Is Ebit The Same As Net Income? No, EBIT is not the same as net income, as revealed by income-partners.net. Understanding the distinctions between these two profitability metrics is crucial for businesses aiming to attract strategic partnerships and boost their revenue streams. By exploring these financial nuances, you can identify ideal collaborators for income growth, revenue enhancement, and strategic expansion, while also navigating the nuances of financial statements and profitability metrics.

1. What is EBIT and How Does It Differ from Net Income?

EBIT, or Earnings Before Interest and Taxes, is not the same as net income. EBIT represents a company’s operating profit before deducting interest expenses and income taxes, whereas net income is the profit remaining after all expenses, including interest and taxes, have been subtracted from revenue. This makes EBIT a better indicator of a company’s core operational performance, while net income reflects overall profitability.

To elaborate, EBIT focuses on the earnings generated solely from a company’s operations, providing a clearer picture of how efficiently a company manages its business activities. Net income, on the other hand, gives a more comprehensive view of the company’s financial health by including factors such as debt management (interest expenses) and tax strategies. According to a study by the University of Texas at Austin’s McCombs School of Business, EBIT is favored when assessing operational efficiency because it removes financial and tax-related distortions. For businesses seeking partnerships on income-partners.net, understanding EBIT can help identify companies with strong core operations, making them attractive collaborators for enhancing revenue and market share.

2. Why is EBIT Used as a Measure of Core Profitability?

EBIT is used as a measure of core profitability because it isolates the earnings generated from a company’s primary business operations, excluding the impact of financing decisions and tax policies. This provides a clearer view of how well a company’s management is running the business, independent of how it is financed or the tax environment it operates in.

EBIT’s focus on operational profitability makes it particularly useful for comparing companies with different capital structures (debt vs. equity) or tax situations. For example, a company with high debt might have a lower net income due to interest expenses, but its EBIT would remain strong if its core operations are efficient. According to Harvard Business Review, EBIT is a valuable metric for investors and analysts because it allows for an “apples-to-apples” comparison of companies, regardless of their financial leverage or tax strategies. This is especially important for those looking for strategic partners on income-partners.net, where assessing core operational strength is key to identifying reliable and effective collaborators.

3. How is Net Income Calculated Compared to EBIT?

Net income is calculated by starting with revenue, subtracting the cost of goods sold (COGS) to get gross profit, then subtracting operating expenses to arrive at EBIT. From EBIT, you subtract interest expense and income taxes to finally arrive at net income. EBIT, on the other hand, is calculated before these interest and tax deductions.

The key difference lies in what is included and excluded. Net income takes into account all revenues and expenses, providing a holistic view of the company’s profitability. EBIT strips away the effects of debt and taxes, focusing solely on operational performance. This distinction is important because it allows potential partners to understand different aspects of a company’s financial health. For instance, a company with a high EBIT but low net income might be heavily leveraged, indicating higher financial risk. Understanding these nuances is critical for making informed decisions when seeking partnerships to increase income and revenue through platforms like income-partners.net.

4. What are the Key Components Included in Net Income but Excluded from EBIT?

Net income includes interest expense, income taxes, and non-core business activities, which are excluded from EBIT. Interest expense reflects the cost of borrowing money, income taxes represent the company’s tax obligations, and non-core business activities include gains or losses from activities outside the company’s primary operations, such as investment income or expenses from discontinued operations.

Excluding these components from EBIT offers a focused view of a company’s operating performance. Interest expense and taxes can vary widely depending on a company’s capital structure and tax planning strategies, potentially distorting the true picture of operational efficiency. Non-core business activities can also create volatility in earnings, making it difficult to assess the sustainability of a company’s core business. According to Entrepreneur.com, EBIT is useful for isolating the results of a company’s day-to-day operations, providing a clearer understanding of its ability to generate profits from its main business activities. For those seeking partners to expand their business on income-partners.net, EBIT helps identify companies with robust operational performance, irrespective of their financing or tax strategies.

5. In What Scenarios is EBIT a More Useful Metric Than Net Income?

EBIT is a more useful metric than net income in scenarios where you want to compare the operational performance of companies with different capital structures, tax situations, or significant non-operating activities. It is also beneficial when assessing a company’s ability to generate profits from its core business operations, independent of financing and tax decisions.

For example, if you are evaluating two companies in the same industry but one has significantly more debt than the other, using EBIT allows you to compare their operational efficiency without the distortion of interest expenses. Similarly, if companies have different tax rates or tax strategies, EBIT helps provide a more level playing field for comparison. In situations where non-operating activities heavily influence a company’s net income, EBIT offers a clearer view of its sustainable core profitability. This is particularly important for users of income-partners.net, where identifying companies with strong operational performance is crucial for establishing successful and profitable partnerships.

6. Can You Provide an Example of How EBIT and Net Income Can Differ Significantly?

Consider two companies, Company A and Company B, both generating $1 million in revenue and incurring $600,000 in operating expenses. This results in an EBIT of $400,000 for both companies. However, Company A has $100,000 in interest expense and pays $75,000 in taxes, resulting in a net income of $225,000. Company B, on the other hand, has $20,000 in interest expense and pays $60,000 in taxes, resulting in a net income of $320,000.

In this example, both companies have the same EBIT, indicating similar operational performance. However, their net incomes differ significantly due to variations in interest expenses and tax payments. This highlights how EBIT can provide a more accurate comparison of operational efficiency, unaffected by financing and tax strategies. For users of income-partners.net, focusing on EBIT in such cases can help identify companies with strong core operations, even if their overall profitability (net income) is affected by financial and tax factors.

EBIT vs Net Income Differences

EBIT vs Net Income Differences

7. How Do Interest Expenses Affect Net Income But Not EBIT?

Interest expenses directly reduce net income because they are subtracted from EBIT as part of the net income calculation. EBIT, however, is calculated before interest expenses, making it unaffected by a company’s financing decisions.

The presence of interest expenses in the net income calculation reflects the cost of debt financing. Companies with significant debt will have higher interest expenses, which in turn reduce their net income. EBIT isolates the impact of these financing decisions, providing a clearer picture of how well a company is performing operationally, irrespective of its debt burden. This distinction is valuable for users of income-partners.net who want to assess the true operational strength of potential partners, without the distortion of financing-related factors.

8. What Role Do Taxes Play in the Difference Between EBIT and Net Income?

Taxes play a significant role in the difference between EBIT and net income. EBIT is calculated before taxes, providing a view of earnings before any tax implications. Net income, however, is calculated after deducting taxes, representing the actual profit available to shareholders after all obligations are met.

The impact of taxes on net income can vary depending on a company’s tax planning strategies and the tax laws in its jurisdiction. Companies may use various tax deductions, credits, and strategies to minimize their tax liabilities, which can significantly affect their net income. By focusing on EBIT, analysts and investors can evaluate a company’s operating performance without the distortion of these tax-related factors. For users of income-partners.net, EBIT provides a standardized measure for comparing companies, irrespective of their tax strategies.

9. How Does EBIT Help in Comparing Companies with Different Capital Structures?

EBIT helps in comparing companies with different capital structures by removing the impact of interest expenses, which vary depending on the amount of debt a company uses. This allows for a more accurate comparison of operational efficiency between companies, regardless of how they are financed.

Companies with high debt levels will have higher interest expenses, which reduce their net income but do not affect their EBIT. By focusing on EBIT, analysts can compare companies’ ability to generate profits from their operations, without the distortion of financing-related factors. This is particularly useful when comparing companies in the same industry, where operational efficiency is a key driver of success. For users of income-partners.net, EBIT provides a valuable tool for identifying companies with strong operational performance, regardless of their capital structure.

10. What are Some Limitations of Using EBIT as a Standalone Metric?

While EBIT is useful for assessing core operational profitability, it has limitations as a standalone metric. It does not account for capital expenditures (CapEx), changes in working capital, or other non-cash items that can significantly impact a company’s cash flow. Additionally, EBIT does not reflect the cost of capital or the risk associated with a company’s operations.

Because EBIT excludes CapEx, it may not fully capture the investment required to maintain or grow a company’s operations. Similarly, changes in working capital can significantly impact a company’s cash flow, which is not reflected in EBIT. Non-cash items, such as depreciation and amortization, can also distort the true picture of a company’s financial performance. According to financial experts, it is important to consider other metrics, such as cash flow from operations and free cash flow, in conjunction with EBIT to gain a comprehensive understanding of a company’s financial health. For users of income-partners.net, it is advisable to use EBIT in combination with other financial metrics to make well-informed partnership decisions.

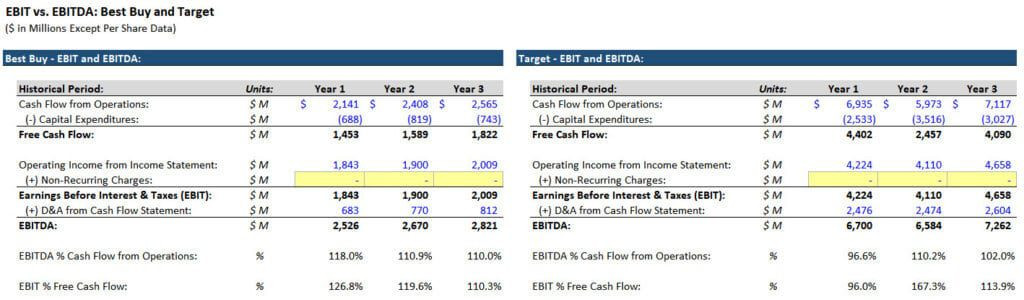

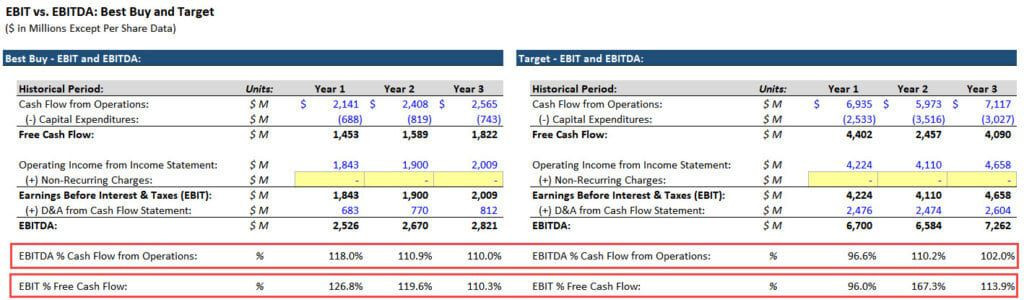

11. Is EBIT a Component of EBITDA?

Yes, EBIT is a component of EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization). EBITDA is calculated by starting with EBIT and adding back depreciation and amortization expenses.

EBITDA provides an even more high-level view of a company’s operational profitability by excluding both financing and accounting-related factors. Depreciation and amortization are non-cash expenses that reflect the reduction in value of a company’s assets over time. Adding these back to EBIT provides a measure of cash flow generated from operations, without considering the impact of capital investments. EBITDA is often used as a proxy for cash flow, particularly in industries with significant capital investments. While useful, EBITDA, like EBIT, has its limitations and should be used in conjunction with other financial metrics for a comprehensive analysis.

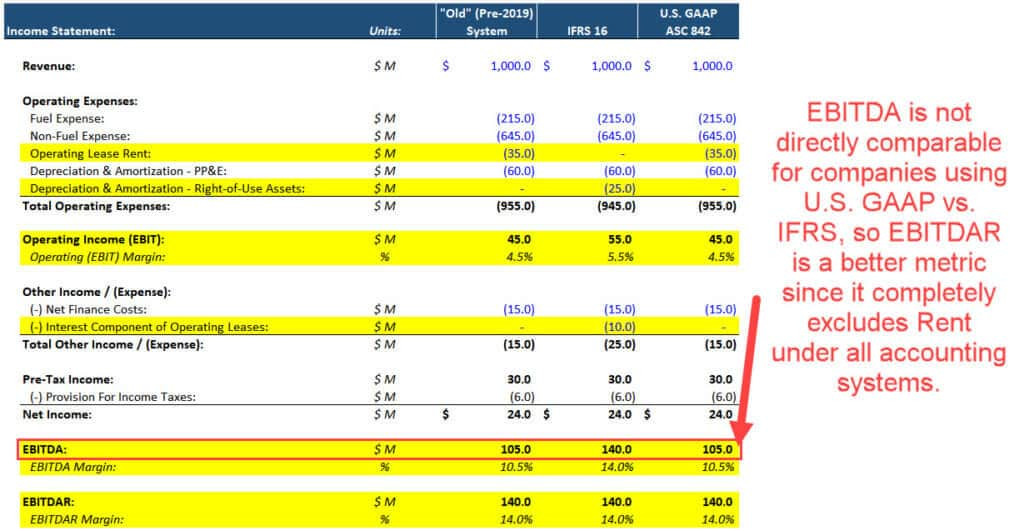

12. How Does Depreciation and Amortization Impact EBIT and EBITDA Differently?

Depreciation and amortization expenses are deducted when calculating EBIT, but they are added back when calculating EBITDA. This means that EBIT reflects the impact of these non-cash expenses on a company’s profitability, while EBITDA does not.

Depreciation and amortization reflect the reduction in value of tangible and intangible assets, respectively. These expenses are recognized over the useful life of the assets and are intended to allocate the cost of the assets to the periods in which they are used. By deducting these expenses, EBIT provides a more conservative view of a company’s profitability. EBITDA, by adding back these expenses, provides a measure of cash flow generated from operations, without considering the impact of these non-cash items.

EBITDA and Lease Accounting

EBITDA and Lease Accounting

13. What is the Significance of Non-Core Business Activities in Net Income?

Non-core business activities can significantly impact net income, but they are excluded from EBIT. These activities include gains or losses from investments, disposal of assets, or discontinued operations, which are not part of a company’s primary business operations.

The inclusion of non-core business activities in net income can create volatility in earnings and make it difficult to assess the sustainability of a company’s core profitability. For example, a company might have a high net income in a particular year due to a one-time gain from the sale of an asset, which is not indicative of its ongoing operational performance. By excluding these activities, EBIT provides a clearer view of a company’s core operational profitability, which is more reliable for assessing its long-term potential.

14. How Can Analyzing Both EBIT and Net Income Provide a More Complete Financial Picture?

Analyzing both EBIT and net income provides a more complete financial picture by offering insights into a company’s operational efficiency and overall profitability. EBIT focuses on core business operations, while net income reflects the impact of financing decisions, tax strategies, and non-core activities.

By comparing EBIT and net income, analysts can gain a deeper understanding of the factors driving a company’s financial performance. A significant difference between the two metrics may indicate that a company’s profitability is heavily influenced by financing or tax strategies, rather than its core operations. This information is valuable for assessing the sustainability and quality of a company’s earnings.

15. What are Common Misconceptions About EBIT and Net Income?

A common misconception is that EBIT and net income are interchangeable measures of profitability. While both metrics provide insights into a company’s financial performance, they focus on different aspects of profitability. EBIT is used to evaluate operational efficiency, while net income reflects overall profitability.

Another misconception is that a higher net income always indicates better financial health. While net income is an important metric, it can be influenced by factors such as debt levels, tax strategies, and non-core activities. A company with a high net income may not necessarily have strong operational performance, and vice versa. Therefore, it is important to consider both EBIT and net income, along with other financial metrics, to gain a complete understanding of a company’s financial health.

16. How Do Changes in Accounting Standards Affect the Calculation of EBIT and Net Income?

Changes in accounting standards can affect the calculation of both EBIT and net income. These changes can impact how revenues and expenses are recognized, which in turn affects the reported profitability of a company.

For example, new standards related to lease accounting or revenue recognition can significantly impact a company’s financial statements. These changes may require companies to recognize assets and liabilities on their balance sheets that were previously off-balance-sheet, or to recognize revenue in a different manner than before. It is important for analysts and investors to stay informed about changes in accounting standards and to understand how these changes can affect the comparability of financial statements over time.

17. What is the Relationship Between EBIT, Net Income, and Free Cash Flow (FCF)?

EBIT, net income, and free cash flow (FCF) are related but distinct metrics that provide different insights into a company’s financial performance. EBIT focuses on operational profitability, net income reflects overall profitability, and FCF measures the cash flow available to a company after accounting for capital expenditures and other investments.

While EBIT and net income are useful for assessing a company’s profitability, they do not necessarily reflect its cash flow. FCF provides a more direct measure of a company’s ability to generate cash, which is essential for funding operations, paying down debt, and returning capital to shareholders. A comprehensive financial analysis should consider all three metrics to gain a complete understanding of a company’s financial health.

18. In What Industries is EBIT More Commonly Used Than Net Income?

EBIT is more commonly used than net income in industries with significant capital investments, such as manufacturing, telecommunications, and energy. In these industries, depreciation and amortization expenses can significantly impact net income, making EBIT a more useful measure of operational profitability.

Additionally, EBIT is often used in industries with complex capital structures, where companies have significant debt levels. By excluding interest expenses, EBIT allows for a more accurate comparison of operational efficiency between companies with different financing strategies. EBIT is also favored in industries where tax strategies can significantly impact net income, such as the technology and pharmaceutical sectors.

EBIT and EBITDA as Cash Flow Proxies

EBIT and EBITDA as Cash Flow Proxies

19. How Can EBIT and Net Income Be Used to Identify Potential Investment Opportunities?

EBIT and net income can be used to identify potential investment opportunities by providing insights into a company’s operational efficiency and overall profitability. Companies with strong EBIT and net income growth may be attractive investment candidates, as they demonstrate the ability to generate sustainable profits from their core operations.

Additionally, comparing EBIT and net income can help identify companies that are undervalued or overvalued by the market. If a company has a strong EBIT but a relatively low net income, it may be undervalued due to factors such as high debt levels or tax strategies. Conversely, a company with a high net income but a weak EBIT may be overvalued, as its profitability may not be sustainable in the long term.

20. What Strategies Can Businesses Employ to Improve Both EBIT and Net Income?

Businesses can employ a variety of strategies to improve both EBIT and net income. To improve EBIT, companies can focus on increasing revenue, reducing operating expenses, and improving operational efficiency. Strategies for increasing revenue include expanding into new markets, developing new products or services, and improving sales and marketing efforts. Cost reduction strategies include streamlining operations, negotiating better terms with suppliers, and reducing waste.

To improve net income, companies can focus on reducing interest expenses, optimizing tax strategies, and improving non-core business activities. Strategies for reducing interest expenses include refinancing debt at lower interest rates and reducing overall debt levels. Tax optimization strategies include taking advantage of tax deductions and credits, and structuring business activities in a tax-efficient manner.

By focusing on these strategies, businesses can improve both their operational efficiency and overall profitability, making them more attractive partners on platforms like income-partners.net.

In conclusion, while EBIT and net income both measure a company’s profitability, they do so from different angles. EBIT provides a focused view of operational efficiency, while net income offers a comprehensive picture of overall profitability. Understanding the nuances of these metrics is crucial for making informed business decisions and identifying strong potential partners.

Are you ready to explore strategic partnerships that can boost your income? Visit income-partners.net today to discover a wide range of opportunities, build valuable relationships, and unlock your business’s full potential. Our platform provides the tools and resources you need to find the perfect collaborators for revenue enhancement, strategic expansion, and long-term success. Don’t wait—start your journey toward greater profitability and growth now! Address: 1 University Station, Austin, TX 78712, United States. Phone: +1 (512) 471-3434. Website: income-partners.net.

FAQ Section: EBIT vs Net Income

1. What does EBIT stand for?

Answer: EBIT stands for Earnings Before Interest and Taxes. It measures a company’s operating profit before deducting interest expenses and income taxes.

2. How is net income calculated?

Answer: Net income is calculated by subtracting all expenses, including interest expenses and income taxes, from revenue.

3. Why is EBIT considered a measure of core profitability?

Answer: EBIT is considered a measure of core profitability because it isolates earnings from primary business operations, excluding the impact of financing decisions and tax policies.

4. What components are included in net income but not in EBIT?

Answer: Net income includes interest expense, income taxes, and non-core business activities, which are excluded from EBIT.

5. In what scenarios is EBIT more useful than net income?

Answer: EBIT is more useful when comparing the operational performance of companies with different capital structures, tax situations, or significant non-operating activities.

6. How do interest expenses affect EBIT and net income?

Answer: Interest expenses reduce net income but do not affect EBIT, as EBIT is calculated before interest expenses.

7. What role do taxes play in the difference between EBIT and net income?

Answer: Taxes are deducted when calculating net income, while EBIT is calculated before taxes, representing earnings before any tax implications.

8. How does EBIT help in comparing companies with different capital structures?

Answer: EBIT helps compare companies with different capital structures by removing the impact of interest expenses, allowing for a more accurate comparison of operational efficiency.

9. What are some limitations of using EBIT as a standalone metric?

Answer: EBIT does not account for capital expenditures, changes in working capital, or other non-cash items that can significantly impact a company’s cash flow.

10. What is the relationship between EBIT, net income, and free cash flow?

Answer: EBIT focuses on operational profitability, net income reflects overall profitability, and free cash flow measures the cash flow available to a company after accounting for capital expenditures and other investments.