Accumulated Other Comprehensive Income (AOCI) represents specific gains and losses, acting as specialized entries within the shareholders’ equity portion of a company’s balance sheet; exploring potential partnership opportunities to boost your income? Income-partners.net offers resources to help you understand AOCI and find strategic collaborations for success. Understand unrealized profits, losses, and financial statement impact with us.

1. Understanding Accumulated Other Comprehensive Income (AOCI)

What exactly is Accumulated Other Comprehensive Income (AOCI)?

AOCI, or Accumulated Other Comprehensive Income, houses unrealized gains and losses excluded from net income, offering a clearer picture of a company’s financial health beyond traditional metrics; it’s where certain profits and losses sit until they’re realized. According to research from the University of Texas at Austin’s McCombs School of Business, in July 2025, understanding AOCI can provide investors and partners with a more comprehensive view of a company’s financial standing, leading to better-informed decisions.

1.1. The Core Concept of AOCI

What’s the fundamental idea behind Accumulated Other Comprehensive Income (AOCI)?

At its heart, AOCI captures financial activities that don’t immediately impact a company’s net income; it provides a fuller picture of a company’s financial position. This includes items like unrealized gains or losses on investments and foreign currency fluctuations. By understanding AOCI, stakeholders gain a more nuanced view of a company’s true financial health, enabling more informed decision-making and strategic planning.

1.2. AOCI vs. Net Income: Key Differences

How does Accumulated Other Comprehensive Income (AOCI) differ from Net Income?

Net income reflects a company’s profitability over a specific period, while AOCI includes unrealized gains and losses not yet recognized in net income; the Financial Accounting Standards Board (FASB) emphasizes the importance of differentiating between these two to provide a more transparent financial overview. Net income is what’s left after all revenues and expenses have been accounted for; AOCI captures changes in equity that aren’t from net income, giving a broader view of a company’s financial changes.

1.3. Why AOCI Matters to Stakeholders

Why should stakeholders care about Accumulated Other Comprehensive Income (AOCI)?

Stakeholders should pay attention to AOCI because it provides a more complete picture of a company’s financial health and stability; it sheds light on unrealized gains and losses. According to Harvard Business Review, companies with strong AOCI figures often demonstrate better long-term financial resilience and strategic management. A positive AOCI can signal effective risk management and investment strategies, whereas a negative AOCI might indicate potential financial vulnerabilities.

2. Components of Accumulated Other Comprehensive Income

What makes up Accumulated Other Comprehensive Income (AOCI)?

AOCI comprises several key components: unrealized gains/losses on available-for-sale securities, foreign currency translation adjustments, pension adjustments, and changes in unrealized gains/losses from derivative instruments; these elements combine to give a holistic view of a company’s financial dynamics. Entrepreneur.com notes that understanding each component is crucial for a comprehensive financial analysis.

2.1. Unrealized Gains and Losses on Investments

What role do unrealized gains and losses on investments play in Accumulated Other Comprehensive Income (AOCI)?

Unrealized gains and losses on investments significantly impact AOCI, reflecting the changes in the fair value of investments that haven’t been sold yet; these fluctuations offer insights into the investment portfolio’s performance. Experts at income-partners.net emphasize that these unrealized values can indicate future financial potential and market responsiveness. Monitoring these figures helps in assessing a company’s investment strategy and its ability to adapt to market changes.

Unrealized Gains and Losses on Investments in AOCI

Unrealized Gains and Losses on Investments in AOCI

2.2. Foreign Currency Translation Adjustments

How do foreign currency translation adjustments affect Accumulated Other Comprehensive Income (AOCI)?

Foreign currency translation adjustments in AOCI account for gains or losses resulting from converting a company’s financial statements from its functional currency to the reporting currency; these adjustments are essential for multinational corporations. These adjustments reflect the impact of currency fluctuations on a company’s consolidated financial statements, providing a more accurate global financial picture. Managing these adjustments effectively can lead to more stable and predictable financial outcomes.

2.3. Pension Adjustments

In what way do pension adjustments influence Accumulated Other Comprehensive Income (AOCI)?

Pension adjustments within AOCI capture changes related to a company’s pension plans, including actuarial gains and losses; these adjustments reflect the long-term obligations and financial health of pension funds. Financial analysts at income-partners.net point out that these adjustments can provide insights into a company’s long-term liabilities and financial planning. Monitoring these adjustments helps stakeholders understand the potential impact of pension obligations on the company’s overall financial stability.

2.4. Derivative Instruments and AOCI

How do derivative instruments tie into Accumulated Other Comprehensive Income (AOCI)?

Changes in the fair value of derivative instruments that are designated as cash flow hedges are recorded in AOCI; these derivatives are used to manage risks like interest rate and currency fluctuations. These changes reflect the effectiveness of the hedging strategy and its impact on the company’s financial position. According to research from the University of Texas at Austin’s McCombs School of Business, effective use of derivatives can stabilize financial performance and reduce volatility.

3. Regulations and Standards Governing AOCI

What rules and standards govern Accumulated Other Comprehensive Income (AOCI)?

AOCI is governed by accounting standards set by the Financial Accounting Standards Board (FASB) and the International Accounting Standards Board (IASB); these regulations ensure consistency and transparency in financial reporting. These standards dictate how AOCI items should be recognized, measured, and presented in financial statements, providing a framework for accurate and comparable financial reporting. Adhering to these regulations is crucial for maintaining investor confidence and regulatory compliance.

3.1. FASB and AOCI

How does the Financial Accounting Standards Board (FASB) regulate Accumulated Other Comprehensive Income (AOCI)?

The FASB provides specific guidelines on how to report AOCI, ensuring that companies present a clear and comprehensive view of their financial performance; these guidelines cover various aspects of AOCI. The FASB standards include detailed instructions on classifying and reporting AOCI items, promoting uniformity and comparability across different companies’ financial statements. Compliance with FASB standards is essential for maintaining credibility and transparency in financial reporting.

3.2. IASB and AOCI

What role does the International Accounting Standards Board (IASB) play in setting standards for Accumulated Other Comprehensive Income (AOCI)?

The IASB sets international accounting standards that also address AOCI, aiming to standardize financial reporting globally; these standards provide a framework for recognizing and reporting AOCI items. The IASB standards ensure that financial statements are consistent and comparable across different countries, facilitating international investment and financial analysis. Adopting IASB standards helps companies communicate their financial performance effectively to a global audience.

3.3. Compliance and Reporting Requirements

What are the essential compliance and reporting requirements for Accumulated Other Comprehensive Income (AOCI)?

Companies must adhere to specific reporting requirements for AOCI, including proper classification and presentation in the financial statements; these requirements ensure transparency and accuracy. According to Entrepreneur.com, accurate reporting of AOCI items can significantly impact a company’s perceived financial health and investor confidence. Compliance involves following both FASB and IASB guidelines, depending on the company’s reporting jurisdiction, to maintain regulatory compliance and stakeholder trust.

4. Calculating Accumulated Other Comprehensive Income

How is Accumulated Other Comprehensive Income (AOCI) calculated?

Calculating AOCI involves tracking and accumulating the changes in its various components, such as unrealized gains/losses, foreign currency adjustments, and pension adjustments, over time; the formula is straightforward but requires careful tracking. The basic formula is: Beginning AOCI + Changes in Unrealized Gains/Losses + Foreign Currency Adjustments + Pension Adjustments = Ending AOCI. This calculation provides a cumulative view of the company’s comprehensive income beyond net income.

4.1. Formula for AOCI

What is the formula used to calculate Accumulated Other Comprehensive Income (AOCI)?

The formula for calculating AOCI is: Beginning AOCI + Changes in Unrealized Gains/Losses + Foreign Currency Adjustments + Pension Adjustments = Ending AOCI; this simple formula summarizes the cumulative impact of comprehensive income items. This calculation integrates all the components of AOCI to provide a comprehensive view of the company’s financial performance. Regular monitoring and accurate calculation of AOCI are crucial for effective financial management.

4.2. Example Calculation

Can you provide an example of how to calculate Accumulated Other Comprehensive Income (AOCI)?

Suppose a company starts with an AOCI of $100,000, has unrealized gains of $20,000, foreign currency losses of $5,000, and pension adjustments of $2,000; the ending AOCI would be $117,000. This example illustrates how different components combine to affect the final AOCI balance. Using this calculation, stakeholders can quickly assess the cumulative impact of various financial activities on the company’s comprehensive income.

4.3. Common Mistakes to Avoid

What are some common mistakes to avoid when calculating Accumulated Other Comprehensive Income (AOCI)?

Common mistakes include misclassifying items, inaccurate currency translations, and errors in pension adjustments; avoiding these mistakes is crucial for accurate financial reporting. Financial experts at income-partners.net stress the importance of double-checking all figures and classifications to ensure accuracy. Regular audits and adherence to accounting standards can help prevent these common errors, ensuring reliable financial reporting.

5. Presentation and Disclosure of AOCI

How should Accumulated Other Comprehensive Income (AOCI) be presented and disclosed in financial statements?

AOCI should be presented in the equity section of the balance sheet and disclosed in the statement of comprehensive income; proper presentation and disclosure are essential for transparency. The presentation should clearly show the different components of AOCI, such as unrealized gains/losses, foreign currency adjustments, and pension adjustments. Disclosures should provide detailed explanations of these items, helping stakeholders understand their impact on the company’s financial position.

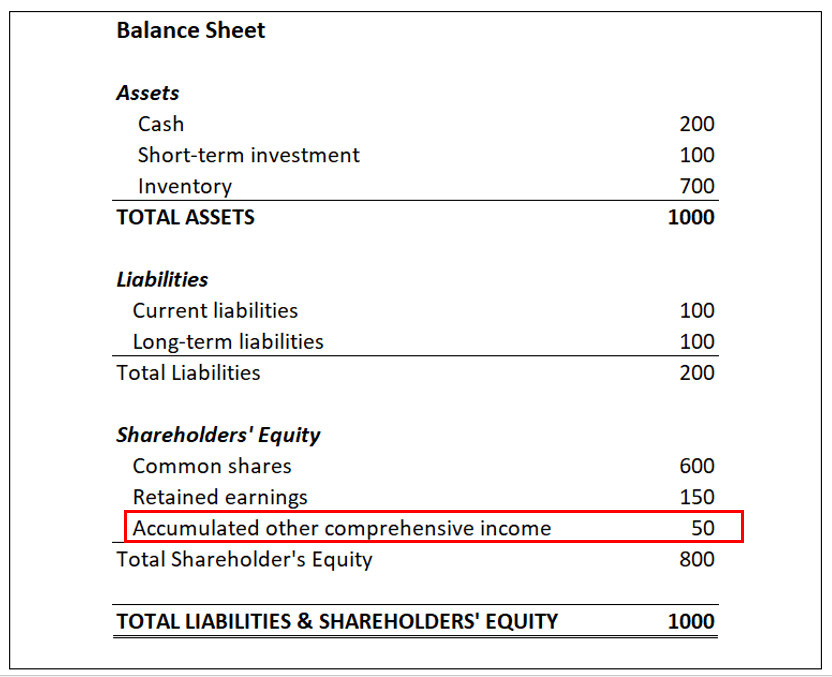

5.1. Balance Sheet Presentation

How should Accumulated Other Comprehensive Income (AOCI) be presented on the balance sheet?

On the balance sheet, AOCI is typically presented as a separate component of shareholders’ equity, distinguishing it from retained earnings and other equity accounts; this clear presentation helps stakeholders understand its significance. AOCI is usually listed after retained earnings, providing a clear view of the total equity. Proper balance sheet presentation is vital for accurate financial analysis and informed decision-making.

5.2. Statement of Comprehensive Income

What is the role of the statement of comprehensive income in disclosing Accumulated Other Comprehensive Income (AOCI)?

The statement of comprehensive income includes AOCI items, providing a detailed view of all changes in equity that are not from transactions with owners; it offers a broader view than the traditional income statement. This statement presents both net income and other comprehensive income, combining them to show the total comprehensive income for the period. The statement of comprehensive income is essential for assessing a company’s overall financial performance.

5.3. Disclosure Requirements

What specific disclosures are required for Accumulated Other Comprehensive Income (AOCI)?

Companies must disclose detailed information about the components of AOCI, including the nature of each item and any related tax effects; these disclosures enhance transparency and understanding. According to research from the University of Texas at Austin’s McCombs School of Business, thorough disclosures help investors and analysts make more informed decisions. Disclosure requirements ensure that stakeholders have access to all relevant information about a company’s AOCI.

6. Impact of AOCI on Financial Analysis

How does Accumulated Other Comprehensive Income (AOCI) impact financial analysis?

AOCI provides a more comprehensive view of a company’s financial health, impacting ratios, performance metrics, and overall financial assessment; it offers insights beyond net income. Financial analysts use AOCI to assess the stability and sustainability of a company’s earnings. Incorporating AOCI into financial analysis can lead to more accurate valuations and better-informed investment decisions.

6.1. Ratios and Performance Metrics

How does Accumulated Other Comprehensive Income (AOCI) affect financial ratios and performance metrics?

AOCI can affect various financial ratios and performance metrics by providing a more complete picture of a company’s financial position, especially when analyzing equity and profitability; it enhances the accuracy of these metrics. For example, incorporating AOCI into the calculation of return on equity (ROE) can provide a more accurate assessment of a company’s profitability. These enhanced metrics offer a more nuanced understanding of financial performance.

6.2. AOCI and Investment Decisions

How should investors consider Accumulated Other Comprehensive Income (AOCI) when making investment decisions?

Investors should consider AOCI as it offers insights into unrealized gains and losses, providing a more complete picture of a company’s financial health; it can influence investment strategies. Harvard Business Review suggests that companies with a positive AOCI trend often represent more stable and reliable investment opportunities. Understanding AOCI helps investors make better-informed decisions and assess potential risks and rewards more accurately.

6.3. AOCI and Credit Analysis

What role does Accumulated Other Comprehensive Income (AOCI) play in credit analysis?

AOCI is a factor in credit analysis, offering insights into a company’s overall financial stability and its ability to meet long-term obligations; it provides a broader view than just net income. Credit analysts use AOCI to assess a company’s equity position and its capacity to absorb potential losses. A strong AOCI balance can indicate a lower risk of default, making the company more attractive to lenders.

7. Real-World Examples of AOCI

Can you provide some real-world examples of how Accumulated Other Comprehensive Income (AOCI) is used by companies?

Several companies across various industries use AOCI to report items like unrealized gains/losses on investments and foreign currency adjustments; these examples illustrate its practical application. For instance, a multinational corporation might use AOCI to report gains and losses from currency fluctuations. These real-world examples show how AOCI provides a more transparent view of a company’s financial activities, aiding stakeholders in making informed decisions.

7.1. AOCI in Multinational Corporations

How do multinational corporations utilize Accumulated Other Comprehensive Income (AOCI)?

Multinational corporations use AOCI extensively to report foreign currency translation adjustments and unrealized gains/losses on international investments; it helps them manage global financial complexities. These adjustments are essential for consolidating financial statements and providing an accurate view of the company’s global financial performance. Effective use of AOCI enables multinational corporations to communicate their financial results more transparently to stakeholders worldwide.

7.2. AOCI in Financial Institutions

What role does Accumulated Other Comprehensive Income (AOCI) play in financial institutions?

Financial institutions use AOCI to report unrealized gains and losses on securities and derivatives, providing a clearer picture of their financial risk management; it’s crucial for assessing their financial health. These institutions must carefully manage and report AOCI items to comply with regulatory requirements and maintain investor confidence. Accurate reporting of AOCI helps stakeholders understand the financial institution’s risk exposure and overall stability.

7.3. AOCI in Manufacturing Companies

How do manufacturing companies use Accumulated Other Comprehensive Income (AOCI)?

Manufacturing companies use AOCI to report pension adjustments and unrealized gains/losses on hedging activities, providing a more complete view of their financial obligations and strategies; it helps in long-term financial planning. These adjustments reflect the long-term liabilities and hedging strategies that impact the company’s financial stability. Proper use of AOCI allows manufacturing companies to communicate their financial position more effectively to investors and creditors.

8. Advantages and Limitations of AOCI

What are the advantages and limitations of using Accumulated Other Comprehensive Income (AOCI)?

AOCI offers a more comprehensive view of a company’s financial health but also has limitations due to its complexity and the subjectivity involved in certain valuations; understanding both is essential. Advantages include providing a more complete picture of financial performance and offering insights into unrealized gains and losses. Limitations include the potential for volatility and the challenges in accurately valuing certain AOCI components.

8.1. Benefits of AOCI

What are the key benefits of reporting Accumulated Other Comprehensive Income (AOCI)?

The benefits of reporting AOCI include a more comprehensive view of financial performance, improved transparency, and better insights into a company’s long-term financial health; these benefits enhance stakeholder understanding. According to Entrepreneur.com, AOCI provides valuable information for investors and analysts, enabling them to make more informed decisions. The increased transparency and detailed financial insights are crucial for maintaining trust and confidence in the company.

8.2. Drawbacks of AOCI

What are the potential drawbacks or limitations of Accumulated Other Comprehensive Income (AOCI)?

Drawbacks of AOCI include its complexity, potential for volatility, and the subjectivity involved in valuing certain components, which can make it challenging to interpret accurately; these limitations must be considered. The complexity can make it difficult for non-experts to understand, while the volatility can create uncertainty about future financial performance. Being aware of these limitations is essential for accurate and balanced financial analysis.

8.3. Mitigating the Limitations

How can companies mitigate the limitations of Accumulated Other Comprehensive Income (AOCI)?

Companies can mitigate the limitations of AOCI by providing clear and detailed disclosures, using consistent valuation methods, and ensuring transparency in their financial reporting practices; these strategies enhance understanding. Regular audits and adherence to accounting standards can also help improve the accuracy and reliability of AOCI reporting. By addressing these limitations, companies can ensure that AOCI provides valuable and trustworthy information to stakeholders.

9. Trends and Future of AOCI

What are the current trends and future outlook for Accumulated Other Comprehensive Income (AOCI)?

Current trends include increased scrutiny of AOCI components and a focus on improving transparency and standardization in reporting; the future may bring more refined accounting standards. Financial experts at income-partners.net anticipate that regulatory bodies will continue to enhance the guidelines for AOCI, aiming to provide more consistent and comparable financial information. These trends will likely lead to more accurate and reliable financial analysis.

9.1. Increased Scrutiny

Why is there increased scrutiny of Accumulated Other Comprehensive Income (AOCI)?

Increased scrutiny of AOCI stems from the desire for greater transparency and accuracy in financial reporting, ensuring that stakeholders have a clear understanding of a company’s financial health; this scrutiny enhances trust. Regulators and investors are increasingly focused on the components of AOCI, seeking to identify any potential risks or inconsistencies. This heightened scrutiny is expected to drive improvements in AOCI reporting practices.

9.2. Standardization Efforts

What efforts are being made to standardize the reporting of Accumulated Other Comprehensive Income (AOCI)?

Efforts to standardize AOCI reporting involve developing more detailed and consistent accounting standards, both nationally and internationally; this aims to improve comparability. Organizations like the FASB and IASB are working to refine the guidelines for AOCI, ensuring that companies report these items in a uniform manner. These standardization efforts are crucial for enhancing the reliability and usefulness of financial statements.

9.3. The Future of AOCI Reporting

What does the future hold for Accumulated Other Comprehensive Income (AOCI) reporting?

The future of AOCI reporting likely includes more detailed disclosures, enhanced standardization, and potentially real-time reporting, providing stakeholders with more timely and accurate information; this will improve decision-making. According to research from the University of Texas at Austin’s McCombs School of Business, advancements in technology and data analytics may also play a role in transforming AOCI reporting. These developments are expected to increase the value and relevance of AOCI in financial analysis.

10. AOCI and Partnering for Success

How can understanding Accumulated Other Comprehensive Income (AOCI) help in forming successful partnerships?

Understanding AOCI can help in forming successful partnerships by providing insights into a potential partner’s financial stability and risk management practices; it allows for informed decisions. A company with a strong AOCI balance is often seen as a more reliable and financially sound partner. Evaluating AOCI can help identify potential risks and opportunities, leading to more strategic and beneficial partnerships.

10.1. Evaluating Potential Partners

How can you use Accumulated Other Comprehensive Income (AOCI) to evaluate potential business partners?

You can use AOCI to evaluate potential business partners by assessing their financial stability, risk management practices, and long-term financial health; it offers a comprehensive view. A partner with a consistently positive AOCI trend may be a more reliable and sustainable collaborator. Analyzing AOCI can help you make informed decisions about potential partnerships, ensuring alignment with your business goals and values.

10.2. Building Stronger Partnerships

How does understanding Accumulated Other Comprehensive Income (AOCI) contribute to building stronger partnerships?

Understanding AOCI contributes to building stronger partnerships by fostering transparency, trust, and mutual understanding of financial positions; it enhances collaboration. When both partners have a clear understanding of each other’s financial health, they can work together more effectively to achieve common goals. This transparency promotes a more collaborative and successful partnership.

10.3. Income-Partners.net and AOCI

How can income-partners.net help you understand and leverage Accumulated Other Comprehensive Income (AOCI) in your partnerships?

Income-partners.net offers resources and insights to help you understand and leverage AOCI in your partnerships, providing valuable tools for financial analysis and strategic decision-making; we help you succeed. Our platform provides access to experts, articles, and tools that can assist you in evaluating potential partners and building stronger, more financially sound collaborations. By leveraging income-partners.net, you can enhance your understanding of AOCI and improve your partnership outcomes.

Ready to find the right partners and boost your income? Visit income-partners.net today to explore partnership opportunities, learn essential strategies, and connect with potential collaborators across the USA. Address: 1 University Station, Austin, TX 78712, United States. Phone: +1 (512) 471-3434. Website: income-partners.net.

Frequently Asked Questions (FAQ) About Accumulated Other Comprehensive Income (AOCI)

1. What is the primary purpose of Accumulated Other Comprehensive Income (AOCI)?

The primary purpose of AOCI is to provide a comprehensive view of a company’s financial performance, including gains and losses that are not yet realized in net income; it enhances transparency. AOCI captures financial activities like unrealized gains on investments and foreign currency fluctuations, offering a more complete picture of a company’s financial health.

2. How does AOCI differ from retained earnings?

AOCI differs from retained earnings in that it includes unrealized gains and losses, while retained earnings represent accumulated net income less dividends; they serve different purposes. Retained earnings reflect profits that have been reinvested in the business, while AOCI captures changes in equity that are not part of net income.

3. What are the main components of AOCI?

The main components of AOCI include unrealized gains and losses on available-for-sale securities, foreign currency translation adjustments, pension adjustments, and changes in unrealized gains/losses from derivative instruments; these elements combine to give a holistic view. Each component reflects different aspects of a company’s financial activities that are not immediately recognized in net income.

4. How is AOCI presented in financial statements?

AOCI is presented in the equity section of the balance sheet and disclosed in the statement of comprehensive income; proper presentation and disclosure are essential for transparency. This clear presentation helps stakeholders understand the different components of AOCI and their impact on the company’s financial position.

5. Why is AOCI important for investors?

AOCI is important for investors because it provides a more complete picture of a company’s financial health, including unrealized gains and losses that can impact future performance; it informs investment decisions. Understanding AOCI helps investors assess the stability and sustainability of a company’s earnings, leading to better-informed investment choices.

6. Can AOCI be negative?

Yes, AOCI can be negative if a company has accumulated more losses than gains in its other comprehensive income components; it indicates potential financial challenges. A negative AOCI balance might suggest that a company has significant unrealized losses on investments or negative foreign currency adjustments.

7. How do accounting standards (FASB and IASB) regulate AOCI?

Accounting standards set by FASB and IASB provide specific guidelines on how to recognize, measure, and present AOCI items, ensuring consistency and transparency; these regulations are crucial. These standards dictate how AOCI components should be classified and reported, promoting uniformity and comparability across different companies’ financial statements.

8. What are some common mistakes to avoid when calculating AOCI?

Common mistakes to avoid when calculating AOCI include misclassifying items, inaccurate currency translations, and errors in pension adjustments; avoiding these mistakes is crucial for accurate financial reporting. Double-checking all figures and classifications and adhering to accounting standards can help prevent these errors.

9. How does AOCI affect financial ratios and performance metrics?

AOCI can affect financial ratios and performance metrics by providing a more complete picture of a company’s financial position, especially when analyzing equity and profitability; it enhances the accuracy of these metrics. Incorporating AOCI into calculations like return on equity (ROE) can provide a more accurate assessment of a company’s financial performance.

10. Where can I find more information and resources about AOCI?

You can find more information and resources about AOCI at income-partners.net, which offers insights, tools, and expert advice for understanding and leveraging AOCI in your partnerships; we are here to help. Our platform provides access to articles, case studies, and financial analysis tools that can assist you in making informed decisions about potential collaborations and investments.