EBIT, often referred to as Operating Income, is indeed largely the same as operating income. Income-partners.net offers a wealth of resources to help you understand the nuances of EBIT, its significance in financial analysis, and how it can play a crucial role in forging profitable partnerships and increasing your bottom line. Let’s explore this further and see how understanding EBIT can help you leverage beneficial collaborations, create strategic alliances, and achieve financial success. Dive in and unlock the potential of this crucial metric.

1. What is EBIT (Earnings Before Interest and Taxes)?

EBIT, which stands for Earnings Before Interest and Taxes, is essentially the same as operating income. It represents a company’s profit from its core business operations, excluding interest expenses and income taxes. Therefore, EBIT shows how profitable a company is from its operations alone, without considering the impact of debt and taxes.

EBIT is calculated by subtracting the cost of goods sold and operating expenses from total revenue. It provides a clear picture of a company’s operating performance and profitability. Understanding EBIT can help you assess the financial viability of potential partnerships, as explained further on income-partners.net.

To further elaborate:

- Core Business Income: EBIT emphasizes the earnings generated from the primary activities of the company, stripping away the effects of financial leverage (interest) and governmental levies (taxes).

- Recurring Revenue: It helps in evaluating the stability of a company’s earnings over time, focusing on sustainable income sources.

- Exclusion of Non-Operating Items: EBIT intentionally excludes items like interest income, gains/losses from investments, and other non-operating incomes, which can skew the actual operational performance.

2. How is EBIT Calculated?

EBIT can be calculated using two primary methods, each offering a unique perspective on a company’s financial performance. Both of these methods are thoroughly explored on income-partners.net, equipping you with the tools to make informed decisions.

Method 1: Revenue Less COGS and Operating Expenses

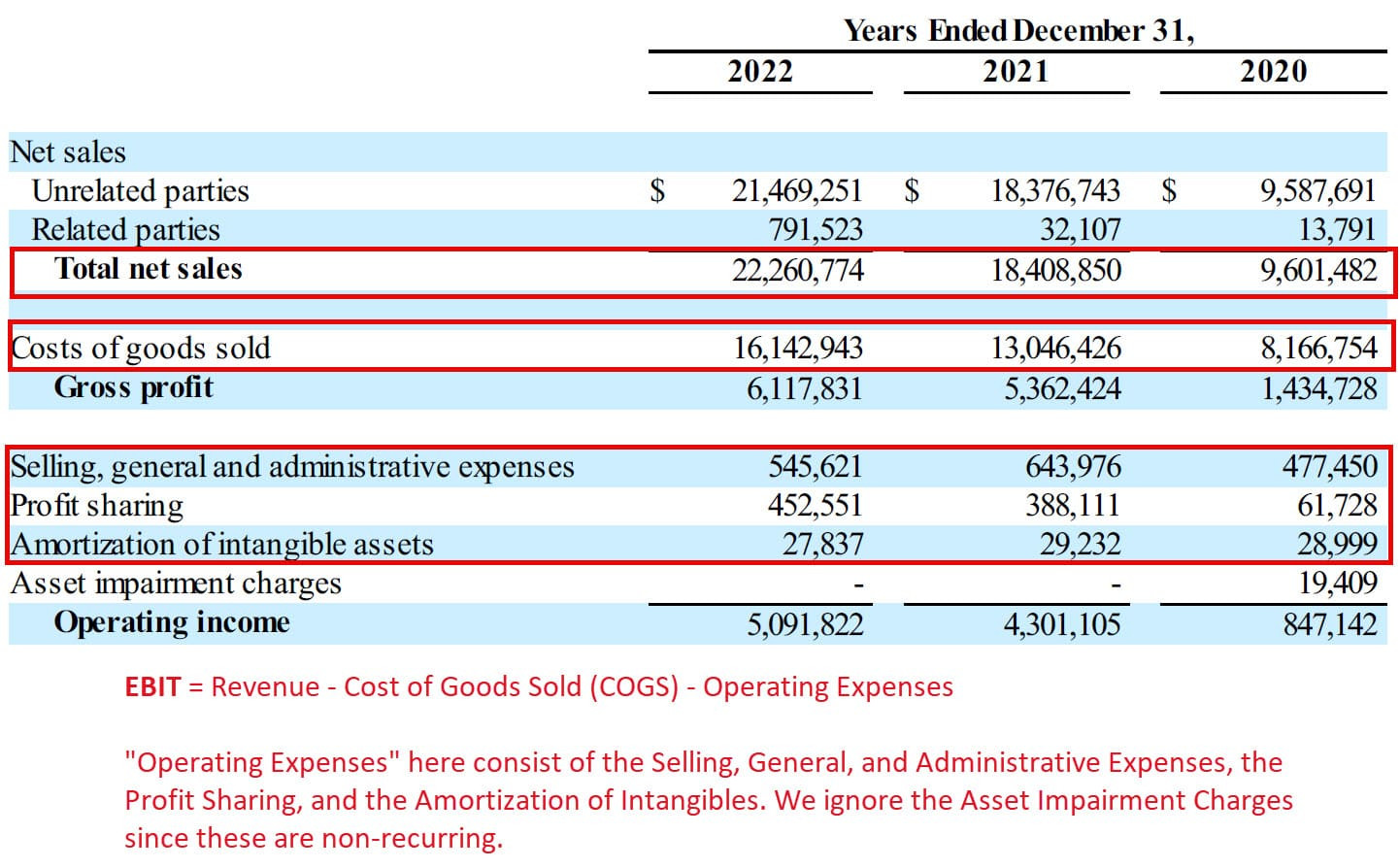

The most straightforward method to calculate EBIT involves starting with total revenue and subtracting the cost of goods sold (COGS) and all operating expenses. This approach provides a clear view of the earnings generated from core business activities before considering financial and tax implications.

EBIT = Total Revenue − Cost of Goods Sold (COGS) − Operating Expenses

- Total Revenue: Represents the total income generated from sales of goods or services.

- Cost of Goods Sold (COGS): Includes direct costs related to producing goods or services.

- Operating Expenses: Encompasses all other expenses incurred in running the business, such as salaries, rent, marketing costs, and depreciation.

For example, if a company has total revenue of $1,000,000, a COGS of $600,000, and operating expenses of $200,000, the EBIT would be:

EBIT = $1,000,000 – $600,000 – $200,000 = $200,000

EBIT calculation using revenue method

EBIT calculation using revenue method

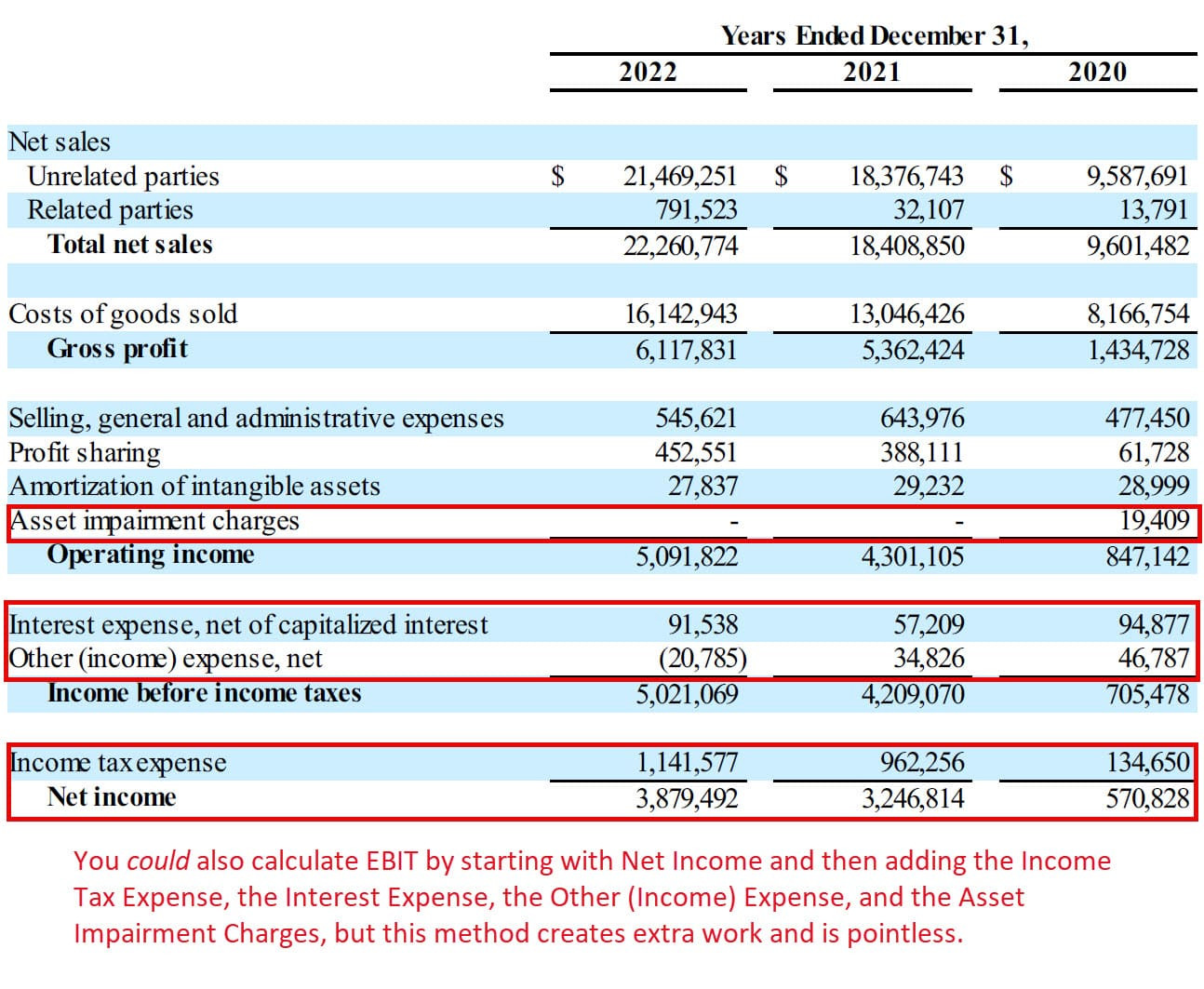

Method 2: Net Income Plus Interest and Taxes

Alternatively, EBIT can be derived by starting with net income and adding back interest expenses and income taxes. This method is useful when you already have the net income figure and want to work backward to find the operating income.

EBIT = Net Income + Interest Expense + Income Taxes

- Net Income: The company’s profit after all expenses, interest, and taxes have been deducted.

- Interest Expense: The cost incurred for borrowing money.

- Income Taxes: The taxes paid on the company’s profits.

For instance, if a company reports a net income of $100,000, has an interest expense of $30,000, and pays $20,000 in income taxes, the EBIT would be:

EBIT = $100,000 + $30,000 + $20,000 = $150,000

EBIT calculation starting with net income

EBIT calculation starting with net income

3. Why is EBIT Important?

EBIT serves as a critical metric for several reasons, offering invaluable insights into a company’s financial health and operational efficiency. Understanding its significance can greatly enhance your strategic partnerships, a key focus at income-partners.net.

- Assessing Operational Efficiency: EBIT provides a clear view of a company’s profitability from its core operations, excluding the impact of capital structure and tax policies. This allows investors and analysts to evaluate how well a company manages its business activities.

- Comparing Companies: EBIT enables a more equitable comparison of companies, especially those with different capital structures or tax situations. By stripping out interest and taxes, it focuses on the underlying business performance.

- Predicting Future Earnings: EBIT is often used as a baseline for forecasting future earnings. Analysts can make projections based on a company’s historical EBIT, adjusted for expected changes in business conditions.

- Valuation Metric: EBIT is a key component in various valuation multiples, such as EV/EBIT (Enterprise Value to EBIT), which helps in determining the fair value of a company. This is particularly useful when evaluating potential acquisition targets or investment opportunities.

- Performance Measurement: Management uses EBIT to measure the performance of various business units or segments. It helps in identifying which areas are most profitable and where improvements are needed.

4. EBIT vs. EBITDA: What’s the Difference?

EBIT and EBITDA are both essential profitability metrics, but they offer different perspectives on a company’s financial performance. The primary difference lies in the inclusion of depreciation and amortization expenses.

- EBIT (Earnings Before Interest and Taxes): Measures a company’s operating profit, excluding interest and taxes. It reflects the profitability of a company’s core operations.

- EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization): Extends EBIT by excluding depreciation and amortization expenses. EBITDA is often used as a proxy for cash flow, as it adds back non-cash expenses.

The formula for EBITDA is:

EBITDA = EBIT + Depreciation + Amortization

Key Differences Summarized

| Feature | EBIT | EBITDA |

|---|---|---|

| Definition | Earnings before interest and taxes | Earnings before interest, taxes, depreciation, and amortization |

| Formula | Revenue – COGS – Operating Expenses | EBIT + Depreciation + Amortization |

| Focus | Operating profitability | Cash flow proxy |

| Depreciation Impact | Includes depreciation, reflecting the wear and tear of assets | Excludes depreciation, providing a clearer picture of current operational cash flow |

| Use Cases | Assessing core business profitability, comparing companies with different capital structures | Evaluating operational cash flow, especially for companies with significant capital investments |

Differences between EBIT EBITDA and Net Income

Differences between EBIT EBITDA and Net Income

When to Use Each Metric

- EBIT: Use EBIT when you want to assess the operating profitability of a company, especially when comparing companies with different capital structures or tax situations.

- EBITDA: Use EBITDA when you want a proxy for cash flow, particularly for companies with significant capital investments and high depreciation expenses.

5. What are the Limitations of Using EBIT?

While EBIT is a valuable metric, it has certain limitations that must be considered to gain a comprehensive understanding of a company’s financial performance.

- Ignores Capital Expenditures: EBIT does not account for capital expenditures (CapEx), which are necessary for maintaining and growing a business. This can be misleading, as companies with high CapEx requirements may appear more profitable than they actually are.

- Excludes Working Capital Changes: Changes in working capital (e.g., accounts receivable, inventory) are not reflected in EBIT. These changes can significantly impact a company’s cash flow and financial health.

- Non-Cash Items: While EBIT excludes depreciation and amortization, it does not exclude all non-cash items. For example, stock-based compensation, which is a non-cash expense, is included in operating expenses and thus affects EBIT.

- One-Time Gains and Losses: EBIT includes one-time gains and losses, which can distort the true picture of a company’s recurring profitability. It’s important to adjust EBIT for these non-recurring items to get a clearer view of performance.

- Interest and Taxes: While excluding interest and taxes allows for easier comparison between companies, it also means that EBIT doesn’t provide a complete view of a company’s overall profitability. Interest expenses and taxes are real costs that affect the bottom line.

6. How is EBIT Used in Financial Modeling and Valuation?

EBIT is a foundational component in financial modeling and valuation, playing a crucial role in determining a company’s worth and future prospects.

- Discounted Cash Flow (DCF) Analysis: EBIT is used to calculate Net Operating Profit After Taxes (NOPAT), which is then used in the Unlevered Free Cash Flow (UFCF) calculation in a DCF model. The DCF model projects future cash flows and discounts them back to their present value to estimate the company’s intrinsic value.

- Valuation Multiples: EBIT is used in valuation multiples, such as Enterprise Value (EV) / EBIT. These multiples are used to compare a company’s valuation to its peers and to the overall market.

- Leveraged Buyout (LBO) Models: In LBO models, EBIT is used to assess the company’s ability to generate cash flow to service debt. It helps determine how much debt the company can take on and still meet its obligations.

- Mergers and Acquisitions (M&A) Models: EBIT is used to evaluate the financial impact of a merger or acquisition. It helps in determining the combined company’s profitability and cash flow.

In summary, EBIT is a critical input in various financial models and valuation techniques, providing a basis for assessing a company’s financial health, forecasting future performance, and determining its fair value. As noted by experts at the University of Texas at Austin’s McCombs School of Business, a sound understanding of EBIT is essential for accurate financial analysis and decision-making.

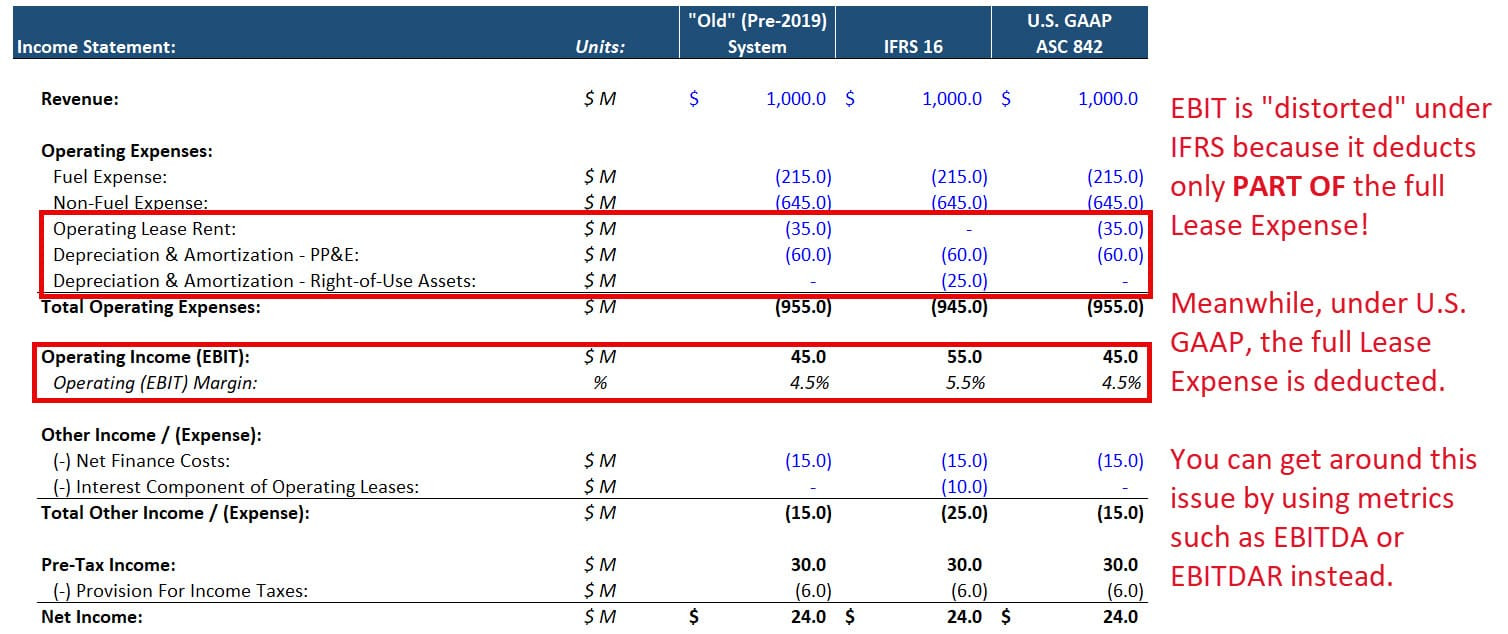

7. How Does EBIT Differ Under IFRS Compared to GAAP?

The accounting standards used can significantly impact how EBIT is calculated and interpreted. International Financial Reporting Standards (IFRS) and Generally Accepted Accounting Principles (GAAP) have key differences that affect EBIT.

- Operating Leases: Under IFRS 16, companies record operating leases directly on their balance sheets as a “Right-of-Use Asset” and a “Lease Liability.” This results in splitting rental expenses into “Lease Interest” and “Lease Depreciation.” Under GAAP, rental expenses for operating leases are listed as a standard operating expense.

- Impact on EBIT: Under IFRS, EBIT only deducts the “Lease Depreciation” portion of the operating lease expense, which can distort comparisons. In contrast, GAAP deducts the entire rental expense as an operating expense.

- Consistency in Valuation: For valuation purposes, it’s crucial to either exclude the entire lease expense or deduct it entirely for consistency. Skipping EBIT and using EBITDA instead can be a simpler solution under IFRS.

8. What Is Considered a Good EBIT Margin?

Determining what constitutes a “good” EBIT margin varies by industry, company maturity, and specific circumstances. There is no one-size-fits-all answer.

- Software Companies: Mature software companies like Microsoft and Oracle often have high EBIT margins, sometimes exceeding 40%, due to high operating leverage.

- Manufacturing Companies: Manufacturing companies typically have lower EBIT margins due to the high costs of physical products, raw materials, and factories.

- Comparable Analysis: EBIT margins are relative, and comparing them to those of comparable public companies is essential. This analysis helps determine whether a company’s margins are “good” or “bad” relative to its peers.

Even within the same industry, nuances exist. For example, Salesforce, while a software company, may have lower EBIT margins compared to Oracle because it’s in a high-growth phase and invests heavily in sales and marketing.

9. Real-World Examples of EBIT Analysis

Examining real-world examples can help clarify how EBIT is used in financial analysis and decision-making. Here are a couple of examples:

- Steel Dynamics: Steel Dynamics, a manufacturing company, has EBIT margins typically ranging from 10% to 20%. This indicates a healthy but not exceptionally high operating profit margin, typical for its industry.

- Microsoft: A mature software company, often boasts EBIT margins above 40%. This reflects the scalability and high operating leverage inherent in the software industry.

By analyzing these examples, investors and analysts can gain a better understanding of how EBIT margins vary across different industries and companies.

10. How Can Income-Partners.net Help You Leverage EBIT for Partnership Success?

Income-partners.net offers valuable resources and insights to help you understand and leverage EBIT for partnership success. By understanding how EBIT works, you can identify financially stable and profitable potential partners.

Identifying Potential Partners

- Financial Viability: Understanding EBIT helps you assess the financial health of potential partners. A strong EBIT indicates a company is profitable from its core operations, making it a more reliable partner.

- Strategic Alignment: By analyzing EBIT, you can ensure potential partners have similar profitability levels and operational efficiencies, leading to more aligned and successful partnerships.

Negotiating Partnership Terms

- Profit Sharing: EBIT can be used as a basis for negotiating profit-sharing agreements. A clear understanding of each partner’s EBIT helps in establishing fair and equitable terms.

- Performance Metrics: EBIT can be used as a key performance indicator (KPI) to measure the success of the partnership. Regular monitoring of EBIT helps in tracking progress and making necessary adjustments.

Maximizing Partnership Value

- Operational Synergies: By understanding how EBIT is generated, you can identify opportunities for operational synergies. Combining resources and expertise can lead to improved EBIT margins for both partners.

- Risk Management: Analyzing EBIT helps in identifying potential risks associated with the partnership. This allows you to develop strategies to mitigate these risks and ensure the long-term success of the partnership.

Income-partners.net provides a platform to connect with potential partners, access financial analysis tools, and gain insights from industry experts. Whether you’re a business owner, investor, or financial analyst, income-partners.net can help you leverage EBIT for partnership success.

In conclusion, EBIT and operating income are essentially the same and offer a valuable insight into a company’s profitability from its core operations. Understanding how to calculate and interpret EBIT can help you make informed decisions, assess potential partners, and maximize the value of your business relationships. By leveraging the resources and expertise available at income-partners.net, you can unlock the potential for profitable collaborations and achieve your financial goals.

Address: 1 University Station, Austin, TX 78712, United States.

Phone: +1 (512) 471-3434.

Website: income-partners.net.

Ready to transform your business through strategic partnerships? Visit income-partners.net today to discover potential partners, gain insights on building successful relationships, and explore strategies to boost your EBIT. Don’t wait – your next profitable partnership awaits.

FAQ About EBIT and Operating Income

1. Is EBIT always equal to operating income?

Yes, EBIT is generally the same as operating income. It represents a company’s earnings before interest and taxes, reflecting the profitability of its core business operations.

2. How do you calculate EBIT from net income?

To calculate EBIT from net income, add back interest expenses and income taxes to the net income figure: EBIT = Net Income + Interest Expense + Income Taxes.

3. Why is EBIT important for investors?

EBIT is important for investors because it provides a clear view of a company’s operational profitability, excluding the impact of capital structure and tax policies, making it easier to compare companies.

4. What are the main limitations of using EBIT?

The main limitations of using EBIT include ignoring capital expenditures, excluding working capital changes, and the inclusion of one-time gains and losses, which can distort the true picture of recurring profitability.

5. How does IFRS impact EBIT compared to GAAP?

Under IFRS, the treatment of operating leases can impact EBIT due to the recognition of lease assets and liabilities on the balance sheet, which differs from GAAP.

6. What is a good EBIT margin, generally speaking?

A “good” EBIT margin varies by industry, but generally, mature software companies may have margins above 40%, while manufacturing companies may have lower margins, typically between 10% and 20%.

7. How is EBIT used in discounted cash flow (DCF) analysis?

EBIT is used to calculate Net Operating Profit After Taxes (NOPAT), which is a key component in the Unlevered Free Cash Flow (UFCF) calculation within a DCF model, used to estimate a company’s intrinsic value.

8. Can EBIT be negative? What does that indicate?

Yes, EBIT can be negative. A negative EBIT indicates that a company’s operating expenses exceed its revenues, resulting in an operating loss.

9. What is the relationship between EBIT and free cash flow (FCF)?

While EBIT is not a direct proxy for free cash flow, it is related. EBIT is used as a starting point to calculate NOPAT, which is then used in the calculation of Unlevered Free Cash Flow (UFCF).

10. How can income-partners.net help with understanding EBIT for partnership opportunities?

income-partners.net provides resources and insights to help you understand and leverage EBIT for partnership success, identify financially stable partners, negotiate partnership terms, and maximize partnership value through operational synergies.