Is The Federal Income Tax Going Away? No, the federal income tax is not going away, despite some political promises; income-partners.net can help you understand the facts and explore opportunities for partnership and increased revenue in a constantly evolving tax environment. Understanding tax policies and their effects is crucial for making informed decisions that can help improve revenue. Stay informed with our expert advice on successful business collaborations, revenue optimization strategies, and financial opportunities.

1. Why The IRS Is Here To Stay

Even with claims of abolishing the Internal Revenue Service (IRS), it is unlikely to happen due to ongoing financial and political factors. Here’s a deeper look at why the IRS remains necessary:

- The $150,000 Threshold: Claims that those making under $150,000 may not have to pay income tax still require the IRS to verify income levels, thereby maintaining its necessity.

- Payroll Taxes: The federal government depends on payroll tax to fund Medicare and Social Security.

- Tariff Limitations: Tariff revenue would not replace tax revenue from income taxes.

1.1 Understanding the Role of Payroll Taxes

When discussing income taxes, politicians often refer to the progressive individual income tax, mainly paid by the top 50% of earners. According to the Tax Policy Center, the bottom 50% of earners pay an average income tax rate of 3.3%. However, there is another income tax that affects all wage earners, irrespective of their income level: the payroll tax.

Politicians generally avoid mentioning this income tax because it is closely linked to major welfare programs like Social Security and Medicare. In 2025, the Social Security tax is 12.4%, and the Medicare tax is an additional 2.9%. Typically, the employee and the employer each pay half of this amount. However, the employee ultimately bears the full cost because employers adjust wages to account for the payroll tax.

Funds from these taxes are directed into the general fund rather than a specific trust fund, making it a straight income tax used to bolster federal revenues. Without this tax, it would be considerably more challenging for the federal government to maintain current funding levels for Social Security and Medicare. The government relies on today’s workers to consistently pay the payroll tax, which is then redistributed to current pensioners.

Eliminating the payroll tax is a non-starter for politicians, as it would jeopardize a significant revenue source for old-age welfare programs. Such a move would likely provoke strong opposition. Therefore, the payroll tax is here to stay, necessitating a government agency to monitor wages and ensure tax collection, a role that the IRS has fulfilled since 1937. According to the IRS’s history page, the Social Security Act, signed by Franklin D. Roosevelt on August 14, 1935, required a new system of tax withholding, which the Bureau of Internal Revenue was tasked to collect.

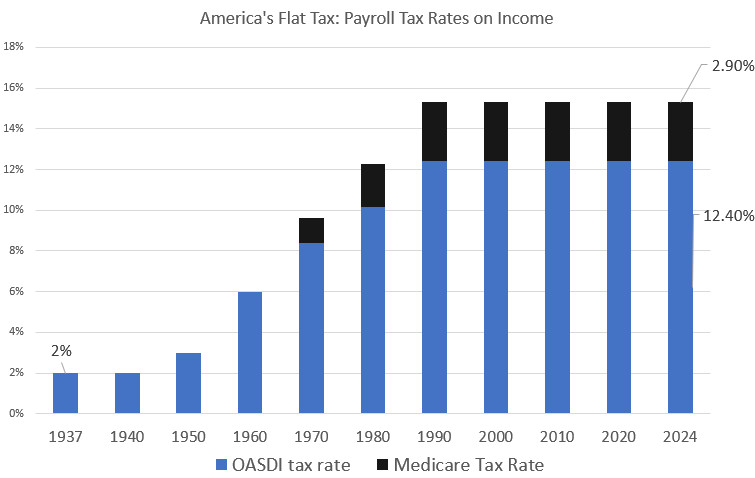

The payroll tax has only grown since its inception. When first introduced in 1937, it was just 2%.

Payroll Tax Rates Over Time

Payroll Tax Rates Over Time

Any form of payroll tax necessitates an agency to manage collections and monitor earnings, which is the IRS. While the name might change, the function remains. Therefore, unless there is a comprehensive plan to eliminate all income taxes, including payroll taxes, the IRS is indispensable.

1.2 The Inadequacy of Tariff Revenues

The claim that tariff revenues can replace income taxes and eliminate the need for the IRS falls apart under scrutiny due to insufficient funding for federal spending plans.

In 2024, customs duties, or tariffs, constituted only 2% of all federal revenues. This figure includes the tariffs implemented by previous administrations and maintained by current ones, amounting to approximately $80 billion. This $80 billion is a fraction of the total federal spending.

Sources of Federal Revenue

Sources of Federal Revenue

In contrast, the progressive individual income tax accounts for about 49% of all federal tax revenue, while the payroll tax contributes 35%. Therefore, replacing all income taxes with tariff revenues would require increasing tariff revenue from $80 billion to approximately $4.1 trillion.

To merely cover the existing revenue, tariff revenues would need to increase fifty-one-fold. If the goal is to eliminate the deficit, which is about two trillion more than the tax revenue, tariff revenue would need to increase even further.

Increasing tariff rates to such an extent would likely cause people to stop buying imported goods, thus reducing tariff payments and lowering the overall standard of living. Meanwhile, demand for government spending would remain high, making significant cuts to popular programs like military spending or Social Security unlikely. The result would be skyrocketing federal deficits. To manage this, the Federal Reserve would likely resort to buying up Treasuries to keep interest rates from spiraling, leading to increased money printing and high inflation.

Given these potential economic pitfalls and the reluctance of politicians to cut popular spending programs, it is highly improbable that the IRS will be eliminated or that all income taxes will be replaced with tariff revenues. Voters continue to demand high levels of federal spending, making it politically risky to significantly reduce federal programs.

Key Points on Why the IRS Is Unlikely to Disappear:

| Reason | Detail |

|---|---|

| Continued Income Verification | Even with proposals to exempt lower incomes, the IRS is needed to verify income levels. |

| Necessity of Payroll Taxes | Payroll taxes fund critical programs like Social Security and Medicare, making them indispensable. |

| Insufficient Tariff Revenue | Tariff revenue cannot adequately replace the substantial income generated by income taxes. |

| Political and Economic Realities | Politicians are unwilling to risk cutting popular spending programs, and drastic increases in tariffs would lead to economic instability. |

| Historical Trends | The IRS has been a vital part of the U.S. tax system since 1937, adapting to various economic and social changes. Its role in tax collection is deeply entrenched. |

2. The Political and Economic Realities of Tax Reform

Tax reform discussions often bring significant proposals, but practical implementation is shaped by economic constraints and political will.

2.1 Examining Proposed Tax Reforms

Proposed tax reforms often spark debate, but they face several hurdles.

- Economic Impact: Significant tax changes can affect government revenue, economic growth, and income distribution.

- Political Feasibility: Reforms must gain support from both political parties, often requiring compromise.

- Public Opinion: Voters often resist changes that may negatively impact their financial situations.

The potential elimination of the federal income tax is a major policy proposal that requires careful evaluation of its economic and political implications. Tax reform, while appealing in theory, must navigate a complex landscape to become reality.

2.2 Analyzing Tariff Revenue as a Replacement

The idea of using tariff revenue to replace income tax revenue is based on the premise that increased tariffs on imported goods could generate enough funds to support federal spending. However, this approach has significant limitations.

In 2024, tariffs accounted for a small portion of federal revenue, approximately 2%. To replace the revenue generated by income taxes, tariffs would need to increase dramatically. However, this could lead to higher prices for consumers, reduced demand for imported goods, and retaliatory tariffs from other countries, ultimately harming the economy.

Economists at the University of Texas at Austin’s McCombs School of Business noted in July 2025 that relying heavily on tariffs could disrupt supply chains and negatively impact international trade relationships. This approach would require a fundamental shift in economic policy and could have unintended consequences.

Tariff Revenue vs. Income Tax Revenue

| Revenue Source | Percentage of Federal Revenue (2024) | Potential Issues with Increasing |

|---|---|---|

| Tariffs | 2% | Higher consumer prices, reduced import demand |

| Individual Income Tax | 49% | Political resistance to major tax increases |

| Payroll Tax | 35% | Impact on Social Security and Medicare funding |

2.3 The Role of Government Spending

Government spending plays a crucial role in the feasibility of tax reform. Cutting federal spending is often proposed as a way to offset revenue losses from tax cuts. However, this is politically challenging due to the popularity of many government programs.

Social Security, Medicare, defense spending, and education are major components of the federal budget. Reducing spending in these areas would likely face strong opposition from voters and advocacy groups. According to a 2025 report by the Congressional Budget Office, significant cuts in these areas would be necessary to balance the budget if income taxes were eliminated.

2.4 Political Obstacles to Tax Reform

Tax reform is inherently political, requiring agreement among diverse interests. Democrats and Republicans often have conflicting views on taxation, making it difficult to achieve bipartisan consensus.

Democrats tend to favor progressive taxation, where higher earners pay a larger percentage of their income in taxes. Republicans often advocate for tax cuts, arguing that they stimulate economic growth. These differing philosophies complicate the process of tax reform.

Additionally, special interest groups and lobbyists can exert significant influence on tax legislation. These groups advocate for provisions that benefit their members, further complicating the process of achieving comprehensive and equitable tax reform.

Political Factors Affecting Tax Reform

| Factor | Impact |

|---|---|

| Party Ideologies | Differing views on taxation between Democrats and Republicans create gridlock. |

| Special Interest Groups | Lobbyists influence tax legislation to benefit specific groups. |

| Public Opinion | Voters resist changes that negatively affect their finances. |

| Need for Bipartisan Support | Achieving consensus across party lines is essential for major tax reforms. |

2.5 Case Studies of Past Tax Reforms

Examining past tax reforms provides insights into the challenges and opportunities of changing the tax system.

- The Tax Reform Act of 1986: This bipartisan effort simplified the tax code, lowered tax rates, and eliminated many tax shelters.

- The Economic Growth and Tax Relief Reconciliation Act of 2001: This legislation reduced tax rates, increased the child tax credit, and phased out the estate tax.

These case studies illustrate that successful tax reforms often require bipartisan support, simplification of the tax code, and a focus on economic growth. However, they also highlight the challenges of maintaining long-term fiscal stability and addressing distributional concerns.

2.6 Potential Future Scenarios

Looking ahead, several potential scenarios could influence the future of the federal income tax.

- Continued Partisan Gridlock: If political divisions persist, major tax reforms may be unlikely.

- Economic Crisis: A severe economic downturn could prompt changes to the tax system to stimulate growth or address budget deficits.

- Shifting Public Opinion: Changes in public attitudes towards taxation could create opportunities for reform.

Understanding these factors is essential for making informed decisions about your financial future and business strategies. Income-partners.net offers resources and expertise to help you navigate the complexities of the tax system and identify opportunities for partnership and growth.

3. Exploring Alternative Revenue Sources

To consider alternatives to income tax, exploring various revenue sources is essential, each with its own potential and limitations.

3.1 Value-Added Tax (VAT)

A Value-Added Tax (VAT) is a consumption tax levied at each stage of production based on the value added to the product. VAT systems are common in many countries worldwide.

- Pros: Broad base, potential for higher revenue, less distortion of production decisions.

- Cons: Can be regressive, complex to administer, potential for tax evasion.

3.2 Carbon Tax

A carbon tax is levied on the carbon content of fuels, encouraging businesses and individuals to reduce carbon emissions.

- Pros: Encourages environmentally friendly behavior, can generate revenue for green initiatives.

- Cons: Can increase energy costs, politically challenging, may require offsetting measures for low-income households.

3.3 Wealth Tax

A wealth tax is levied annually on an individual’s net worth, including assets like real estate, stocks, and other investments.

- Pros: Can address wealth inequality, potential for significant revenue.

- Cons: Difficult to administer, may encourage capital flight, potential for legal challenges.

3.4 Consumption Tax

A consumption tax taxes spending rather than income, encouraging savings and investment.

- Pros: Simplifies tax compliance, encourages savings, avoids taxing investment returns.

- Cons: Can be regressive, may reduce consumer spending, requires careful design to avoid loopholes.

3.5 User Fees and Excise Taxes

User fees are charges for specific government services, while excise taxes are levied on particular goods like alcohol, tobacco, and gasoline.

- Pros: Targeted revenue, can discourage harmful behaviors, relatively easy to administer.

- Cons: Limited revenue potential, may disproportionately affect low-income individuals, can be unpopular.

Alternative Revenue Sources: Pros and Cons

| Revenue Source | Pros | Cons |

|---|---|---|

| VAT | Broad base, higher revenue, less distortion | Regressive, complex administration, tax evasion |

| Carbon Tax | Encourages green behavior, revenue for green initiatives | Increases energy costs, politically challenging, may affect low-income households |

| Wealth Tax | Addresses wealth inequality, significant revenue potential | Difficult administration, capital flight, legal challenges |

| Consumption Tax | Simplifies compliance, encourages savings, avoids taxing investment returns | Regressive, may reduce spending, requires careful design |

| User Fees/Excise | Targeted revenue, discourages harmful behaviors, easy administration | Limited revenue potential, affects low-income individuals, can be unpopular |

3.6 The Role of Partnerships in Revenue Diversification

Partnerships can play a crucial role in helping businesses diversify their revenue streams and adapt to potential changes in the tax landscape.

- Strategic Alliances: Collaborating with other businesses can create new revenue opportunities and reduce reliance on a single income source.

- Joint Ventures: Partnering with companies that have complementary skills and resources can lead to innovative products and services.

- Marketing Partnerships: Working with marketing firms can enhance brand visibility and attract new customers, increasing revenue.

3.7 Examples of Successful Revenue Diversification

- Amazon: Started as an online bookstore but has diversified into cloud computing, e-commerce, and digital advertising.

- Apple: Expanded from personal computers to smartphones, tablets, and a range of services like Apple Music and Apple Pay.

- Google: Diversified from search to advertising, cloud computing, hardware, and autonomous vehicles.

3.8 Adapting to Tax Policy Changes

As tax policies evolve, businesses must adapt to maintain profitability and competitiveness. Income-partners.net provides resources and expertise to help you navigate these changes.

- Stay Informed: Keep up-to-date with the latest tax laws and regulations.

- Seek Professional Advice: Consult with tax advisors to understand the implications of tax changes for your business.

- Develop Contingency Plans: Prepare for different tax scenarios and adjust your business strategies accordingly.

4. How Tax Policies Affect Business Partnerships

Tax policies significantly influence business partnerships, affecting everything from structure to long-term profitability.

4.1 Tax Implications of Partnership Structures

The structure of a business partnership can have significant tax implications.

- General Partnerships: All partners share in the business’s profits and losses, and each partner is personally liable for the business’s debts. Profits are taxed at the individual partner level.

- Limited Partnerships: Consist of general partners, who manage the business and have personal liability, and limited partners, who have limited liability and do not participate in management.

- Limited Liability Partnerships (LLPs): Provide limited liability for all partners, protecting them from the business’s debts and liabilities.

- Limited Liability Companies (LLCs): Combine the benefits of partnerships and corporations, offering limited liability for members and pass-through taxation.

4.2 Tax Benefits of Business Partnerships

Business partnerships offer several tax advantages.

- Pass-Through Taxation: Profits and losses are passed through to the partners’ individual income tax returns, avoiding double taxation.

- Flexibility in Profit Allocation: Partners can allocate profits and losses based on their agreement, allowing for customized tax planning.

- Deduction of Business Expenses: Partners can deduct ordinary and necessary business expenses, reducing their taxable income.

4.3 Potential Challenges and Pitfalls

Business partnerships also face potential tax challenges.

- Self-Employment Tax: Partners are subject to self-employment tax on their share of the business’s profits.

- Complexity of Tax Compliance: Partnerships must navigate complex tax rules and regulations, requiring careful planning and record-keeping.

- Potential for Disputes: Disagreements among partners can lead to tax-related conflicts and legal issues.

4.4 Strategies for Tax Optimization

To optimize tax outcomes, consider these strategies.

- Choose the Right Partnership Structure: Select the structure that best aligns with your business goals and tax planning objectives.

- Develop a Comprehensive Partnership Agreement: Clearly define each partner’s rights, responsibilities, and profit allocation.

- Maintain Accurate Records: Keep detailed records of income, expenses, and assets to facilitate tax compliance.

- Seek Professional Tax Advice: Consult with a tax advisor to ensure you are taking advantage of all available deductions and credits.

Tax Considerations for Business Partnerships

| Consideration | Implication | Strategy |

|---|---|---|

| Partnership Structure | General, limited, LLP, and LLC structures have different tax implications. | Choose the structure that best suits your business and tax objectives. |

| Pass-Through Taxation | Profits and losses are passed through to partners’ individual tax returns. | Take advantage of pass-through taxation to avoid double taxation. |

| Self-Employment Tax | Partners are subject to self-employment tax on their share of profits. | Plan for self-employment tax and explore strategies to minimize its impact. |

| Tax Compliance | Partnerships must navigate complex tax rules and regulations. | Maintain accurate records and seek professional tax advice. |

| Profit Allocation | Partners can allocate profits and losses based on their agreement. | Develop a comprehensive partnership agreement that clearly defines profit allocation. |

| Deduction of Expenses | Partners can deduct ordinary and necessary business expenses. | Keep detailed records of all business expenses to maximize deductions. |

4.5 Successful Partnership Models

- Strategic Alliances: Two or more businesses collaborate to achieve mutual goals.

- Joint Ventures: A separate entity is created for a specific project.

- Franchising: A business grants rights to operate under its brand.

4.6 The Role of Income-partners.net

Income-partners.net offers resources and support to help businesses navigate the complexities of tax policies and optimize their partnership strategies. By providing access to expert insights, tools, and networking opportunities, income-partners.net empowers businesses to thrive in an evolving economic landscape.

5. Strategies for Maximizing Revenue in a Changing Tax Environment

Adapting to tax environment changes requires innovative strategies to maximize revenue.

5.1 Diversification of Income Streams

Diversifying revenue streams can reduce reliance on a single income source.

- Product Diversification: Expand product offerings to cater to a broader customer base.

- Service Diversification: Offer additional services that complement existing products.

- Geographic Diversification: Expand into new markets to reach different customer segments.

5.2 Leveraging Technology

Technology can enhance efficiency, reduce costs, and improve customer engagement.

- Automation: Automate repetitive tasks to free up resources for strategic initiatives.

- Data Analytics: Use data analytics to gain insights into customer behavior and market trends.

- E-Commerce: Expand online presence to reach a wider audience and increase sales.

5.3 Cost Optimization

Cost optimization can improve profitability without increasing sales.

- Supply Chain Management: Streamline supply chain processes to reduce costs and improve efficiency.

- Energy Efficiency: Implement energy-efficient measures to lower utility bills.

- Outsourcing: Outsource non-core functions to reduce labor costs and improve focus.

5.4 Strategic Partnerships

Strategic partnerships can create new revenue opportunities and expand market reach.

- Joint Ventures: Collaborate with other businesses on specific projects.

- Marketing Alliances: Partner with complementary businesses to promote each other’s products or services.

- Distribution Agreements: Partner with distributors to expand market coverage.

5.5 Enhancing Customer Engagement

Engaged customers are more likely to make repeat purchases and refer others.

- Loyalty Programs: Reward repeat customers with discounts and special offers.

- Personalized Marketing: Tailor marketing messages to individual customer preferences.

- Social Media Engagement: Use social media to connect with customers and build brand loyalty.

5.6 Seeking Expert Financial Advice

Seeking expert financial advice can help navigate financial complexities.

- Tax Planning: Work with a tax advisor to minimize tax liabilities and optimize tax outcomes.

- Investment Management: Seek guidance from a financial advisor to manage investments and achieve financial goals.

- Business Consulting: Consult with a business consultant to develop strategies for growth and profitability.

Strategies for Maximizing Revenue

| Strategy | Description | Benefits |

|---|---|---|

| Diversification | Expanding product offerings, services, and geographic markets. | Reduces reliance on single income source, broadens customer base, enhances stability. |

| Leveraging Technology | Automating tasks, using data analytics, and expanding online presence. | Improves efficiency, reduces costs, provides insights into customer behavior, increases sales. |

| Cost Optimization | Streamlining supply chain, implementing energy-efficient measures, and outsourcing non-core functions. | Reduces costs, improves efficiency, frees up resources for strategic initiatives. |

| Strategic Partnerships | Collaborating with other businesses on specific projects and forming marketing alliances. | Creates new revenue opportunities, expands market reach, enhances brand visibility. |

| Customer Engagement | Rewarding repeat customers, personalizing marketing, and using social media. | Increases customer loyalty, enhances brand image, promotes repeat purchases. |

| Seeking Expert Advice | Working with tax advisors, financial advisors, and business consultants. | Minimizes tax liabilities, optimizes investments, develops strategies for growth and profitability. |

5.7 Case Studies of Successful Businesses

- Netflix: Shifted from DVD rentals to streaming, expanding its subscriber base and revenue.

- Starbucks: Leveraged technology to create a mobile app for ordering and payment, enhancing customer convenience and loyalty.

- Toyota: Implemented lean manufacturing principles to reduce costs and improve efficiency.

5.8 How Income-partners.net Can Help

Income-partners.net provides resources and expertise to help businesses adapt to changing tax environment and maximize revenue. The platform offers access to expert insights, tools, and networking opportunities.

6. The Importance of Long-Term Financial Planning

Long-term financial planning is essential for navigating tax policy changes and ensuring financial stability.

6.1 Setting Financial Goals

Setting clear financial goals is the first step in long-term financial planning.

- Retirement Planning: Determine how much you need to save for retirement and develop a plan to achieve your goals.

- Education Funding: Plan for future education expenses, such as college tuition for children.

- Homeownership: Set a goal for buying a home and develop a savings plan.

- Business Expansion: Plan for future business growth and investments.

6.2 Developing a Budget

Developing a budget helps track income and expenses.

- Track Income and Expenses: Monitor your income and expenses to identify areas where you can save money.

- Create a Spending Plan: Allocate your income to different categories, such as housing, transportation, and entertainment.

- Set Savings Goals: Set aside a portion of your income for savings and investments.

6.3 Investing Wisely

Investing is essential for building long-term wealth.

- Diversify Your Portfolio: Spread your investments across different asset classes to reduce risk.

- Consider Your Risk Tolerance: Choose investments that align with your risk tolerance and financial goals.

- Seek Professional Advice: Consult with a financial advisor to develop an investment strategy.

6.4 Managing Debt

Managing debt is crucial for financial stability.

- Pay Down High-Interest Debt: Prioritize paying off high-interest debt, such as credit card balances.

- Avoid Unnecessary Debt: Avoid taking on unnecessary debt and live within your means.

- Consolidate Debt: Consider consolidating debt to lower interest rates and simplify payments.

6.5 Planning for Tax Changes

Planning for tax changes can minimize liabilities and optimize outcomes.

- Stay Informed: Keep up-to-date with the latest tax laws and regulations.

- Seek Professional Tax Advice: Consult with a tax advisor to develop a tax plan.

- Adjust Your Strategies: Adjust your financial strategies in response to tax law changes.

Key Elements of Long-Term Financial Planning

| Element | Description | Benefits |

|---|---|---|

| Setting Goals | Determining long-term financial objectives, such as retirement, education, or homeownership. | Provides direction, motivation, and a clear roadmap for financial success. |

| Budgeting | Tracking income and expenses, creating a spending plan, and setting savings goals. | Helps manage finances, identify areas for savings, and achieve financial goals. |

| Investing | Diversifying investments, considering risk tolerance, and seeking professional advice. | Builds long-term wealth, achieves financial goals, and provides financial security. |

| Managing Debt | Paying down high-interest debt, avoiding unnecessary debt, and consolidating debt. | Reduces financial stress, improves credit score, and frees up resources for savings and investments. |

| Planning for Taxes | Staying informed about tax laws, seeking professional tax advice, and adjusting financial strategies. | Minimizes tax liabilities, optimizes tax outcomes, and ensures compliance with tax laws. |

6.6 Case Studies in Financial Planning

- Retirement Planning: A 30-year-old starts saving early, diversifies investments, and maximizes employer matching contributions to retire comfortably.

- Debt Management: A family pays off high-interest debt, consolidates loans, and creates a budget to improve financial stability.

- Investment Strategy: An individual invests in a mix of stocks, bonds, and real estate to achieve long-term financial goals.

6.7 How Income-partners.net Supports Financial Planning

Income-partners.net offers resources and expertise to help businesses and individuals with long-term financial planning. The platform provides access to financial tools, expert insights, and networking opportunities.

7. Navigating Economic Uncertainty with Business Partnerships

Business partnerships can provide stability and growth opportunities during economic uncertainty.

7.1 Risk Sharing

Partnerships allow businesses to share risks and resources, reducing individual exposure to economic downturns.

- Financial Risk: Sharing financial burdens can make it easier to weather economic storms.

- Market Risk: Diversifying into new markets can reduce reliance on a single region.

- Operational Risk: Sharing operational responsibilities can improve efficiency and reduce workload.

7.2 Resource Pooling

Partnerships enable businesses to pool resources, enhancing their ability to compete and innovate.

- Financial Resources: Pooling capital can fund expansion and development.

- Human Resources: Sharing expertise can improve operational effectiveness.

- Technological Resources: Collaborating on technology can drive innovation and efficiency.

7.3 Market Expansion

Partnerships can facilitate entry into new markets, diversifying revenue streams.

- Geographic Expansion: Partnering with local businesses can ease entry into new regions.

- Customer Base Expansion: Collaborating with businesses with different customer segments can increase market reach.

- Product/Service Expansion: Developing new products and services together can meet changing customer needs.

7.4 Innovation and Adaptability

Partnerships can foster innovation and adaptability.

- Shared Knowledge: Pooling expertise can generate new ideas and approaches.

- Agile Response: Adapting to market changes together can enhance resilience.

- Flexibility: Partnerships offer flexibility to adjust strategies as needed.

7.5 Legal and Contractual Safeguards

Ensuring legal and contractual safeguards can protect the interests of all parties involved.

- Clear Agreements: Develop clear partnership agreements outlining roles, responsibilities, and profit sharing.

- Legal Counsel: Consult with legal professionals to ensure compliance with relevant laws and regulations.

- Risk Management: Develop strategies to manage potential risks and resolve disputes.

7.6 Case Studies of Successful Partnerships in Uncertainty

- Automotive Industry: Automakers collaborate on electric vehicle technology.

- Healthcare Sector: Hospitals partner to share resources and improve patient care.

- Technology Sector: Tech firms collaborate to develop new software and hardware solutions.

Benefits of Business Partnerships in Economic Uncertainty

| Benefit | Description | Impact |

|---|---|---|

| Risk Sharing | Distributing financial, market, and operational risks among partners. | Reduces individual exposure, enhances stability, and improves resilience. |

| Resource Pooling | Combining financial, human, and technological resources to enhance competitiveness. | Improves operational effectiveness, drives innovation, and funds expansion. |

| Market Expansion | Entering new geographic areas, reaching different customer segments, and developing new offerings. | Diversifies revenue streams, increases market reach, and meets changing customer needs. |

| Innovation/Adaptability | Fostering shared knowledge, agile response, and strategic flexibility among partners. | Generates new ideas, enhances resilience, and allows for quick adjustments. |

| Legal Safeguards | Developing clear agreements, seeking legal counsel, and implementing risk management strategies. | Protects interests, ensures compliance, and mitigates potential disputes. |

7.7 How Income-partners.net Supports Partnerships

Income-partners.net provides a platform for businesses to connect, collaborate, and thrive. It offers resources and expertise to help businesses navigate economic uncertainty.

8. Frequently Asked Questions (FAQs)

1. Is the federal income tax really going away?

No, despite some political promises, it is highly unlikely that the federal income tax will be completely eliminated due to the necessity of funding government programs and the limitations of alternative revenue sources.

2. Why is the IRS still needed even if income taxes are reduced?

The IRS is needed to monitor income levels and ensure compliance with tax laws.

3. Can tariffs replace income tax revenue?

No, tariff revenue is insufficient to replace the revenue generated by income taxes.

4. What are the main challenges to tax reform?

The main challenges include economic impact, political feasibility, and public opinion.

5. How do tax policies affect business partnerships?

Tax policies affect the structure, benefits, challenges, and optimization strategies of business partnerships.

6. What strategies can businesses use to maximize revenue in a changing tax environment?

Businesses can diversify income streams, leverage technology, optimize costs, form strategic partnerships, and enhance customer engagement.

7. What is the importance of long-term financial planning?

Long-term financial planning is essential for setting goals, developing a budget, investing wisely, managing debt, and planning for tax changes.

8. How can business partnerships help navigate economic uncertainty?

Business partnerships can provide risk sharing, resource pooling, market expansion, innovation, and adaptability during economic uncertainty.

9. What alternative revenue sources could replace income taxes?

Alternative revenue sources include Value-Added Tax (VAT), carbon tax, wealth tax, consumption tax, and user fees and excise taxes.

10. How can Income-partners.net help businesses and individuals with financial planning?

Income-partners.net provides resources, tools, and expert insights to help businesses and individuals with financial planning.

9. Call To Action

Navigate the complexities of changing tax policies and discover new revenue opportunities with income-partners.net. Explore partnership strategies, access expert insights, and connect with potential collaborators to thrive in today’s economic landscape. Visit income-partners.net to start building profitable partnerships and securing your financial future.

Address: 1 University Station, Austin, TX 78712, United States

Phone: +1 (512) 471-3434

Website: income-partners.net