Are EBIT and operating income the same thing? Yes, EBIT (Earnings Before Interest and Taxes) is the same as operating income; it’s a critical metric for assessing a company’s core profitability, useful for strategic partnerships and revenue enhancement. At income-partners.net, we help you understand and leverage this key financial indicator to identify potential partners and boost your income. Optimize your financial analysis with a solid understanding of EBIT, also known as operating profit, and its impact on earnings analysis.

1. Understanding EBIT and Operating Income

EBIT, or Earnings Before Interest and Taxes, is indeed the same as Operating Income. It represents a company’s profit from its core business operations before deducting interest expenses and income taxes. Think of EBIT as the financial snapshot of a business’s capacity to generate profit from its primary activities, before accounting for capital structure and tax implications.

1.1. Components of EBIT

To fully grasp EBIT, understanding its components is essential. EBIT is calculated by subtracting operating expenses from gross profit. Here’s a closer look at these components:

- Gross Profit: Revenue less the cost of goods sold (COGS).

- Operating Expenses: Costs incurred from normal business operations, including salaries, rent, marketing, and depreciation.

1.2. Why EBIT Matters

EBIT is a crucial metric for several reasons:

- Performance Evaluation: It allows for a clear comparison of operating profitability between different companies, regardless of their capital structure or tax policies.

- Financial Modeling: EBIT serves as a key input for financial models, especially in discounted cash flow (DCF) analysis, as it is used to derive unlevered free cash flow (UFCF).

- Operational Efficiency: Changes in EBIT can highlight improvements or declines in a company’s operational efficiency.

1.3. Real-World Example

Let’s say Company A and Company B both operate in the same industry but have different capital structures. Company A has significant debt, leading to high-interest expenses, while Company B has minimal debt. By comparing their EBIT, you can assess their operational performance without the distortion of interest expenses. If Company A has a higher EBIT, it indicates that its core business operations are more profitable than Company B’s, despite the interest expenses.

2. How to Calculate EBIT

There are several methods to calculate EBIT, depending on the information available:

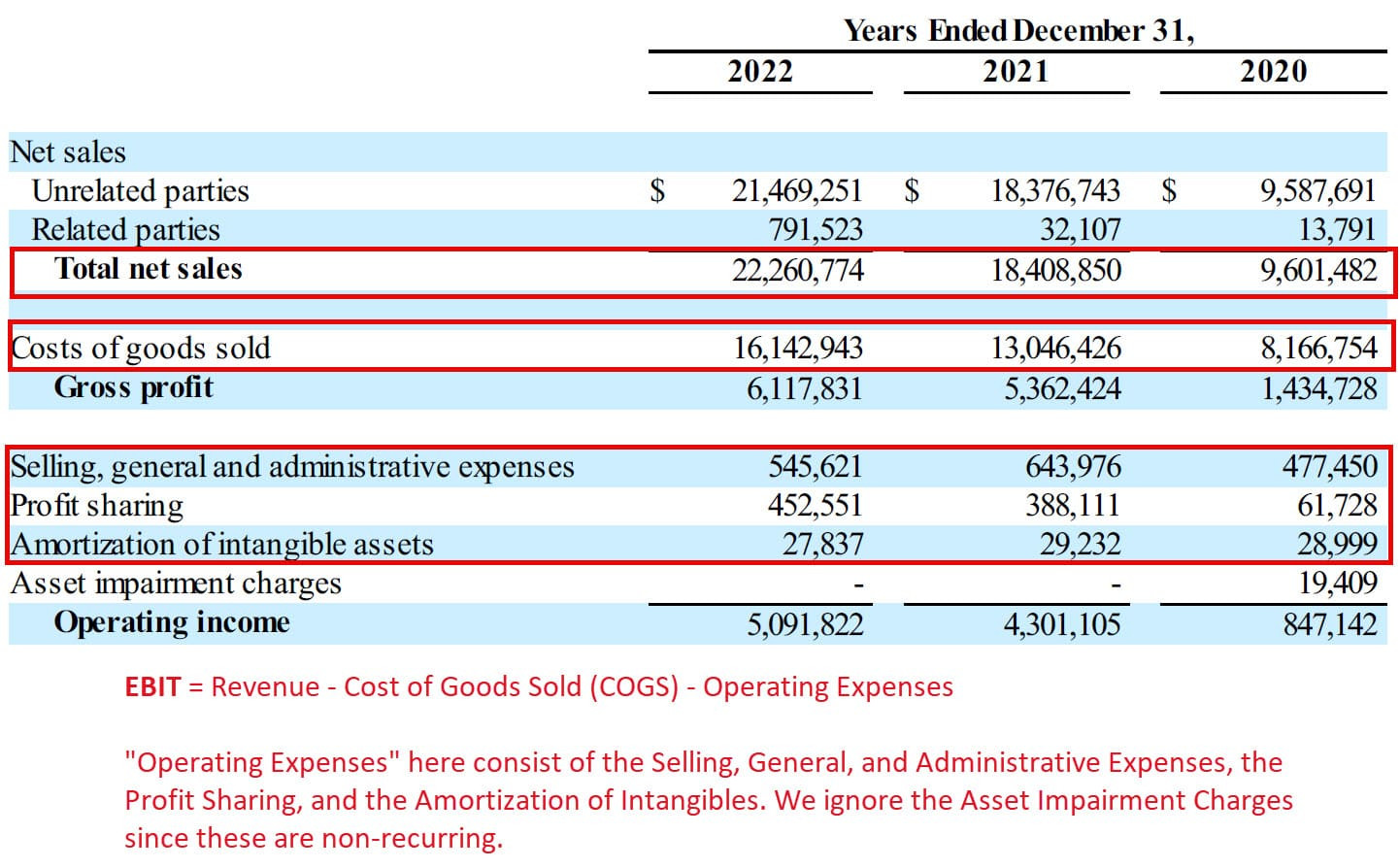

2.1. Method 1: Revenue – COGS – Operating Expenses

This is the most straightforward method, where you subtract the cost of goods sold (COGS) and all operating expenses from the total revenue.

Formula:

EBIT = Revenue - COGS - Operating Expenses

Example:

Suppose a company has revenue of $1,000,000, COGS of $400,000, and operating expenses of $200,000.

EBIT = $1,000,000 - $400,000 - $200,000 = $400,000

2.2. Method 2: Gross Profit – Operating Expenses

This method starts with the gross profit, which is revenue minus COGS, and then subtracts operating expenses.

Formula:

EBIT = Gross Profit - Operating Expenses

Example:

Using the same values from the previous example, where revenue is $1,000,000 and COGS is $400,000, the gross profit is $600,000. With operating expenses of $200,000.

EBIT = $600,000 - $200,000 = $400,000

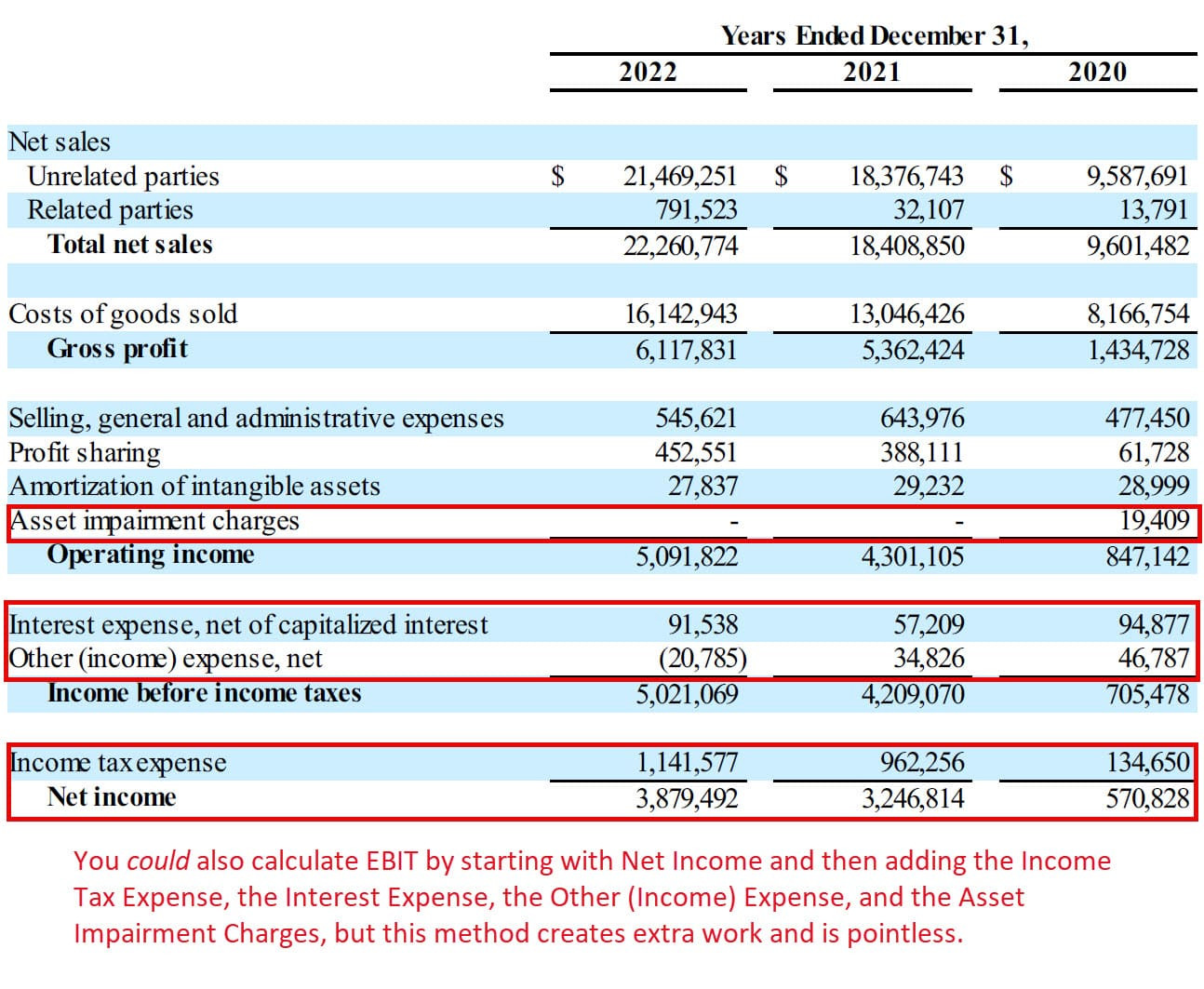

2.3. Method 3: Net Income + Interest + Taxes

While less common, you can also derive EBIT from net income by adding back interest expenses and income taxes.

Formula:

EBIT = Net Income + Interest Expense + Income Taxes

Example:

If a company has a net income of $200,000, interest expense of $50,000, and income taxes of $150,000.

EBIT = $200,000 + $50,000 + $150,000 = $400,000

2.4. Comprehensive Example Table

| Item | Amount |

|---|---|

| Revenue | $1,000,000 |

| COGS | $400,000 |

| Gross Profit | $600,000 |

| Operating Expenses | $200,000 |

| Net Income | $200,000 |

| Interest Expense | $50,000 |

| Income Taxes | $150,000 |

| EBIT | $400,000 |

3. EBIT vs. EBITDA: What’s the Difference?

EBITDA, or Earnings Before Interest, Taxes, Depreciation, and Amortization, is another profitability metric that is often compared to EBIT. While EBIT excludes interest and taxes, EBITDA goes a step further by excluding depreciation and amortization.

3.1. Understanding EBITDA

EBITDA is used to assess a company’s operating performance without the impact of non-cash expenses (depreciation and amortization), as well as capital structure and taxes. It provides a clearer picture of a company’s cash-generating ability from its operations.

3.2. Key Differences

- Depreciation and Amortization: EBIT includes depreciation and amortization as operating expenses, while EBITDA excludes them.

- Focus: EBIT focuses on operating profitability, while EBITDA focuses on cash flow generation.

- Use Cases: EBIT is often used in financial modeling and valuation, while EBITDA is frequently used in leveraged buyout (LBO) analysis and assessing debt repayment capacity.

3.3. Calculation Example

Consider a company with the following financials:

- Net Sales: $5,000,000

- Cost of Goods Sold: $2,000,000

- Operating Expenses: $1,500,000

- Depreciation & Amortization: $500,000

- Interest Expense: $200,000

- Taxes: $300,000

EBIT Calculation:

- Gross Profit: $5,000,000 – $2,000,000 = $3,000,000

- EBIT: $3,000,000 – $1,500,000 = $1,500,000

EBITDA Calculation:

- EBITDA: $1,500,000 + $500,000 = $2,000,000

3.4. When to Use Each Metric

- EBIT: Use when assessing operating profitability and comparing companies with different capital structures.

- EBITDA: Use when evaluating cash flow generation and comparing companies with different levels of fixed assets.

3.5. Comparative Analysis Table

| Metric | Includes | Excludes | Focus | Use Cases |

|---|---|---|---|---|

| EBIT | Operating Profit, Depreciation & Amortization | Interest, Taxes | Operating Profitability | Financial Modeling, Valuation |

| EBITDA | Operating Profit | Interest, Taxes, Depreciation & Amortization | Cash Flow Generation | LBO Analysis, Debt Repayment Capacity |

4. The Significance of EBIT Margin

The EBIT margin, also known as the operating margin, is a profitability ratio that measures a company’s operating profit as a percentage of its revenue. It is a key indicator of how well a company manages its costs and generates profit from its core operations.

4.1. Understanding EBIT Margin

The EBIT margin is calculated by dividing EBIT by total revenue. It shows the percentage of revenue that remains after deducting operating expenses, but before accounting for interest and taxes.

4.2. Formula for EBIT Margin

EBIT Margin = (EBIT / Total Revenue) * 100

4.3. Interpreting EBIT Margin

A higher EBIT margin indicates that the company is more efficient in controlling its operating expenses and generating profit from sales. Conversely, a lower EBIT margin may suggest inefficiencies in operations or higher costs.

4.4. Benchmarking EBIT Margin

The ideal EBIT margin varies by industry. For example, software companies may have higher EBIT margins due to lower operating costs, while manufacturing companies may have lower margins due to higher production costs. Therefore, it is essential to benchmark a company’s EBIT margin against its industry peers.

4.5. Example Calculation

Consider a company with an EBIT of $500,000 and total revenue of $2,000,000.

EBIT Margin = ($500,000 / $2,000,000) * 100 = 25%

This means that for every dollar of revenue, the company earns 25 cents in operating profit.

4.6. Industry Comparison

According to a study by the University of Texas at Austin’s McCombs School of Business in July 2023, the average EBIT margin for the software industry is around 30%, while the manufacturing industry averages around 10%. A company with a 25% EBIT margin in the software industry may be underperforming compared to its peers, while a company with a 12% EBIT margin in the manufacturing industry may be performing well.

4.7. Factors Affecting EBIT Margin

Several factors can influence a company’s EBIT margin:

- Pricing Strategy: Higher prices can increase revenue and improve the EBIT margin, provided sales volume is maintained.

- Cost Management: Efficient cost control can reduce operating expenses and boost the EBIT margin.

- Operational Efficiency: Streamlined operations and improved productivity can lower costs and increase profitability.

- Industry Dynamics: Competitive pressures and market conditions can impact pricing and costs, affecting the EBIT margin.

4.8. How to Improve EBIT Margin

- Increase Revenue: Focus on increasing sales volume and pricing strategies.

- Reduce Costs: Implement cost-cutting measures and improve operational efficiency.

- Optimize Pricing: Adjust pricing strategies to maximize revenue and profitability.

- Enhance Efficiency: Streamline operations and improve productivity to lower costs.

4.9. EBIT Margin Analysis Table

| Category | Description | Impact on EBIT Margin |

|---|---|---|

| Revenue | Increase in sales volume or pricing | Positive |

| Cost of Goods Sold | Reduction in production costs | Positive |

| Operating Expenses | Reduction in administrative, sales, and marketing expenses | Positive |

| Operational Efficiency | Streamlined processes and improved productivity | Positive |

| Industry Dynamics | Competitive pressures and market conditions affecting pricing and costs | Can be positive or negative depending on the specific conditions |

5. EBIT in Financial Modeling and Valuation

EBIT is a fundamental component in financial modeling and valuation, serving as a key input in various analyses. Its role in projecting future performance and determining a company’s intrinsic value is crucial for investors and analysts.

5.1. EBIT as a Starting Point

In financial modeling, EBIT often serves as the starting point for forecasting future profitability. Analysts project revenue growth and operating expenses to arrive at future EBIT figures. These projections are then used in discounted cash flow (DCF) models and other valuation techniques.

5.2. Discounted Cash Flow (DCF) Models

EBIT is used to calculate Net Operating Profit After Taxes (NOPAT), which is a key component of Unlevered Free Cash Flow (UFCF). UFCF is then discounted back to its present value to determine the company’s enterprise value.

5.3. Valuation Multiples

EBIT is also used in valuation multiples, such as Enterprise Value (EV) to EBIT. This multiple helps investors assess how much they are paying for a company’s operating profit. By comparing this multiple to industry peers, investors can determine if a company is overvalued or undervalued.

5.4. Sensitivity Analysis

Analysts perform sensitivity analysis on EBIT projections to understand how changes in key assumptions, such as revenue growth and operating margins, impact the company’s valuation. This helps in assessing the robustness of the valuation and identifying potential risks and opportunities.

5.5. Example Scenario

Suppose an analyst is building a DCF model for a company. The analyst projects the following EBIT for the next five years:

| Year | EBIT Projection |

|---|---|

| 1 | $600,000 |

| 2 | $700,000 |

| 3 | $800,000 |

| 4 | $900,000 |

| 5 | $1,000,000 |

Using these EBIT projections, the analyst calculates NOPAT and UFCF, which are then used to determine the company’s enterprise value.

5.6. Impact of Assumptions

The accuracy of EBIT projections depends heavily on the assumptions made about revenue growth and operating expenses. If the analyst is overly optimistic about revenue growth, the EBIT projections may be too high, leading to an overvaluation of the company.

5.7. Valuation Table

| Metric | Year 1 | Year 2 | Year 3 | Year 4 | Year 5 |

|---|---|---|---|---|---|

| EBIT | $600,000 | $700,000 | $800,000 | $900,000 | $1,000,000 |

| Tax Rate | 25% | 25% | 25% | 25% | 25% |

| NOPAT | $450,000 | $525,000 | $600,000 | $675,000 | $750,000 |

| Capital Expenditures | $100,000 | $110,000 | $120,000 | $130,000 | $140,000 |

| Depreciation & Amortization | $80,000 | $90,000 | $100,000 | $110,000 | $120,000 |

| Unlevered Free Cash Flow | $430,000 | $505,000 | $580,000 | $655,000 | $730,000 |

6. Industry-Specific Considerations for EBIT

Different industries have unique operational and financial characteristics that can significantly impact EBIT. Understanding these industry-specific nuances is crucial for accurate financial analysis and valuation.

6.1. Technology Industry

The technology industry often boasts high EBIT margins due to its scalable business models and relatively low cost of goods sold. Companies like software developers and cloud service providers typically have high operating leverage, meaning that incremental sales generate significant profits.

6.2. Manufacturing Industry

In contrast, the manufacturing industry tends to have lower EBIT margins. These companies incur substantial costs related to raw materials, labor, and production facilities. Operational efficiency and cost management are critical for manufacturers to maintain healthy EBIT margins.

6.3. Retail Industry

The retail industry is characterized by high competition and fluctuating consumer demand. Retailers must carefully manage inventory, pricing, and promotional activities to drive sales and control costs. EBIT margins in the retail sector can vary widely depending on factors such as brand strength, store location, and online presence.

6.4. Healthcare Industry

The healthcare industry faces unique challenges related to regulatory compliance, reimbursement rates, and technological advancements. Healthcare providers and pharmaceutical companies must invest heavily in research and development, clinical trials, and marketing. EBIT margins in the healthcare sector can be influenced by factors such as patent protection, drug pricing, and government policies.

6.5. Financial Services Industry

The financial services industry is subject to strict regulatory oversight and market volatility. Banks, insurance companies, and investment firms must manage risk effectively and comply with capital requirements. EBIT margins in the financial services sector can be impacted by factors such as interest rates, credit spreads, and asset quality.

6.6. Industry Comparison Table

| Industry | Typical EBIT Margin | Key Factors Affecting EBIT |

|---|---|---|

| Technology | 20% – 40% | Scalability, operating leverage |

| Manufacturing | 5% – 15% | Cost of goods sold, operational efficiency |

| Retail | 3% – 10% | Inventory management, pricing |

| Healthcare | 10% – 25% | Regulatory compliance, research and development |

| Financial Services | 15% – 30% | Risk management, regulatory oversight |

7. Common Pitfalls in EBIT Analysis

While EBIT is a useful metric, it is essential to be aware of common pitfalls that can lead to inaccurate analysis.

7.1. Ignoring Non-Operating Items

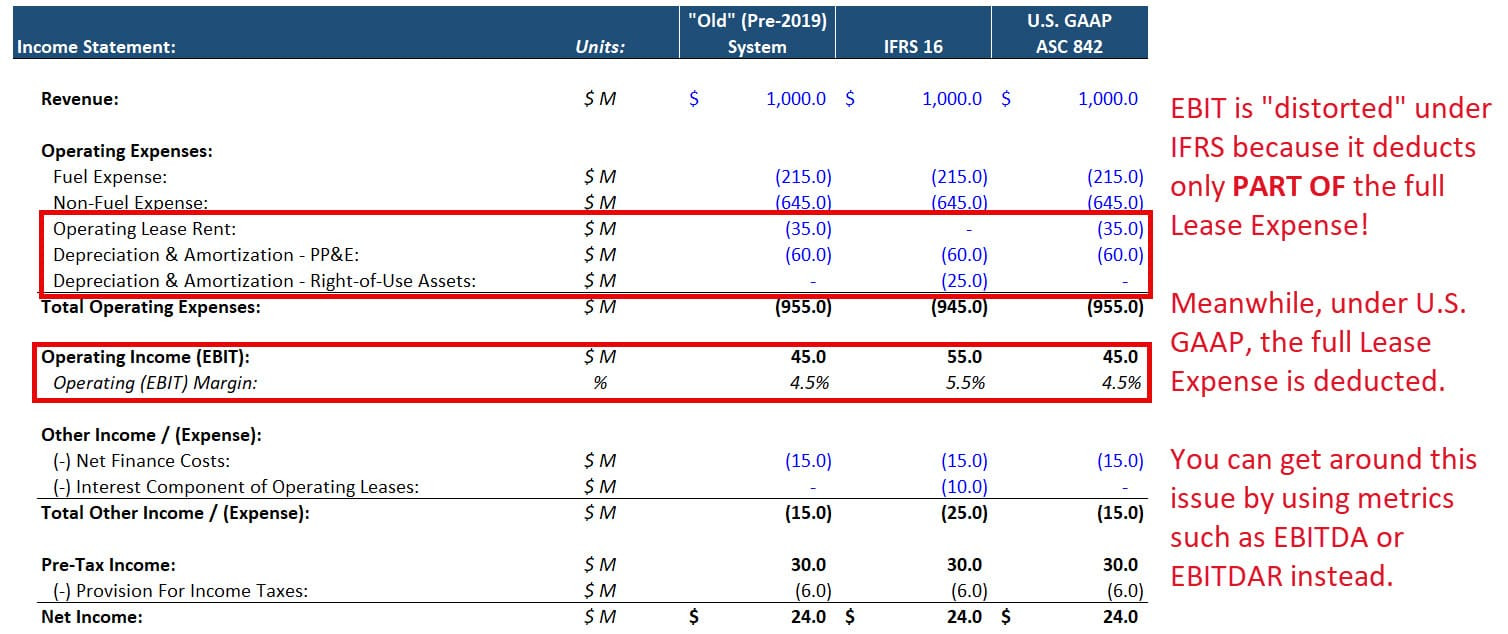

EBIT focuses on operating income but may overlook significant non-operating items such as gains or losses from investments, restructuring charges, or asset impairments. These items can distort the true picture of a company’s profitability and should be analyzed separately.

7.2. Neglecting Capital Structure

EBIT excludes interest expenses, which means it does not reflect the impact of a company’s capital structure on its profitability. Companies with high levels of debt may have lower net income due to interest expenses, even if their operating performance is strong.

7.3. Overlooking Industry Differences

EBIT margins can vary widely across industries, so it is essential to benchmark a company’s performance against its industry peers. Comparing a company’s EBIT margin to the average for its industry can provide valuable insights into its competitive position.

7.4. Failing to Consider Non-Cash Expenses

EBIT includes non-cash expenses such as depreciation and amortization, which can affect a company’s reported profitability. While these expenses are legitimate costs of doing business, they do not represent actual cash outflows.

7.5. Using EBIT in Isolation

EBIT should not be used in isolation but rather in conjunction with other financial metrics such as revenue growth, net income, and cash flow. A comprehensive analysis of a company’s financial performance requires a holistic approach.

7.6. Pitfalls Analysis Table

| Pitfall | Description | Impact on Analysis |

|---|---|---|

| Ignoring Non-Operating Items | Overlooking gains or losses from investments, restructuring charges, etc. | Distorted view of profitability |

| Neglecting Capital Structure | Failing to consider the impact of debt on profitability | Incomplete assessment of financial health |

| Overlooking Industry Differences | Not benchmarking against industry peers | Misleading comparisons and conclusions |

| Failing to Consider Non-Cash Expenses | Not accounting for the impact of depreciation and amortization | Inaccurate assessment of cash flow generation |

| Using EBIT in Isolation | Not considering other financial metrics such as revenue growth and net income | Limited understanding of overall financial performance |

8. Enhancing Revenue Through Strategic Partnerships

Strategic partnerships can be a powerful mechanism for enhancing revenue and driving EBIT growth. By aligning with complementary businesses, companies can expand their market reach, access new technologies, and improve their competitive positioning.

8.1. Types of Strategic Partnerships

- Joint Ventures: Two or more companies create a new entity to pursue a specific business opportunity.

- Licensing Agreements: One company grants another the right to use its intellectual property, such as patents, trademarks, or copyrights.

- Distribution Agreements: One company agrees to distribute another company’s products or services.

- Co-Marketing Agreements: Two or more companies collaborate on marketing campaigns to promote their respective products or services.

8.2. Benefits of Strategic Partnerships

- Increased Revenue: Partnerships can open up new markets and customer segments, leading to higher sales.

- Reduced Costs: Sharing resources and expenses with partners can lower operating costs and improve profitability.

- Enhanced Innovation: Collaborating with other companies can foster innovation and lead to the development of new products and services.

- Improved Competitive Positioning: Partnerships can strengthen a company’s competitive advantage by combining complementary strengths.

8.3. Building Successful Partnerships

- Identify Complementary Partners: Look for companies that offer products, services, or technologies that complement your own.

- Establish Clear Goals and Objectives: Define the goals and objectives of the partnership upfront to ensure alignment and focus.

- Develop a Detailed Agreement: Create a comprehensive partnership agreement that outlines the roles, responsibilities, and financial terms of the arrangement.

- Foster Open Communication: Maintain open and transparent communication with your partners to build trust and resolve issues effectively.

8.4. Strategic Partnerships Examples

- Technology: A software company partners with a hardware manufacturer to offer integrated solutions.

- Retail: A retailer partners with a logistics provider to improve supply chain efficiency.

- Healthcare: A pharmaceutical company partners with a research institution to develop new drugs.

8.5. Partnership Strategies Table

| Strategy | Description | Potential Benefits |

|---|---|---|

| Market Expansion | Partnering to enter new geographic markets | Increased revenue, expanded customer base |

| Product Development | Collaborating on new product development | Enhanced innovation, competitive advantage |

| Cost Reduction | Sharing resources and expenses with partners | Lower operating costs, improved profitability |

| Technology Integration | Integrating complementary technologies | Enhanced product offerings, improved customer experience |

9. Maximizing Income With Strategic Partnerships at Income-Partners.Net

At income-partners.net, we provide the resources and expertise you need to identify, evaluate, and build successful strategic partnerships. Our platform offers a comprehensive directory of potential partners, as well as tools and resources to help you structure and manage your partnerships effectively.

9.1. Identifying Potential Partners

Our platform allows you to search for potential partners based on industry, size, location, and other criteria. You can also view detailed profiles of potential partners, including their financial performance, product offerings, and strategic goals.

9.2. Evaluating Partnership Opportunities

We provide tools to help you evaluate potential partnership opportunities, including financial analysis templates, due diligence checklists, and legal resources. Our experts can also provide customized advice and support to help you make informed decisions.

9.3. Structuring Partnership Agreements

We offer a variety of partnership agreement templates that you can customize to fit your specific needs. Our legal experts can also review your partnership agreements to ensure that they are legally sound and protect your interests.

9.4. Managing Partnership Relationships

We provide tools to help you manage your partnership relationships effectively, including project management software, communication platforms, and performance tracking dashboards. Our experts can also provide ongoing support and guidance to help you build and maintain strong partnerships.

9.5. Success Stories

Many of our clients have successfully used our platform to identify and build strategic partnerships that have significantly increased their revenue and profitability. For example, one of our clients, a small software company, partnered with a larger hardware manufacturer and increased their sales by 50% in the first year of the partnership.

9.6. Success Table

| Client | Industry | Partnership Type | Results |

|---|---|---|---|

| Small Software Company | Software | Hardware Integration | 50% increase in sales in the first year |

| Mid-Sized Manufacturer | Manufacturing | Distribution Agreement | 30% increase in market reach |

| Large Retailer | Retail | Logistics Partnership | 20% reduction in supply chain costs |

Unlock your business’s potential by exploring strategic alliances and maximizing income streams. Join income-partners.net today and discover the transformative power of collaboration.

10. Frequently Asked Questions (FAQs) About EBIT and Operating Income

10.1. Is EBIT the Same as Net Income?

No, EBIT (Earnings Before Interest and Taxes) is not the same as net income. EBIT represents a company’s profit from its core business operations before deducting interest expenses and income taxes, while net income is the profit after all expenses, including interest and taxes, have been deducted.

10.2. Why Is EBIT Important?

EBIT is important because it provides a clear picture of a company’s operating profitability, allowing for comparisons between companies with different capital structures and tax policies. It is also a key input in financial modeling and valuation.

10.3. How Is EBIT Used in Valuation?

EBIT is used in valuation as a starting point for calculating Net Operating Profit After Taxes (NOPAT) and Unlevered Free Cash Flow (UFCF), which are used in discounted cash flow (DCF) models. It is also used in valuation multiples, such as Enterprise Value (EV) to EBIT.

10.4. What Is a Good EBIT Margin?

A good EBIT margin varies by industry. Generally, a higher EBIT margin indicates greater efficiency in controlling operating expenses and generating profit from sales.

10.5. What Are the Limitations of EBIT?

Limitations of EBIT include ignoring non-operating items, neglecting capital structure, overlooking industry differences, failing to consider non-cash expenses, and using EBIT in isolation.

10.6. How Can Strategic Partnerships Increase EBIT?

Strategic partnerships can increase EBIT by expanding market reach, accessing new technologies, reducing costs, and improving competitive positioning.

10.7. How Does Income-Partners.Net Help with Strategic Partnerships?

Income-partners.net helps with strategic partnerships by providing a comprehensive directory of potential partners, tools to evaluate partnership opportunities, partnership agreement templates, and resources to manage partnership relationships effectively.

10.8. What Is the Difference Between EBIT and EBITDA?

EBIT (Earnings Before Interest and Taxes) includes depreciation and amortization, while EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) excludes these non-cash expenses.

10.9. Can EBIT Be Negative?

Yes, EBIT can be negative if a company’s operating expenses exceed its gross profit. This indicates that the company is losing money from its core business operations.

10.10. How Do I Calculate EBIT?

You can calculate EBIT using one of the following formulas:

- EBIT = Revenue – COGS – Operating Expenses

- EBIT = Gross Profit – Operating Expenses

- EBIT = Net Income + Interest Expense + Income Taxes

Ready to discover new pathways to revenue generation and strategic alliances? Visit income-partners.net to connect with potential partners and elevate your business performance.

Business Networking Events

Business Networking Events

Effective marketing campaigns

Effective marketing campaigns

Net Income – Earnings

Net Income – Earnings

EBIT – Leases

EBIT – Leases