Corporate income tax is a crucial aspect of business finance that impacts profitability and investment. At income-partners.net, we help businesses understand these complexities and connect them with strategic partners to optimize their financial strategies. This article explores what corporate income tax is, how it affects businesses, and strategies to manage it effectively, ultimately boosting your income and fostering successful partnerships. We’ll also explore how strategic alliances can lead to tax-efficient growth.

1. Understanding Corporate Income Tax: A Comprehensive Guide

Is corporate income tax something that’s been on your mind? Yes, corporate income tax (CIT) is a tax levied on the profits of C corporations by federal and state governments. This tax impacts a company’s net income and influences investment decisions. This guide breaks down the complexities of CIT, offering clear insights for businesses seeking to thrive in today’s economic landscape.

1.1. What Exactly Is Corporate Income Tax?

Corporate income tax (CIT) is a direct tax imposed on the profits a corporation makes during a specific period, usually a financial year. It’s a significant source of revenue for both federal and state governments, used to fund public services and infrastructure. However, it’s essential to note that not all businesses are subject to CIT; many operate as pass-through entities.

1.2. Pass-Through Entities vs. C Corporations

Pass-through entities, such as partnerships, S corporations, LLCs, and sole proprietorships, don’t pay CIT at the corporate level. Instead, their profits are “passed through” to the owners, who then report the income on their individual income tax returns. This structure can offer tax advantages, especially for smaller businesses. On the other hand, C corporations are subject to CIT, which can impact their overall profitability.

1.3. The Significance of Understanding CIT

Understanding CIT is crucial for several reasons. It allows businesses to:

- Make informed financial decisions: Knowing the tax implications of business activities helps in planning and resource allocation.

- Optimize tax strategies: Strategic tax planning can reduce the tax burden and improve cash flow.

- Comply with tax laws: Understanding CIT requirements ensures compliance and avoids penalties.

- Attract investors: A clear understanding of CIT demonstrates financial responsibility and transparency, attracting potential investors.

1.4. How CIT Impacts Business Decisions

CIT can influence a wide range of business decisions, including:

- Investment: CIT affects the profitability of investments, influencing whether a company decides to invest in new projects or assets.

- Financing: The tax deductibility of interest expenses can impact a company’s choice of financing methods.

- Location: State-level CIT rates can influence where a company chooses to locate its operations.

- Compensation: CIT can affect decisions about employee compensation and benefits.

2. Decoding Corporate Tax Rates: Federal, State, and Global Perspectives

Concerned about keeping up with corporate tax rates? The corporate tax rate is a percentage of a company’s profits that it must pay in taxes. These rates vary significantly across federal, state, and international jurisdictions, impacting business profitability and strategic decision-making. Here’s a breakdown of corporate tax rates:

2.1. Federal Corporate Tax Rate in the United States

The federal corporate tax rate in the United States is currently a flat 21%, as established by the Tax Cuts and Jobs Act (TCJA) of 2017. This rate applies to all C corporations, regardless of their income level. Before the TCJA, the federal corporate tax rate was 35%, which was one of the highest among developed countries. The reduction aimed to make U.S. businesses more competitive globally.

According to research from the University of Texas at Austin’s McCombs School of Business, in July 2025, the 21% federal corporate tax rate has spurred increased investment and job growth due to enhanced corporate profitability.

2.2. State Corporate Tax Rates: A Varied Landscape

State corporate income tax rates vary widely. Some states, like Nevada, Ohio, South Dakota, Texas, Washington, and Wyoming, levy no corporate income tax, offering a significant advantage for businesses operating within their borders. Other states, however, do tax corporate profits, with rates ranging from a few percentage points to over 10%. For example, as of 2024:

- New Jersey: 9% (highest in the nation)

- Pennsylvania: 8.99%

- Iowa: 8.4%

- Minnesota: 9.8%

- Alaska: 9.4%

These variations can influence a company’s decision on where to establish or expand its operations.

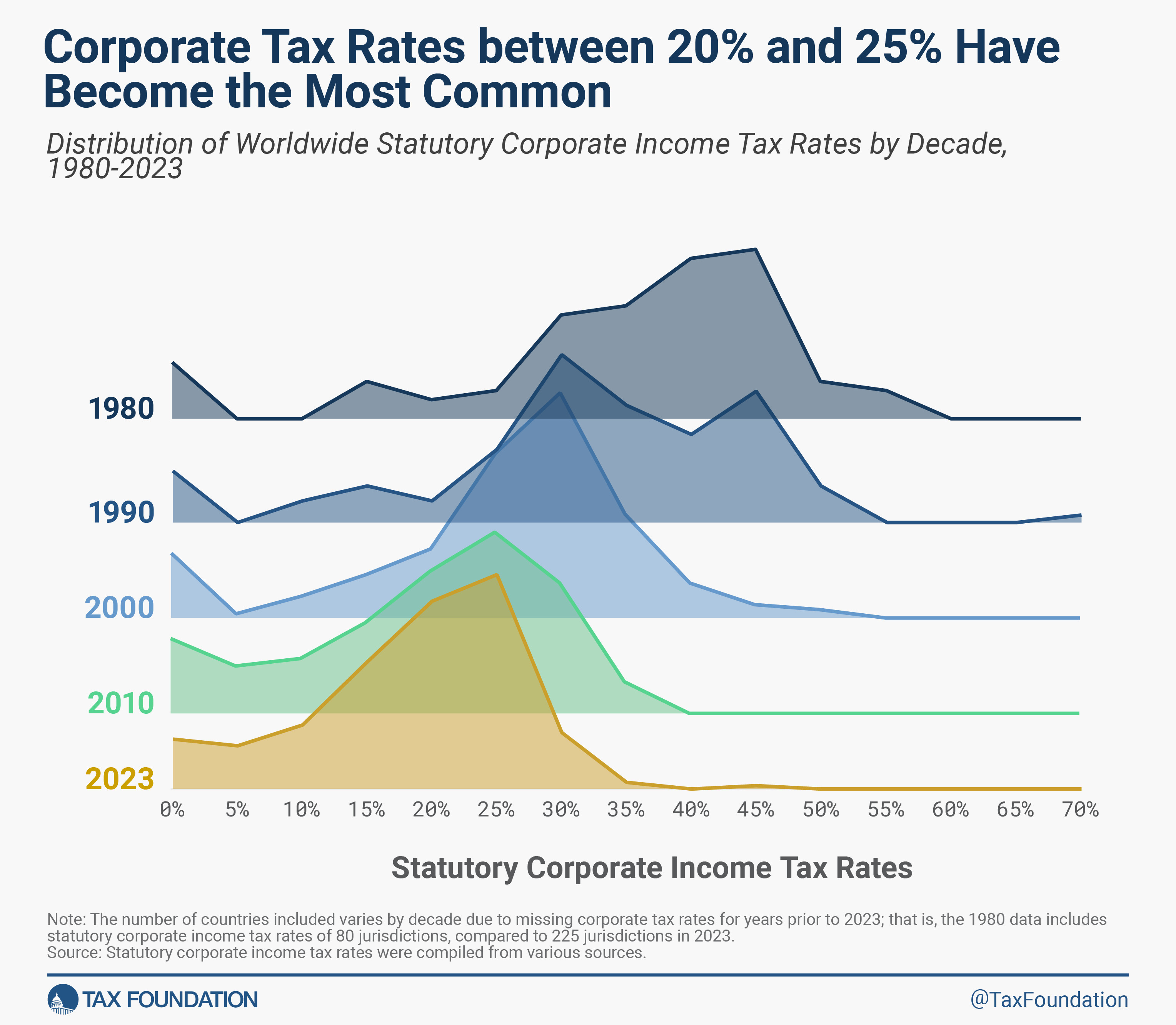

State corporate income tax rates have a wide range

State corporate income tax rates have a wide range

2.3. The Combined Impact: State and Federal Rates

The combined state and federal corporate income tax rate is the sum of the federal rate (21%) and the state rate. For example, a corporation operating in New Jersey would face a combined rate of 30% (21% federal + 9% state). This combined rate is what truly impacts a business’s bottom line.

2.4. International Corporate Tax Rates: A Global Perspective

Corporate tax rates vary significantly around the world. Some countries have very low rates to attract foreign investment, while others have higher rates to fund extensive social programs. As of 2024, some notable international corporate tax rates include:

- Ireland: 12.5%

- Singapore: 17%

- United Kingdom: 19%

- Canada: 15% (federal), with additional provincial rates

- France: 25%

- Germany: Approximately 30% (including trade tax and surcharge)

These international variations can influence multinational corporations’ decisions on where to locate their headquarters, manufacturing facilities, and other operations.

2.5. The Influence of Tax Rates on Business Strategy

Corporate tax rates significantly influence business strategy in several ways:

- Location Decisions: Companies may choose to locate or relocate their operations to jurisdictions with lower tax rates.

- Investment Decisions: Tax rates impact the after-tax return on investment, influencing whether a company decides to invest in new projects or assets.

- Financing Decisions: The tax deductibility of interest expenses can impact a company’s choice of financing methods.

- Transfer Pricing: Multinational corporations may use transfer pricing strategies to shift profits to lower-tax jurisdictions.

- Mergers and Acquisitions: Tax considerations often play a significant role in mergers and acquisitions, with companies seeking to take advantage of tax benefits or reduce their overall tax burden.

3. Navigating the Corporate Tax Base: What Counts as Taxable Income?

Do you need a better understanding of taxable income? The corporate tax base is the amount of profit a company earns that is subject to corporate income tax. It’s calculated by subtracting allowable deductions from a company’s revenues. Knowing what constitutes taxable income and how to calculate it is vital for accurate tax planning and compliance.

3.1. Defining the Corporate Tax Base

The corporate tax base is generally defined as a business’s profits, which are revenues (what a business makes in sales) minus costs (the cost of doing business). However, the calculation of taxable income can be complex, with various rules and regulations governing what can be deducted.

3.2. Revenue: The Starting Point

Revenue is the total amount of money a company receives from its business activities. This includes sales of goods or services, as well as any other income generated by the company. It’s the starting point for calculating the corporate tax base.

3.3. Deductible Expenses: Reducing Taxable Income

Deductible expenses are costs that a company can subtract from its revenue to reduce its taxable income. Common deductible expenses include:

- Cost of Goods Sold (COGS): The direct costs of producing goods or services.

- Salaries and Wages: Compensation paid to employees.

- Rent: Payments for office or factory space.

- Utilities: Costs for electricity, gas, water, and other utilities.

- Advertising: Expenses for marketing and promoting the business.

- Depreciation: The gradual expensing of an asset’s cost over its useful life.

- Interest: Payments on business loans.

- Business Travel: Expenses for travel related to business activities.

3.4. Capital Investments and Depreciation

Costs of capital investments—such as equipment, machinery, and buildings—cannot be fully deducted when they are incurred. Instead, they must be deducted over an extended period of time through depreciation. This inflates a business’s taxable income in the short term and thus increases the cost of capital. Depreciation methods, such as straight-line or accelerated depreciation, can impact the amount of depreciation expense recognized each year.

3.5. Inventory Valuation: Impacting Taxable Income

Inventory valuation methods, such as First-In, First-Out (FIFO) and Last-In, First-Out (LIFO), can also impact a business’s tax base. FIFO assumes that the first items purchased are the first ones sold, while LIFO assumes that the last items purchased are the first ones sold. The choice of inventory valuation method can affect the cost of goods sold and, therefore, the taxable income.

3.6. Net Operating Losses: Carryforwards and Carrybacks

Net operating losses (NOLs) occur when a business’s deductible expenses exceed its revenue. Businesses can carry forward or carry back NOLs to offset taxable income in other years. Carryforwards allow a business to use the NOL to reduce taxable income in future years, while carrybacks allow a business to use the NOL to reduce taxable income in prior years. The rules governing NOL carryforwards and carrybacks have changed over time, impacting how businesses can use them to manage their tax liability.

3.7. Tax Credits: Direct Reductions in Tax Liability

Tax credits are direct reductions in a company’s tax liability. They are often used to incentivize specific behaviors, such as investing in renewable energy or hiring veterans. Common tax credits for businesses include:

- Research and Development (R&D) Tax Credit: For companies that invest in research and development activities.

- Work Opportunity Tax Credit (WOTC): For companies that hire individuals from certain target groups.

- Renewable Energy Tax Credits: For companies that invest in renewable energy projects.

3.8. Strategic Tax Planning: Optimizing the Tax Base

Strategic tax planning involves using various legal strategies to minimize a company’s tax liability. This includes:

- Choosing the right business structure: Selecting the most tax-efficient business structure (e.g., S corporation vs. C corporation).

- Maximizing deductions: Taking advantage of all available deductions to reduce taxable income.

- Utilizing tax credits: Claiming all eligible tax credits to reduce tax liability.

- Deferring income: Delaying the recognition of income to a later year when tax rates may be lower.

- Accelerating deductions: Accelerating the recognition of deductions to an earlier year when tax rates may be higher.

4. Who Really Pays Corporate Income Tax? Unpacking the Burden

Ever wondered who truly bears the burden of corporate income tax? While C corporations are legally required to pay corporate income tax, the economic burden of the tax falls not only on the business itself but also on its consumers and employees through higher prices and lower wages. Understanding this distribution is key to grasping the broader economic effects of CIT.

4.1. The Legal Obligation: C Corporations

C corporations are legally obligated to pay corporate income tax on their profits. This is a direct tax levied on the corporation itself, and the corporation is responsible for calculating and paying the tax. However, the economic burden of the tax is not always borne solely by the corporation.

4.2. The Economic Burden: A Broader Perspective

The economic burden of the corporate income tax is distributed among various stakeholders, including:

- Shareholders: Corporate income tax reduces the profits available to shareholders, either through lower dividends or reduced stock prices.

- Employees: Companies may respond to higher corporate income taxes by reducing wages or benefits, shifting some of the tax burden onto employees.

- Consumers: Companies may pass on higher corporate income taxes to consumers through higher prices for goods and services.

4.3. Impact on Shareholders: Reduced Returns

Corporate income tax reduces the after-tax profits available to shareholders. This can result in lower dividends, as the company has less cash to distribute to shareholders. It can also lead to reduced stock prices, as investors may be less willing to invest in companies that are subject to high corporate income taxes.

4.4. Impact on Employees: Lower Wages and Benefits

Companies may respond to higher corporate income taxes by reducing wages or benefits for employees. This is because higher taxes reduce the company’s overall profitability, and companies may seek to offset this by reducing labor costs. This can result in lower wages, reduced benefits, or even job losses.

4.5. Impact on Consumers: Higher Prices

Companies may pass on higher corporate income taxes to consumers through higher prices for goods and services. This is because higher taxes increase the company’s costs, and companies may seek to recover these costs by increasing prices. This can result in consumers paying more for the goods and services they purchase.

4.6. Pass-Through Entities: A Different Burden

Pass-through entities, such as partnerships, S corporations, LLCs, and sole proprietorships, do not pay corporate income tax at the corporate level. Instead, their profits are “passed through” to the owners, who then report the income on their individual income tax returns. This means that the economic burden of the tax falls directly on the owners of the business.

4.7. The Debate: Who Ultimately Bears the Burden?

There is ongoing debate among economists about who ultimately bears the burden of the corporate income tax. Some argue that it primarily falls on shareholders, while others argue that it primarily falls on employees or consumers. The actual distribution likely depends on a variety of factors, including the industry, the competitiveness of the market, and the elasticity of supply and demand.

Reducing corporate income tax rates is an efficient way to grow the economy

Reducing corporate income tax rates is an efficient way to grow the economy

4.8. Policy Implications: Tax Reform and Economic Growth

Understanding who bears the burden of the corporate income tax is crucial for policymakers considering tax reform. Changes to the corporate income tax rate can have significant impacts on shareholders, employees, and consumers, as well as on overall economic growth. Some argue that reducing the corporate income tax rate can stimulate economic growth by increasing corporate profitability and investment.

5. The Role of Corporate Tax Revenue in the Economy

Curious about where corporate tax money goes? Corporate tax revenue is a significant source of funding for government services and infrastructure. However, its share of total tax revenue has been declining over the years. Understanding the role of corporate tax revenue in the economy provides insights into government finances and economic policy.

5.1. Corporate Tax Revenue: A Source of Government Funding

Corporate tax revenue is a significant source of funding for federal, state, and local governments. This revenue is used to fund a wide range of public services, including:

- Education: Funding for schools, colleges, and universities.

- Infrastructure: Building and maintaining roads, bridges, and other infrastructure.

- Healthcare: Funding for public health programs and healthcare services.

- National Defense: Funding for the military and national security.

- Social Security: Funding for retirement and disability benefits.

- Other Government Services: Funding for various other government services, such as law enforcement, environmental protection, and social welfare programs.

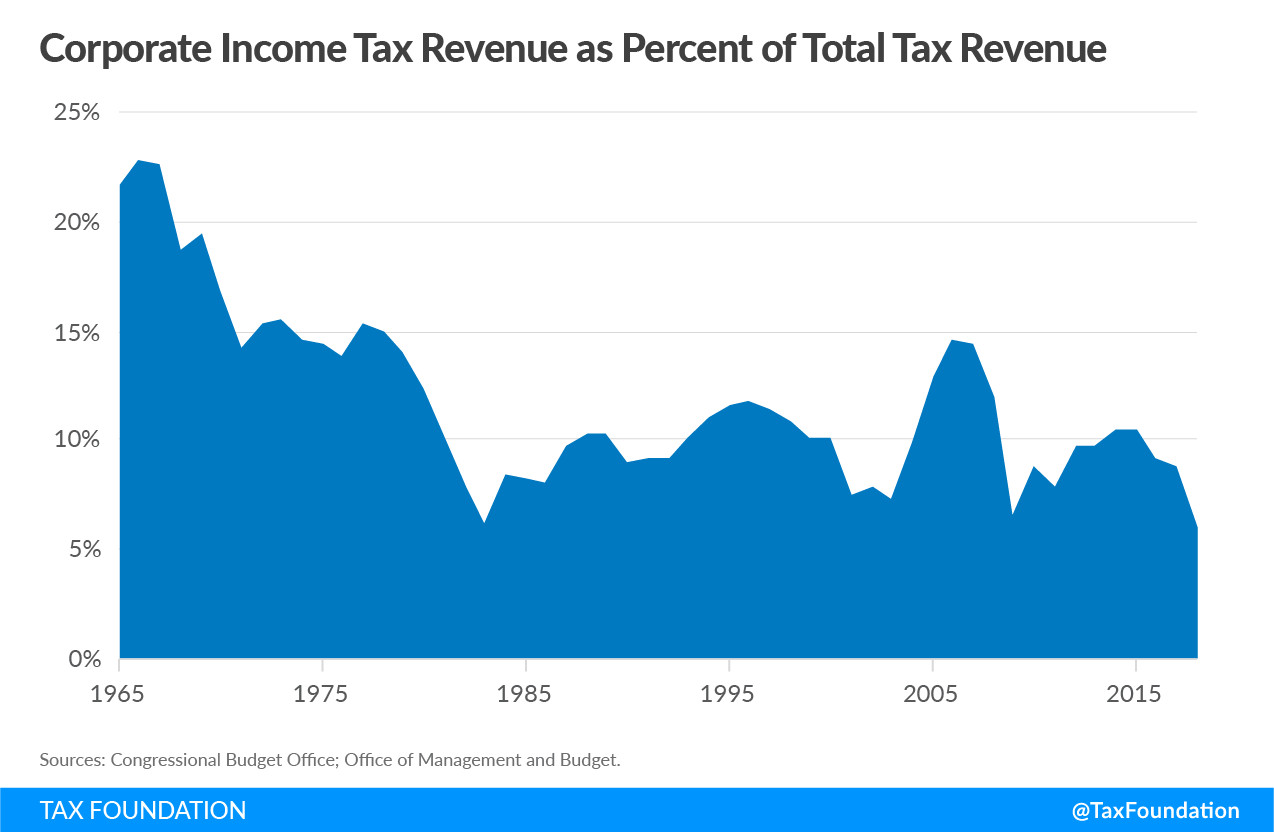

5.2. Declining Share of Total Tax Revenue

Over the last 50 years, corporate tax revenue as a percentage of total tax revenue has been declining. This is partly because C corporations tend to be taxed more heavily than pass-through businesses, which has led to a decline in C corporations and an increase in pass-through businesses. Other factors contributing to the decline include changes in tax laws, increased tax avoidance, and shifts in the economy.

5.3. The Rise of Pass-Through Entities

Pass-through entities, such as partnerships, S corporations, LLCs, and sole proprietorships, have become increasingly popular over the years. This is partly because they offer tax advantages compared to C corporations. Pass-through entities are not subject to corporate income tax at the corporate level; instead, their profits are “passed through” to the owners, who then report the income on their individual income tax returns. This can result in lower overall tax liability, especially for smaller businesses.

5.4. Impact of Tax Law Changes

Changes in tax laws have also contributed to the decline in corporate tax revenue. For example, the Tax Cuts and Jobs Act (TCJA) of 2017 reduced the federal corporate tax rate from 35% to 21%. This significantly reduced the amount of corporate tax revenue collected by the federal government.

5.5. Tax Avoidance Strategies

Companies may use various tax avoidance strategies to reduce their corporate income tax liability. These strategies can include:

- Transfer Pricing: Shifting profits to lower-tax jurisdictions through transfer pricing arrangements.

- Tax Havens: Locating operations in tax havens, which are countries or jurisdictions with low or no corporate income taxes.

- Debt Shifting: Shifting debt to higher-tax jurisdictions to deduct interest expenses.

- Inversions: Merging with a foreign company and relocating the corporate headquarters to a lower-tax jurisdiction.

5.6. Economic Implications

The decline in corporate tax revenue has several economic implications. It reduces the amount of funding available for government services, which may lead to cuts in spending or increases in other taxes. It also affects the distribution of the tax burden, with a greater share of the burden falling on individuals and other types of businesses.

5.7. The Debate: Should Corporate Taxes Be Increased?

There is ongoing debate among policymakers and economists about whether corporate taxes should be increased. Some argue that increasing corporate taxes would provide more funding for government services and reduce income inequality. Others argue that increasing corporate taxes would harm economic growth by reducing corporate profitability and investment.

Corporate income tax revenue

Corporate income tax revenue

5.8. Alternative Revenue Sources

Given the declining share of corporate tax revenue, governments may need to explore alternative revenue sources to fund public services. These sources can include:

- Individual Income Taxes: Increasing individual income tax rates or broadening the tax base.

- Sales Taxes: Increasing sales tax rates or expanding the types of goods and services subject to sales tax.

- Property Taxes: Increasing property tax rates or reassessing property values.

- Excise Taxes: Imposing excise taxes on specific goods or services, such as alcohol, tobacco, or gasoline.

- Carbon Taxes: Imposing taxes on carbon emissions to address climate change.

6. Maximizing Profitability Through Strategic Partnerships

Do you want to maximize profitability? Strategic partnerships can offer businesses unique opportunities to optimize their operations, reduce costs, and increase revenue, all of which can positively impact their corporate tax liability. By working with the right partners, companies can achieve tax-efficient growth and enhance their overall financial performance.

6.1. Identifying Synergistic Partners

The first step in maximizing profitability through strategic partnerships is identifying the right partners. Look for companies that offer complementary products or services, have a strong market presence, or possess unique capabilities that can benefit your business. Synergistic partnerships can create new revenue streams, reduce costs, and improve overall efficiency.

6.2. Cost Reduction Through Shared Resources

One of the key benefits of strategic partnerships is the ability to share resources and reduce costs. This can include sharing office space, equipment, technology, or personnel. By pooling resources, companies can achieve economies of scale and reduce their overall expenses, leading to higher profitability and lower tax liability.

6.3. Revenue Enhancement Through Joint Ventures

Joint ventures are a type of strategic partnership in which two or more companies pool their resources to undertake a specific project or business activity. Joint ventures can be a powerful way to increase revenue by entering new markets, developing new products or services, or expanding into new geographic areas. The increased revenue can lead to higher profitability and a greater ability to manage corporate tax obligations.

6.4. Tax Planning in Partnership Agreements

When forming a strategic partnership, it’s crucial to consider the tax implications of the arrangement. The partnership agreement should clearly outline how profits and losses will be allocated among the partners and how tax liabilities will be handled. Proper tax planning can help minimize the overall tax burden and ensure that each partner is in compliance with tax laws.

6.5. Leveraging Tax Credits and Incentives

Strategic partnerships can also provide opportunities to leverage tax credits and incentives that may not be available to individual companies. For example, a partnership may be able to qualify for research and development tax credits, renewable energy tax credits, or other incentives that can reduce its overall tax liability.

6.6. Transfer Pricing Considerations

In international strategic partnerships, transfer pricing can be a significant consideration. Transfer pricing refers to the pricing of goods, services, and intangible assets between related parties, such as subsidiaries of a multinational corporation. Companies must ensure that their transfer pricing policies are compliant with tax laws to avoid penalties and maintain a positive relationship with tax authorities.

6.7. Compliance and Reporting

Strategic partnerships must comply with all applicable tax laws and regulations. This includes accurately reporting income and expenses, filing tax returns on time, and maintaining proper documentation. Non-compliance with tax laws can result in penalties, interest charges, and other sanctions.

6.8. The Role of Income-Partners.Net

Income-partners.net can play a vital role in helping businesses maximize profitability through strategic partnerships. We offer a platform for businesses to connect with potential partners, explore collaboration opportunities, and access resources and expertise to support their partnership efforts. Our goal is to help businesses find the right partners to achieve tax-efficient growth and enhance their overall financial performance.

Looking for the right strategic partner? At income-partners.net, we connect businesses with opportunities for collaboration and growth, helping you navigate the complexities of corporate income tax while maximizing your profitability. Visit our website today to explore potential partnerships and discover how we can help you achieve tax-efficient success. Address: 1 University Station, Austin, TX 78712, United States. Phone: +1 (512) 471-3434. Website: income-partners.net.

7. Strategies for Effective Corporate Tax Management

Are you seeking ways to manage your corporate tax effectively? Effective corporate tax management involves implementing strategies to minimize tax liability while remaining compliant with tax laws. These strategies can include tax planning, taking advantage of deductions and credits, and optimizing business structure.

7.1. Proactive Tax Planning

Proactive tax planning is the cornerstone of effective corporate tax management. This involves anticipating tax liabilities and implementing strategies to minimize them before the end of the tax year. Proactive tax planning can help businesses avoid surprises and make informed financial decisions.

7.2. Maximizing Deductions and Credits

One of the most effective ways to reduce corporate tax liability is to maximize deductions and credits. This involves taking advantage of all available deductions for expenses such as salaries, rent, utilities, and depreciation. It also involves claiming all eligible tax credits, such as the research and development tax credit and the work opportunity tax credit.

7.3. Optimizing Business Structure

The choice of business structure can have a significant impact on corporate tax liability. S corporations and LLCs offer pass-through taxation, while C corporations are subject to corporate income tax. Businesses should carefully consider their options and choose the structure that is most tax-efficient for their specific circumstances.

7.4. Timing of Income and Expenses

The timing of income and expenses can also impact corporate tax liability. Businesses may be able to defer income to a later year when tax rates may be lower or accelerate deductions to an earlier year when tax rates may be higher. Proper timing of income and expenses can help businesses minimize their overall tax burden.

7.5. Transfer Pricing Strategies

Multinational corporations can use transfer pricing strategies to shift profits to lower-tax jurisdictions. This involves setting the prices for goods, services, and intangible assets transferred between related parties in a way that minimizes overall tax liability. However, transfer pricing must be carefully managed to comply with tax laws and avoid penalties.

7.6. International Tax Planning

International tax planning involves structuring international operations to minimize corporate tax liability. This can include locating operations in tax havens, using tax treaties to reduce withholding taxes, and optimizing the use of foreign tax credits. International tax planning can be complex, and businesses should seek expert advice to ensure compliance with tax laws.

7.7. Compliance and Risk Management

Compliance with tax laws is essential for effective corporate tax management. Businesses must accurately report income and expenses, file tax returns on time, and maintain proper documentation. Failure to comply with tax laws can result in penalties, interest charges, and other sanctions.

7.8. The Role of Tax Professionals

Tax professionals can play a vital role in helping businesses manage their corporate tax liability. They can provide expert advice on tax planning, compliance, and risk management. Tax professionals can also help businesses navigate the complexities of tax laws and regulations.

8. Common Mistakes to Avoid in Corporate Tax Management

Want to steer clear of costly errors? Avoiding common mistakes in corporate tax management is crucial for maintaining compliance and minimizing tax liability. These mistakes can range from improper record-keeping to failing to take advantage of available deductions and credits.

8.1. Inadequate Record-Keeping

Inadequate record-keeping is one of the most common mistakes in corporate tax management. Businesses must maintain accurate and complete records of all income and expenses to support their tax filings. Failure to do so can result in penalties and interest charges.

8.2. Missing Deductions and Credits

Many businesses fail to take advantage of all available deductions and credits, resulting in higher tax liability. Businesses should carefully review their expenses and activities to identify all deductions and credits for which they are eligible.

8.3. Improper Classification of Expenses

Improper classification of expenses can also lead to mistakes in corporate tax management. Businesses must properly classify expenses as either deductible or non-deductible. Improper classification can result in overstating deductions and understating tax liability.

8.4. Failure to Comply with Tax Laws

Failure to comply with tax laws is a serious mistake that can result in penalties, interest charges, and other sanctions. Businesses must stay up-to-date on tax laws and regulations and ensure that they are in compliance.

8.5. Neglecting Transfer Pricing Rules

Multinational corporations must comply with transfer pricing rules when setting the prices for goods, services, and intangible assets transferred between related parties. Neglecting transfer pricing rules can result in penalties and adjustments to taxable income.

8.6. Ignoring State and Local Taxes

Many businesses focus primarily on federal taxes and neglect state and local taxes. State and local taxes can be significant, and businesses must comply with all applicable state and local tax laws.

8.7. Waiting Until the Last Minute

Waiting until the last minute to prepare tax filings is a common mistake that can result in errors and missed deadlines. Businesses should start preparing their tax filings well in advance of the due date to ensure accuracy and compliance.

8.8. Not Seeking Professional Advice

Many businesses try to manage their corporate tax liability without seeking professional advice. This can be a costly mistake, as tax laws are complex and constantly changing. Businesses should seek advice from qualified tax professionals to ensure that they are in compliance and minimizing their tax liability.

9. Staying Updated on Corporate Tax Law Changes

Do you need to keep up with the latest tax laws? Corporate tax laws are constantly changing, and businesses must stay updated to remain compliant and minimize their tax liability. Monitoring legislative changes, court decisions, and IRS guidance is essential for effective corporate tax management.

9.1. Monitoring Legislative Changes

Legislative changes can have a significant impact on corporate tax laws. Businesses should monitor legislative activity at the federal and state levels to stay informed about potential changes that could affect their tax liability.

9.2. Tracking Court Decisions

Court decisions can also impact corporate tax laws. Businesses should track court decisions to understand how tax laws are being interpreted and applied. Court decisions can provide valuable guidance on tax planning and compliance.

9.3. Reviewing IRS Guidance

The IRS issues guidance on various tax matters, including corporate income tax. Businesses should review IRS guidance to stay informed about the IRS’s interpretation of tax laws and regulations. IRS guidance can include revenue rulings, revenue procedures, notices, and other publications.

9.4. Subscribing to Tax Newsletters and Alerts

Subscribing to tax newsletters and alerts is a great way to stay updated on corporate tax law changes. Many tax professionals and organizations offer newsletters and alerts that provide timely updates on legislative changes, court decisions, IRS guidance, and other tax-related news.

9.5. Attending Tax Seminars and Conferences

Attending tax seminars and conferences is another way to stay updated on corporate tax law changes. These events provide opportunities to learn from tax experts, network with other professionals, and gain insights into the latest developments in corporate tax.

9.6. Engaging with Tax Professionals

Engaging with tax professionals is essential for staying updated on corporate tax law changes. Tax professionals can provide expert advice on tax planning, compliance, and risk management. They can also help businesses navigate the complexities of tax laws and regulations.

9.7. Utilizing Online Resources

Numerous online resources can help businesses stay updated on corporate tax law changes. These resources include the IRS website, tax publications, and online tax services. Businesses should utilize these resources to stay informed and compliant.

9.8. The Importance of Continuous Learning

Staying updated on corporate tax law changes is an ongoing process that requires continuous learning. Businesses must invest in training and education to ensure that their employees are knowledgeable about tax laws and regulations. Continuous learning is essential for effective corporate tax management.

10. Frequently Asked Questions (FAQs) About Corporate Income Tax

Still have questions? Here are some frequently asked questions (FAQs) about corporate income tax to help clarify common concerns and provide valuable insights.

10.1. What is the difference between corporate income tax and individual income tax?

Corporate income tax is levied on the profits of corporations, while individual income tax is levied on the income of individuals. Corporations pay tax on their profits at the corporate level, while individuals pay tax on their income at the individual level.

10.2. What is the current federal corporate tax rate in the United States?

The current federal corporate tax rate in the United States is 21%, as established by the Tax Cuts and Jobs Act (TCJA) of 2017.

10.3. What are pass-through entities, and how are they taxed?

Pass-through entities, such as partnerships, S corporations, LLCs, and sole proprietorships, are not subject to corporate income tax at the corporate level. Instead, their profits are “passed through” to the owners, who then report the income on their individual income tax returns.

10.4. What are deductible expenses for corporate income tax purposes?

Deductible expenses are costs that a company can subtract from its revenue to reduce its taxable income. Common deductible expenses include the cost of goods sold, salaries and wages, rent, utilities, advertising, depreciation, and interest.

10.5. What are tax credits, and how do they reduce corporate tax liability?

Tax credits are direct reductions in a company’s tax liability. They are often used to incentivize specific behaviors, such as investing in research and development or hiring veterans.

10.6. How do net operating losses (NOLs) impact corporate income tax?

Net operating losses (NOLs) occur when a business’s deductible expenses exceed its revenue. Businesses can carry forward or carry back NOLs to offset taxable income in other years.

10.7. What is transfer pricing, and why is it important for multinational corporations?

Transfer pricing refers to the pricing of goods, services, and intangible assets between related parties, such as subsidiaries of a multinational corporation. Companies must ensure that their transfer pricing policies are compliant with tax laws to avoid penalties and maintain a positive relationship with tax authorities.

10.8. How can strategic partnerships impact corporate tax liability?

Strategic partnerships can offer businesses unique opportunities to optimize their operations, reduce costs, and increase revenue, all of which can positively impact their corporate tax liability.

10.9. What are some common mistakes to avoid in corporate tax management?

Some common mistakes to avoid in corporate tax management include inadequate record-keeping, missing deductions and credits, improper classification of expenses, failure to comply with tax laws, neglecting transfer pricing rules, ignoring state and local taxes, waiting until the last minute, and not seeking professional advice.

10.10. How can businesses stay updated on corporate tax law changes?

Businesses can stay updated on corporate tax law changes by monitoring legislative changes, tracking court decisions, reviewing IRS guidance, subscribing to tax newsletters and alerts, attending tax seminars and conferences, engaging with tax professionals, and utilizing online resources.

Navigating corporate income tax can be challenging, but with the right knowledge and strategies, businesses can minimize their tax liability and maximize their profitability. Visit income-partners.net to explore strategic partnerships and discover how we can help you achieve tax-efficient success. Address: 1 University Station, Austin, TX 78712, United States. Phone: +1 (512) 471-3434. Website: income-partners.net.