Is Operating Income The Same As Ebit (Earnings Before Interest and Taxes)? Yes, operating income and EBIT are the same thing; it is a company’s earnings before interest and taxes. Understanding this equivalence is crucial for forging successful partnerships that boost your bottom line. At income-partners.net, we offer strategies and resources to navigate financial landscapes and identify lucrative collaborations. With the right know-how, you can leverage operating income for strategic growth.

1. Understanding EBIT and Operating Income

Is operating income the same as EBIT? Yes, operating income is the same as EBIT, representing a company’s earnings from its core business operations before accounting for interest and taxes. According to a study by the University of Texas at Austin’s McCombs School of Business, understanding EBIT is critical for assessing a company’s fundamental profitability. This metric helps in comparing companies on an equal footing, irrespective of their capital structure or tax strategies.

EBIT, or Earnings Before Interest and Taxes, is a key indicator of a company’s profitability from its core operations. It’s often referred to as operating income and is found on the income statement. EBIT is calculated by subtracting the cost of goods sold (COGS) and operating expenses from revenue. This calculation provides a clear picture of how well a company is performing in its primary business activities. EBIT is a valuable tool for investors and analysts because it allows them to compare the profitability of different companies without the distortions of debt financing and tax policies. It focuses solely on the operational efficiency of the business.

1.1 What EBIT Represents

EBIT is calculated as gross profit minus operating expenses, often adjusted for non-recurring charges. It signifies the core, recurring business income before considering capital structure and taxes.

1.2 Why EBIT Matters

EBIT is vital because it normalizes financial comparisons between companies. For instance, a company with high debt might show lower net income due to interest expenses, but EBIT allows a fairer comparison based on operational efficiency.

2. How to Calculate EBIT

What is the best way to calculate EBIT? The best way to calculate EBIT depends on the available information, but generally, starting with revenue and subtracting COGS and operating expenses is the most straightforward approach. Income-partners.net can guide you through this process with tailored financial analysis tools and expert support. Understanding this calculation is fundamental for assessing potential partnership opportunities.

Calculating EBIT can be done in several ways, depending on the available data. Here are the primary methods:

2.1 Method 1: Revenue – COGS – Operating Expenses

This is the most direct method. Start with the total revenue, subtract the cost of goods sold (COGS), and then subtract all operating expenses.

Example:

- Revenue: $22,260,774

- COGS: $16,142,943

- Operating Expenses: $545,621 (Selling) + $452,551 (General & Administrative) + $27,738 (Other)

- EBIT = $22,260,774 – $16,142,943 – $545,621 – $452,551 – $27,738 = $5,091,822

2.2 Method 2: Operating Income + Non-Recurring Charges

If you already have the operating income figure, you can add back any non-recurring charges that may have reduced it.

Example:

- Operating Income: $847,142

- Non-Recurring Charges (Asset Impairment): $19,409

- EBIT = $847,142 + $19,409 = $866,551

2.3 Method 3: Net Income + Taxes + Interest + Non-Core Items

Though less recommended, you can start with net income and add back taxes, interest expenses, non-core income/expenses, and non-recurring charges. This method is more complex and prone to errors.

Example:

- Net Income: $X

- Taxes: $Y

- Net Interest Expense: $Z

- Non-Core Income/Expenses: $A

- Non-Recurring Charges: $B

- EBIT = $X + $Y + $Z + $A + $B

2.4 Choosing the Right Method

The first method is preferable if you want a detailed view of the company’s operational efficiency. The second is simpler if operating income is already known, and non-recurring charges are the only adjustments needed. The third is generally avoided due to its complexity.

3. EBIT vs. EBITDA vs. Net Income

How does EBIT differ from EBITDA and Net Income? EBIT, EBITDA, and Net Income each measure a company’s profitability differently. EBIT focuses on core business profitability, while EBITDA adds back depreciation and amortization to reflect cash flow. Net Income represents profit after all expenses, including taxes and interest. Income-partners.net can help you interpret these metrics to make informed partnership decisions.

| Metric | Definition | Focus |

|---|---|---|

| EBIT | Earnings Before Interest and Taxes; a proxy for core, recurring business profitability, before the impact of capital structure and taxes. | Core business profitability |

| EBITDA | Earnings Before Interest, Taxes, Depreciation, and Amortization; a proxy for core, recurring business cash flow from operations. | Core business cash flow from operations |

| Net Income | Profit after taxes, interest, and non-core business activities. | Overall profit after all expenses |

EBIT, EBITDA, and Net Income each serve a distinct purpose in financial analysis. EBIT zeroes in on the operational profitability of a company, excluding the impacts of debt and taxes. EBITDA goes a step further by also excluding depreciation and amortization, providing a clearer picture of cash flow generation from operations. Net Income, on the other hand, represents the bottom line, accounting for all expenses, including interest, taxes, and any non-core activities. The choice of which metric to use depends on the specific analysis being performed.

3.1 EBIT (Earnings Before Interest and Taxes)

EBIT, or Earnings Before Interest and Taxes, is a financial metric that measures a company’s profitability from its core operations, excluding the effects of interest and taxes. It is calculated by subtracting operating expenses from revenue. EBIT provides a clear picture of a company’s ability to generate profit from its primary business activities, without the influence of debt financing or tax strategies. This makes it a useful tool for comparing companies with different capital structures or tax situations.

3.2 EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization)

EBITDA, or Earnings Before Interest, Taxes, Depreciation, and Amortization, builds upon EBIT by also excluding depreciation and amortization expenses. These are non-cash expenses that can distort a company’s true cash flow. EBITDA is often used as a proxy for a company’s operating cash flow, as it represents the cash a company generates from its operations before accounting for capital investments or financing activities. However, it’s important to note that EBITDA does not fully represent cash flow, as it excludes working capital changes and capital expenditures.

3.3 Net Income

Net Income, often referred to as the “bottom line,” is a company’s profit after all expenses have been deducted from revenue, including interest, taxes, depreciation, and amortization. It represents the actual profit available to shareholders after all obligations have been met. Net Income is a widely used measure of profitability, but it can be influenced by various factors, such as accounting methods, financing decisions, and tax strategies. As a result, it’s important to consider other metrics, such as EBIT and EBITDA, to gain a more complete understanding of a company’s financial performance.

4. Why EBIT is Useful

What makes EBIT a useful metric for financial analysis? EBIT offers a clear view of a company’s operational profitability, unaffected by financing decisions or tax strategies. This makes it ideal for comparing companies with different capital structures. At income-partners.net, we use EBIT to help our partners identify businesses with solid operational performance.

4.1 Operational Efficiency

EBIT focuses solely on a company’s operational efficiency, excluding the impacts of debt and taxes. This allows analysts and investors to assess how well a company is performing in its core business activities, without the distortions of financing decisions or tax strategies.

4.2 Comparison Across Companies

EBIT facilitates easier comparisons between companies with different capital structures or tax situations. By excluding interest and taxes, EBIT provides a level playing field for assessing the underlying profitability of different businesses.

4.3 Indicator of Financial Health

EBIT serves as an indicator of a company’s ability to meet its financial obligations. By comparing EBIT to interest expense, analysts can assess a company’s ability to cover its debt payments. A higher EBIT relative to interest expense indicates a stronger financial position.

5. Real-World Applications of EBIT

Where is EBIT used in financial modeling and valuation? EBIT is a crucial starting point for calculating NOPAT and UFCF in DCF models, and it features prominently in LBO, M&A, and credit models. Income-partners.net leverages EBIT in its valuation models to provide accurate and insightful financial analysis for potential partners.

5.1 Financial Modeling

EBIT is a fundamental input in financial models, particularly in discounted cash flow (DCF) analysis. It’s used to calculate net operating profit after taxes (NOPAT), which is then used to derive unlevered free cash flow (UFCF).

5.2 Valuation

EBIT is used as a valuation multiple, such as Enterprise Value / EBIT, to assess a company’s relative valuation compared to its peers. However, adjustments may be necessary under IFRS due to lease accounting (discussed below).

5.3 Capital Structure Analysis

EBIT helps in assessing a company’s capital structure. By comparing EBIT to interest expenses, investors can gauge the company’s ability to cover its debt obligations.

6. EBIT in Financial Models and Valuation

How is EBIT used in financial models and valuation processes? EBIT serves as a crucial starting point for calculating NOPAT and Unlevered Free Cash Flow (UFCF) in DCF models and is used extensively in financial models for LBOs, M&A, and credit analysis. At income-partners.net, we emphasize the importance of sound assumptions when forecasting EBIT to ensure accurate financial modeling.

EBIT is a cornerstone in financial modeling and valuation, playing a crucial role in various analyses:

6.1 DCF Modeling

In Discounted Cash Flow (DCF) models, EBIT is the foundation for calculating Net Operating Profit After Taxes (NOPAT) and Unlevered Free Cash Flow (UFCF). These metrics are essential for determining the intrinsic value of a company.

6.2 LBO, M&A, and Credit Models

EBIT is used extensively in financial models for Leveraged Buyouts (LBOs), Mergers & Acquisitions (M&A), and credit analysis. It helps assess the financial viability and potential returns of these transactions.

6.3 Valuation Multiples

EBIT is also used as a valuation multiple, such as Enterprise Value / EBIT. This multiple helps compare a company’s valuation to its peers and assess whether it is overvalued or undervalued.

6.4 The Importance of Sound Assumptions

When forecasting EBIT in financial models, it’s crucial to have sound assumptions. For example, if you project that a company’s EBIT will increase from $100 to $110, you need to understand why that happens. Is it due to increased sales volume, higher prices, or reduced expenses? Each of these factors should be carefully analyzed and supported by realistic assumptions.

6.5 Example of EBIT in Valuation

Consider two companies, Company A and Company B, operating in the same industry. Company A has an EBIT of $50 million, while Company B has an EBIT of $40 million. If both companies have similar growth prospects and risk profiles, Company A would generally be considered more valuable based on its higher operating profitability.

6.6 Advanced Financial Modeling Techniques

In advanced financial modeling, EBIT is often used in conjunction with other metrics and ratios to provide a more comprehensive view of a company’s financial performance. For example, analysts may use EBIT to calculate interest coverage ratios, which measure a company’s ability to meet its debt obligations.

6.7 Benefits of Understanding EBIT

Understanding EBIT is essential for anyone involved in financial analysis, investing, or corporate finance. It provides a clear picture of a company’s operating profitability and helps in making informed decisions about investments, acquisitions, and capital allocation.

7. EBIT Under IFRS for International Companies

How does IFRS impact the use of EBIT? Under IFRS, lease accounting can distort EBIT due to the way operating leases are recorded. It’s often better to use EBITDA and ensure that Enterprise Value includes the Lease Liability for non-U.S.-based companies. Income-partners.net provides expert guidance on navigating these accounting differences to ensure accurate financial comparisons.

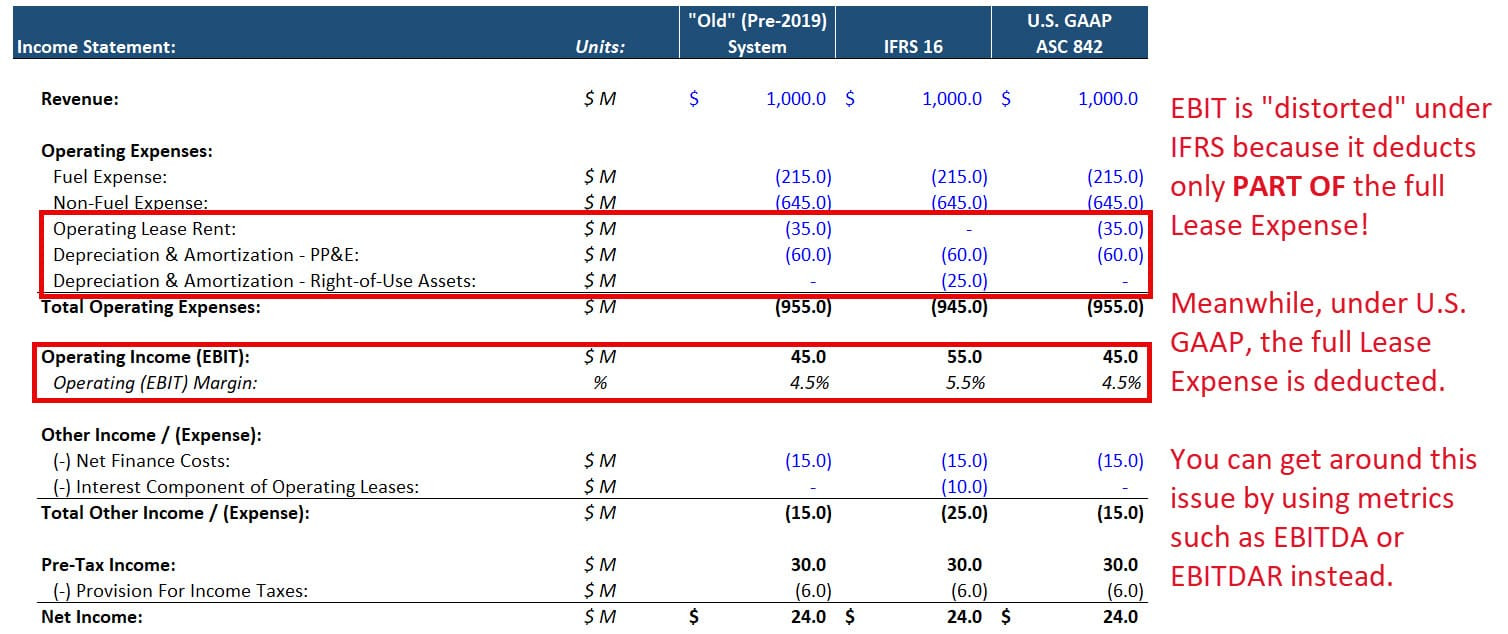

7.1 Impact of Lease Accounting

Under International Financial Reporting Standards (IFRS), lease accounting can distort EBIT due to the way operating leases are recorded. In 2019, companies began to record operating leases directly on their balance sheets under IFRS 16 (ASC 842 in the U.S.). This involves recognizing a “Right-of-Use Asset” on the assets side and a “Lease Liability” on the liabilities & equity side.

7.2 Differences from U.S. GAAP

Under U.S. Generally Accepted Accounting Principles (GAAP), companies still list the rental expense for operating leases as a standard operating expense on their income statements. However, under IFRS, companies now split this rental expense into “Lease Interest” and “Lease Depreciation,” even though it is still a simple cash expense in reality.

7.3 Distortion of EBIT

As a result, under IFRS, EBIT only deducts part of the operating lease expense – the Lease Depreciation – which makes it problematic to use in valuations. When calculating a valuation multiple such as Enterprise Value / EBIT, if a liability is counted within Enterprise Value, the denominator (EBIT) should exclude or add back the entire corresponding lease expense.

7.4 The Simplest Solution

The simplest solution is to skip EBIT in valuation multiples, use Enterprise Value / EBITDA instead, and ensure that Enterprise Value includes the Lease Liability for non-U.S.-based companies.

7.5 Example Scenario

Consider a company that leases office space. Under U.S. GAAP, the company would record the full rental expense as an operating expense, reducing EBIT. Under IFRS, the company would record lease depreciation and lease interest, with only the depreciation affecting EBIT. This difference can make it difficult to compare the company’s EBIT to that of its U.S. counterparts.

7.6 Implications for Valuation

When valuing international companies using EBIT, it’s important to be aware of these differences in lease accounting. Failure to account for these differences can lead to inaccurate valuations and investment decisions.

7.7 Recommendations

For non-U.S.-based companies reporting under IFRS, it’s often better to use EBITDA rather than EBIT for valuation purposes. Additionally, ensure that Enterprise Value includes the Lease Liability to provide a more accurate picture of the company’s financial position.

8. What is a “Good” EBIT Margin?

What constitutes a good EBIT margin? There’s no universal answer, as it varies by industry and company maturity. Large software firms often have margins of 40% or more, while manufacturing companies typically have lower margins. Income-partners.net helps you benchmark EBIT margins against industry peers to assess financial health accurately.

Determining what constitutes a “good” EBIT margin is not a one-size-fits-all answer. It largely depends on the industry, the company’s maturity, and the specific economic environment. Here are some guidelines:

8.1 Industry Benchmarks

Different industries have different average EBIT margins. For example, large, mature software companies like Microsoft and Oracle often have operating margins of 40% or more. This is because they have high operating leverage; the cost of producing an additional unit of software is very low compared to the initial development cost.

8.2 Manufacturing Companies

On the other hand, manufacturing companies typically have much lower EBIT margins. This is because they have higher costs associated with physical products: raw materials, parts, inventory, and manufacturing facilities. For example, a steel company like Steel Dynamics might have operating margins between 10% and 20% in most years.

8.3 Company Maturity

The maturity of a company also plays a role in its EBIT margin. Newer, high-growth companies often have lower EBIT margins because they are investing heavily in sales, marketing, and research and development to grow their market share. As they mature and achieve economies of scale, their EBIT margins tend to increase.

8.4 Example Scenarios

- Software Company: A software company with an EBIT margin of 45% would generally be considered to have a very healthy profit margin.

- Manufacturing Company: A manufacturing company with an EBIT margin of 15% would be considered to be performing well in its industry.

- High-Growth Startup: A high-growth startup with an EBIT margin of 5% might be considered to be on track if it is rapidly growing its revenue and market share.

8.5 How to Determine if an EBIT Margin is “Good”

To determine if a company’s EBIT margin is “good,” it’s important to compare it to its peers in the same industry and consider its stage of growth. A company with an EBIT margin that is significantly higher than its peers may be outperforming them, while a company with a significantly lower EBIT margin may be struggling.

8.6 Factors Influencing EBIT Margin

Several factors can influence a company’s EBIT margin, including:

- Pricing Power: Companies with strong brands or unique products may have the ability to charge higher prices, leading to higher margins.

- Cost Structure: Companies with efficient cost structures can produce goods or services at a lower cost, leading to higher margins.

- Operating Efficiency: Companies that are able to manage their operations efficiently can minimize expenses and maximize profitability.

- Competition: Companies in highly competitive industries may face pressure to lower prices, leading to lower margins.

9. Finding Partnership Opportunities with Income-Partners.net

How can income-partners.net help me find the right business partners? Income-partners.net offers diverse information on partnership types, strategies for building effective relationships, and potential collaboration opportunities. We can help you navigate the complexities of business partnerships to boost your income.

9.1 Identifying the Right Partners

Finding the right business partners is crucial for success. At income-partners.net, we provide insights and resources to help you identify potential partners who align with your goals and values.

9.2 Types of Partnerships

There are various types of business partnerships, each with its own advantages and disadvantages. Some common types include:

- Strategic Alliances: Partnerships between companies with complementary strengths to achieve a common goal.

- Joint Ventures: A new entity created by two or more companies to pursue a specific project or opportunity.

- Distribution Partnerships: Agreements where one company distributes another company’s products or services.

- Affiliate Partnerships: Arrangements where one company promotes another company’s products or services in exchange for a commission.

9.3 Strategies for Building Effective Relationships

Building strong relationships with your business partners is essential for long-term success. Some key strategies include:

- Clear Communication: Open and honest communication is crucial for building trust and avoiding misunderstandings.

- Shared Goals: Align your goals and objectives with those of your partners to ensure that you are working towards the same outcomes.

- Mutual Respect: Treat your partners with respect and value their contributions.

- Regular Meetings: Schedule regular meetings to discuss progress, address issues, and strengthen your relationship.

9.4 Potential Collaboration Opportunities

Income-partners.net helps you discover potential collaboration opportunities by providing a platform to connect with other businesses and individuals who are seeking partners. Whether you are looking for funding, expertise, or market access, our platform can help you find the right partners to achieve your goals.

9.5 Success Stories

Many businesses have achieved remarkable success through strategic partnerships. For example, two small businesses might combine their resources and expertise to develop a new product or enter a new market. A larger company may partner with a startup to gain access to innovative technologies or business models.

9.6 Benefits of Partnering with Income-Partners.net

Partnering with income-partners.net offers numerous benefits, including:

- Access to a Network of Potential Partners: Connect with a diverse range of businesses and individuals who are seeking partners.

- Expert Guidance: Receive expert advice and support on all aspects of business partnerships, from finding the right partners to negotiating agreements.

- Increased Revenue: Boost your revenue by leveraging the resources and expertise of your partners.

- Reduced Costs: Lower your costs by sharing resources and expenses with your partners.

- Enhanced Innovation: Drive innovation by collaborating with partners who bring new ideas and perspectives.

10. Key Takeaways and Next Steps

What are the key steps to take after understanding EBIT and partnership opportunities? Focus on using EBIT to evaluate potential partners, understanding the nuances of lease accounting under IFRS, and leveraging income-partners.net to find strategic alliances. Visit our website today to explore partnership opportunities and boost your income!

10.1 Review the Basics

- EBIT Defined: EBIT, or Earnings Before Interest and Taxes, is the same as operating income and represents a company’s earnings from its core business operations before accounting for interest and taxes.

- Calculation Methods: EBIT can be calculated by subtracting the cost of goods sold (COGS) and operating expenses from revenue, or by adding back non-recurring charges to operating income.

- Comparison with EBITDA and Net Income: EBIT focuses on core business profitability, while EBITDA adds back depreciation and amortization to reflect cash flow, and Net Income represents profit after all expenses.

10.2 Evaluate Potential Partners Using EBIT

When evaluating potential business partners, use EBIT as a key metric to assess their operational efficiency and profitability. This will help you identify partners with strong financial fundamentals.

10.3 Understand IFRS and Lease Accounting

If you are considering partnerships with international companies, be aware of the nuances of lease accounting under IFRS. Remember that lease accounting can distort EBIT, so it is often better to use EBITDA for valuation purposes.

10.4 Leverage Income-Partners.net

Visit income-partners.net to explore partnership opportunities and connect with other businesses and individuals who are seeking partners. Our platform offers resources, expert guidance, and access to a network of potential partners to help you achieve your business goals.

10.5 Contact Information

For more information about income-partners.net, you can contact us at:

- Address: 1 University Station, Austin, TX 78712, United States

- Phone: +1 (512) 471-3434

- Website: income-partners.net

FAQ: Understanding EBIT and Operating Income

Here are some frequently asked questions about EBIT and operating income:

1. What is EBIT and why is it important?

EBIT, or Earnings Before Interest and Taxes, measures a company’s profitability from its core operations, excluding the effects of interest and taxes. It is important because it provides a clear picture of a company’s ability to generate profit from its primary business activities, without the influence of debt financing or tax strategies.

2. How do you calculate EBIT?

EBIT can be calculated by subtracting the cost of goods sold (COGS) and operating expenses from revenue. Alternatively, if you have the operating income figure, you can add back any non-recurring charges that may have reduced it.

3. What is the difference between EBIT and EBITDA?

EBITDA, or Earnings Before Interest, Taxes, Depreciation, and Amortization, builds upon EBIT by also excluding depreciation and amortization expenses. These are non-cash expenses that can distort a company’s true cash flow.

4. What is the difference between EBIT and Net Income?

Net Income, often referred to as the “bottom line,” is a company’s profit after all expenses have been deducted from revenue, including interest, taxes, depreciation, and amortization.

5. How is EBIT used in financial modeling and valuation?

EBIT is a fundamental input in financial models, particularly in discounted cash flow (DCF) analysis. It’s used to calculate net operating profit after taxes (NOPAT), which is then used to derive unlevered free cash flow (UFCF).

6. What is a good EBIT margin?

There is no one-size-fits-all answer to this question. It largely depends on the industry, the company’s maturity, and the specific economic environment.

7. How does IFRS impact the use of EBIT?

Under International Financial Reporting Standards (IFRS), lease accounting can distort EBIT due to the way operating leases are recorded. As a result, it’s often better to use EBITDA for valuation purposes.

8. Can EBIT be negative?

Yes, EBIT can be negative if a company’s operating expenses exceed its revenue. This indicates that the company is losing money from its core operations.

9. What are some limitations of using EBIT?

EBIT does not reflect a company’s cash flow, as it excludes non-cash expenses such as depreciation and amortization. Additionally, it does not take into account a company’s capital structure or tax strategies.

10. Where can I find more information about EBIT?

You can find more information about EBIT on websites such as income-partners.net, which offers insights and resources on financial analysis and business partnerships. Additionally, you can consult financial textbooks and articles for a more in-depth understanding of this metric.

11. How can income-partners.net help me find business partners?

Income-partners.net provides a platform to connect with other businesses and individuals who are seeking partners. Whether you are looking for funding, expertise, or market access, our platform can help you find the right partners to achieve your goals.

EBIT vs EBITDA vs Net Income

EBIT vs EBITDA vs Net Income

At income-partners.net, we’re dedicated to helping you navigate the complexities of financial metrics like EBIT and find the perfect partners to drive your business success. Don’t miss out on the opportunity to elevate your income and expand your network. Visit us today and take the first step towards a prosperous future!