Corporate income taxes are taxes levied on company profits, and understanding them is crucial for businesses aiming for strategic partnerships and increased revenue, something income-partners.net excels at facilitating. This understanding can lead to identifying opportunities for business expansion and financial growth. This article explores the intricacies of corporate income taxes (CIT), their impact, and how businesses can navigate them effectively.

1. What Exactly Are Corporate Income Taxes?

Corporate income taxes (CIT) are taxes imposed on the profits of C corporations by federal, state, and sometimes even local governments. These taxes represent a significant cost of doing business and can greatly influence a company’s financial planning and investment decisions.

To elaborate, corporate income tax is a direct tax, meaning it’s levied directly on the income or profits of corporations. This is different from indirect taxes, like sales tax, which are levied on transactions. The amount of corporate income tax a company pays depends on its taxable income, which is calculated by subtracting allowable deductions from its gross income. These deductions can include expenses like salaries, rent, and depreciation of assets. The remaining amount is then subject to the applicable corporate tax rate.

It’s also important to distinguish between different types of business structures. While C corporations are subject to corporate income tax, other business structures like sole proprietorships, partnerships, and S corporations are considered “pass-through” entities. This means their profits are not taxed at the corporate level but are instead passed through to the owners or shareholders, who then report the income on their individual income tax returns. This difference in tax treatment can have a significant impact on the overall tax burden of a business and is an important factor to consider when choosing a business structure.

2. What Are the Current Corporate Tax Rates in the U.S.?

The current federal corporate income tax rate in the United States is a flat 21 percent, established by the Tax Cuts and Jobs Act (TCJA) of 2017. However, state corporate income tax rates vary, leading to different combined rates across the country.

Prior to the TCJA, the federal corporate tax rate was 35 percent, among the highest in the world. The reduction to 21 percent was intended to make the U.S. more competitive globally and encourage investment in the country. While the federal rate is now fixed at 21 percent, many states also levy their own corporate income taxes. These state rates vary widely, ranging from 0 percent in states like South Dakota and Wyoming to over 9 percent in states like Iowa and New Jersey. This means the total corporate income tax rate a company faces can vary significantly depending on where it’s located.

It’s also worth noting that some states have a graduated corporate income tax system, where the tax rate increases as the company’s income rises. Additionally, some cities and counties may also impose their own local corporate income taxes. Therefore, it’s crucial for businesses to understand the specific tax laws and rates in the jurisdictions where they operate.

3. Which States Have the Lowest and Highest Corporate Income Tax Rates?

Several states, including Nevada, Ohio, South Dakota, Texas, Washington, and Wyoming, have no corporate income tax. On the other end, states like New Jersey and Iowa have some of the highest rates.

These differences in state corporate income tax rates can significantly impact a company’s decision on where to locate its business. States with no or low corporate income taxes often attract businesses seeking to minimize their tax burden, leading to economic growth and job creation. This is particularly true for businesses with mobile operations or those that can easily relocate.

However, corporate income tax is not the only factor businesses consider when choosing a location. Other factors like the cost of living, availability of skilled labor, infrastructure, and regulatory environment also play a crucial role. Therefore, states often compete to attract businesses by offering a combination of tax incentives and other benefits.

For instance, Texas, with its no corporate income tax policy, has experienced significant business growth in recent years, attracting companies from California and other high-tax states. This has contributed to the state’s economic prosperity and job creation. On the other hand, states with high corporate income taxes may struggle to retain businesses and attract new investment.

4. How Is Corporate Taxable Income Calculated?

Corporate taxable income is generally calculated as a company’s revenues minus its costs of doing business, but with specific rules about deductions for capital investments and other items.

More specifically, the calculation of corporate taxable income starts with a company’s gross income, which includes all revenues from sales, services, and investments. From this, companies can deduct ordinary and necessary business expenses, such as salaries, rent, utilities, and marketing costs. However, there are specific rules and limitations on certain deductions.

One important area is the treatment of capital investments, such as equipment, machinery, and buildings. Unlike ordinary business expenses, the full cost of capital investments cannot be deducted in the year they are incurred. Instead, companies must depreciate these assets over their useful lives, deducting a portion of the cost each year. This depreciation can be calculated using various methods, such as straight-line depreciation or accelerated depreciation.

Another important factor is the treatment of net operating losses (NOLs). If a company experiences a loss in a given year, it may be able to carry that loss forward to offset future taxable income or carry it back to offset past taxable income. However, there are often limitations on the amount of NOLs that can be carried forward or back, as well as the number of years they can be carried. Inventory valuation methods, such as FIFO (first-in, first-out) and LIFO (last-in, first-out), can also affect a company’s taxable income.

5. What Are Pass-Through Businesses, and How Are They Taxed Differently?

Pass-through businesses, like partnerships, S corporations, and LLCs, don’t pay corporate income tax. Instead, their profits are passed through to their owners or shareholders, who pay individual income tax on their share of the profits.

The tax treatment of pass-through businesses is one of the most significant differences between them and C corporations. In a C corporation, the company itself pays corporate income tax on its profits. Then, when those profits are distributed to shareholders as dividends, the shareholders pay individual income tax on those dividends. This is often referred to as “double taxation,” as the same profits are taxed twice.

Pass-through businesses avoid this double taxation. Instead, the business’s profits are treated as if they were earned directly by the owners or shareholders. The profits are then reported on the owners’ individual income tax returns and taxed at their individual income tax rates. This can result in a lower overall tax burden, especially for businesses with relatively low profits.

However, there are also potential drawbacks to the pass-through structure. For example, owners of pass-through businesses may be subject to self-employment taxes on their share of the profits, which are not applicable to shareholders of C corporations. Additionally, the tax laws governing pass-through businesses can be complex, and owners may need to carefully plan their tax strategies to minimize their tax liability.

6. Who Ultimately Pays the Corporate Income Tax?

While corporations directly pay the corporate income tax, the burden of the tax is ultimately borne by a combination of the company’s shareholders, employees, and customers.

The distribution of the corporate income tax burden is a complex economic issue that has been studied extensively. While corporations are legally responsible for paying the tax, they can often pass some of the burden on to other parties.

For example, companies may respond to higher corporate income taxes by reducing wages or benefits for their employees. This effectively shifts some of the tax burden onto the employees. Similarly, companies may increase prices for their products or services, passing some of the tax burden on to their customers.

However, the extent to which companies can shift the tax burden depends on various factors, such as the elasticity of demand for their products, the competitiveness of the market, and the bargaining power of their employees. In general, companies in competitive industries with price-sensitive customers may have a harder time passing on the tax burden.

Shareholders also bear a portion of the corporate income tax burden, as the tax reduces the company’s profits and thus the value of their shares. This is particularly true for shareholders who hold their shares in taxable accounts, as they will owe capital gains taxes when they sell their shares.

7. How Does Corporate Income Tax Affect Economic Growth?

High corporate income tax rates can discourage investment and economic growth by reducing companies’ after-tax profits and increasing the cost of capital.

According to research from the University of Texas at Austin’s McCombs School of Business, in July 2025, lower corporate tax rates correlate with increased investment, job creation, and overall economic output. This is because lower taxes leave companies with more money to invest in new equipment, research and development, and hiring new employees.

On the other hand, high corporate income tax rates can discourage these activities, leading to slower economic growth. This is particularly true for small businesses and startups, which may have limited access to capital and are more sensitive to changes in tax rates.

The impact of corporate income tax on economic growth is a topic of ongoing debate among economists. Some argue that corporate income tax is a relatively inefficient tax that distorts investment decisions and hinders economic growth. Others argue that it is a necessary source of revenue for government services and that its impact on economic growth is relatively small.

However, there is a general consensus that corporate income tax can have a negative impact on economic growth if the rates are too high or the tax system is too complex. Therefore, policymakers often consider the potential impact on economic growth when making decisions about corporate income tax policy.

8. What Are Some Common Corporate Tax Deductions?

Common corporate tax deductions include expenses like salaries, rent, interest, depreciation, and research and development costs.

These deductions help reduce a company’s taxable income, lowering its overall tax liability. Salaries are typically deductible as long as they are reasonable and necessary for the business. Rent paid for office space or other business property is also deductible. Interest expenses, such as interest on loans used to finance business operations, are generally deductible as well.

Depreciation is a deduction that allows companies to recover the cost of capital assets, such as equipment and buildings, over their useful lives. This deduction is intended to reflect the wear and tear of these assets over time. Research and development (R&D) costs are also deductible, as they are considered investments in future growth.

In addition to these common deductions, there are many other deductions that may be available to corporations, depending on their specific circumstances. These can include deductions for charitable contributions, business travel expenses, and insurance premiums. It’s essential for companies to keep accurate records of their expenses and consult with a tax professional to ensure they are taking all the deductions they are entitled to.

9. What Is the Impact of Tax Cuts and Jobs Act (TCJA) on Corporate Taxes?

The Tax Cuts and Jobs Act (TCJA) of 2017 significantly reduced the federal corporate income tax rate from 35 percent to 21 percent, impacting corporate tax liabilities and business investment decisions.

The TCJA was one of the most significant tax reforms in decades, and it had a profound impact on corporate taxes. In addition to reducing the corporate tax rate, the TCJA also made several other changes to the corporate tax system.

For example, the TCJA eliminated the corporate alternative minimum tax (AMT), which was a parallel tax system that required corporations to calculate their tax liability under two different sets of rules and pay the higher amount. The TCJA also made changes to the rules governing depreciation, allowing companies to immediately deduct the full cost of certain assets in the year they are placed in service.

The TCJA’s impact on corporate tax liabilities has been significant. According to the Tax Policy Center, the TCJA reduced corporate tax revenues by about $1.35 trillion over the first 10 years after its enactment. This has led to lower tax bills for many corporations and increased after-tax profits.

The TCJA’s impact on business investment decisions is more complex. Some argue that the lower corporate tax rate has encouraged investment and job creation, while others argue that it has primarily benefited shareholders and has had little impact on the overall economy.

10. How Can Businesses Optimize Their Corporate Tax Strategy?

Businesses can optimize their corporate tax strategy by taking advantage of available deductions, credits, and incentives, as well as by carefully planning their business structure and operations.

One of the most important steps in optimizing a corporate tax strategy is to take advantage of all available deductions. This includes deductions for ordinary and necessary business expenses, depreciation, and research and development costs. Companies should also be aware of any special deductions or credits that may be available to them, such as credits for hiring certain types of employees or investing in renewable energy.

Careful planning of a business structure can also help optimize a corporate tax strategy. As mentioned earlier, pass-through businesses are taxed differently from C corporations, and the choice of business structure can have a significant impact on a company’s overall tax burden. Companies should carefully consider the pros and cons of each structure before making a decision.

Finally, companies can optimize their corporate tax strategy by carefully planning their business operations. This includes making decisions about where to locate their business, how to finance their operations, and how to manage their inventory. By carefully considering the tax implications of these decisions, companies can minimize their tax liability and maximize their after-tax profits.

11. What Role Do Tax Credits Play in Corporate Tax Planning?

Tax credits directly reduce the amount of tax a company owes and can be a valuable tool for incentivizing specific behaviors or investments.

Tax credits are different from tax deductions in that they directly reduce the amount of tax a company owes, rather than reducing its taxable income. For example, if a company has a tax liability of $100,000 and claims a tax credit of $10,000, its tax liability will be reduced to $90,000.

Tax credits can be used to incentivize a variety of behaviors or investments, such as hiring certain types of employees, investing in renewable energy, or conducting research and development. They can be a valuable tool for companies looking to reduce their tax liability while also pursuing socially responsible or economically beneficial activities.

However, tax credits can also be complex and may have specific requirements or limitations. For example, some tax credits may only be available to companies that meet certain size or income thresholds. Others may have limitations on the amount of credit that can be claimed in a given year.

It’s essential for companies to carefully research and understand the requirements of any tax credits they are considering claiming. They should also keep accurate records of their expenses and consult with a tax professional to ensure they are meeting all the necessary requirements.

12. How Do Net Operating Losses (NOLs) Affect Corporate Taxes?

Net operating losses (NOLs) can be used to reduce taxable income in other years, either by carrying them forward to future years or carrying them back to prior years, subject to certain limitations.

When a company experiences a loss in a given year, it may be able to use that loss to reduce its taxable income in other years. This is done through a mechanism called net operating loss (NOL) carryforwards and carrybacks.

NOL carryforwards allow companies to carry the loss forward to future years and use it to offset taxable income in those years. For example, if a company has an NOL of $100,000 in 2023, it may be able to carry that loss forward to 2024 and use it to reduce its taxable income in that year.

NOL carrybacks allow companies to carry the loss back to prior years and use it to offset taxable income in those years. For example, if a company has an NOL of $100,000 in 2023, it may be able to carry that loss back to 2022 and use it to reduce its taxable income in that year.

However, there are often limitations on the amount of NOLs that can be carried forward or back, as well as the number of years they can be carried. For example, the Tax Cuts and Jobs Act (TCJA) limited the NOL deduction to 80% of taxable income and eliminated NOL carrybacks for most businesses.

NOLs can be a valuable tool for companies that experience losses, as they can help reduce their overall tax liability. However, it’s important for companies to understand the limitations on NOL carryforwards and carrybacks and to carefully plan their tax strategies to maximize the benefits of NOLs.

13. What Are the Implications of Transfer Pricing for Corporate Income Taxes?

Transfer pricing, the pricing of transactions between related entities, can significantly impact corporate income taxes, as it affects the allocation of profits between different tax jurisdictions.

Transfer pricing refers to the pricing of goods, services, and intangible property between related entities, such as a parent company and its subsidiaries. These transactions can have a significant impact on corporate income taxes, as they affect the allocation of profits between different tax jurisdictions.

For example, if a parent company in a low-tax jurisdiction sells goods to its subsidiary in a high-tax jurisdiction at a low price, the subsidiary will have lower profits and pay less tax in the high-tax jurisdiction. Conversely, the parent company will have higher profits and pay more tax in the low-tax jurisdiction.

Tax authorities around the world closely scrutinize transfer pricing practices to ensure that companies are not using them to artificially shift profits to low-tax jurisdictions. They require companies to use the “arm’s length principle” when pricing transactions between related entities, which means that the prices should be comparable to those that would be charged between unrelated parties in similar transactions.

Companies must maintain detailed documentation to support their transfer pricing practices and demonstrate that they are in compliance with the arm’s length principle. Failure to comply with transfer pricing rules can result in significant penalties and adjustments to a company’s tax liability.

14. How Do International Tax Treaties Affect Corporate Income Taxes?

International tax treaties can reduce or eliminate double taxation and provide rules for allocating taxing rights between countries, affecting multinational corporations.

International tax treaties are agreements between two or more countries that are designed to reduce or eliminate double taxation and provide rules for allocating taxing rights between the countries. These treaties can have a significant impact on corporate income taxes, particularly for multinational corporations.

One of the primary purposes of tax treaties is to prevent double taxation. This occurs when the same income is taxed in two different countries. Tax treaties typically provide rules for determining which country has the primary right to tax certain types of income.

For example, a tax treaty may provide that business profits are only taxable in the country where the business has a “permanent establishment,” such as a factory or office. If a company has a permanent establishment in both countries, the treaty may provide rules for allocating the profits between the two countries.

Tax treaties can also provide for reduced rates of withholding tax on dividends, interest, and royalties paid to residents of the other country. These reduced rates can make it more attractive for companies to invest in or do business with companies in the other country.

Tax treaties are complex legal documents, and it’s essential for companies to understand the provisions of any tax treaties that may affect their business. They should also consult with a tax professional to ensure they are in compliance with the treaty rules.

15. What Are the Key Differences Between Federal and State Corporate Income Taxes?

Federal corporate income taxes are levied at a flat rate nationwide, while state corporate income taxes vary significantly by state, with some states having no corporate income tax.

One of the key differences between federal and state corporate income taxes is the rate. The federal corporate income tax rate is currently a flat 21 percent for all corporations, regardless of their income or location.

State corporate income tax rates, on the other hand, vary significantly by state. Some states, such as Nevada, Ohio, South Dakota, Texas, Washington, and Wyoming, have no corporate income tax at all. Other states, such as New Jersey and Iowa, have some of the highest corporate income tax rates in the country.

Another difference is the tax base. The federal corporate income tax base is generally the same for all corporations, although there may be some differences depending on the industry or type of business. State corporate income tax bases, on the other hand, can vary significantly by state. Some states may use the federal tax base as a starting point, while others may have their own unique definitions of taxable income.

Finally, the rules for filing and paying corporate income taxes can also vary between the federal government and the states. The federal government has its own set of forms and procedures for filing and paying corporate income taxes. States also have their own set of forms and procedures, which can be different from the federal rules.

16. How Does Corporate Tax Compliance Differ for Small vs. Large Businesses?

Small businesses often have simpler tax compliance requirements than large businesses, but they still need to understand and follow all applicable tax laws.

Corporate tax compliance can differ significantly for small businesses versus large businesses. Small businesses often have simpler tax compliance requirements than large businesses, but they still need to understand and follow all applicable tax laws.

One of the main differences is the complexity of the tax returns. Small businesses typically file simpler tax returns than large businesses, as they have fewer transactions and less complex financial statements. However, they still need to accurately report their income, expenses, and deductions.

Another difference is the level of resources available for tax compliance. Large businesses typically have dedicated tax departments or hire outside tax professionals to handle their tax compliance. Small businesses, on the other hand, may not have the resources to hire dedicated tax staff and may rely on the owners or managers to handle tax compliance.

Finally, the risk of audit can also differ for small businesses versus large businesses. While all businesses are subject to audit by the IRS or state tax authorities, large businesses may be more likely to be audited due to the complexity of their tax returns and the potential for significant tax adjustments.

Regardless of their size, all businesses need to take tax compliance seriously and ensure they are following all applicable tax laws. They should also keep accurate records of their income, expenses, and deductions and consult with a tax professional if they have any questions or concerns.

17. What Are Some Common Mistakes to Avoid in Corporate Tax Planning?

Common mistakes to avoid in corporate tax planning include failing to take advantage of available deductions, not keeping accurate records, and not seeking professional advice.

Corporate tax planning can be complex, and it’s easy for businesses to make mistakes that can result in higher tax liabilities or penalties. Here are some common mistakes to avoid in corporate tax planning:

- Failing to take advantage of available deductions: Many businesses fail to take advantage of all the deductions they are entitled to, which can result in higher tax liabilities. It’s essential to carefully review all available deductions and ensure you are claiming all those you are eligible for.

- Not keeping accurate records: Accurate recordkeeping is essential for tax compliance. Businesses should keep detailed records of their income, expenses, and deductions. Failure to keep accurate records can make it difficult to prepare tax returns accurately and can increase the risk of audit.

- Not seeking professional advice: Tax laws can be complex, and it’s often helpful to seek professional advice from a tax advisor. A tax advisor can help you understand the tax laws that apply to your business and develop a tax plan that minimizes your tax liability.

- Misclassifying workers: Misclassifying workers as independent contractors instead of employees can result in significant tax penalties. It’s important to understand the rules for classifying workers and to properly classify your workers.

- Ignoring state and local taxes: Many businesses focus on federal taxes but ignore state and local taxes. State and local taxes can be significant, and it’s important to understand the tax laws in the states and localities where you do business.

By avoiding these common mistakes, businesses can minimize their tax liability and ensure they are in compliance with all applicable tax laws.

18. What Resources Are Available to Help Businesses Understand Corporate Income Taxes?

Resources available to help businesses understand corporate income taxes include the IRS website, tax publications, and professional tax advisors.

Understanding corporate income taxes can be challenging, but there are many resources available to help businesses. Here are some of the most helpful resources:

- IRS website: The IRS website (www.irs.gov) is a comprehensive source of information on federal taxes. It includes tax forms, instructions, publications, and FAQs.

- Tax publications: The IRS publishes a variety of tax publications that provide detailed guidance on specific tax topics. These publications are available for free on the IRS website.

- Professional tax advisors: Tax advisors can provide personalized advice and guidance on corporate income taxes. They can help you understand the tax laws that apply to your business and develop a tax plan that minimizes your tax liability.

- Small Business Administration (SBA): The SBA provides resources and support to small businesses, including information on taxes.

- State tax agencies: State tax agencies provide information on state corporate income taxes.

- Tax software: Tax software can help you prepare and file your corporate income tax returns.

By using these resources, businesses can gain a better understanding of corporate income taxes and ensure they are in compliance with all applicable tax laws.

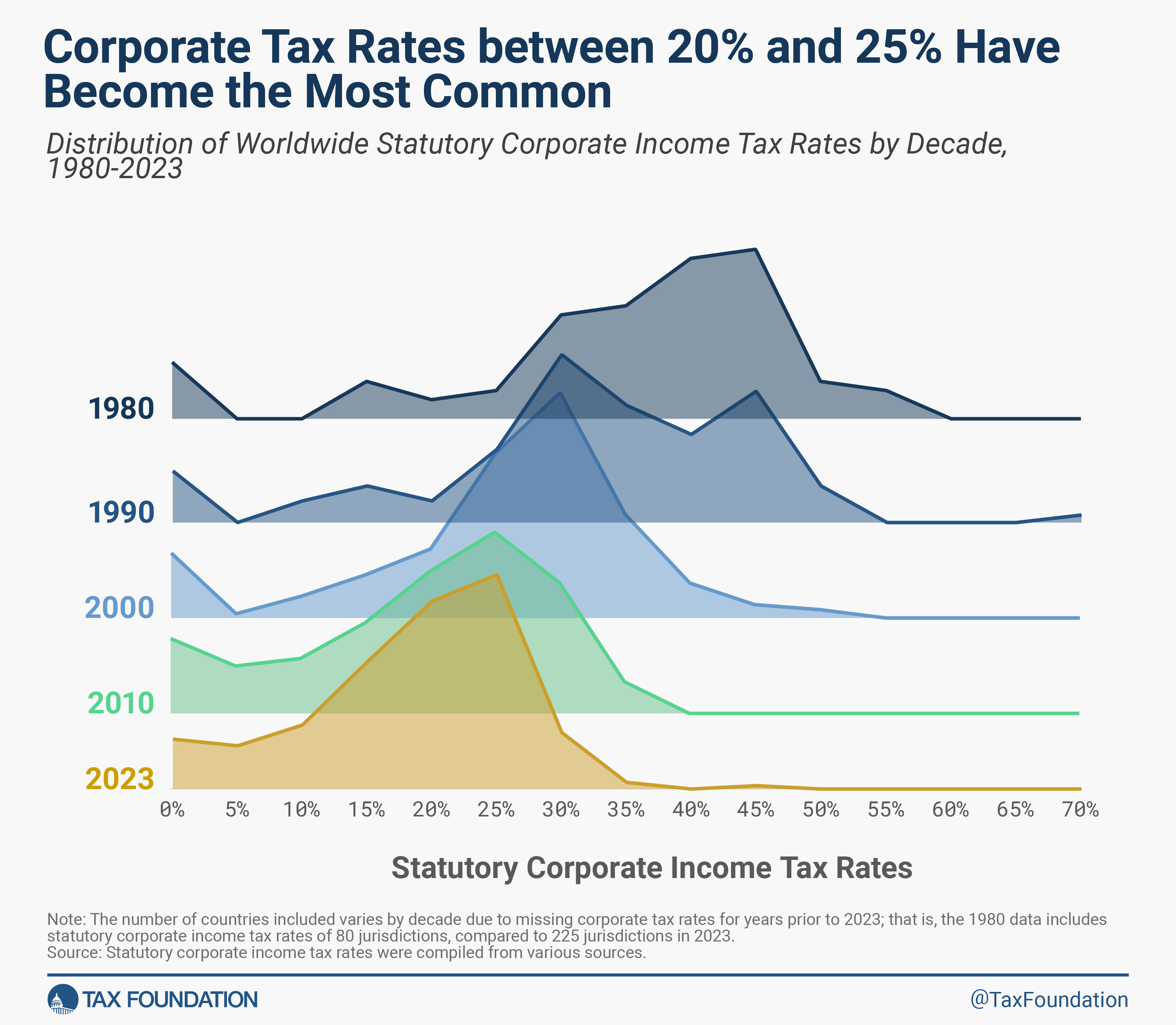

Corporate income tax rate trends and comparisons with OECD countries

Corporate income tax rate trends and comparisons with OECD countries

19. How Can Income-Partners.Net Help Businesses Navigate Corporate Income Taxes and Improve Profitability?

Income-partners.net offers resources and connections to help businesses understand tax implications, find strategic partners, and increase revenue, ultimately improving profitability. By leveraging strategic partnerships, businesses can optimize operations and reduce their effective tax rate.

Navigating corporate income taxes is complex, but with the right strategies and partners, businesses can optimize their tax position and improve profitability. income-partners.net provides a platform for businesses to connect, share knowledge, and find partners who can help them navigate these challenges.

Here are some ways that income-partners.net can help businesses navigate corporate income taxes and improve profitability:

- Connect with tax professionals: income-partners.net can connect you with experienced tax professionals who can provide personalized advice and guidance on corporate income taxes.

- Find strategic partners: income-partners.net can help you find strategic partners who can help you optimize your operations and reduce your effective tax rate. For example, you may be able to partner with a business in a low-tax jurisdiction to reduce your overall tax liability.

- Access resources and information: income-partners.net provides access to a variety of resources and information on corporate income taxes, including articles, guides, and webinars.

- Share knowledge and best practices: income-partners.net provides a platform for businesses to share knowledge and best practices on corporate income taxes. You can learn from the experiences of other businesses and share your own insights.

- Identify opportunities for growth: By connecting with other businesses and accessing valuable resources, income-partners.net can help you identify opportunities for growth that can improve your profitability and reduce your tax burden.

To further illustrate, consider a business looking to expand into a new market. By partnering with a local business in that market through income-partners.net, they can gain valuable insights into the local tax laws and regulations. This knowledge can help them structure their expansion in a way that minimizes their tax liability and maximizes their profitability.

20. What Are Some Emerging Trends in Corporate Income Taxation?

Emerging trends in corporate income taxation include increased international cooperation on tax issues, the rise of digital taxes, and a focus on tax transparency.

The world of corporate income taxation is constantly evolving, and there are several emerging trends that businesses need to be aware of. Here are some of the most significant emerging trends:

- Increased international cooperation on tax issues: Governments around the world are increasingly working together to address tax avoidance and evasion by multinational corporations. This includes efforts to combat base erosion and profit shifting (BEPS), which is the practice of shifting profits to low-tax jurisdictions to reduce overall tax liability.

- The rise of digital taxes: With the growth of the digital economy, many countries are considering or implementing taxes on digital services. These taxes are designed to capture revenue from companies that provide digital services in a country but may not have a physical presence there.

- A focus on tax transparency: There is growing pressure on companies to be more transparent about their tax affairs. This includes requirements to disclose information about their tax strategies, their tax payments, and their relationships with tax authorities.

- Changes to corporate tax rates: Corporate tax rates have been declining in many countries in recent years, but there is some debate about whether this trend will continue. Some countries may choose to increase corporate tax rates to fund government spending or to address concerns about income inequality.

- The impact of technology on tax compliance: Technology is playing an increasing role in tax compliance. Tax authorities are using data analytics and artificial intelligence to identify tax evasion and fraud. Businesses are also using technology to automate tax compliance processes and improve accuracy.

By staying informed about these emerging trends, businesses can be better prepared to navigate the changing landscape of corporate income taxation.

Frequently Asked Questions (FAQs)

- What is the difference between corporate income tax and individual income tax? Corporate income tax is levied on company profits, while individual income tax is levied on individuals’ income.

- How often do corporations pay income taxes? Corporations typically pay income taxes quarterly through estimated tax payments.

- Are there any tax advantages to being a small business? Small businesses may qualify for certain deductions and credits not available to larger corporations.

- Can losses from one year offset profits in another year? Yes, net operating losses (NOLs) can be carried forward or back to offset profits in other years, subject to limitations.

- What is the role of a tax advisor in corporate tax planning? A tax advisor can provide expert advice on tax laws, deductions, and strategies to minimize tax liability.

- How does transfer pricing affect corporate income taxes for multinational corporations? Transfer pricing affects the allocation of profits between different tax jurisdictions, impacting tax liabilities.

- What are the main goals of international tax treaties? The main goals are to avoid double taxation and set rules for taxing rights between countries.

- How does the Tax Cuts and Jobs Act of 2017 impact corporate taxes? It significantly reduced the federal corporate income tax rate from 35% to 21%.

- What are the implications of digital taxes for companies operating online? Digital taxes aim to capture revenue from companies providing digital services, even without a physical presence.

- Why is tax transparency becoming more important for corporations? Tax transparency promotes accountability and reduces tax avoidance by disclosing tax strategies and payments.

Understanding corporate income taxes is essential for businesses seeking strategic partnerships and increased revenue. income-partners.net can be a valuable resource for connecting with experts, finding opportunities, and staying informed about the latest trends in corporate taxation.

Ready to explore how strategic partnerships can optimize your tax position and boost your bottom line? Visit income-partners.net today to discover potential partners and unlock new opportunities for financial growth. Find your ideal partners and start building profitable relationships right now! Address: 1 University Station, Austin, TX 78712, United States. Phone: +1 (512) 471-3434. Website: income-partners.net.