rate.

- Long-Term Capital Gains: These are profits from assets held for more than one year and are taxed at lower capital gains rates. The specific rate depends on your income level.

- Rental Income: Rental income is the money you receive from renting out a property. You can deduct expenses related to the rental property, such as mortgage interest, property taxes, and repairs, to reduce your taxable rental income.

Strategic Considerations for Investment Income:

- Tax-Advantaged Accounts: Utilize tax-advantaged accounts like Roth IRAs and 401(k)s to shield your investment income from taxes. Roth accounts offer tax-free withdrawals in retirement, while traditional accounts offer tax deductions on contributions.

- Tax-Loss Harvesting: This involves selling investments that have lost value to offset capital gains. This can help reduce your overall tax liability.

- Holding Period: Be mindful of the holding period for assets you sell, as long-term capital gains are taxed at lower rates than short-term capital gains.

- Qualified Dividends: Hold stocks for the required period to ensure that dividends are classified as qualified dividends and taxed at lower rates.

Example:

Let’s say you’re an investor in Austin who earned the following investment income in 2024:

- Qualified Dividends: $5,000

- Interest Income: $2,000

- Short-Term Capital Gains: $3,000

- Long-Term Capital Gains: $8,000

The qualified dividends and long-term capital gains would be taxed at lower capital gains rates, while the interest income and short-term capital gains would be taxed at your ordinary income tax rate. By understanding these nuances and implementing tax-smart investment strategies, you can optimize your portfolio’s after-tax returns.

4. How Are Business Profits and Losses Treated for Tax Purposes?

Business profits are a key component of taxable income for entrepreneurs and self-employed individuals, but business losses can offset other income, potentially reducing your overall tax liability. Navigating these complexities effectively, possibly with the aid of a strategic partner from income-partners.net, is essential for maximizing your business’s financial health.

Here’s a detailed look at how business profits and losses are treated for tax purposes:

- Business Profits: If you’re self-employed or own a business, your business profits are generally considered taxable income. This includes income from sales, services, and other business activities.

- Business Expenses: You can deduct ordinary and necessary business expenses from your business income to reduce your taxable profits. These expenses can include things like rent, utilities, supplies, marketing, and travel.

- Pass-Through Entities: Many small businesses are structured as pass-through entities, such as sole proprietorships, partnerships, or S corporations. In these cases, the business’s profits and losses “pass through” to the owners’ individual tax returns.

- Business Losses: If your business incurs a loss, you may be able to deduct the loss from your other income, such as wages or investment income. However, there are limits on the amount of business losses you can deduct in a given year.

- Net Operating Loss (NOL): If your business losses exceed your other income, you may have a net operating loss (NOL). You can generally carry back an NOL to prior tax years or carry it forward to future tax years to offset income.

Strategic Considerations for Business Profits and Losses:

- Record Keeping: Maintain accurate and detailed records of your business income and expenses. This will make it easier to calculate your taxable profits and claim all eligible deductions.

- Entity Structure: Choose the right business entity structure for your needs. Factors to consider include liability protection, tax implications, and administrative complexity.

- Tax Planning: Work with a tax professional to develop a tax plan that minimizes your tax liability while complying with all applicable laws.

- Qualified Business Income (QBI) Deduction: If you’re a pass-through entity, you may be eligible for the Qualified Business Income (QBI) deduction, which can further reduce your taxable income.

Example:

Let’s say you’re a freelance web designer in Austin who earned $70,000 in business income in 2024. You also had $20,000 in business expenses, such as software subscriptions, office supplies, and marketing costs.

- Business Income: $70,000

- Business Expenses: $20,000

- Taxable Business Profit: $50,000

Your taxable income from your business would be $50,000. You may also be eligible for the QBI deduction, which could further reduce your taxable income. Conversely, if your business expenses exceeded your income, you could have a business loss that could offset other income on your tax return. By carefully managing your business finances and working with a tax professional, you can optimize your tax strategy and maximize your business’s profitability.

5. How Do Deductions and Exemptions Reduce Taxable Income?

Deductions and exemptions are key tools for reducing your taxable income, thereby lowering your tax liability; deductions reduce your income subject to tax, while exemptions (though less common now) were fixed amounts that reduced taxable income. Strategic use of deductions and understanding available exemptions, potentially in collaboration with a financial partner from income-partners.net, is essential for effective tax planning.

Let’s explore how deductions and exemptions work:

- Deductions: A tax deduction reduces your taxable income, which in turn reduces the amount of tax you owe. There are two main types of deductions:

- Above-the-Line Deductions: These deductions are subtracted from your gross income to arrive at your Adjusted Gross Income (AGI). Common above-the-line deductions include contributions to traditional IRAs, student loan interest payments, and alimony payments (for divorce agreements finalized before 2019).

- Below-the-Line Deductions: After calculating your AGI, you can choose to either take the standard deduction or itemize your deductions. Itemized deductions include expenses like medical expenses (above a certain percentage of AGI), state and local taxes (SALT, up to a limit), mortgage interest, and charitable contributions.

- Exemptions: Historically, exemptions were fixed amounts that you could deduct from your taxable income for yourself, your spouse, and each of your dependents. However, the Tax Cuts and Jobs Act of 2017 suspended personal and dependent exemptions, so they are no longer available for tax years 2018 through 2025.

Strategic Considerations for Deductions and Exemptions:

- Standard Deduction vs. Itemizing: Determine whether it’s more beneficial to take the standard deduction or itemize your deductions. If your itemized deductions exceed the standard deduction, it’s generally better to itemize.

- Maximize Deductions: Take advantage of all eligible deductions to reduce your taxable income. This includes deductions for retirement contributions, student loan interest, medical expenses, and charitable contributions.

- Tax Planning: Work with a tax professional to identify all available deductions and develop a tax plan that minimizes your tax liability.

Examples of Common Deductions:

- Retirement Contributions: Contributions to traditional IRAs and 401(k)s are generally deductible, which can significantly reduce your taxable income.

- Student Loan Interest: You can deduct the interest you pay on student loans, up to a certain limit.

- Medical Expenses: You can deduct medical expenses that exceed a certain percentage of your AGI.

- State and Local Taxes (SALT): You can deduct state and local taxes, such as property taxes and state income taxes, up to a limit of $10,000 per household.

- Mortgage Interest: You can deduct the interest you pay on your mortgage, up to certain limits.

- Charitable Contributions: You can deduct contributions you make to qualified charitable organizations.

Example:

Let’s say you’re a homeowner in Austin with the following deductions in 2024:

- Mortgage Interest: $12,000

- State and Local Taxes (Property Taxes): $8,000

- Charitable Contributions: $3,000

Your total itemized deductions would be $23,000. If the standard deduction for your filing status is less than $23,000, it would be more beneficial for you to itemize your deductions. By strategically utilizing deductions, you can significantly reduce your taxable income and lower your tax bill.

6. What Are Some Examples of Nontaxable Income?

While most income is taxable, certain types of income are considered nontaxable by the IRS, including gifts, inheritances (though estate taxes may apply), life insurance proceeds, and certain scholarships. Identifying and understanding these exclusions, with advice potentially from partners at income-partners.net, can help you better manage your overall financial picture.

Let’s take a closer look at examples of nontaxable income:

- Gifts: Money or property you receive as a gift is generally not considered taxable income. However, the person giving the gift may be subject to gift tax if the value of the gift exceeds a certain amount ($18,000 per recipient in 2024).

- Inheritances: Money or property you inherit from a deceased person is generally not considered taxable income. However, the deceased person’s estate may be subject to estate tax if the value of the estate exceeds a certain amount.

- Life Insurance Proceeds: The proceeds you receive from a life insurance policy are generally not considered taxable income.

- Certain Scholarships and Grants: Scholarships and grants used to pay for tuition, fees, and required course materials are generally not considered taxable income. However, amounts used for room and board may be taxable.

- Child Support Payments: Child support payments you receive are not considered taxable income.

- Workers’ Compensation Benefits: Workers’ compensation benefits you receive for job-related injuries or illnesses are not considered taxable income.

- Certain Welfare Benefits: Certain welfare benefits, such as Supplemental Security Income (SSI) and Temporary Assistance for Needy Families (TANF), are not considered taxable income.

- Distributions from Roth IRA (under certain circumstances): Distributions of contributions and earnings from your Roth IRA are tax-free, as long as you have satisfied the requirements for qualified distribution

Strategic Considerations for Nontaxable Income:

- Gift Tax Planning: If you plan to give significant gifts, consult with a tax advisor to understand the gift tax rules and minimize your tax liability.

- Estate Planning: Work with an estate planning attorney to develop an estate plan that minimizes estate taxes and ensures your assets are distributed according to your wishes.

- Scholarship and Grant Reporting: Keep accurate records of how you use scholarship and grant funds to ensure that you can exclude them from your taxable income.

Example:

Let’s say you received the following income in 2024:

- Salary: $70,000

- Gift from a Relative: $10,000

- Life Insurance Proceeds: $50,000

Your taxable income would be based on your salary of $70,000. The gift and life insurance proceeds would not be considered taxable income. By understanding the rules surrounding nontaxable income, you can better manage your finances and avoid unnecessary tax liabilities.

7. How Does Filing Status Impact Taxable Income Calculations?

Your filing status—single, married filing jointly, married filing separately, head of household, or qualifying widow(er)—significantly impacts your standard deduction, tax brackets, and eligibility for certain credits and deductions. Selecting the correct filing status, potentially with guidance from a partner on income-partners.net, is crucial for minimizing your tax liability.

Let’s explore how different filing statuses affect your taxable income:

- Single: This filing status is for unmarried individuals who do not qualify for any other filing status.

- Married Filing Jointly: This filing status is for married couples who choose to file a joint tax return. It generally offers the most favorable tax treatment for married couples.

- Married Filing Separately: This filing status is for married couples who choose to file separate tax returns. It may be beneficial in certain situations, such as when one spouse has significant medical expenses or student loan debt.

- Head of Household: This filing status is for unmarried individuals who pay more than half the costs of keeping up a home for a qualifying child or other relative. It offers a larger standard deduction and more favorable tax brackets than the single filing status.

- Qualifying Widow(er) with Dependent Child: This filing status is for a surviving spouse whose spouse died within the past two years and who has a dependent child. It offers the same standard deduction and tax brackets as the married filing jointly status.

Impact on Standard Deduction:

The standard deduction varies depending on your filing status:

- Single: $14,600 (2024)

- Married Filing Jointly: $29,200 (2024)

- Married Filing Separately: $14,600 (2024)

- Head of Household: $21,900 (2024)

- Qualifying Widow(er) with Dependent Child: $29,200 (2024)

Impact on Tax Brackets:

Tax brackets also vary depending on your filing status. For example, the income thresholds for each tax bracket are generally higher for married filing jointly than for single filers.

Impact on Credits and Deductions:

Some tax credits and deductions are only available to certain filing statuses. For example, the child and dependent care credit has different rules depending on whether you’re single, married filing jointly, or head of household.

Strategic Considerations for Filing Status:

- Determine Eligibility: Carefully determine which filing status you’re eligible for. If you’re unsure, consult with a tax professional.

- Compare Tax Liabilities: If you’re married, calculate your tax liability under both the married filing jointly and married filing separately statuses to see which results in the lowest tax bill.

- Consider the Impact on Credits and Deductions: Be aware of how your filing status affects your eligibility for various tax credits and deductions.

Example:

Let’s say you’re a single parent in Austin with a dependent child. You may be eligible to file as head of household, which would give you a larger standard deduction and more favorable tax brackets than if you filed as single. By choosing the correct filing status, you can significantly reduce your taxable income and lower your tax bill.

8. How Do State and Local Taxes Interact With Federal Taxable Income?

State and local taxes (SALT), such as property taxes and state income taxes, can be deducted on your federal tax return, subject to a limit, potentially reducing your federal taxable income; understanding these interactions, possibly with advice from a tax-focused partner from income-partners.net, is key for maximizing your tax savings.

Here’s how state and local taxes interact with federal taxable income:

- Itemized Deduction: You can deduct state and local taxes as an itemized deduction on your federal tax return. However, the Tax Cuts and Jobs Act of 2017 limited the amount of SALT you can deduct to $10,000 per household.

- Types of SALT: The state and local taxes you can deduct include:

- State and Local Income Taxes: This includes state and local income taxes withheld from your paycheck or paid during the year.

- State and Local Property Taxes: This includes property taxes you pay on your home or other real estate.

- State and Local Sales Taxes: If you choose not to deduct state and local income taxes, you can deduct state and local sales taxes instead. This may be beneficial if you live in a state with no income tax.

- Limitation: The $10,000 limit applies to the total amount of state and local income taxes, property taxes, and sales taxes you can deduct. It’s not a separate limit for each type of tax.

Strategic Considerations for SALT Deduction:

- Track Your SALT Payments: Keep accurate records of your state and local tax payments throughout the year.

- Determine Deduction Method: Determine whether it’s more beneficial to deduct state and local income taxes or state and local sales taxes. This will depend on your individual circumstances and the tax laws in your state.

- Consider the Impact of the Limit: Be aware of the $10,000 limit on the SALT deduction. If your state and local taxes exceed this amount, you won’t be able to deduct the full amount.

Example:

Let’s say you’re a homeowner in Austin, Texas (which has no state income tax), and you paid the following state and local taxes in 2024:

- Property Taxes: $9,000

- State Income Taxes (Texas has no state income tax): $0

You would be able to deduct $9,000 as an itemized deduction on your federal tax return. However, if you also paid state income taxes in another state, your total SALT deduction would be limited to $10,000. By understanding the rules surrounding the SALT deduction, you can maximize your tax savings and reduce your federal taxable income.

9. What Role Do Tax Credits Play in Reducing Tax Liability Compared to Taxable Income?

Tax credits directly reduce your tax liability, dollar for dollar, offering a more potent benefit than deductions, which only reduce taxable income. Identifying and claiming eligible tax credits, possibly with guidance from a financial expert from income-partners.net, is an essential strategy for minimizing your tax burden.

Here’s a breakdown of the role tax credits play in reducing tax liability:

- Direct Reduction of Tax Liability: Tax credits directly reduce the amount of tax you owe. For example, a $1,000 tax credit reduces your tax bill by $1,000.

- More Valuable Than Deductions: Tax credits are generally more valuable than deductions because they directly reduce your tax liability, while deductions only reduce your taxable income.

- Refundable vs. Nonrefundable Credits: Tax credits can be either refundable or nonrefundable.

- Refundable Credits: Refundable credits can result in a refund even if you don’t owe any taxes. For example, the Earned Income Tax Credit is a refundable credit.

- Nonrefundable Credits: Nonrefundable credits can only reduce your tax liability to $0. They cannot result in a refund. For example, the Child Tax Credit is a nonrefundable credit (although a portion of it may be refundable).

- Examples of Common Tax Credits:

- Child Tax Credit: This credit is for taxpayers with qualifying children.

- Earned Income Tax Credit (EITC): This credit is for low- to moderate-income workers and families.

- Child and Dependent Care Credit: This credit is for taxpayers who pay for child care or dependent care expenses so they can work or look for work.

- American Opportunity Tax Credit (AOTC): This credit is for students in their first four years of college.

- Lifetime Learning Credit: This credit is for students taking courses to improve their job skills.

- Energy Credits: There are several tax credits available for homeowners who make energy-efficient improvements to their homes.

Strategic Considerations for Tax Credits:

- Determine Eligibility: Carefully determine which tax credits you’re eligible for. The eligibility requirements can be complex, so it’s important to review them carefully.

- Claim All Eligible Credits: Be sure to claim all tax credits you’re eligible for. This can significantly reduce your tax liability.

- Keep Accurate Records: Keep accurate records of expenses related to tax credits, such as child care expenses or education expenses.

Example:

Let’s say you’re a single parent in Austin with a qualifying child and you’re eligible for the Child Tax Credit. The Child Tax Credit is worth up to $2,000 per child (for 2024). If your tax liability is $3,000 and you claim the Child Tax Credit for $2,000, your tax liability would be reduced to $1,000. If you’re also eligible for the Earned Income Tax Credit, you could potentially receive a refund even if you don’t owe any taxes. By understanding and claiming all eligible tax credits, you can significantly reduce your tax burden and improve your financial situation.

10. How Can I Strategically Plan to Minimize My Taxable Income and Maximize My Partnership Opportunities?

Strategic tax planning involves proactive measures to reduce your taxable income through deductions, credits, and tax-advantaged investments, while also identifying partnership opportunities that can enhance your financial position. Leveraging resources like income-partners.net is invaluable for connecting with potential partners and accessing expert advice on optimizing your tax strategy.

Here’s how you can strategically plan to minimize your taxable income and maximize your partnership opportunities:

- Maximize Deductions: Take advantage of all eligible deductions, such as deductions for retirement contributions, student loan interest, medical expenses, and charitable contributions.

- Utilize Tax Credits: Claim all tax credits you’re eligible for, such as the Child Tax Credit, Earned Income Tax Credit, and Child and Dependent Care Credit.

- Invest in Tax-Advantaged Accounts: Invest in tax-advantaged accounts like 401(k)s, IRAs, and HSAs to shield your investment income from taxes.

- Tax-Loss Harvesting: Use tax-loss harvesting to offset capital gains with capital losses.

- Choose the Right Business Entity: If you’re a business owner, choose the right business entity structure for your needs. Factors to consider include liability protection, tax implications, and administrative complexity.

- Partner Strategically: Seek out partnership opportunities that can enhance your financial position. This could include partnering with other businesses, investors, or experts in your field.

- Seek Professional Advice: Work with a tax professional and a financial advisor to develop a comprehensive tax plan and financial strategy that minimizes your tax liability and maximizes your partnership opportunities.

Specific Strategies for Entrepreneurs:

- Maximize Business Expense Deductions: Keep accurate records of all your business expenses and claim all eligible deductions.

- Take Advantage of the QBI Deduction: If you’re a pass-through entity, you may be eligible for the Qualified Business Income (QBI) deduction, which can further reduce your taxable income.

- Consider a Solo 401(k): If you’re self-employed, consider setting up a solo 401(k) to save for retirement and reduce your taxable income.

Specific Strategies for Investors:

- Invest in Tax-Efficient Investments: Consider investing in tax-efficient investments, such as municipal bonds or ETFs that track broad market indexes.

- Hold Investments for the Long Term: Hold investments for more than one year to qualify for long-term capital gains rates, which are generally lower than ordinary income tax rates.

- Use a Roth IRA: Consider using a Roth IRA to save for retirement and enjoy tax-free withdrawals in retirement.

Example:

Let’s say you’re an entrepreneur in Austin who is looking to minimize your taxable income and maximize your partnership opportunities. You could:

- Maximize your business expense deductions.

- Take advantage of the QBI deduction.

- Set up a solo 401(k) to save for retirement.

- Partner with other businesses in your industry.

- Seek advice from a tax professional and a financial advisor.

By implementing these strategies, you can significantly reduce your taxable income, maximize your partnership opportunities, and achieve your financial goals.

Ready to Take Control of Your Taxable Income and Unlock Lucrative Partnerships?

At income-partners.net, we understand the challenges you face in finding the right partners, building strong relationships, and navigating the complexities of business and finance. Whether you’re an entrepreneur seeking strategic alliances, an investor searching for promising projects, or a professional looking to expand your network, we provide the resources and connections you need to succeed.

Explore our platform to:

- Discover diverse partnership opportunities: Connect with potential partners across various industries and sectors.

- Learn effective relationship-building strategies: Access expert advice and resources on how to build and maintain successful partnerships.

- Stay updated on the latest trends and opportunities: Get insights into emerging trends and opportunities in the business world.

Don’t wait – visit income-partners.net today and start building the partnerships that will drive your success!

Address: 1 University Station, Austin, TX 78712, United States

Phone: +1 (512) 471-3434

Website: income-partners.net

Frequently Asked Questions (FAQ) About Taxable Income

1. What is the difference between gross income and taxable income?

Gross income is the total income you receive before any deductions or exemptions, while taxable income is the amount of income subject to tax after deductions and exemptions are applied.

2. What are some common examples of taxable income?

Common examples of taxable income include wages, salaries, tips, investment income, business profits, and rental income.

3. What are some common examples of nontaxable income?

Examples of nontaxable income include gifts, inheritances, life insurance proceeds, and certain scholarships and grants.

4. How do deductions reduce my taxable income?

Deductions reduce the amount of your income that is subject to tax, which in turn reduces your tax liability.

5. What is the standard deduction, and how does it affect my taxable income?

The standard deduction is a fixed amount that you can deduct from your adjusted gross income (AGI) to reduce your taxable income. The amount of the standard deduction varies depending on your filing status.

6. What are itemized deductions, and how do they differ from the standard deduction?

Itemized deductions are specific expenses that you can deduct from your AGI, such as medical expenses, state and local taxes, and charitable contributions. You can choose to either take the standard deduction or itemize your deductions, whichever results in a lower taxable income.

7. How do tax credits differ from deductions?

Tax credits directly reduce your tax liability, dollar for dollar, while deductions only reduce your taxable income.

8. How does my filing status affect my taxable income calculation?

Your filing status affects your standard deduction, tax brackets, and eligibility for certain credits and deductions.

9. Can business losses reduce my overall taxable income?

Yes, business losses can offset other income, potentially reducing your overall tax liability.

10. Where can I find reliable information and resources to help me understand taxable income and tax planning strategies?

You can find reliable information and resources on the IRS website, reputable tax preparation websites, and by consulting with a qualified tax professional. Additionally, income-partners.net provides valuable resources and connections to help you navigate the complexities of taxable income and optimize your financial strategy.