What Is A Comfortable Retirement Income, and how can you achieve it? This is a question many people ask as they plan for their future. At income-partners.net, we help you explore various income streams and strategic partnerships to ensure a financially secure and fulfilling retirement, offering comprehensive insights and actionable strategies for achieving your financial goals. By understanding retirement income needs, exploring diverse partnership opportunities, and leveraging resources like income-partners.net, you can confidently chart a course toward a financially secure and fulfilling retirement.

1. Understanding Retirement Income Needs

1.1. Why Focus on Income, Not Just Savings?

Many people fixate on a specific savings target, such as $1 million, without considering if that sum will generate sufficient income to sustain their desired lifestyle throughout retirement. The key to a comfortable retirement lies in ensuring a consistent and adequate income stream, not just accumulating a large lump sum. It’s less about the money in your account and more about the income it generates.

Instead of solely focusing on a savings target, prioritize strategies that generate steady income, which aligns perfectly with the partnership opportunities explored on income-partners.net. This approach ensures long-term financial stability and peace of mind. For example, by collaborating with strategic partners, you can develop income-generating assets that provide a reliable stream of revenue throughout your retirement.

1.2. Estimating Your Retirement Income Needs

A common guideline suggests replacing approximately 80% of your pre-retirement income to maintain your current lifestyle. For example, if your annual income is $100,000, you should aim for $80,000 per year in retirement. However, this is just a starting point. Several factors can influence your actual needs:

- Reduced Expenses: Retirement often brings reduced expenses, such as no longer needing to save for retirement, lower commuting costs, and potentially a paid-off mortgage.

- Lifestyle Choices: Your desired retirement lifestyle significantly impacts your income needs. Frequent travel and hobbies may require a higher income, while downsizing or simplifying your life could reduce your financial requirements.

- Healthcare Costs: Healthcare expenses often increase in retirement, so it’s important to factor in potential medical costs.

Therefore, a personalized assessment is essential to accurately determine your ideal retirement income. You can tailor your retirement plan based on your lifestyle aspirations and financial circumstances.

1.3. The Importance of Personalized Planning

Relying solely on general rules of thumb can be misleading. Instead, consider your unique circumstances, including your health, family situation, and retirement goals.

Key Considerations:

- Personal Health: Anticipate healthcare costs, especially if you have pre-existing conditions.

- Family Needs: Consider any ongoing financial support for family members.

- Lifestyle Aspirations: Factor in travel, hobbies, and other activities you plan to pursue.

Accurate retirement planning involves a thorough evaluation of your individual circumstances and goals. Tailoring your strategy to your specific needs ensures a more secure and fulfilling retirement.

2. Identifying Reliable Income Sources

2.1. Social Security Benefits

Social Security is a crucial component of retirement income for many Americans. Your benefit amount depends on your earnings history and the age at which you begin claiming benefits.

Key Points:

- Benefit Calculation: Social Security benefits are based on your average indexed monthly earnings during your working years.

- Claiming Age: You can claim benefits as early as age 62, but your monthly amount will be reduced. Waiting until your full retirement age (FRA) or age 70 will result in a higher monthly benefit.

- Income Replacement Rate: Social Security typically replaces a smaller percentage of income for higher-income earners.

To estimate your potential benefits, review your Social Security statement or create an account on the Social Security Administration (SSA) website. This information helps you plan effectively and understand the role Social Security plays in your retirement income strategy.

2.2. Pension Plans

Pension plans, which provide a guaranteed monthly income, are another valuable source of retirement funds. If you have a pension from a current or former employer, factor this into your income projections.

Understanding Pensions:

- Defined Benefit Plans: Traditional pensions are defined benefit plans, promising a specific monthly payment upon retirement.

- Vesting Requirements: Pension plans often have vesting requirements, meaning you must work for a certain period to be eligible for benefits.

- Lump-Sum Options: Some pensions offer a lump-sum payout instead of monthly payments. Carefully evaluate the pros and cons of each option before making a decision.

Pensions offer a reliable income stream and can significantly enhance your financial security during retirement. Understanding the details of your pension plan is essential for comprehensive retirement planning.

2.3. Annuities and Reverse Mortgages

Annuities and reverse mortgages can provide additional income streams during retirement.

Annuities:

- Definition: An annuity is a contract with an insurance company that guarantees a stream of payments in exchange for a lump sum or series of payments.

- Types: Immediate annuities start paying out immediately, while deferred annuities accumulate value over time before providing income.

- Benefits: Annuities can provide a predictable income stream and protect against the risk of outliving your savings.

Reverse Mortgages:

- Definition: A reverse mortgage allows homeowners aged 62 and older to borrow against their home equity without selling the home.

- Loan Advances: Borrowers receive loan advances in the form of monthly payments, a line of credit, or a lump sum.

- Repayment: The loan balance grows over time and is repaid when the borrower sells the home, moves out, or passes away.

Both annuities and reverse mortgages can be valuable tools for generating retirement income. Evaluate these options carefully, considering your financial situation and long-term goals.

2.4. The Power of Strategic Partnerships

Beyond traditional income sources, strategic partnerships can significantly boost your retirement income. By collaborating with other businesses or individuals, you can unlock new revenue streams and opportunities.

Benefits of Partnerships:

- Diversification: Partnerships can diversify your income sources, reducing reliance on savings and investments.

- Leveraged Resources: Partners can bring unique skills, resources, and networks to the table, enhancing your earning potential.

- Passive Income: Well-structured partnerships can generate passive income, providing financial security with minimal effort.

At income-partners.net, you can explore various partnership opportunities tailored to your skills and interests. Strategic partnerships offer a dynamic and innovative approach to enhancing your retirement income.

Financial security planning for retirement income

Financial security planning for retirement income

3. Calculating Your Savings Needs

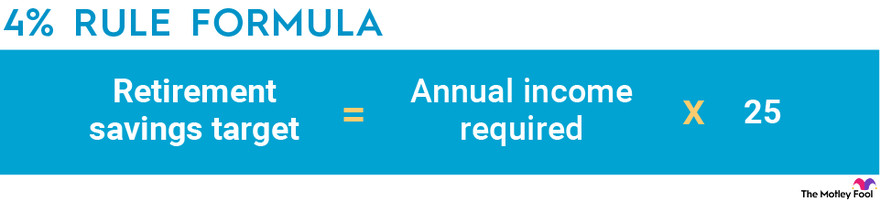

3.1. The 4% Rule: A Guideline for Withdrawals

After estimating your retirement income from sources like Social Security and pensions, determine how much additional income you need from your savings. A common guideline for sustainable withdrawals is the 4% rule.

Understanding the 4% Rule:

- Withdrawal Rate: The 4% rule suggests withdrawing 4% of your retirement savings in the first year of retirement, adjusting this amount annually for inflation.

- Longevity: This rule is designed to ensure your savings last for at least 30 years.

- Market Fluctuations: The 4% rule assumes a balanced portfolio of stocks and bonds and may need adjustments based on market conditions.

To calculate your retirement savings target using the 4% rule, divide your annual income needed from savings by 0.04. For example, if you need $48,000 per year from your savings, you should aim for $1.2 million in retirement accounts.

3.2. Adjusting for Inflation and Market Volatility

Inflation and market volatility can significantly impact your retirement savings.

Inflation:

- Impact: Inflation erodes the purchasing power of your savings, so it’s important to adjust your withdrawal amounts to keep up with rising costs.

- Strategies: Consider investing in assets that tend to outpace inflation, such as real estate or inflation-protected securities.

Market Volatility:

- Impact: Market downturns can reduce your portfolio value, potentially requiring you to withdraw less during those periods.

- Strategies: Maintain a diversified portfolio and consider keeping some cash on hand to avoid selling investments during market downturns.

Adapting your retirement plan to account for inflation and market volatility is crucial for long-term financial security. Regularly review and adjust your strategy as needed.

3.3. Retirement Calculators and Financial Advisors

Retirement calculators and financial advisors can provide personalized guidance and help you refine your savings targets.

Retirement Calculators:

- Benefits: Retirement calculators can estimate your savings needs based on your income, expenses, and retirement goals.

- Limitations: Calculators are only as accurate as the data you input, so be sure to use realistic assumptions.

Financial Advisors:

- Benefits: Financial advisors offer personalized advice tailored to your specific situation and can help you create a comprehensive retirement plan.

- Considerations: Choose an advisor who is experienced, trustworthy, and fee-based.

Both retirement calculators and financial advisors can be valuable resources for planning your retirement. Use them to gain insights, refine your strategies, and make informed decisions.

4. The Role of Strategic Partnerships in Retirement Income

4.1. Leveraging Partnerships for Passive Income

Strategic partnerships can be a powerful tool for generating passive income during retirement. By collaborating with other businesses or individuals, you can create income streams that require minimal ongoing effort.

Examples of Passive Income Partnerships:

- Affiliate Marketing: Partner with businesses to promote their products or services, earning a commission on sales generated through your referral links.

- Rental Properties: Partner with a property manager to oversee your rental properties, generating income without the day-to-day management responsibilities.

- Online Courses: Collaborate with experts to create and sell online courses, earning royalties on course sales.

Strategic partnerships offer a flexible and scalable approach to generating passive income during retirement. Explore partnership opportunities that align with your skills and interests to create a diversified income stream.

4.2. Diversifying Income Streams Through Collaboration

Diversifying your income streams is essential for reducing risk and ensuring financial stability during retirement. Strategic partnerships can help you achieve this diversification.

Benefits of Diversification:

- Reduced Risk: By diversifying your income streams, you reduce your reliance on any single source of funds.

- Increased Stability: A diversified income portfolio can provide more consistent cash flow, even during economic downturns or market volatility.

- Enhanced Opportunities: Diversification opens up new opportunities for growth and income generation.

At income-partners.net, you can explore a wide range of partnership opportunities across different industries and sectors. Diversifying your income streams through collaboration ensures a more secure and fulfilling retirement.

4.3. Finding the Right Partners on income-partners.net

income-partners.net is a valuable resource for finding strategic partners and exploring new income opportunities. The platform connects you with like-minded individuals and businesses, facilitating collaboration and growth.

Benefits of Using income-partners.net:

- Diverse Network: Access a diverse network of potential partners across various industries.

- Targeted Opportunities: Find partnership opportunities that align with your skills, interests, and financial goals.

- Expert Resources: Access expert resources and guidance to help you navigate the world of strategic partnerships.

income-partners.net provides the tools and resources you need to build successful partnerships and enhance your retirement income. Explore the platform today and start building your future.

5. Overcoming Retirement Planning Challenges

5.1. Addressing Unexpected Healthcare Costs

Healthcare costs are a significant concern for retirees. Planning for these expenses is crucial for maintaining financial security.

Strategies for Managing Healthcare Costs:

- Health Savings Account (HSA): If you are eligible, contribute to a health savings account to save for future healthcare expenses.

- Medicare Planning: Understand your Medicare coverage options and choose the plan that best meets your needs.

- Long-Term Care Insurance: Consider purchasing long-term care insurance to cover potential costs associated with nursing homes or home healthcare.

Addressing healthcare costs proactively ensures you can afford quality care without jeopardizing your financial security.

5.2. Adapting to Early Retirement

Many workers retire earlier than planned due to layoffs, health issues, or caregiving responsibilities. Adapting to early retirement requires careful planning and adjustments.

Strategies for Adapting to Early Retirement:

- Reassess Your Budget: Evaluate your expenses and make adjustments to align with your reduced income.

- Explore Part-Time Work: Consider part-time work or consulting to supplement your income and stay active.

- Delay Social Security: If possible, delay claiming Social Security benefits to increase your monthly payment.

Adapting to early retirement involves flexibility, creativity, and a willingness to adjust your plans. With careful planning, you can maintain a comfortable lifestyle despite retiring earlier than expected.

5.3. Combating Inflation’s Impact

Inflation erodes the purchasing power of your savings, making it essential to plan for rising costs during retirement.

Strategies for Combating Inflation:

- Inflation-Protected Securities: Invest in Treasury Inflation-Protected Securities (TIPS) or other inflation-protected assets.

- Adjust Your Withdrawal Rate: Periodically review your withdrawal rate and adjust it to keep pace with inflation.

- Diversify Your Investments: Diversify your investment portfolio to include assets that tend to outpace inflation, such as real estate or commodities.

Combating inflation requires proactive planning and a willingness to adjust your strategies as needed. By staying informed and adapting to changing economic conditions, you can protect your retirement income from the impact of inflation.

6. Real-Life Examples and Success Stories

6.1. Case Study: The Power of Affiliate Marketing

Consider the story of John, a retired teacher who partnered with an online education platform to promote their courses. Through affiliate marketing, John earns a commission on every student who enrolls through his referral links. This partnership provides a steady stream of passive income, allowing John to pursue his passion for travel without financial worries.

6.2. Case Study: Generating Income Through Property Management

Meet Mary, a retired executive who partnered with a property management company to oversee her rental properties. The property manager handles tenant screening, maintenance, and rent collection, allowing Mary to generate income without the day-to-day responsibilities of property management. This partnership provides a reliable source of passive income, enabling Mary to enjoy a comfortable retirement.

6.3. Case Study: Collaboration to Develop Online Courses

Consider the story of David, a retired engineer who partnered with a local university to create online courses. Through this collaboration, David shares his expertise with students around the world, earning royalties on course sales. This partnership provides a fulfilling and financially rewarding way for David to stay active and engaged during retirement.

These success stories illustrate the potential of strategic partnerships to enhance retirement income and provide a fulfilling lifestyle. Explore partnership opportunities that align with your skills and interests to create your own success story.

Diversifying investment portfolio during retirement

Diversifying investment portfolio during retirement

7. Actionable Steps to Secure Your Retirement Income

7.1. Assessing Your Current Financial Situation

Begin by assessing your current financial situation. Gather information about your income, expenses, assets, and liabilities. This assessment provides a clear picture of your starting point and helps you identify areas for improvement.

Key Steps:

- Calculate Your Net Worth: Determine your assets (e.g., savings, investments, real estate) and subtract your liabilities (e.g., debts, loans).

- Track Your Expenses: Monitor your spending habits to identify areas where you can reduce costs.

- Review Your Credit Report: Check your credit report for errors and address any issues that could impact your financial health.

7.2. Setting Realistic Retirement Goals

Set realistic retirement goals based on your lifestyle aspirations and financial circumstances. Consider factors such as your desired retirement age, location, and activities.

Key Considerations:

- Retirement Age: Determine when you plan to retire and how long you expect to live in retirement.

- Location: Consider where you want to live during retirement and the associated cost of living.

- Activities: Factor in the costs of hobbies, travel, and other activities you plan to pursue.

7.3. Exploring Partnership Opportunities on income-partners.net

Explore partnership opportunities on income-partners.net to diversify your income streams and enhance your financial security.

How to Use income-partners.net:

- Create a Profile: Create a detailed profile highlighting your skills, interests, and financial goals.

- Browse Opportunities: Browse partnership opportunities that align with your profile and interests.

- Connect with Partners: Connect with potential partners and discuss collaboration opportunities.

income-partners.net provides the tools and resources you need to find strategic partners and build a secure retirement income.

8. Expert Advice and Recommendations

8.1. Seeking Guidance from Financial Advisors

Consider seeking guidance from a qualified financial advisor to create a personalized retirement plan.

Benefits of Working with a Financial Advisor:

- Personalized Advice: Financial advisors provide tailored advice based on your specific situation and goals.

- Investment Management: They can help you manage your investments and create a diversified portfolio.

- Retirement Planning: Financial advisors can assist with retirement planning, Social Security optimization, and estate planning.

8.2. Staying Informed About Market Trends

Stay informed about market trends and economic conditions that could impact your retirement savings.

Resources for Staying Informed:

- Financial News Outlets: Follow reputable financial news outlets for updates on market trends and economic developments.

- Industry Reports: Review industry reports and research to gain insights into specific sectors.

- Professional Conferences: Attend professional conferences and seminars to network with industry experts and learn about new trends.

Staying informed about market trends and economic conditions allows you to make informed decisions and adjust your retirement plan as needed.

8.3. Continuous Learning and Adaptation

Retirement planning is an ongoing process that requires continuous learning and adaptation. Stay open to new ideas, strategies, and opportunities.

Strategies for Continuous Learning:

- Read Books and Articles: Read books and articles on retirement planning, investing, and personal finance.

- Attend Workshops and Seminars: Attend workshops and seminars to learn about new strategies and techniques.

- Network with Peers: Network with other retirees and share insights and experiences.

Continuous learning and adaptation are essential for navigating the complexities of retirement planning and ensuring long-term financial security.

9. FAQs: Planning for a Comfortable Retirement Income

9.1. How Much Money Do I Realistically Need to Retire Comfortably?

You typically need enough money to replace about 80% of your pre-retirement income. However, the exact amount depends on your lifestyle, expenses, and income sources like Social Security and pensions.

9.2. Can I Retire at 60 with $500,000?

Retiring at 60 with $500,000 is possible but requires careful planning. Consider your retirement goals, projected Social Security income, and whether you have debt. Using the 4% withdrawal rule, you could withdraw about $20,000 annually.

9.3. What Is the Average 401(k) Balance for a 65-Year-Old?

According to Vanguard’s How America Saves 2024 report, the average 401(k) balance for savers 65 and older who didn’t have an outstanding loan was $282,669.

9.4. What Is the $1,000-a-Month Rule for Retirement?

The $1,000-a-month rule for retirement states that you’ll need $240,000 in savings for every $1,000 of monthly retirement income, assuming a 5% annual withdrawal rate.

9.5. How Can Strategic Partnerships Boost My Retirement Income?

Strategic partnerships can generate passive income through affiliate marketing, rental properties, online courses, and other collaborative ventures. This can diversify your income streams and reduce reliance on savings.

9.6. What Role Does Social Security Play in Retirement Income?

Social Security is a significant income source for many retirees, with benefits based on your earnings history and claiming age. Estimating your potential benefits is crucial for comprehensive retirement planning.

9.7. How Do I Address Unexpected Healthcare Costs in Retirement?

Plan for healthcare costs by contributing to a Health Savings Account (HSA), understanding your Medicare options, and considering long-term care insurance.

9.8. What Strategies Can Help Combat Inflation During Retirement?

Combat inflation by investing in inflation-protected securities, adjusting your withdrawal rate, and diversifying your investment portfolio.

9.9. How Can income-partners.net Help Me Find the Right Partners?

income-partners.net provides a diverse network of potential partners across various industries, targeted opportunities aligned with your skills, and expert resources to navigate strategic partnerships.

9.10. What Are the Key Steps to Securing My Retirement Income?

Assess your current financial situation, set realistic retirement goals, explore partnership opportunities on income-partners.net, seek guidance from financial advisors, stay informed about market trends, and continuously learn and adapt.

10. Conclusion: Taking Control of Your Retirement Future

Planning for a comfortable retirement income requires a proactive and strategic approach. By understanding your income needs, exploring diverse income sources, and leveraging resources like income-partners.net, you can confidently chart a course toward a financially secure and fulfilling retirement. Whether you’re just starting your career or approaching retirement age, it’s never too late to take control of your financial future and build the retirement you deserve.

Ready to take the next step?

Visit income-partners.net today to explore partnership opportunities, discover strategies for building passive income, and connect with like-minded individuals who are committed to achieving financial independence. Your dream retirement is within reach – start planning today!

Address: 1 University Station, Austin, TX 78712, United States

Phone: +1 (512) 471-3434

Website: income-partners.net