What Happens If A Simple Trust Does Not Distribute Income? In short, the trust will be liable for income taxes. Income-partners.net can help you navigate these complex situations and find strategic partnerships that maximize your income and minimize tax burdens. Learn how to optimize your trust management and unlock new financial opportunities with expert insights and resources. Boost your income and partnership potential today!

1. Understanding Simple Trusts and Income Distribution

What is a Simple Trust?

A simple trust is a legal arrangement where the trustee is required to distribute all of its income currently, cannot make charitable contributions, and does not distribute principal, as defined by Regs. Sec. 1.651(a)-1. Understanding this definition is crucial for managing your trust effectively and avoiding potential tax issues, according to legal experts at income-partners.net.

What Constitutes Income in a Simple Trust?

Income in a simple trust typically includes dividends, interest, and other forms of current earnings. This income is distinct from capital gains, which are usually considered part of the principal and taxed at the trust level. Understanding what constitutes income is essential for proper distribution and tax planning.

What is the Role of the Trustee in Income Distribution?

The trustee plays a vital role in ensuring that all income is distributed according to the trust agreement and applicable laws. This involves accurately calculating the trust’s income, managing expenses, and making timely distributions to the beneficiaries. Effective trust administration is critical to maintaining compliance and maximizing benefits.

2. The Tax Cuts and Jobs Act (TCJA) and Its Impact on Simple Trusts

How Did the TCJA Change the Taxation of Simple Trusts?

The Tax Cuts and Jobs Act (TCJA) brought significant changes to the taxation of simple trusts, primarily by eliminating the deductibility of miscellaneous itemized deductions subject to the 2% floor of adjusted gross income (AGI) for tax years 2018 through 2025, under Sec. 67. This change has a profound impact on how taxable income is calculated for simple trusts.

What are Miscellaneous Itemized Deductions and Why Were They Important?

Miscellaneous itemized deductions include expenses like investment advisory fees, which were previously deductible. The elimination of these deductions means that while these expenses are still factored into trust accounting income (TAI), they are no longer deductible when calculating taxable income and distributable net income (DNI).

How Does the TCJA Affect the Calculation of Trust Accounting Income (TAI) and Distributable Net Income (DNI)?

The TCJA has created a disparity between TAI and DNI. TAI is the trust’s income as calculated by the terms of the trust’s governing document and local law, while DNI is used for the income taxation of estates, trusts, and their beneficiaries. The disallowance of 2% itemized deductions means that DNI can now be greater than TAI, which can lead to unexpected tax liabilities at the trust level.

3. Consequences of Not Distributing Income

What Happens If a Simple Trust Does Not Distribute All of Its Income?

If a simple trust does not distribute all of its income, the undistributed income is taxed at the trust level. This can result in an unexpected tax liability, as simple trusts are typically designed to avoid taxation at the trust level by distributing all income to beneficiaries.

How Does the Disallowance of Certain Deductions Lead to Undistributed Income?

The disallowance of miscellaneous itemized deductions, such as investment advisory fees, means that DNI can be higher than TAI. If the trustee distributes an amount equal to TAI, there will still be taxable income remaining at the trust level, as the distribution will be less than DNI.

What is the Tax Rate on Undistributed Income in a Simple Trust?

Undistributed income in a simple trust is taxed at the trust income tax rates, which can be quite high. For example, in 2024, trusts reach the highest tax bracket of 37% at a much lower income threshold compared to individual taxpayers.

4. Understanding Trust Accounting Income (TAI) vs. Distributable Net Income (DNI)

What is Trust Accounting Income (TAI) and How is it Calculated?

Trust Accounting Income (TAI) is the income of the trust as determined by the trust agreement and applicable local law. It represents the amount that the trustee is required to distribute to the beneficiaries. The calculation of TAI involves determining the trust’s income according to state law and the trust document.

What is Distributable Net Income (DNI) and How is it Calculated?

Distributable Net Income (DNI) is a tax concept used to determine the amount of income that is taxable to the beneficiaries. DNI acts as the upper limit for the distribution deduction that the trust can claim. It is calculated by adjusting the trust’s taxable income, and is critical for determining the tax implications for both the trust and its beneficiaries.

Why is the Difference Between TAI and DNI Important for Tax Planning?

The difference between TAI and DNI is crucial for tax planning because it determines the amount of income that is taxed at the trust level versus the beneficiary level. When DNI is greater than TAI, the trust may have taxable income even if it distributes all of its TAI, resulting in a tax liability for the trust.

5. Types of Deductions Affected by the TCJA

What Deductions are Considered Miscellaneous Itemized Deductions?

Miscellaneous itemized deductions include various expenses that an individual might deduct, such as investment advisory fees, certain legal fees, and other similar costs. These are detailed under Sec. 67 of the tax code. Understanding which deductions fall into this category is essential for accurate tax planning.

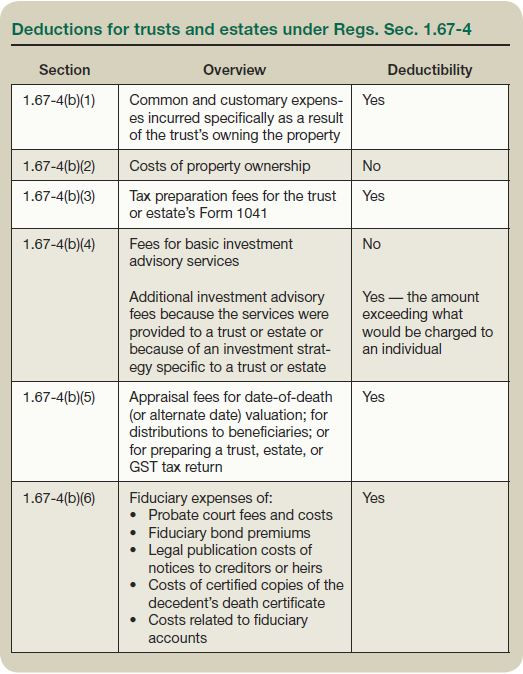

How Does Regs. Sec. 1.67-4 Clarify Deductible vs. Nondeductible Expenses?

Regs. Sec. 1.67-4 provides guidance on which costs are paid or incurred in connection with trust administration, helping to determine if an expense will cause a discrepancy between DNI and TAI. It differentiates between expenses that are fully deductible for an estate or trust versus those that could be incurred by an individual.

What are Ownership Costs and How are They Treated?

Ownership costs are expenses incurred by an owner of property simply by being the owner, such as repairs, maintenance, condo fees, and insurance costs. These costs are generally not deductible for income tax purposes because they could be incurred by individuals, as outlined in Regs. Sec. 1.67-4(b)(2).

Deductions for trusts and estates under Regs. Sec. 1.67-4

Deductions for trusts and estates under Regs. Sec. 1.67-4

6. Exceptions to the Disallowance of Deductions

Are There Any Exceptions Where Investment Advisory Fees Can Still Be Deducted?

Yes, there are exceptions where investment advisory fees can still be deducted. If the costs incurred by the trust exceed those that would be charged to an individual because the services were provided specifically to a trust, or the costs were attributable to an unusual investment objective or the need for a specialized balancing of interests, the additional costs may be deductible.

How Do Appraisal Fees Factor into Deductible Expenses?

Appraisal fees incurred to determine the fair market value of assets for a decedent’s estate or trust, to determine value for distributions to beneficiaries, or to prepare the trust’s income tax return are deductible. These are not costs typically incurred by an individual.

What Other Fiduciary Expenses are Generally Deductible?

Other fiduciary expenses that are not commonly or customarily incurred by individuals and are therefore deductible include probate court fees and costs, fiduciary bond premiums, legal publication costs of notices to creditors or heirs, costs of certified copies of the decedent’s death certificate, and costs related to fiduciary accounts, as discussed in Regs. Sec. 1.67-4(b)(6).

7. State Law and the Uniform Principal and Income Act (UPAIA)

How Does State Law Affect the Calculation of TAI?

The calculation of TAI is significantly influenced by state law, as it defines how income and expenses are allocated between the income and principal of the trust. Preparers must be aware of the specific state law that applies to the trust when preparing its income tax return.

What is the Uniform Principal and Income Act (UPAIA)?

The Uniform Principal and Income Act (UPAIA) provides guidelines for allocating receipts and disbursements between income and principal. Most states have adopted the UPAIA, but with modifications that vary by state.

Why is it Important to Know Which State Law Applies to the Trust?

Knowing which state law applies to the trust is critical because it determines how certain items, such as investment and management fees, are allocated between income and principal. This allocation directly impacts the calculation of TAI and, consequently, the amount of income that must be distributed to the beneficiaries.

8. Real-World Examples and Case Studies

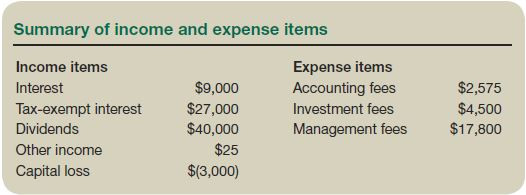

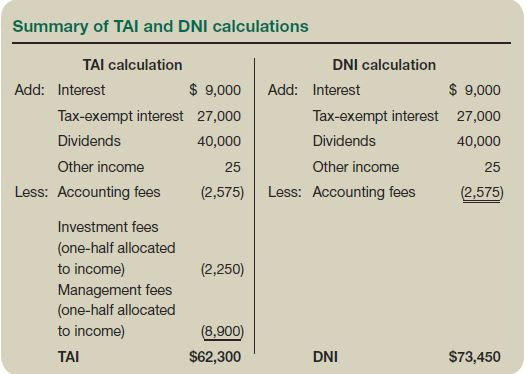

Can You Provide an Example of How the TCJA Impacts a Simple Trust’s Tax Liability?

Consider a trust with $80,000 in dividends, $2,000 in accounting fees, and $18,000 in investment and management fees. Under applicable state law, half of the investment and management fees are allocated to income. The TAI would be $71,000 (80,000 – 9,000). However, the DNI would be $78,000 (80,000 – 2,000). If the trust distributes $71,000, it will have taxable income of $7,000 at the trust level because the investment fees are not deductible for DNI purposes.

How Would This Situation Have Been Different Before the TCJA?

Before the TCJA, the investment and management fees would have been deductible, resulting in a lower DNI. This would have allowed the trust to distribute all of its income without incurring a tax liability at the trust level.

What are the Key Takeaways from These Examples?

The key takeaway is that the TCJA has introduced complexities that require careful planning to avoid unintended tax consequences. Understanding the interplay between TAI, DNI, and the disallowance of certain deductions is essential for effective trust management.

Summary of income and expense items

Summary of income and expense items

Summary of TAI and DNI calculations

Summary of TAI and DNI calculations

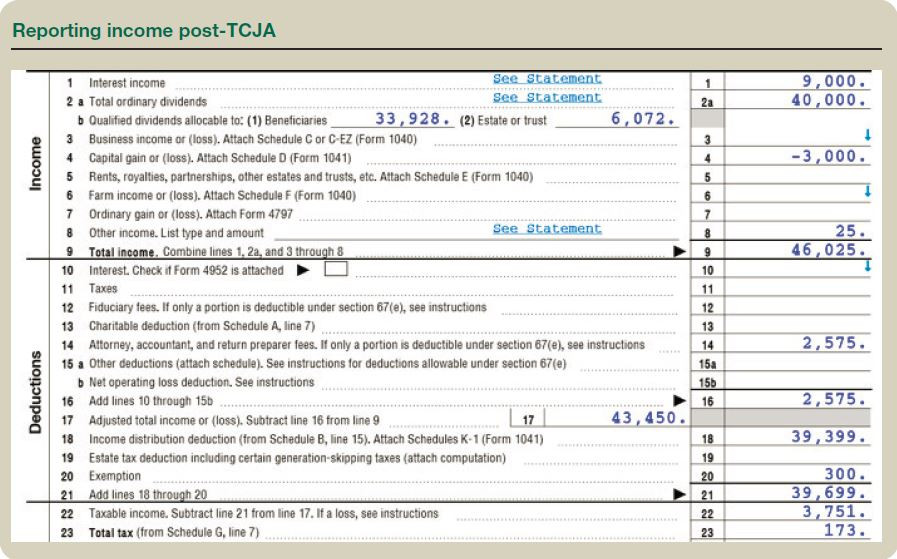

9. Preparing Form 1041 Post-TCJA

What Changes Should Tax Preparers Be Aware of When Filing Form 1041 for Simple Trusts?

Tax preparers need to be particularly aware of the disallowance of miscellaneous itemized deductions and how this affects the calculation of DNI. They should also carefully review the trust agreement and applicable state law to determine the proper calculation of TAI.

How is the Income Distribution Deduction Calculated Under the TCJA?

The income distribution deduction is calculated based on the smaller of the DNI or the amount of income required to be distributed. If DNI is greater than TAI, the distribution deduction will be limited to the TAI amount, potentially resulting in taxable income at the trust level.

What are Some Common Mistakes to Avoid When Preparing Form 1041?

Common mistakes include failing to properly allocate expenses between income and principal, not understanding the nuances of state law, and overlooking the disallowance of miscellaneous itemized deductions. Thoroughness and attention to detail are essential when preparing Form 1041 for simple trusts.

Reporting income post-TCJA

Reporting income post-TCJA

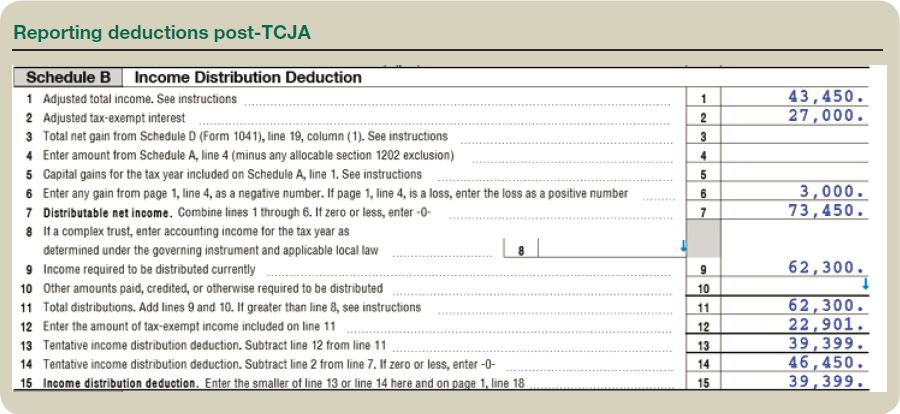

Reporting deductions post-TCJA

Reporting deductions post-TCJA

Reporting income and deductions pre-TCJA

Reporting income and deductions pre-TCJA

10. Strategies for Minimizing Tax Liability

What Strategies Can Trustees Use to Minimize the Tax Liability of a Simple Trust?

Trustees can use several strategies to minimize tax liability, including maximizing deductible expenses that are not subject to the 2% floor, making strategic distributions to beneficiaries, and ensuring that the trust’s investments are tax-efficient.

How Can Strategic Distributions Help Reduce Taxable Income?

Strategic distributions involve distributing income in a way that minimizes the overall tax burden. This might involve distributing income to beneficiaries in lower tax brackets or timing distributions to offset losses.

What Role Does Tax-Efficient Investing Play in Trust Management?

Tax-efficient investing involves choosing investments that generate less taxable income, such as municipal bonds or tax-advantaged accounts. This can help reduce the overall tax liability of the trust and maximize returns for the beneficiaries.

11. The Importance of Professional Advice

Why Should Trustees Seek Professional Advice When Managing Simple Trusts?

Trustees should seek professional advice due to the complexities of trust taxation and the potential for unintended tax consequences. A qualified tax advisor or estate planning attorney can provide valuable guidance and help trustees navigate these issues effectively.

What Type of Professionals Can Assist with Trust Management and Tax Planning?

Professionals who can assist with trust management and tax planning include certified public accountants (CPAs), estate planning attorneys, and financial advisors. These professionals have the expertise and knowledge to help trustees make informed decisions and minimize tax liabilities.

How Can Income-partners.net Help Trustees Find the Right Professionals?

Income-partners.net offers a platform for connecting with experienced professionals who specialize in trust management and tax planning. Our network includes CPAs, attorneys, and financial advisors who can provide the guidance and support you need to effectively manage your simple trust.

12. Staying Compliant with Tax Laws

What Steps Can Trustees Take to Ensure Compliance with Tax Laws?

Trustees can take several steps to ensure compliance with tax laws, including keeping accurate records, filing tax returns on time, and seeking professional advice when needed. Staying informed about changes in tax law is also essential.

How Often Should Trustees Review Their Trust Documents and Tax Plans?

Trustees should review their trust documents and tax plans at least annually, or more frequently if there are significant changes in tax law or the trust’s financial situation. Regular reviews can help identify potential issues and ensure that the trust is managed in a tax-efficient manner.

What Resources are Available for Staying Updated on Tax Law Changes?

Resources for staying updated on tax law changes include the IRS website, professional tax publications, and updates from tax advisory firms. Subscribing to newsletters and attending seminars can also help trustees stay informed.

13. Common Scenarios and Solutions

What Should a Trustee Do If They Realize They Have Not Distributed Enough Income?

If a trustee realizes they have not distributed enough income, they should consult with a tax advisor to determine the best course of action. This might involve making a corrective distribution or filing an amended tax return.

How Can a Trustee Handle Unexpected Expenses That Impact Income Distribution?

If unexpected expenses arise, the trustee should carefully review the trust agreement and applicable state law to determine how to allocate these expenses. Seeking professional advice is also recommended.

What Strategies Can Be Used to Plan for Future Tax Law Changes?

Planning for future tax law changes involves staying informed about potential changes and developing strategies to mitigate their impact. This might include adjusting investment strategies, modifying distribution plans, or seeking legislative changes.

14. The Future of Trust Taxation

What are Some Potential Future Changes in Trust Taxation?

Potential future changes in trust taxation could include modifications to the rules regarding itemized deductions, changes to the trust income tax rates, or revisions to the definition of DNI. Staying informed about these potential changes is crucial for effective trust management.

How Can Trustees Prepare for These Changes?

Trustees can prepare for these changes by staying informed, seeking professional advice, and developing flexible trust plans that can be adapted to changing circumstances.

What Role Will Technology Play in Future Trust Management?

Technology will play an increasingly important role in future trust management, with advancements in accounting software, tax preparation tools, and online resources. These technologies can help trustees streamline their operations, improve accuracy, and stay compliant with tax laws.

15. Income-partners.net: Your Partner in Financial Success

How Does Income-partners.net Support Trustees and Beneficiaries?

Income-partners.net provides a comprehensive platform for trustees and beneficiaries, offering resources, tools, and connections to help them manage their trusts effectively. Our network of professionals includes CPAs, attorneys, and financial advisors who can provide expert guidance and support.

What Resources and Tools Does Income-partners.net Offer?

Income-partners.net offers a variety of resources and tools, including articles, guides, calculators, and a directory of qualified professionals. These resources can help trustees and beneficiaries make informed decisions and achieve their financial goals.

How Can Income-partners.net Help You Find Strategic Partnerships to Increase Your Income?

Income-partners.net specializes in connecting individuals and businesses with strategic partnerships that drive growth and increase income. Whether you are looking for investment opportunities, joint ventures, or other collaborative ventures, our platform can help you find the right partners to achieve your financial objectives.

FAQ: Simple Trusts and Income Distribution

1. What is a simple trust?

A simple trust requires all income to be distributed currently, makes no charitable contributions, and does not distribute principal.

2. What happens if a simple trust doesn’t distribute all its income?

The undistributed income is taxed at the trust level, potentially leading to unexpected tax liabilities.

3. How did the TCJA affect simple trusts?

The TCJA eliminated certain itemized deductions, increasing the likelihood of taxable income at the trust level.

4. What is the difference between TAI and DNI?

TAI is trust accounting income based on the trust agreement and state law, while DNI is distributable net income used for tax purposes.

5. Are investment advisory fees deductible for simple trusts?

Generally, no, but exceptions exist if the fees are specific to trust management needs.

6. How does state law affect TAI?

State law dictates how income and expenses are allocated, impacting the calculation of TAI.

7. What strategies can minimize tax liability for simple trusts?

Maximize deductible expenses, make strategic distributions, and invest tax-efficiently.

8. Why should trustees seek professional advice?

Trust taxation is complex; professionals can help navigate and minimize tax consequences.

9. How can trustees stay compliant with tax laws?

Keep accurate records, file returns on time, and stay informed about tax law changes.

10. Where can trustees find resources for trust management?

Income-partners.net offers resources, tools, and a network of professionals for trust management.

Navigating the complexities of simple trusts requires a comprehensive understanding of tax laws, state regulations, and strategic financial planning. What happens if a simple trust does not distribute income? The answer, as we’ve explored, is that the trust will be responsible for paying taxes on the undistributed amount. By staying informed, seeking professional advice, and leveraging the resources available at income-partners.net, trustees and beneficiaries can effectively manage their trusts, minimize tax liabilities, and maximize their financial success. Explore your partnership potential and elevate your income with us today Address: 1 University Station, Austin, TX 78712, United States. Phone: +1 (512) 471-3434. Website: income-partners.net.