What Income Qualifies For Covered California? The answer lies within the Federal Poverty Level (FPL) and your household details, which income-partners.net breaks down to help you understand eligibility for financial assistance. Knowing this, you can figure out how to get help paying for health coverage.

At income-partners.net, we understand that navigating income qualifications can be complex. We aim to simplify this process, ensuring you can easily access affordable healthcare through income assessments, healthcare subsidies, and financial aid programs. Let us help you explore the opportunities for affordable care, healthcare access, and governmental aid that are available.

1. Decoding Covered California Income Limits: A Comprehensive Guide

Covered California uses income limits to decide who gets financial help and what kind of health coverage they can get. To get help from the government, people’s household income must be between 0% and 400% of the Federal Poverty Level (FPL). Your household income figures out if you can get help from Covered California or Medi-Cal.

To be eligible for coverage, these criteria need to be met:

- You have to live in California.

- You can’t be in Medicare or have healthcare from your job.

- You have to be a lawfully present immigrant.

Keep in mind that free health insurance plans exist; California’s low-income cutoffs are below $47,520 annually. Families of four with earnings below California’s median household income — $97,200 yearly — are eligible for government assistance based on their income. The family gets more help from the government if their net household income is lower. Tax deductions can reduce your income level.

Where does Medi-Cal fit in? Medi-Cal, which is California’s Medicaid program, gives health coverage to low-income households that are eligible. It is the state’s health insurance marketplace about Covered California.

Decoding Covered California income limits

Decoding Covered California income limits

2. Variables Affecting Covered California Income Limits

Income limits depend on three things: the sources of income, how the household is set up (like families with different immigration statuses), and if the income changes with the seasons, which can affect applications. These things decide if someone or a family can get Covered California and Medi-Cal.

2.1. Modified Adjusted Gross Income (MAGI)

MAGI includes your adjusted gross income from your tax return, plus a few other things, like:

- Interest that isn’t taxed.

- Social Security benefits that aren’t taxed.

- Money earned and housing costs from working in another country.

2.2. Federal Poverty Level (FPL)

The FPL, which the Department of Health and Human Services (HHS) releases every year, changes based on household size and how fast prices are rising. It decides if you can get different government support programs and subsidies. Here are the estimated numbers for 2024:

- $14,580 for one person

- $19,720 for two people

- $24,860 for three people

- $30,000 for four people

2.3. Medi-Cal Income Limits

Medi-Cal income limits are a percentage of the FPL. They vary by group:

| Adults (19-64) | Children (Under 19) | Pregnant Women | Aged, Blind, or Disabled | |

|---|---|---|---|---|

| Income Limit | Up to 138% of FPL | Up to 266% of FPL | Up to 213% of FPL | Generally up to 138% of FPL |

| Additional Information | Varies based on income and assets | |||

| Source | ca.db101.org |

3. Exploring Health Plans Based on Income in California

Health plans come in four levels: Bronze, Silver, Gold, and Platinum. Bronze plans have lower premiums but higher out-of-pocket costs, while Platinum plans have higher premiums but lower out-of-pocket costs. To pick the right plan, you need to think about the premiums and what you’re okay with paying when you need medical care.

All plans include basic health benefits, many preventive services, and a network of doctors and hospitals. Staying in the network helps lower your costs. Open enrollment usually runs from November 1 to January 31, which is when you can sign up for a plan. If you want to enroll outside this time, you need a qualifying life event, like getting married, having a baby, or losing your job.

| Bronze | Silver | Gold | Platinum | |

|---|---|---|---|---|

| Premiums | Lowest | Moderate | Higher | Highest |

| Out-of-Pocket Costs | Highest | Moderate | Lower | Lowest |

| Coverage | Covers about half of your health costs | Covers more than half, with cost-sharing reductions | Covers most of your health costs | Covers almost all of your health costs |

| Ideal For | Low monthly premiums | Those who qualify for cost-sharing reductions | Willing to pay higher monthly premiums | Those who need a lot of care and can pay higher premiums |

3.1. Silver-Enhanced Plans On Income

Depending on your California salary, you might get Cost Sharing Reduction (CSR) on Silver Plans:

- 0% – 138% of FPL: You qualify for Medi-Cal.

- Greater than 138% – 400% of FPL: You qualify for a subsidy on a Covered California plan.

- Greater than 138% to 150%: You also qualify for the Silver Enhanced 94 Plan.

- Greater than 150% to 200%: You also qualify for the Silver Enhanced 87 Plan.

- Greater than 200% to 250%: You qualify for the Silver Enhanced 73 Plan.

Keep in mind, kids qualify for Medi-Cal up to 266% of the FPL. So, they don’t qualify for CSR or Enhanced Silver Plans 73, 87, or 94. According to Covered California income guidelines and salary restrictions, if someone or a family makes less than 400% of the FPL, they can get government help based on their income.

4. Understanding Health Insurance Income Limits During Pregnancy

In California, pregnant women have higher income limits for health coverage through Medi-Cal, which makes sure they get full care during their pregnancy. If they make more than the Medi-Cal limits, Covered California’s financial help still makes their healthcare more affordable.

According to the Affordable Care Act, all marketplace and Medicaid plans have to cover pregnancy and childbirth. You can get pregnancy coverage even if you’re already pregnant when you apply. Health coverage matters when you’re planning to have a baby because:

- It makes it easier to get prenatal care: Pregnant women should see their doctors often during pregnancy to check how things are going and find any problems. Finding problems early helps keep you and your baby healthy.

- It makes the delivery affordable: The U.S. is known for high costs for delivery and maternity care. You might have to pay some money yourself. But, depending on your income and health coverage, insurance can cut the cost of delivery a lot.

- It gives you access to emergency care: Everyone wants a healthy pregnancy, but problems can happen. Getting quick emergency treatment can help save you and your baby.

A pregnant woman in California accessing healthcare

A pregnant woman in California accessing healthcare

Since having health coverage and healthcare is key during pregnancy, the income rules for pregnant women are a bit different than for people who aren’t pregnant. Here’s what you might qualify for, based on your income:

- Medi-Cal: If you make between 138% and 213% of the poverty level, you might get MAGI Medi-Cal while you’re pregnant.

- Medi-Cal Access Program (MCAP): The Covered California income limits for MCAP are between 213% and 322% of the poverty level. MCAP charges a small fee and gives full coverage to pregnant people.

When you apply for Medi-Cal while pregnant, they assume you’re eligible while they check your application. That means you can get coverage right away, so you and your baby get the care you need.

5. Exploring Income Limits for Medi-Cal for Families With Children

For adults to qualify for Medi-Cal, their household income needs to be less than 138% of the FPL. But, according to the Covered California income guide, kids can get Medi-Cal if their family’s income is 266% or less. The kids have to be under 19 to qualify. C-CHIP, which is the County Children’s Health Initiative Program, also offers health coverage for kids if the family income is more than 266% and up to 322% of the FPL.

6. How To Provide Proof of Income for Covered California

The proof of income you need for your Covered California application depends on whether you’re self-employed or work for someone else. If you work for someone else, you’ll need:

- Your most recent pay stubs, showing how much you’ve earned this year

- Your W-2 forms from last year (if you don’t have these, a letter from your employer confirming your income)

If you’re self-employed, you need to gather:

- 1099 Forms from businesses or clients who paid you

- Your most recent tax return, including any extra forms

- A statement showing your income and expenses for the current year

- Bank statements showing deposits from your self-employment income

If you have other income sources, add these documents to your application:

- A benefits letter from the Social Security Administration

- Documents showing your pension or retirement income

- Documents confirming any unemployment benefits you’ve received

- Legal documents showing alimony you’ve received

- Statements from your investment accounts showing dividends or interest

To make your application go faster, send your documents in quickly and make sure they’re easy to read. Fill out all the parts of any forms that have multiple pages.

7. Reporting Mid-Year Changes in Household Earnings

If your California income goes up during the year, it might change the subsidies you can get from Covered California. It might also change if you, your spouse, or your kids can get certain government assistance programs. If your income changes a lot in the middle of the year, you might need to tell Covered California or Medi-Cal.

Reporting these changes helps make sure you get the right amount of financial help, and it can help you avoid problems later. Changes to report include raises or cuts in wages, changes in self-employment income, changes in unemployment benefits, and one-time payments like bonuses or inheritances. You should also report changes in your household, like getting married or divorced, having a baby, the death of a family member, or a dependent who is no longer eligible for coverage because of their age.

You should also report any changes to your taxes, address, or other health coverage. Reporting these changes helps you keep your coverage, gives you a chance to change your health plan, and helps you get the right subsidy.

8. Get a Quote and Calculate Your Covered California Discount

Knowing the income limits for Covered California is key. This info will help you see if you can get help and how much financial help you might get for health insurance. Once you know what you want to apply for, gather the documents you need and fill them out quickly to make the process easier.

If you need health insurance or help paying for it, you might be able to get Medi-Cal or a subsidy. Income-partners.net can help you find out if you can get a subsidized or Medi-Cal plan based on your income and situation.

Navigating Covered California can feel overwhelming. But with the right insights and resources, finding affordable health coverage is within reach. Understanding the income thresholds, exploring available plans, and gathering necessary documentation are key steps in this process.

Ready to take control of your health coverage? Visit income-partners.net today to explore personalized solutions, discover potential partnerships, and unlock opportunities for financial growth. Don’t wait, your path to affordable healthcare and strategic alliances starts now!

9. Frequently Asked Questions (FAQs) About Covered California Income Qualifications

Here are some frequently asked questions about income and Covered California:

9.1. What is the income limit to qualify for Covered California?

The income limit to qualify for Covered California varies based on household size but generally ranges from 0% to 400% of the Federal Poverty Level (FPL). For individuals, this can be up to approximately $58,320 per year in 2024, while for a family of four, it can be up to $120,000. These limits are updated annually.

9.2. How does Covered California calculate income?

Covered California uses Modified Adjusted Gross Income (MAGI) to determine eligibility. MAGI includes your adjusted gross income plus any tax-exempt interest, non-taxable Social Security benefits, and foreign earned income.

9.3. What happens if my income changes during the year?

If your income changes significantly during the year, you must report the change to Covered California. This may affect your eligibility for subsidies and cost-sharing reductions. Reporting changes promptly ensures you receive the correct amount of financial assistance.

9.4. Can I still get Covered California if my income is too high?

Even if your income is above 400% of the FPL, you may still be eligible for a federal premium tax credit to lower your premium to a maximum of 8.5% of your income, based on the second-lowest-cost Silver plan in your area.

9.5. What if I am self-employed? How do I prove my income?

Self-employed individuals can provide proof of income through 1099 forms, tax returns, a statement detailing current income and expenses, and bank statements showing self-employment income.

9.6. Do children have different income limits for Medi-Cal?

Yes, children may qualify for Medi-Cal with a higher household income limit compared to adults. Children under 19 may be eligible if the family income is at or below 266% of the FPL.

9.7. How do income limits differ for pregnant women?

Pregnant women in California have access to increased income limits for healthcare coverage through Medi-Cal. If their income falls between 138% and 213% of the poverty level, they may qualify for MAGI Medi-Cal during pregnancy.

9.8. What are Silver-Enhanced Plans, and how do they relate to income?

Silver-Enhanced Plans provide additional cost-sharing reductions based on income. Individuals with incomes between 138% and 250% of the FPL may qualify for these plans, which offer lower out-of-pocket costs.

9.9. What is the difference between Covered California and Medi-Cal?

Covered California is the state’s health insurance marketplace where individuals and families can purchase health insurance plans. Medi-Cal is California’s Medicaid program, providing free or low-cost health coverage to eligible low-income residents.

9.10. Where can I get help understanding my options and applying?

income-partners.net provides resources and information to help you understand your options and navigate the application process. Additionally, you can get assistance from certified enrollers or by contacting Covered California directly.

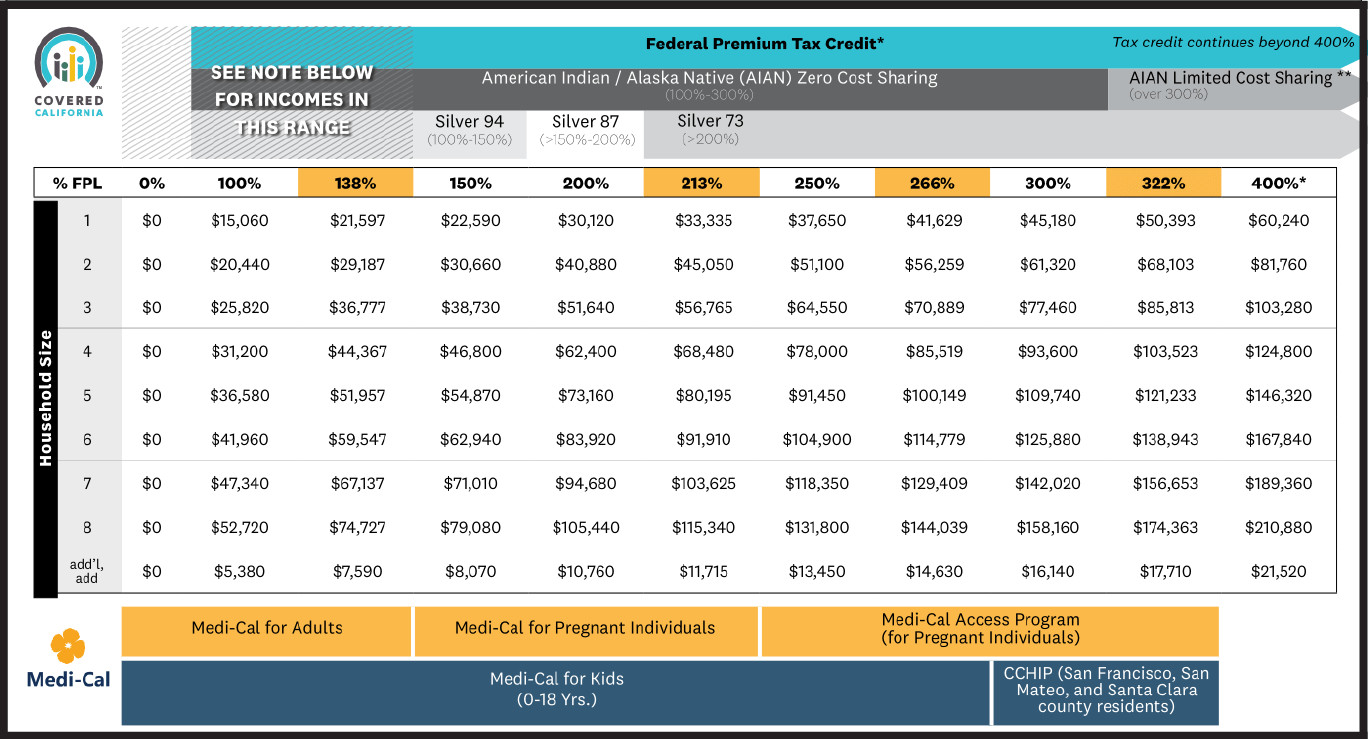

10. 2025 Income Chart

Your financial help and whether you qualify for various Covered California or Medi-Cal programs depends on your income, based on the Federal Poverty Level (FPL).

Covered California program eligibility by federal poverty level table

Covered California program eligibility by federal poverty level table

* Consumers at 400% FPL or higher may receive a federal premium tax credit to lower their premium to a maximum of 8.5 percent of their income based on the second-lowest-cost Silver plan in their area.