Debt-to-income ratio (DTI) is a crucial metric for assessing financial health, especially for individuals and businesses seeking partnership opportunities to boost income, and income-partners.net can help. This ratio is a percentage reflecting how much of your gross monthly income goes toward debt payments, providing insight into your financial obligations and stability. Explore how to leverage strategic partnerships for financial success, discover lucrative collaboration opportunities, and learn how to improve your DTI for better financial prospects.

1. What is Debt-to-Income Ratio (DTI)?

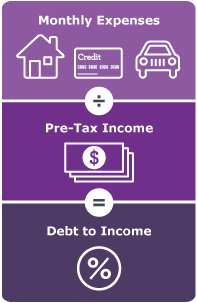

Debt-to-income ratio (DTI) is a financial metric comparing your monthly debt payments to your gross monthly income, expressed as a percentage. It’s used by lenders to assess your ability to manage monthly payments and repay debts. A lower DTI typically indicates a healthier financial situation, signaling to lenders that you have more income available to cover debts. According to research from the University of Texas at Austin’s McCombs School of Business, a lower DTI is often correlated with a higher likelihood of loan approval and better interest rates.

1.1. How is DTI Calculated?

Calculating DTI involves a simple formula: divide your total monthly debt payments by your gross monthly income.

DTI = (Total Monthly Debt Payments / Gross Monthly Income) x 100

For instance, if your monthly debt payments total $2,000 and your gross monthly income is $6,000, your DTI is 33%.

1.2. Why is DTI Important?

DTI is important because it provides a snapshot of your financial health, influencing your ability to secure loans, mortgages, and other credit. Lenders use DTI to gauge the risk associated with lending you money; a lower DTI suggests you’re less likely to default on your obligations. Additionally, monitoring your DTI can help you make informed decisions about managing your finances and taking on new debt.

1.3. What are the Ideal DTI Ranges?

Ideal DTI ranges vary, but generally:

- 36% or less: Considered excellent, indicating a comfortable balance between debt and income.

- 37% to 43%: Acceptable, but leaves less room for unexpected expenses.

- 44% to 50%: Concerning, suggesting you may be overextended.

- Over 50%: High-risk, indicating significant financial strain.

Maintaining a DTI below 36% is often recommended for financial stability and flexibility.

2. What Payments Are Included in the DTI Calculation?

Understanding what payments to include when calculating your DTI is essential for an accurate assessment. DTI typically includes recurring monthly debt obligations.

2.1. Monthly Housing Costs

Monthly housing costs include rent or mortgage payments, property taxes, homeowner’s insurance, and homeowner association (HOA) fees. These are primary components of your debt obligations related to housing.

2.1.1. Rent Payments

If you’re renting, include your monthly rent payment in your DTI calculation. This is a straightforward debt obligation.

2.1.2. Mortgage Payments

For homeowners, include the principal, interest, property taxes, and insurance (PITI) in your mortgage payment.

2.2. Credit Card Payments

Credit card payments include the minimum payment due on each card. While it’s tempting to only include the minimum, consider including the amount you typically pay to get a clearer picture of your debt management.

2.2.1. Minimum Payments

The minimum payment is the smallest amount you must pay each month to keep your account in good standing. Lenders use this figure in DTI calculations.

2.2.2. Average or Typical Payments

Including the average or typical payment you make each month can provide a more realistic view of your debt obligations, especially if you usually pay more than the minimum.

2.3. Loan Payments

Loan payments include auto loans, student loans, personal loans, and any other installment loans. These are fixed monthly obligations that significantly impact your DTI.

2.3.1. Auto Loans

Include your monthly auto loan payment. This is a common debt obligation for many individuals.

2.3.2. Student Loans

Student loan payments are a significant part of debt for many, especially recent graduates. Be sure to include all student loan payments.

2.3.3. Personal Loans

Personal loans taken for various purposes should also be included in your DTI calculation.

2.4. Child Support and Alimony

If you’re required to pay child support or alimony, these payments must be included in your monthly debt obligations. These are legal obligations that affect your disposable income.

2.5. Other Recurring Debts

Other recurring debts can include payments for items like furniture, medical bills on a payment plan, or any other regular debt payments not covered above.

3. What Expenses Are NOT Included in DTI Calculation?

Knowing which expenses not to include in your DTI calculation is just as important as knowing what to include. Certain everyday expenses aren’t considered debts in the traditional sense.

3.1. Utilities

Utilities such as electricity, water, gas, and internet are not included in DTI calculations. These are considered variable living expenses.

3.2. Groceries

Groceries are another variable expense that isn’t included in DTI. These costs can fluctuate and aren’t considered fixed debt obligations.

3.3. Transportation Costs (excluding auto loans)

While auto loan payments are included, other transportation costs like gas, maintenance, and public transit fares are not.

3.4. Healthcare Costs

Routine healthcare costs, such as doctor visits and prescription medications, are excluded from DTI calculations.

3.5. Insurance Premiums (excluding homeowner’s insurance)

Life insurance, health insurance, and auto insurance premiums (separate from homeowner’s insurance, which is included in mortgage payments) are not included in DTI.

3.6. Entertainment and Recreation

Expenses for entertainment, hobbies, and recreational activities are not included in DTI.

4. How DTI Affects Your Ability to Get Credit

Your DTI significantly impacts your ability to get credit. Lenders use it to assess risk and determine the terms of loans and credit lines.

4.1. Mortgage Approval

For mortgages, a lower DTI increases your chances of approval and can result in better interest rates and terms. Lenders prefer DTIs below 36%.

4.2. Loan Approval

Similarly, for other loans like auto loans or personal loans, a lower DTI improves your approval odds and can lead to more favorable terms.

4.3. Credit Card Approval

When applying for credit cards, a lower DTI signals to issuers that you’re a responsible borrower, making you more likely to be approved with a higher credit limit.

4.4. Interest Rates and Loan Terms

A lower DTI often translates to lower interest rates and better loan terms because you’re seen as a less risky borrower.

4.5. Refinancing Options

When refinancing a mortgage or other loan, a healthy DTI can open up more options and potentially save you money over the life of the loan.

5. Strategies to Improve Your Debt-to-Income Ratio

Improving your DTI involves either decreasing your debt payments, increasing your income, or a combination of both.

5.1. Increase Your Income

Increasing your income directly lowers your DTI. Consider strategies such as seeking a raise, taking on a side hustle, or starting a business.

5.1.1. Negotiate a Raise

Negotiating a raise at your current job can increase your monthly income, thus lowering your DTI.

5.1.2. Take on a Side Hustle

A side hustle, like freelancing, consulting, or driving for a rideshare service, can supplement your income and improve your DTI. Income-partners.net can help you find lucrative side hustles and partnership opportunities to further boost your earnings.

5.1.3. Start a Business

Starting a business can significantly increase your income potential, although it may take time to become profitable.

5.2. Reduce Your Debt

Reducing your debt lowers your monthly debt payments, directly impacting your DTI. Strategies include the debt snowball and debt avalanche methods.

5.2.1. Debt Snowball Method

The debt snowball method involves paying off your smallest debts first, regardless of interest rate, to gain momentum and motivation.

5.2.2. Debt Avalanche Method

The debt avalanche method focuses on paying off debts with the highest interest rates first, which can save you more money in the long run.

5.2.3. Balance Transfer

Transferring high-interest credit card balances to a card with a lower interest rate can reduce your monthly payments and save you money on interest.

5.2.4. Debt Consolidation

Debt consolidation involves taking out a new loan to pay off multiple existing debts, ideally at a lower interest rate, simplifying your payments and potentially lowering your DTI.

5.3. Refinance Existing Loans

Refinancing loans, such as mortgages or student loans, can lower your interest rate and monthly payments, thereby improving your DTI.

5.3.1. Mortgage Refinancing

Refinancing your mortgage can result in lower monthly payments if you secure a better interest rate or extend the loan term.

5.3.2. Student Loan Refinancing

Refinancing student loans can also lower your interest rate and monthly payments, particularly if your credit score has improved since you took out the loans.

5.4. Avoid Taking on New Debt

Avoiding new debt, especially unnecessary purchases on credit, can prevent your DTI from increasing.

5.5. Budgeting and Expense Tracking

Creating a budget and tracking your expenses helps you identify areas where you can cut back, freeing up more money to pay down debt or save.

6. DTI for Business Owners and Entrepreneurs

For business owners and entrepreneurs, DTI is just as critical, influencing their ability to secure business loans and investments.

6.1. Personal vs. Business DTI

Business owners need to consider both their personal and business DTI. Lenders often evaluate both to assess overall financial health.

6.2. How Business Debt Affects Personal DTI

If you’ve personally guaranteed business debts, these obligations are included in your personal DTI calculation.

6.3. Strategies for Managing Business and Personal Debt

Managing business and personal debt requires careful planning and financial discipline. Strategies include keeping business and personal finances separate and regularly reviewing financial statements.

6.4. Seeking Partnerships to Improve Business Finances

Seeking strategic partnerships can improve business finances by bringing in additional revenue and resources, indirectly improving your overall financial health and DTI. Income-partners.net offers numerous opportunities to find such partnerships.

7. Common Mistakes to Avoid When Calculating DTI

Avoiding common mistakes when calculating your DTI ensures an accurate assessment of your financial situation.

7.1. Including Net Income Instead of Gross Income

Always use gross monthly income (before taxes and deductions) rather than net income when calculating your DTI.

7.2. Forgetting to Include All Debt Payments

Make sure to include all recurring debt payments, no matter how small, for an accurate DTI calculation.

7.3. Using Inconsistent Data

Use consistent and up-to-date data for both income and debt to avoid inaccuracies.

7.4. Ignoring Variable Income

If your income varies, calculate an average monthly income over several months to get a more accurate picture.

7.5. Not Factoring in Future Expenses

Consider any upcoming expenses or changes in income that could affect your DTI in the future.

8. Tools and Resources for Calculating and Managing DTI

Several tools and resources can help you calculate and manage your DTI effectively.

8.1. Online DTI Calculators

Numerous online DTI calculators can quickly estimate your DTI. These tools require you to input your income and debt information.

8.2. Budgeting Apps

Budgeting apps like Mint, YNAB (You Need a Budget), and Personal Capital can help you track your income, expenses, and debt, making it easier to manage your DTI.

8.3. Financial Advisors

Consulting with a financial advisor can provide personalized guidance on managing your debt and improving your DTI.

8.4. Credit Counseling Services

Credit counseling services offer assistance with debt management, budgeting, and improving your overall financial health.

9. Real-Life Examples of DTI Impact

Looking at real-life examples can illustrate how DTI impacts financial situations and decisions.

9.1. Case Study 1: First-Time Homebuyer

A first-time homebuyer with a DTI of 40% may struggle to get approved for a mortgage or may face higher interest rates.

9.2. Case Study 2: Small Business Loan

A small business owner with a high personal DTI may find it challenging to secure a business loan, as lenders view them as a higher risk.

9.3. Case Study 3: Debt Consolidation Success

An individual who successfully consolidated their debts and lowered their DTI was able to save money on interest and improve their credit score.

10. The Future of DTI in Financial Planning

DTI will likely remain a critical metric in financial planning, with potential changes in how it’s evaluated and used by lenders.

10.1. Potential Changes in Lending Practices

Lending practices may evolve to incorporate more sophisticated methods of assessing risk, but DTI will likely remain a key factor.

10.2. The Role of Technology in DTI Management

Technology and financial apps will continue to play a significant role in helping individuals and businesses manage their DTI effectively.

10.3. Adapting to Economic Changes

Adapting to economic changes, such as interest rate fluctuations and income shifts, is crucial for maintaining a healthy DTI.

In conclusion, understanding what is included in a debt-to-income ratio is vital for maintaining financial health and securing favorable credit terms. By accurately calculating your DTI, managing your debt, and seeking opportunities to increase your income, you can improve your financial standing and achieve your goals. Don’t forget to explore income-partners.net for valuable partnership opportunities and strategies to boost your income and optimize your financial future.

Ready to take control of your financial future? Visit income-partners.net today to discover partnership opportunities, learn effective relationship-building strategies, and connect with potential partners in the USA. Don’t miss out on the chance to transform your income and achieve lasting financial success. Contact us at Address: 1 University Station, Austin, TX 78712, United States. Phone: +1 (512) 471-3434 or visit our website income-partners.net.

FAQ: Understanding Debt-to-Income Ratio

1. What exactly does debt-to-income ratio (DTI) measure?

Debt-to-income ratio (DTI) measures the percentage of your gross monthly income that goes towards paying your monthly debt obligations. It indicates how much of your income is used to cover debts versus how much is available for other expenses.

2. How do I calculate my debt-to-income ratio?

To calculate your DTI, divide your total monthly debt payments by your gross monthly income (before taxes and deductions) and multiply by 100 to get a percentage.

3. What is considered a good debt-to-income ratio?

A good DTI is generally considered to be 36% or less. A DTI between 37% and 43% is acceptable but leaves less room for financial flexibility. A DTI of 44% to 50% is concerning, and anything over 50% is considered high-risk.

4. Which debt payments should I include when calculating my DTI?

Include monthly rent or mortgage payments, credit card payments (minimum amount due), auto loans, student loans, personal loans, child support, alimony, and any other recurring debt payments.

5. What expenses are not included in the debt-to-income ratio calculation?

Expenses not included in DTI are utilities, groceries, transportation costs (excluding auto loans), healthcare costs, insurance premiums (excluding homeowner’s insurance), and entertainment expenses.

6. How does my debt-to-income ratio affect my ability to get a loan or mortgage?

Lenders use your DTI to assess your ability to repay a loan. A lower DTI indicates lower risk, making you more likely to be approved for a loan or mortgage with better interest rates and terms.

7. Can I improve my debt-to-income ratio? If so, how?

Yes, you can improve your DTI by either increasing your income, reducing your debt, or a combination of both. Strategies include negotiating a raise, taking on a side hustle, paying off debt using the snowball or avalanche method, and refinancing loans.

8. How does personal debt impact my business’s ability to secure financing?

If you’ve personally guaranteed business debts, these obligations are included in your personal DTI calculation. Lenders often evaluate both your personal and business finances to assess overall risk.

9. What are some common mistakes to avoid when calculating DTI?

Common mistakes include using net income instead of gross income, forgetting to include all debt payments, using inconsistent data, ignoring variable income, and not factoring in future expenses.

10. Where can I find tools and resources to help me calculate and manage my DTI?

You can find online DTI calculators, budgeting apps, and financial advisors to help you calculate and manage your DTI. Credit counseling services can also provide assistance with debt management and budgeting.