Is understanding how your income affects your Medicare premiums a source of confusion? Income plays a significant role in calculating Medicare Part B premiums, and at income-partners.net, we’re here to simplify the process and help you navigate potential partnership opportunities to enhance your income while strategically planning for your healthcare costs. By understanding the factors that influence your premiums, you can make informed financial decisions, potentially discover new revenue streams through strategic partnerships, and optimize your overall financial well-being. Let’s delve into how income impacts your Medicare premiums and how you can plan effectively, and consider how partnership could bring more abundance to your future.

1. How Is Medicare Part B Premium Determined?

Your Medicare Part B premium is primarily determined by your income. The standard monthly premium for Medicare Part B in 2023 was $164.90, but this amount can be higher depending on your income level. According to the Centers for Medicare & Medicaid Services (CMS), about 7% of Medicare beneficiaries pay more than the standard premium, through what’s known as the Income-Related Monthly Adjustment Amount (IRMAA).

1.1 What is the Income-Related Monthly Adjustment Amount (IRMAA)?

The Income-Related Monthly Adjustment Amount (IRMAA) is an additional charge tacked onto your standard Medicare Part B and Part D premiums, based on your modified adjusted gross income (MAGI). This means high-income earners pay more for their Medicare coverage.

1.2 How Does the Social Security Administration (SSA) Determine IRMAA?

The Social Security Administration (SSA) determines your IRMAA using your MAGI from two years prior to the current premium year. For example, your 2023 Medicare premiums were based on your 2021 MAGI. The SSA obtains this information from the IRS.

1.3 What Happens if the IRS Cannot Provide MAGI Information?

If the IRS cannot provide MAGI information for the relevant tax year (e.g., due to an extension or non-filing), the SSA will use tax information from three years prior to the premium year. Once the MAGI for two years prior becomes available, the IRMAA will be adjusted accordingly.

2. What Income Counts Towards Medicare Premiums?

Modified Adjusted Gross Income (MAGI) is the key income measure used to determine Medicare premiums. MAGI includes your adjusted gross income (AGI) plus certain tax-exempt income.

2.1 What is Included in Modified Adjusted Gross Income (MAGI)?

MAGI for Medicare premium purposes includes:

- Adjusted Gross Income (AGI): This is your gross income minus certain deductions, such as contributions to traditional IRAs, student loan interest, and self-employment taxes.

- Tax-Exempt Interest Income: This includes interest from state and local bonds.

- Other Tax-Exempt Income: This may include income excluded under specific sections of the Internal Revenue Code (IRC), such as income from U.S. savings bonds used for higher education tuition and fees.

- Foreign Earned Income Exclusion: As noted in Congressional Research Service Report The Use of Modified Adjusted Gross Income (MAGI) in Federal Health Programs), this includes earned income of U.S. citizens living abroad that was excluded from gross income.

- Income from U.S. Territories: This includes income from sources within Guam, American Samoa, the Northern Mariana Islands, or Puerto Rico not otherwise included in AGI.

2.2 How Does Capital Gains Impact Medicare Premiums?

Capital gains are included in your adjusted gross income (AGI), which is a component of your MAGI. Therefore, realizing significant capital gains can increase your MAGI and potentially raise your Medicare Part B premiums.

2.3 How Do Retirement Account Withdrawals Affect Medicare Premiums?

Withdrawals from taxable retirement accounts, such as 401(k)s and traditional IRAs, are also included in your AGI. Large taxable withdrawals can significantly increase your MAGI and, consequently, your Medicare premiums.

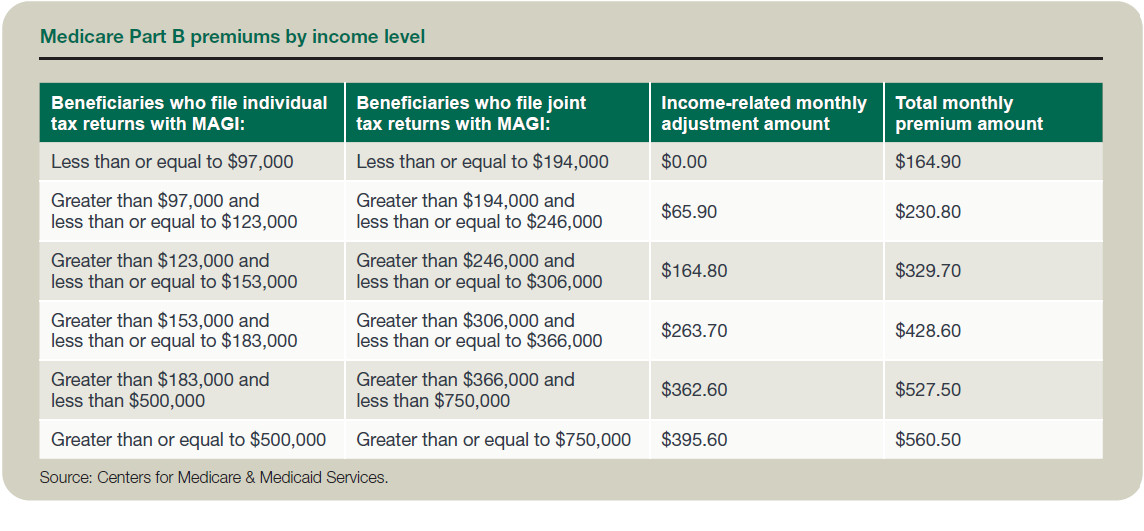

3. Medicare Part B Premiums by Income Level: A Detailed Breakdown

Medicare Part B premiums are structured in tiers based on income levels. Higher income levels result in higher monthly premiums.

3.1 2023 Medicare Part B Premium Brackets

Here’s a breakdown of the 2023 Medicare Part B premiums based on individual and joint filing income levels (based on 2021 MAGI):

| Individual MAGI | Joint Filing MAGI | Monthly Premium | |

|---|---|---|---|

| Standard Premium | Up to $91,000 | Up to $182,000 | $164.90 |

| IRMAA Tier 1 | $91,001 to $114,000 | $182,001 to $228,000 | $230.80 |

| IRMAA Tier 2 | $114,001 to $142,000 | $228,001 to $284,000 | $329.70 |

| IRMAA Tier 3 | $142,001 to $170,000 | $284,001 to $340,000 | $428.60 |

| IRMAA Tier 4 | $170,001 to $500,000 | $340,001 to $750,000 | $527.50 |

| IRMAA Tier 5 | Over $500,000 | Over $750,000 | $560.50 |

3.2 2024 Medicare Part B Premium Brackets

Here’s a breakdown of the 2024 Medicare Part B premiums based on individual and joint filing income levels (based on 2022 MAGI):

| Individual MAGI | Joint Filing MAGI | Monthly Premium | |

|---|---|---|---|

| Standard Premium | Up to $103,000 | Up to $206,000 | $174.70 |

| IRMAA Tier 1 | $103,001 to $129,000 | $206,001 to $258,000 | $244.60 |

| IRMAA Tier 2 | $129,001 to $161,000 | $258,001 to $322,000 | $349.60 |

| IRMAA Tier 3 | $161,001 to $193,000 | $322,001 to $386,000 | $454.50 |

| IRMAA Tier 4 | $193,001 to $500,000 | $386,001 to $750,000 | $559.40 |

| IRMAA Tier 5 | Over $500,000 | Over $750,000 | $594.00 |

3.3 Why Is There a Two-Year Lag in Income Calculation?

The two-year lag exists because the SSA relies on tax data from the IRS, which takes time to process and finalize. This lag can make it challenging to plan accurately, as your current income may differ significantly from your income two years prior.

4. Appealing Medicare Premium Determinations

If you disagree with the SSA’s determination of your Medicare Part B premium, you have the right to appeal.

4.1 How Can You Initiate an Appeal?

You can initiate an appeal by completing Form SSA-561-U2, Request for Reconsideration. This form allows you to provide additional information or documentation to support your case.

4.2 Where Can You Find More Information on Appealing Medicare Part B Premium Determinations?

For detailed information on appealing Medicare Part B premium determinations, refer to the SSA’s Medicare Annual Verification Notices: Frequently Asked Questions. This resource provides answers to common questions about the appeal process.

4.3 What Is Form SSA-561-U2?

Form SSA-561-U2 is the official form used to request a reconsideration of a decision made by the Social Security Administration (SSA). You can use this form to appeal a Medicare Part B premium determination if you believe it is incorrect.

5. Life-Changing Events and Their Impact on Medicare Premiums

Certain life-changing events can significantly reduce your income and may qualify you for a reduction in your monthly IRMAA.

5.1 What Life-Changing Events Can Affect Your Medicare Premiums?

According to Section 2507 of the Social Security Handbook, the following life-changing events may warrant a reduction in your IRMAA:

- Marriage

- Divorce or annulment

- Death of your spouse

- Work stoppage

- Work reduction

- Loss of income-producing property

- Loss or reduction of pension income

- Receipt of employer settlement payment

5.2 How Can You Request a Reduction in Your IRMAA Due to a Life-Changing Event?

You can request a reduction in your monthly IRMAA by filing Form SSA-44, Medicare Income-Related Monthly Adjustment Amount — Life-Changing Event. Alternatively, you can schedule an interview with your local SSA office.

5.3 What is Form SSA-44?

Form SSA-44, Medicare Income-Related Monthly Adjustment Amount — Life-Changing Event, is used to inform the Social Security Administration (SSA) of a life-changing event that has significantly reduced your income.

6. Penalties for Late Enrollment in Medicare Part B

Failing to enroll in Medicare Part B when first eligible can result in significant lifetime penalties.

6.1 What Is the Penalty for Late Enrollment in Medicare Part B?

The penalty for late enrollment in Medicare Part B is an additional 10% to the current Part B premium for each full 12-month period that you could have had Part B coverage but did not enroll. This penalty is lifelong. (See Medicare’s “Avoid Late Enrollment Penalties” page.)

6.2 Can Late Enrollment Penalties Apply to Other Parts of Medicare?

Yes, additional late enrollment penalties can also apply for Part A and/or Part D coverage. It’s important to enroll in all parts of Medicare when first eligible to avoid these penalties.

6.3 Is Part A Premium-Free?

Part A is premium-free for those who paid Medicare taxes for at least 10 years. Enrollment in Part A is automatic for anyone collecting Social Security benefits.

7. Strategic Planning to Minimize Medicare Premiums

Planning around the IRMAA can be challenging due to the two-year lag in income calculation, but strategic financial planning can help minimize the impact of income on your Medicare premiums.

7.1 What Are Some Basic Planning Techniques to Minimize Medicare Premiums?

Basic planning techniques include:

- Deferring Income: Delaying income to future years can help keep your MAGI below the threshold for higher premiums in the current year.

- Accelerating Above-the-Line Deductions: Increasing deductions such as contributions to traditional IRAs can reduce your AGI and, consequently, your MAGI.

7.2 How Can the Sale of Investments Affect Medicare Premiums, and What Strategies Can Be Used to Mitigate This Impact?

The sale of investments or other assets can lead to unexpected increases in your Medicare Part B premiums.

Structuring sales using the installment method or selling assets over several tax years may be effective to avoid an income spike in a single year. Gifting assets versus selling them might be another option to consider.

7.3 How Can Retirement Account Planning Help Minimize Medicare Premiums?

Those who are still working may be able to make additional contributions to their retirement accounts. Maximize contributions to cash-or-deferred arrangements, and explore contributions to individual retirement accounts (IRAs), including spousal IRAs.

8. Retirement Account Strategies and Medicare Premiums

Careful planning with retirement accounts can help manage your MAGI and minimize your Medicare premiums.

8.1 How Do Required Minimum Distributions (RMDs) Impact Medicare Premiums?

Required Minimum Distributions (RMDs) from retirement accounts are included in your AGI and can increase your MAGI. Planning when and how to take RMDs is crucial to managing your Medicare premiums.

8.2 Can RMDs from Employer-Sponsored Plans Be Deferred?

Yes, RMDs from employer-sponsored plans are not required as long as you are still working. Terminating employment on January 1 will count as another year for RMD deferral purposes.

8.3 What Are the Implications of Roth Conversions on Medicare Premiums?

Making a Roth conversion before enrolling in Part B or doing the conversion in a single year can significantly increase your MAGI. While Roth conversions can offer long-term tax benefits, it’s important to consider the immediate impact on your Medicare premiums.

9. Partnership Opportunities to Offset Medicare Costs

Exploring partnership opportunities can provide additional income streams that may help offset the costs of higher Medicare premiums.

9.1 What Types of Partnerships Can Help Increase Income?

Consider various partnership models, such as:

- Strategic Alliances: Collaborating with other businesses to offer complementary products or services.

- Joint Ventures: Partnering with another entity to undertake a specific project or venture.

- Affiliate Marketing: Earning commissions by promoting other companies’ products or services.

- Distribution Partnerships: Partnering with distributors to expand your market reach.

9.2 How Can Income-Partners.Net Help You Find Suitable Partnership Opportunities?

Income-partners.net provides a platform to connect with potential partners, explore various partnership models, and discover opportunities to increase your income.

9.3 What Resources Does Income-Partners.Net Offer for Building Successful Partnerships?

Income-partners.net offers resources such as:

- Informational Articles: Providing insights into different types of partnerships and their potential benefits.

- Networking Opportunities: Connecting you with potential partners in various industries.

- Strategic Planning Tools: Helping you assess your partnership goals and identify compatible partners.

Business partnership concept with jigsaw

Business partnership concept with jigsaw

10. Professional Guidance and Resources

Seeking professional guidance can help you navigate the complexities of Medicare premiums and develop a comprehensive financial plan.

10.1 Why Is Professional Guidance Important?

Professionals can analyze your specific financial situation, explain the Medicare Part B premium calculation, and help you make informed decisions to minimize your premiums while maximizing your income.

10.2 What Resources Does AICPA Offer?

The AICPA offers resources such as:

- Guide to Social Security Planning (8th ed.) by Theodore J. Sarenski

- Guide to Retirement & Elder Planning: Healthcare Coverage Planning (6th ed.) by Sullivan

10.3 How Can Knowing the Factors Involved in Medicare Part B Premium Calculation Allow for Effective Planning?

Understanding the factors involved in the calculation of the Medicare Part B premium allows for effective planning, including understanding the consequences of current tax planning choices on future premiums.

Conclusion

Understanding What Income Is Used To Determine Medicare Premiums is crucial for effective financial planning. By understanding how MAGI affects your premiums, exploring partnership opportunities through income-partners.net, and seeking professional guidance, you can make informed decisions to minimize your healthcare costs and maximize your income. Take control of your financial future by exploring partnerships, optimizing your income, and planning strategically for your Medicare premiums.

Ready to explore partnership opportunities and take control of your financial future? Visit income-partners.net today to discover strategies for increasing your income and optimizing your Medicare premiums. Don’t miss out on the chance to connect with potential partners and unlock new opportunities for growth!

FAQ: Understanding Income and Medicare Premiums

1. What happens if my income changes significantly from the year used to calculate my Medicare premium?

If you experience a life-changing event that significantly reduces your income, you can request a re-determination of your Medicare premium by filing Form SSA-44 with the Social Security Administration.

2. Can I deduct my Medicare premiums from my taxes?

You may be able to deduct your Medicare premiums as a medical expense if you itemize deductions on your tax return. However, the amount you can deduct is limited to the amount exceeding 7.5% of your adjusted gross income (AGI).

3. What is the difference between Medicare Part B and Part D, and how is income used to determine premiums for each?

Medicare Part B covers medical services, while Part D covers prescription drugs. Both Part B and Part D premiums are subject to IRMAA based on your modified adjusted gross income (MAGI).

4. How do I report a life-changing event to the Social Security Administration for Medicare premium adjustments?

You can report a life-changing event by completing Form SSA-44, Medicare Income-Related Monthly Adjustment Amount — Life-Changing Event, and submitting it to the Social Security Administration (SSA).

5. Are there any income limits for receiving assistance with Medicare premiums?

Yes, there are income limits for receiving assistance with Medicare premiums through programs like the Medicare Savings Program (MSP). These programs help individuals with limited income and resources pay for their Medicare premiums and other healthcare costs.

6. What if I disagree with the Social Security Administration’s determination of my Medicare premium?

If you disagree with the Social Security Administration’s (SSA) determination of your Medicare premium, you have the right to appeal. You can initiate an appeal by completing Form SSA-561-U2, Request for Reconsideration.

7. How does tax-exempt income affect my Medicare premiums?

Tax-exempt income, such as interest from state and local bonds, is included in your modified adjusted gross income (MAGI), which is used to determine your Medicare premiums.

8. Can I reduce my Medicare premiums by contributing to a health savings account (HSA)?

Contributing to a health savings account (HSA) can reduce your adjusted gross income (AGI), which is a component of your modified adjusted gross income (MAGI). This can potentially lower your Medicare premiums.

9. What are the income thresholds for IRMAA in 2024?

As an individual, if your modified adjusted gross income is above $103,000, you’ll pay more than the standard premium. As a couple filing jointly, that threshold is $206,000.

10. How does delaying Social Security benefits impact my future Medicare premiums?

Delaying Social Security benefits does not directly impact your Medicare premiums. However, delaying Social Security benefits can result in a higher monthly benefit amount, which may indirectly affect your overall financial situation and ability to pay for healthcare costs, including Medicare premiums.