Is a good income to rent ratio on your mind? It’s a critical question! Let’s unlock the formula that paves your way to financial stability and profitable partnerships, only at income-partners.net! Discover how to ensure you can comfortably afford your rental while maximizing income opportunities and building solid financial ground. We’ll explore the relationship between earnings and rental affordability.

1. Understanding the Rent to Income Ratio

What exactly is a rent to income ratio? Simply put, a rent to income ratio is the percentage of your gross monthly income that goes towards paying rent, and a good ratio is crucial for financial stability. The income to rent ratio helps tenants and landlords alike in assessing the affordability of a rental property. This ratio is a critical tool for assessing financial well-being and ensuring renters can comfortably manage their housing costs alongside other financial obligations.

1.1. Why This Ratio Matters

The rent to income ratio serves as an important indicator for both renters and landlords, and is a key performance indicator. For renters, it’s a gauge of financial health, ensuring that housing costs don’t overextend their budget. For landlords, it’s a way to predict a tenant’s reliability in paying rent, minimizing the risk of late or missed payments. By understanding this ratio, tenants can make informed decisions about where they can afford to live, while landlords can secure stable rental income.

1.2. Benchmarking a Good Ratio

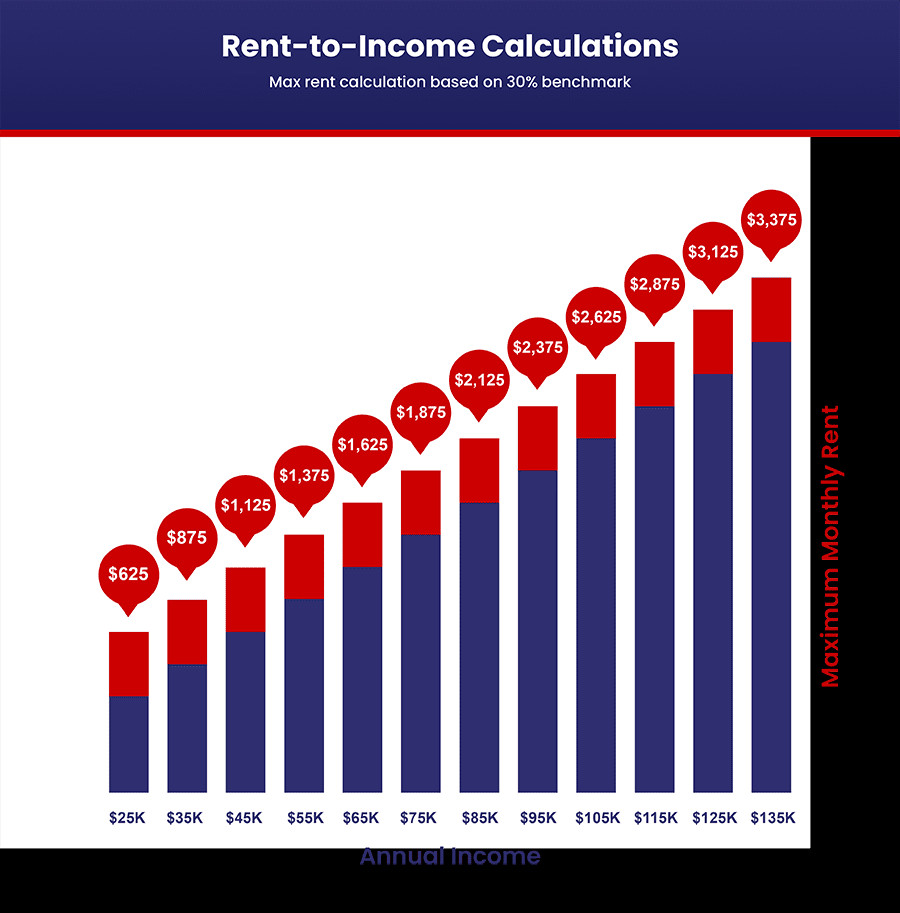

So, what constitutes a good rent to income ratio? While opinions vary, the general consensus is that you shouldn’t spend more than 30% of your gross monthly income on rent. Sticking to this benchmark allows you to cover essential expenses, save for future goals, and handle unexpected costs without financial strain. Remember, this percentage is a guideline; individual circumstances may require adjusting this figure.

1.3. Exploring the Consequences of Exceeding the Ideal Ratio

When rent consumes a significant portion of your income, you may find yourself in a financially precarious position. Exceeding the ideal rent to income ratio can lead to a number of challenges:

- Limited Savings: High rent costs leave less room for saving, making it difficult to achieve financial goals like buying a home or investing.

- Increased Debt: Relying on credit cards or loans to cover basic expenses becomes more likely, leading to a cycle of debt.

- Financial Stress: Constant worry about making ends meet can take a toll on your mental and physical health.

- Reduced Discretionary Spending: Less money is available for leisure activities, hobbies, and other enjoyment, impacting your overall quality of life.

1.4. Real-World Perspective

Consider the impact of exceeding a 30% rent to income ratio in a high-cost city such as Austin, TX. For an individual earning $60,000 annually, a rent exceeding $1,500 monthly would surpass the recommended threshold. This could mean sacrificing savings goals, limiting leisure activities, or taking on additional debt to maintain their lifestyle.

2. Methods for Calculating Rent to Income Ratio

What are the most effective ways to calculate the rent to income ratio? Here are some tried-and-true methods, with a focus on simplicity and accuracy:

2.1. The Basic Calculation

The fundamental way to calculate the rent to income ratio involves dividing your gross monthly income by your monthly rent and then multiplying by 100 to express it as a percentage.

Rent to Income Ratio = (Monthly Rent / Gross Monthly Income) x 100

For example, if your gross monthly income is $5,000 and your rent is $1,500:

($1,500 / $5,000) x 100 = 30%

2.2. Income-Based Approach

This method focuses on determining the maximum rent you can afford based on your income. If we stick to the 30% rule, the calculation looks like this:

Maximum Affordable Rent = Gross Monthly Income x 0.30

Using the same income of $5,000, the maximum affordable rent would be:

$5,000 x 0.30 = $1,500

2.3. The 40x Rule

A variation of the income-based approach, the 40x rule suggests that your annual income should be at least 40 times the monthly rent.

Minimum Annual Income = Monthly Rent x 40

For a rent of $1,500, the required annual income would be:

$1,500 x 40 = $60,000

2.4. Applying Different Income Calculation Methods

According to research from the University of Texas at Austin’s McCombs School of Business, real estate decisions are made by the income method, so you can know what kind of home to buy based on your income.

monthly rental income

monthly rental income

2.5. Practical Application

Let’s apply these methods to a real-life scenario:

Scenario: You’re considering an apartment in Austin, TX, with a monthly rent of $1,800. Your gross monthly income is $6,000.

- Basic Calculation: ($1,800 / $6,000) x 100 = 30%

- Income-Based Approach: $6,000 x 0.30 = $1,800

- The 40x Rule: $1,800 x 40 = $72,000

Based on these calculations, the apartment falls within the recommended rent to income ratio, suggesting it’s an affordable option.

3. Factors Influencing the Ideal Rent to Income Ratio

What factors play a role in determining your ideal rent to income ratio? Let’s take a look:

3.1. Geographical Location

The cost of living varies significantly depending on the location. In high-cost cities such as New York, San Francisco, or Austin, the 30% rule may be unrealistic due to higher rent prices. In more affordable areas, you may be able to find suitable housing options while staying well below this threshold.

3.2. Personal Financial Situation

Your individual financial situation plays a significant role in determining your ideal rent to income ratio. Consider factors such as:

- Debt Payments: High student loan, credit card, or auto loan payments can strain your budget, requiring a lower rent to income ratio.

- Savings Goals: If you’re aggressively saving for a down payment on a home or retirement, you may want to allocate a smaller percentage of your income to rent.

- Lifestyle Choices: Your spending habits and lifestyle choices can impact your ability to afford rent. If you enjoy frequent dining out or expensive hobbies, you may need to adjust your rent accordingly.

3.3. Economic Conditions

Economic factors such as inflation, job market stability, and interest rates can influence the affordability of rent. In times of economic uncertainty, it may be prudent to aim for a lower rent to income ratio to provide a financial cushion.

3.4. Rental Market Dynamics

The dynamics of the local rental market also play a role. In competitive markets with high demand and limited supply, landlords may have stricter income requirements, potentially pushing the rent to income ratio higher.

3.5. Considering Additional Costs

When calculating your rent to income ratio, be sure to factor in additional costs associated with renting a property. These may include:

- Utilities: Electricity, water, gas, and internet bills can add a significant amount to your monthly expenses.

- Renter’s Insurance: Protecting your belongings with renter’s insurance is essential.

- Parking Fees: If parking is not included in your rent, factor in monthly parking fees.

- Pet Fees: If you have pets, you may need to pay additional pet fees or pet rent.

3.6. Case Scenario

Suppose you’re considering a rental in Austin, TX, with a monthly rent of $1,600. You have student loan payments of $400 per month, a car payment of $300 per month, and credit card debt totaling $200 per month. Your gross monthly income is $5,500.

In this scenario, your total monthly debt payments amount to $900. Subtracting this from your gross monthly income leaves you with $4,600 for rent and other expenses. Your adjusted rent to income ratio would be ($1,600 / $4,600) x 100 = 34.78%. This is slightly above the recommended 30% threshold, suggesting you may need to re-evaluate your budget or consider a less expensive rental option.

4. Strategies for Managing Your Rent to Income Ratio

How can you effectively manage your rent to income ratio to achieve financial stability and peace of mind?

4.1. Negotiating Rent

Don’t hesitate to negotiate rent with landlords, especially in competitive rental markets. Research comparable properties in the area to demonstrate that the asking rent is above market value. Highlight your strengths as a tenant, such as a strong credit history, stable employment, and a history of responsible renting.

4.2. Finding a Roommate

Sharing housing costs with a roommate can significantly reduce your individual rent burden. Not only does it lower your rent to income ratio, but it also allows you to split utility bills and other shared expenses.

4.3. Increasing Your Income

Exploring opportunities to increase your income can improve your rent to income ratio and enhance your overall financial situation. Consider options such as:

- Side Hustles: Freelancing, part-time jobs, or starting your own business can supplement your income.

- Negotiating a Raise: If you’re performing well at your current job, negotiate a raise or promotion.

- Investing: Investing in stocks, bonds, or real estate can generate passive income over time.

4.4. Relocating to a More Affordable Area

If you’re struggling to afford rent in your current location, consider relocating to a more affordable area. Research cities or neighborhoods with lower housing costs and comparable job opportunities.

4.5. Downsizing

Consider downsizing to a smaller apartment or home to reduce your rent expenses. Assess your space needs and determine if you can comfortably live in a smaller unit.

4.6. Budgeting and Expense Tracking

Create a detailed budget to track your income and expenses. Identify areas where you can cut back on spending and allocate more funds towards rent. There are numerous budgeting apps and tools available to help you manage your finances effectively.

4.7. Exploring Government Assistance Programs

Research government assistance programs that may provide rental assistance or housing vouchers to eligible individuals and families. These programs can help reduce your rent burden and improve your financial stability.

4.8. A Case Study

Meet Sarah, a young professional living in Austin, TX. Sarah’s gross monthly income is $4,500, and she’s considering an apartment with a monthly rent of $1,600.

- Current Rent to Income Ratio: ($1,600 / $4,500) x 100 = 35.56%

- Analysis: Sarah’s current rent to income ratio exceeds the recommended 30% threshold, indicating she may be stretching her budget.

Sarah’s Strategies for Improvement:

- Negotiating Rent: Sarah successfully negotiates a $100 reduction in rent, bringing it down to $1,500.

- Finding a Roommate: Sarah finds a roommate to share housing costs, splitting the rent in half to $750 each.

- Increasing Income: Sarah starts a side hustle freelancing as a graphic designer, earning an additional $500 per month.

New Rent to Income Ratio:

- Rent: $750

- Gross Monthly Income: $5,000

- Rent to Income Ratio: ($750 / $5,000) x 100 = 15%

By implementing these strategies, Sarah significantly improved her rent to income ratio, achieving greater financial stability and peace of mind.

5. Landlord’s Perspective: Income Requirements for Renting

What income requirements do landlords typically have for prospective tenants? Let’s explore:

5.1. Typical Income Thresholds

Landlords often use income thresholds as a primary criterion for evaluating tenant eligibility. A common requirement is that tenants must earn at least 2.5 to 3 times the monthly rent.

5.2. Verifying Income

Landlords typically verify income through various means, including:

- Pay Stubs: Requesting recent pay stubs to confirm employment and income.

- Tax Returns: Reviewing tax returns to assess annual income.

- Bank Statements: Examining bank statements to verify deposits and income sources.

- Employment Verification: Contacting employers to confirm employment status and salary.

5.3. Alternative Income Sources

Landlords may also consider alternative income sources, such as:

- Savings: Assessing savings accounts or investment portfolios to determine financial stability.

- Investments: Evaluating income from investments, such as dividends or rental properties.

- Government Assistance: Factoring in government assistance programs, such as Social Security or disability benefits.

- Alimony or Child Support: Considering alimony or child support payments as income sources.

5.4. Exceptions to Income Requirements

In some cases, landlords may make exceptions to strict income requirements, such as:

- Co-Signers: Requiring a co-signer with a strong credit history and sufficient income to guarantee rent payments.

- Increased Security Deposit: Requesting a larger security deposit to mitigate the risk of non-payment.

- Rent Guarantee Insurance: Requiring tenants to purchase rent guarantee insurance to protect against rent defaults.

5.5. Fair Housing Laws

Landlords must comply with fair housing laws, which prohibit discrimination based on protected characteristics such as race, color, religion, national origin, sex, familial status, and disability.

5.6. Case Example

Consider a landlord in Austin, TX, renting out a property with a monthly rent of $1,800. The landlord requires tenants to have a gross monthly income of at least 3 times the rent, which amounts to $5,400.

The landlord verifies income by requesting recent pay stubs, tax returns, and employment verification. They also consider alternative income sources, such as savings and investments.

In one instance, a prospective tenant’s income falls slightly below the required threshold. However, the tenant has a co-signer with a strong credit history and sufficient income to guarantee rent payments. The landlord approves the tenant’s application, considering the co-signer as an additional layer of security.

6. Leveraging Partnerships to Boost Income

How can you leverage strategic partnerships to increase your income and improve your rent to income ratio? income-partners.net offers a unique platform to explore collaborative opportunities.

6.1. Identifying Synergistic Partnerships

Start by identifying potential partners whose skills, resources, or networks complement your own. Consider businesses or individuals in related industries or those who cater to a similar target market.

6.2. Exploring Different Types of Partnerships

There are numerous types of partnerships you can explore, including:

- Joint Ventures: Collaborating on a specific project or venture to share resources and profits.

- Affiliate Marketing: Promoting each other’s products or services to earn commissions on sales.

- Strategic Alliances: Forming long-term partnerships to leverage each other’s strengths and expand market reach.

- Referral Partnerships: Exchanging referrals to generate new leads and customers.

6.3. Building Mutually Beneficial Relationships

Focus on building mutually beneficial relationships with your partners. Ensure that each party benefits from the collaboration and that the partnership is based on trust, transparency, and shared goals.

6.4. Monetizing Partnerships

Explore various ways to monetize your partnerships, such as:

- Revenue Sharing: Splitting revenue generated from joint projects or ventures.

- Commission-Based Agreements: Earning commissions on sales or leads generated through partnerships.

- Cross-Promotional Campaigns: Leveraging each other’s marketing channels to promote products or services and drive revenue.

6.5. Case Illustration

Consider a freelance graphic designer looking to increase their income. They partner with a local marketing agency to offer design services to the agency’s clients.

- Partnership Structure: The graphic designer receives a commission on each design project referred by the marketing agency.

- Income Boost: Through this partnership, the graphic designer significantly increases their income, allowing them to afford a more desirable rental property.

- Improved Rent to Income Ratio: With the additional income, the graphic designer’s rent to income ratio improves, enhancing their financial stability.

6.6. Unlocking Opportunities

income-partners.net offers resources and tools to help you identify potential partners, negotiate agreements, and monetize your collaborations. By leveraging strategic partnerships, you can boost your income, improve your rent to income ratio, and achieve your financial goals.

7. Case Studies: Real-Life Examples of Rent to Income Ratio Management

What do real-life scenarios teach us about managing the rent to income ratio effectively?

7.1. The Urban Professional

Profile: A young professional living in a bustling city, earning a moderate income.

Challenge: High rent prices in the city make it difficult to maintain a healthy rent to income ratio.

Solution:

- Finding a Roommate: The professional shares an apartment with a roommate to split housing costs.

- Negotiating Rent: They successfully negotiate a lower rent by highlighting their excellent credit history and stable employment.

- Budgeting and Expense Tracking: They create a detailed budget to track expenses and identify areas to cut back on spending.

Outcome: By implementing these strategies, the urban professional significantly improves their rent to income ratio, achieving greater financial stability.

7.2. The Freelancer

Profile: A freelancer with fluctuating income.

Challenge: Inconsistent income makes it challenging to plan for rent payments and maintain a stable rent to income ratio.

Solution:

- Building an Emergency Fund: The freelancer establishes an emergency fund to cover rent payments during periods of low income.

- Diversifying Income Streams: They diversify income streams by offering multiple services and pursuing various freelance opportunities.

- Negotiating Flexible Payment Terms: They negotiate flexible payment terms with their landlord, allowing them to pay rent in installments during slow months.

Outcome: By taking these steps, the freelancer manages their rent to income ratio effectively, even in the face of income fluctuations.

7.3. The Student

Profile: A student with limited income and student loan debt.

Challenge: High rent prices and student loan payments strain the student’s budget, making it difficult to afford housing.

Solution:

- Exploring Affordable Housing Options: The student explores affordable housing options, such as dormitories or shared apartments.

- Seeking Rental Assistance: They apply for rental assistance programs to help cover a portion of their rent.

- Part-Time Employment: They secure part-time employment to supplement their income and cover living expenses.

Outcome: By utilizing these resources and strategies, the student manages their rent to income ratio effectively while pursuing their education.

7.4. Key Takeaways

These case studies underscore the importance of proactive rent to income ratio management. By employing a combination of strategies, individuals can navigate the challenges of affordable housing and achieve financial stability.

8. Common Pitfalls to Avoid

What are some common mistakes to avoid when assessing the rent to income ratio?

8.1. Ignoring Additional Expenses

Failing to account for additional expenses such as utilities, transportation, and groceries can distort your perception of affordability. Always factor in all living expenses when calculating your rent to income ratio.

8.2. Overestimating Income

Relying on potential or unreliable income sources can lead to financial strain if those sources don’t materialize. Base your rent to income ratio calculations on stable, verifiable income.

8.3. Neglecting Debt Payments

Ignoring debt payments such as student loans, credit card debt, or auto loans can create an unrealistic view of your financial situation. Factor in all debt obligations when assessing your rent to income ratio.

8.4. Overlooking Unexpected Costs

Life is full of surprises, and unexpected expenses can arise at any time. Build a financial cushion to cover unexpected costs and avoid relying on credit cards or loans to pay rent.

8.5. Ignoring Market Trends

Failing to consider market trends such as rising rent prices or changes in interest rates can lead to poor financial decisions. Stay informed about market conditions and adjust your rent to income ratio accordingly.

8.6. Case Scenario

Consider a young professional who fails to account for additional expenses such as utilities, transportation, and groceries when calculating their rent to income ratio. They assume that their rent is affordable based on their income alone.

However, after moving into their new apartment, they quickly realize that their utility bills are higher than expected, and transportation costs are straining their budget. They struggle to make ends meet and fall behind on rent payments.

By avoiding these common pitfalls and taking a proactive approach to financial planning, individuals can make informed decisions about housing affordability and maintain a healthy rent to income ratio.

9. The Future of Renting: Trends and Predictions

What trends and predictions will shape the future of renting?

9.1. Increasing Rent Prices

Rent prices are expected to continue rising in many markets due to factors such as population growth, limited housing supply, and inflation.

9.2. Shift Towards Urbanization

Urbanization trends are likely to persist, with more people moving to cities for job opportunities and lifestyle amenities.

9.3. Rise of Co-Living Spaces

Co-living spaces, which offer shared housing with communal amenities, are gaining popularity as an affordable housing option, especially among young professionals.

9.4. Focus on Amenities and Services

Renters are increasingly seeking apartments with amenities such as fitness centers, co-working spaces, and pet-friendly features.

9.5. Technological Innovations

Technological innovations such as smart home devices, online rent payment systems, and virtual property tours are transforming the rental experience.

9.6. Sustainability Initiatives

Sustainability initiatives such as energy-efficient appliances, green building materials, and recycling programs are becoming more prevalent in rental properties.

9.7. Flexile Leases

Shorter and more flexible lease terms are more common to allow the workforce to move around easier for employment.

9.8. Expert Opinion

According to real estate experts, the future of renting will be shaped by a combination of economic, demographic, and technological factors. Landlords and tenants alike will need to adapt to these changes to thrive in the evolving rental landscape.

9.9. Staying Ahead

To stay ahead of the curve, renters should focus on improving their financial literacy, exploring affordable housing options, and leveraging technology to streamline the rental process. Landlords should invest in amenities and services that appeal to modern renters, embrace sustainability initiatives, and adapt to changing market dynamics.

10. Resources for Renters and Landlords

Where can renters and landlords find valuable resources to navigate the rental market?

10.1. Online Rent Calculators

Online rent calculators can help renters determine how much rent they can afford based on their income and expenses.

10.2. Budgeting Apps

Budgeting apps can assist renters in tracking their income and expenses, identifying areas to cut back on spending, and saving for future goals.

10.3. Housing Counseling Agencies

Housing counseling agencies offer free or low-cost counseling services to renters and landlords on topics such as budgeting, credit repair, and tenant rights.

10.4. Tenant Rights Organizations

Tenant rights organizations provide legal assistance and advocacy services to renters facing housing issues such as eviction, discrimination, or unsafe living conditions.

10.5. Landlord Associations

Landlord associations offer resources and support to landlords on topics such as tenant screening, lease agreements, and property management.

10.6. Government Agencies

Government agencies such as the Department of Housing and Urban Development (HUD) provide information and resources on affordable housing programs, fair housing laws, and rental assistance programs.

10.7. Income-Partners.net

income-partners.net offers a wealth of resources for renters and landlords alike, including articles, guides, and tools on topics such as rent to income ratio management, partnership opportunities, and financial planning.

10.8. Address and Contact

For further assistance, you can contact income-partners.net at:

- Address: 1 University Station, Austin, TX 78712, United States

- Phone: +1 (512) 471-3434

- Website: income-partners.net

These resources can empower renters and landlords to make informed decisions, navigate the rental market effectively, and achieve their financial goals.

Frequently Asked Questions (FAQ) About Rent to Income Ratio

1. What exactly does the rent to income ratio measure?

The rent to income ratio measures the percentage of your gross monthly income that goes towards rent, reflecting the affordability of your housing.

2. Why is understanding the rent to income ratio important?

It helps ensure financial stability, aids budgeting, and assists in making informed housing decisions for both renters and landlords.

3. What is generally considered a good rent to income ratio?

A rent to income ratio of 30% or less is considered ideal, allowing for other expenses and savings.

4. How do I calculate my rent to income ratio?

Divide your monthly rent by your gross monthly income, then multiply by 100 to get the percentage.

5. What factors can influence the ideal rent to income ratio for an individual?

Geographical location, personal financial situation (including debts and savings), and current economic conditions all play a role.

6. What strategies can renters use to manage their rent to income ratio effectively?

Negotiating rent, finding a roommate, increasing income, and relocating to a more affordable area are effective strategies.

7. How do landlords use the rent to income ratio in tenant screening?

Landlords use it to assess a potential tenant’s ability to pay rent, often requiring an income that is 2.5 to 3 times the monthly rent.

8. Can alternative income sources be considered by landlords?

Yes, landlords may consider savings, investments, or government assistance as alternative income sources.

9. What are some common pitfalls to avoid when calculating and managing the rent to income ratio?

Ignoring additional expenses, overestimating income, and neglecting debt payments are common mistakes.

10. Where can renters and landlords find resources to help them understand and manage the rent to income ratio?

Online calculators, budgeting apps, housing counseling agencies, and websites like income-partners.net provide valuable resources.

Take action today and visit income-partners.net to discover partnership opportunities, refine your financial strategies, and secure a future where your income supports your dreams. Start building beneficial relationships and financial security now and make an amazing business partnership!