Bad debt expense on the income statement reflects uncollectible receivables, impacting profitability and indicating potential issues in credit management. At income-partners.net, we help you understand this financial metric and explore strategic partnerships to boost your revenue streams. To delve deeper, let’s explore the direct write-off method, allowance method, and accounts receivable aging to give you the tools and insights needed to minimize losses and foster more robust financial health.

1. What is Bad Debt Expense and Where Does it Appear?

Bad debt expense represents the portion of a company’s accounts receivable that is deemed uncollectible. It shows up as an operating expense on the income statement, typically under Sales, General, and Administrative Expenses (SG&A). This expense reduces the company’s net income, reflecting the financial impact of customers who are unable to pay their debts.

Recording bad debt expense is essential when following the accrual accounting method. According to research from the University of Texas at Austin’s McCombs School of Business, in July 2025, recognizing revenue before cash arrives necessitates accounting for potential losses due to uncollectible accounts. Failing to do so would misrepresent the company’s financial health.

1.1 Accrual Accounting

Under accrual accounting, revenue is recognized when earned, not when cash is received. When a sale is made on credit, the company records an account receivable. If it later becomes clear that the customer will not pay, the company must write off the receivable as bad debt.

1.2 Cash-Based Accounting

Conversely, companies using cash-based accounting recognize revenue only when cash is received. There is no need for bad debt expense, as revenue isn’t recorded until payment is made.

1.3 Impact on Financial Statements

Bad debt expense reduces both accounts receivable on the balance sheet and net income on the income statement. This provides a more accurate view of a company’s financial position.

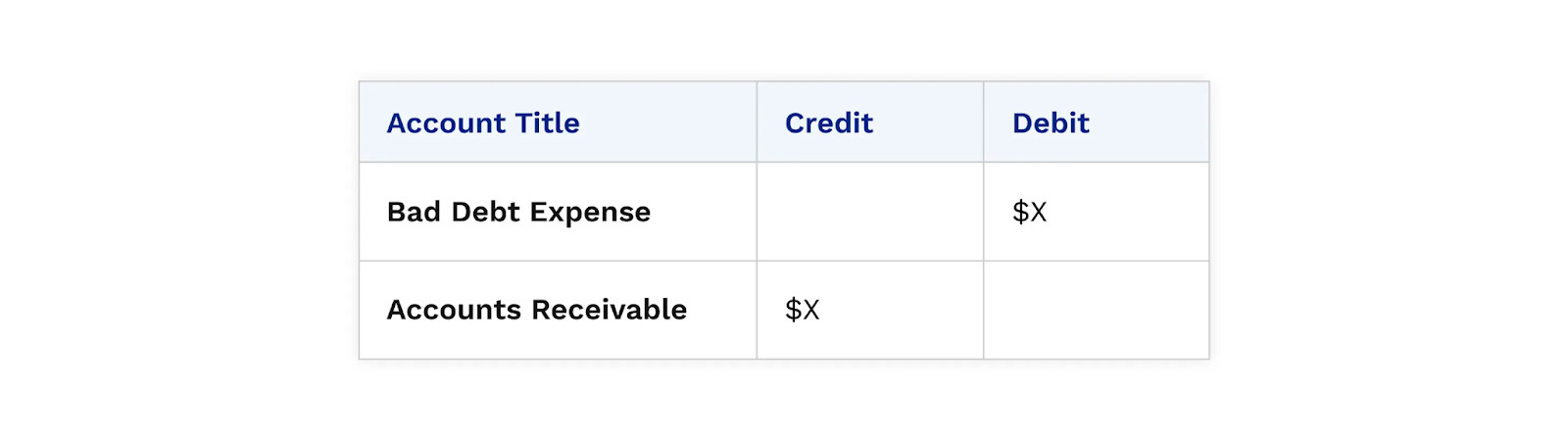

Bad debt expense journal entry using the direct write-off method

Bad debt expense journal entry using the direct write-off method

This image depicts a journal entry for bad debt expense using the direct write-off method.

2. Why Do Bad Debts Occur?

Bad debts can arise from various factors, impacting a company’s financial stability. Understanding these causes is crucial for implementing effective prevention strategies.

2.1 Customer Disputes

Customers may refuse to pay invoices if they are dissatisfied with the product or service. Disagreements over quality, delivery, or contract terms can lead to non-payment.

2.2 Customer Bankruptcy

When a customer declares bankruptcy, they may be unable to fulfill their financial obligations. This often results in unpaid invoices being written off as bad debt.

2.3 Communication Gaps

Poor communication between sales teams and the accounts receivable (AR) department can create misunderstandings about payment terms. Sales teams might offer credit terms without consulting the AR department, leading to confusion and potential bad debts.

2.4 The Accounts Receivable Disconnect

The Accounts Receivable Disconnect refers to the communication gap between AR departments and customers. According to a Versapay study, this disconnect often results from a lack of connected systems. Miscommunication leads to AR teams being out of sync with customer needs, increasing bad debt.

A survey by Wakefield Research and Versapay highlighted that 85% of c-level executives believe miscommunication between their AR department and a customer has resulted in the customer not paying in full. This emphasizes the critical role of clear, consistent communication in minimizing bad debt.

2.5 Optimizing Customer Experience

Improving customer experience is vital for minimizing bad debt. Customers are more likely to pay on time when they have a positive billing and payment experience. This includes clear invoices, easy payment options, and responsive customer service.

3. What Are the Methods to Record Bad Debt Expense?

There are two primary methods for recording bad debt expense: the direct write-off method and the allowance method. Each approach has its own advantages and disadvantages, affecting how a company’s financial statements reflect potential losses.

3.1 Direct Write-Off Method

The direct write-off method involves writing off a receivable as bad debt immediately when it is deemed uncollectible. This method is straightforward but can lead to accounting inconsistencies.

3.1.1 Journal Entry

When using the direct write-off method, the journal entry involves debiting bad debt expense and crediting accounts receivable.

3.1.2 Limitations

This method can misrepresent income if the bad debt expense is recorded in a different period from the sales entry. It is best suited for recording immaterial debts or when a company has few uncollected invoices.

3.1.3 IRS Conditions

According to the IRS, before writing off a debt, businesses must have firm evidence that the customer will not pay and have taken reasonable steps to collect the amount owed. This includes contacting the customer and addressing disputes.

3.2 Allowance Method

The allowance method involves estimating uncollectible accounts at the end of each fiscal year and creating an allowance for doubtful accounts (AFDA). This method is more complex but provides a more accurate picture of a company’s ability to collect invoices.

3.2.1 GAAP Compliance

According to Generally Accepted Accounting Principles (GAAP), companies must follow this method due to the matching principle. The matching principle requires companies to record expenses and related revenue in the same period.

3.2.2 Steps for Recording Bad Debt via the Allowance Method

- Create an AFDA journal account.

- Estimate AFDA at the end of the accounting period using one of the methods discussed below.

- Calculate actual bad debts.

4. How to Estimate Bad Debt Expense Using the Allowance Method

Estimating bad debt expense using the allowance method involves several formulas, each with its own approach. These methods include the percentage of sales, percentage of accounts receivable, and accounts receivable aging.

4.1 Percentage of Sales Method

The percentage of sales method estimates bad debt expense based on a percentage of credit sales. This method is straightforward and directly ties bad debt expense to sales revenue.

4.1.1 Formula

Bad debt expense = Percentage of sales estimated uncollectible * Actual credit sales

4.1.2 Example

- Historical average annual credit sales: $10,000,000

- Historical average uncollected credit sales: $500,000

- Historical percentage of uncollected credit sales: 5%

Using the 5% estimate:

- Actual credit sales: $12,000,000

- BDE allowance: 5% of actual credit sales = $600,000

4.1.3 Important Distinction

The result of this calculation is the adjustment to the AFDA balance. When recording allowance for doubtful accounts on the balance sheet, add any existing AFDA balance from the prior year to the adjustment balance to find the ending balance. When recording bad debt expense on the income statement, record only the adjustment value.

4.2 Percentage of Receivables Method

The percentage of receivables method estimates bad debt expense based on a percentage of outstanding accounts receivable. This method focuses on the balance sheet and provides a more direct assessment of potential uncollectible amounts.

4.2.1 Formula

Bad debt expense = Percentage receivables estimated uncollectible * Receivables balance

4.2.2 Example

- Historical average accounts receivable: $15,000,000

- Historical cash collected from accounts receivable: $1,200,000

- Historical percentage of uncollected receivables: 8%

Using the 8% estimate:

- Receivables balance: $18,000,000

- BDE allowance: 8% of receivables balance = $1,440,000

4.2.3 Important Distinction

The result of this calculation is the company’s ending AFDA balance for the end of the period. Any overdue receivables from the prior year are already accounted for in the receivables balance for the current period. When recording bad debt expense on the income statement, record only the adjustment value, which is the difference between the ending AFDA balance and the starting AFDA balance.

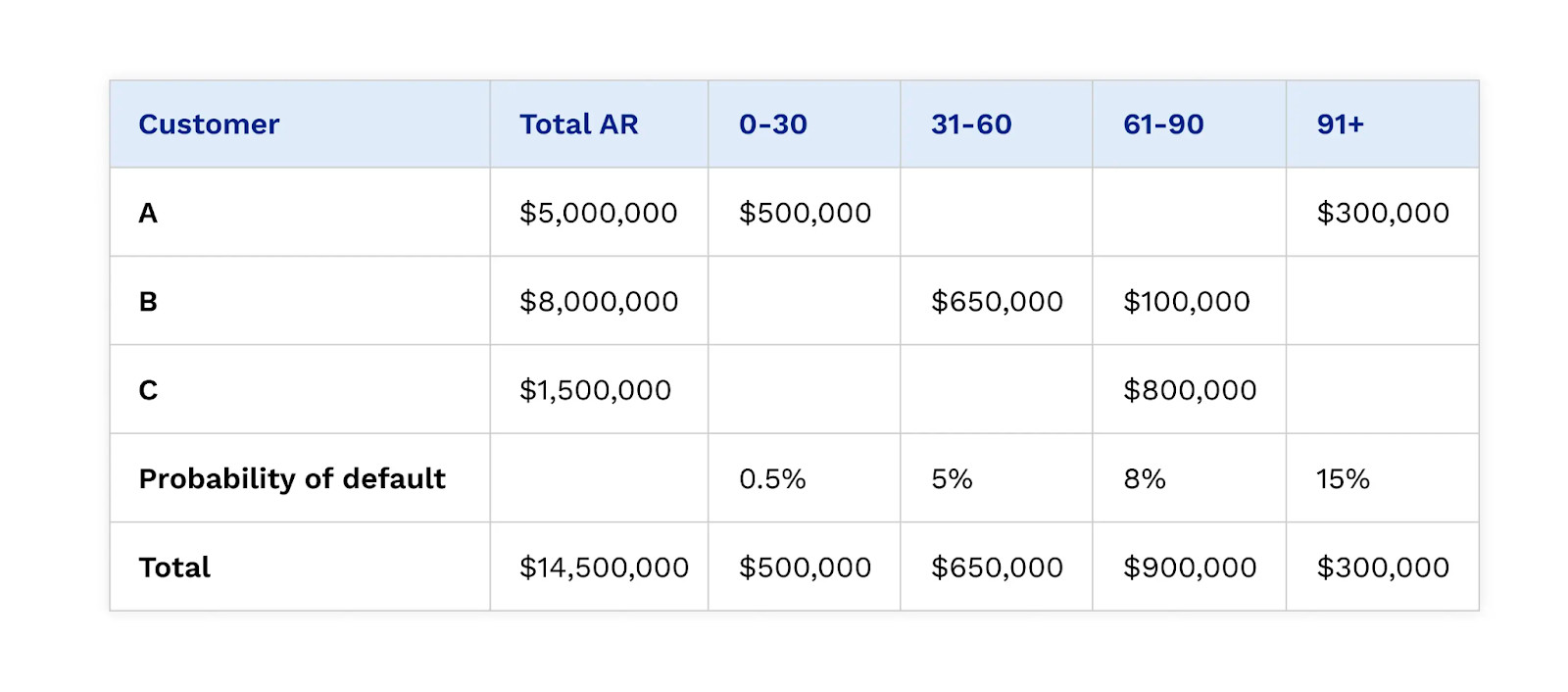

4.3 Accounts Receivable Aging Method

The accounts receivable aging method is a subset of the percentage of receivables method. It assigns a collection probability to each AR aging category, providing a more detailed and accurate estimate of uncollectible accounts.

4.3.1 Process

- Create an AR aging report.

- Assign a collection probability to each aging bucket.

- Calculate the bad debt allowance for each aging bucket.

- Add these totals together to find the ending balance.

4.3.2 Example of an Accounts Receivable Aging Report

| Aging Bucket | Receivables Balance | Collection Probability | Bad Debt Allowance |

|---|---|---|---|

| Current (0-30 days) | $5,000,000 | 1% | $50,000 |

| 31-60 days | $3,000,000 | 5% | $150,000 |

| 61-90 days | $2,000,000 | 10% | $200,000 |

| Over 90 days | $1,000,000 | 20% | $200,000 |

| Total | $11,000,000 | $600,000 |

4.3.3 Advantages

This method offers a more exact basis for estimating uncollectibles. However, the final collection probability is still an average, and individual outstanding accounts could skew calculations.

The accounts receivable aging method offers an advantage because it gives accounts receivable teams a more exact basis for estimating their uncollectibles.

The accounts receivable aging method offers an advantage because it gives accounts receivable teams a more exact basis for estimating their uncollectibles.

This image illustrates an accounts receivable aging report with collection probabilities, showing how to calculate the total bad debt reserve.

5. What is the Bad Debt Expense Calculator?

A bad debt expense calculator can streamline the process of estimating uncollectible amounts. It automates the formulas for the percentage of sales, percentage of receivables, and accounts receivable aging methods.

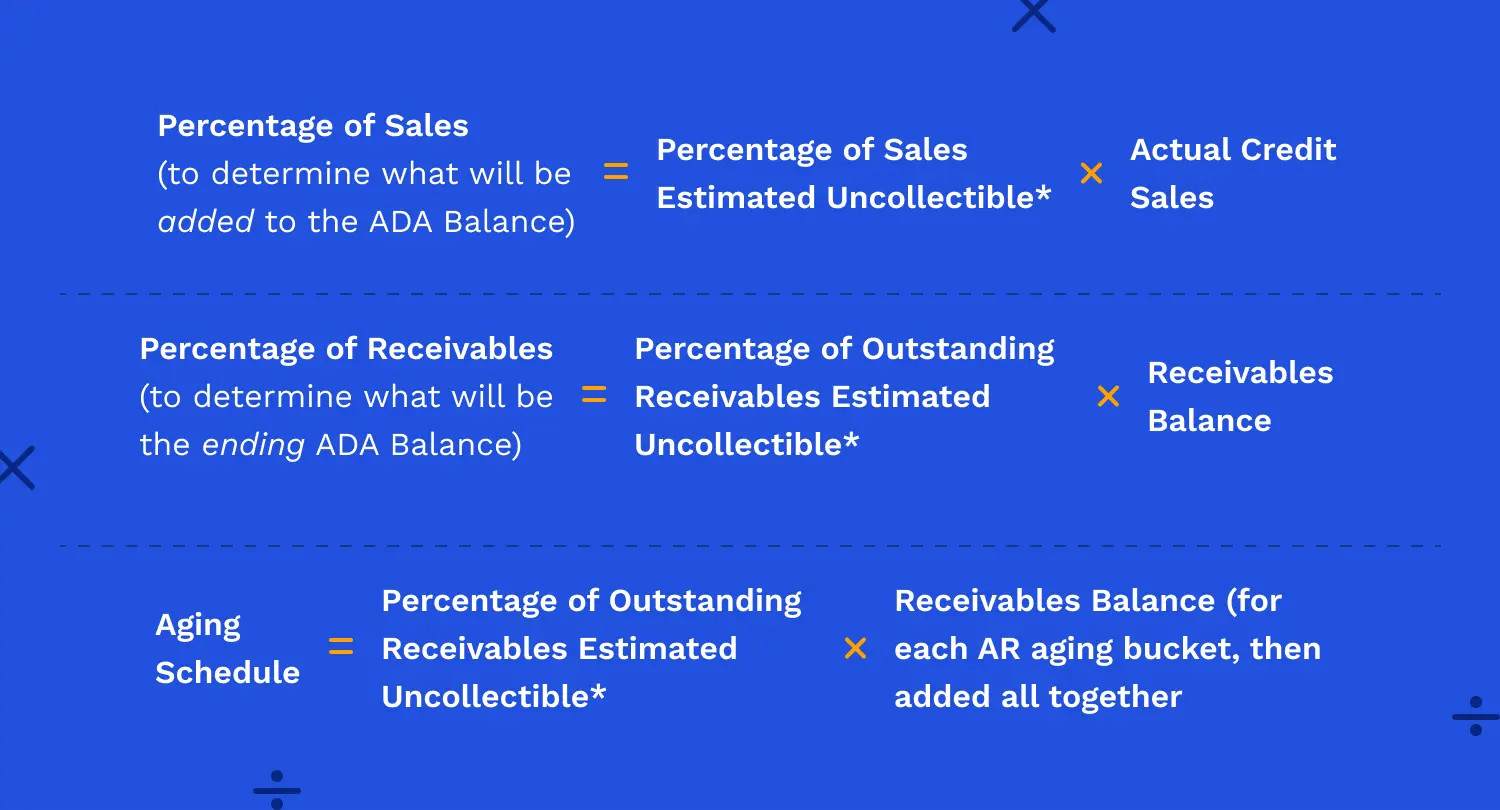

5.1 Formulas

- Percentage of sales = Percentage of sales estimated uncollectible * Actual credit sales

- Percentage of receivables = Percentage of outstanding receivables estimated uncollectible * Receivables Balance

- Aging schedule = Percentage of outstanding receivables estimated uncollectible * Receivables balance (for each aging bucket, then added all together)

5.2 Consistency

Any bad debt expense formula can be used, as long as you remain consistent from year to year. If you change methods, disclose this in your financial statements.

Based on data from previous years

Based on data from previous years

This image shows an overview of how to calculate bad debt expense using the three main methods: percentage of sales, percentage of receivables, and aging schedule.

6. How Collaborative Accounts Receivable Minimizes Bad Debt Expense

Collaborative accounts receivable (AR) solutions can significantly reduce bad debt expenses by optimizing collection management. Versapay, for instance, uses automation and cloud-based collaboration to align customers, sales, and AR teams.

6.1 Transparent Communication

Collaborative AR enhances communication between AR staff and customers. It addresses issues like disputed invoice charges or missing remittance information by providing a centralized platform for all necessary information.

6.1.1 Dispute Resolution

AR teams can seamlessly involve necessary team members to resolve disputes, tapping into shared knowledge faster. Customers gain full visibility into their outstanding balances and can make payments through a self-service portal.

6.1.2 Transparent Credit Policies

This minimizes disputes and creates transparent credit policies, removing barriers to on-time payments.

6.2 Alignment Between Sales and AR Teams

Collaborative AR improves communication between sales and AR teams. Sales teams can access customer payment history and cash flow data to make informed credit decisions.

6.2.1 Informed Credit Decisions

By accessing data on customer payment behavior, sales teams can negotiate credit terms effectively. This ensures no misunderstandings about credit terms and early payment incentives.

6.2.2 Beneficial Credit Cycles

The result is credit cycles that benefit both customers and the organization.

6.3 Focus on Value-Added Work

A collaborative AR tool combines cloud-based collaboration features with AR automation. AR teams can automate invoicing, collections, payment processing, and cash application workflows.

6.3.1 Strategic Focus

Automating routine tasks allows AR teams to focus on strategic, value-added work, such as uncovering the causes of payment delays and better understanding customer needs.

6.3.2 Improved Customer Relationships

This not only strengthens customer relationships but also minimizes bad debt expense by reducing the likelihood of receivables becoming uncollectible.

7. What Role Does a Strong Credit Policy Play in Minimizing Bad Debt?

A strong credit policy is essential for minimizing bad debt. It sets clear guidelines for extending credit to customers and outlines procedures for managing and collecting receivables.

7.1 Key Components of a Credit Policy

- Credit Evaluation: Assessing the creditworthiness of potential customers before extending credit.

- Credit Limits: Setting appropriate credit limits based on the customer’s financial strength.

- Payment Terms: Clearly defining payment terms, including due dates and late payment penalties.

- Collection Procedures: Establishing procedures for following up on overdue invoices and pursuing collections.

7.2 Benefits of a Strong Credit Policy

- Reduced Risk: Minimizes the risk of extending credit to customers who are likely to default.

- Improved Cash Flow: Ensures timely payments and reduces the need for extensive collection efforts.

- Better Customer Relationships: Promotes transparency and clear communication, fostering trust with customers.

7.3 Implementing a Credit Policy

- Develop Clear Guidelines: Create a written policy that outlines all aspects of credit management.

- Communicate the Policy: Ensure all employees, especially those in sales and AR, understand the policy.

- Enforce the Policy: Consistently apply the policy to all customers, regardless of size or relationship.

- Regularly Review and Update: Periodically review the policy and update it as needed to reflect changing business conditions.

8. What are the Key Performance Indicators (KPIs) to Monitor Bad Debt?

Monitoring key performance indicators (KPIs) is crucial for tracking and managing bad debt effectively. These metrics provide insights into the effectiveness of credit and collection efforts.

8.1 Key KPIs

- Bad Debt Expense Ratio: Bad debt expense divided by total sales. This ratio indicates the percentage of sales that are uncollectible.

- Days Sales Outstanding (DSO): The average number of days it takes to collect receivables. A higher DSO may indicate potential collection problems.

- Collection Effectiveness Index (CEI): Measures the percentage of receivables collected during a specific period. A lower CEI may signal issues with collection efforts.

- Aging of Receivables: A report that categorizes receivables by the length of time they have been outstanding. This helps identify overdue invoices and potential bad debts.

8.2 Benchmarking KPIs

Compare your company’s KPIs to industry benchmarks to assess performance. This helps identify areas for improvement and set realistic goals.

8.3 Using KPIs to Drive Improvement

- Track KPIs Regularly: Monitor KPIs on a monthly or quarterly basis.

- Analyze Trends: Identify trends and patterns in the data.

- Take Corrective Action: Implement changes to credit and collection policies based on the analysis.

- Measure Results: Track KPIs after implementing changes to assess their effectiveness.

9. What Strategies Can Be Implemented to Improve Debt Collection?

Implementing effective debt collection strategies is crucial for minimizing bad debt and improving cash flow. These strategies range from proactive communication to more assertive collection efforts.

9.1 Proactive Communication

- Clear Invoices: Ensure invoices are clear, accurate, and easy to understand.

- Payment Reminders: Send regular payment reminders before and after the due date.

- Offer Payment Options: Provide multiple payment options, such as online payments, ACH transfers, and payment plans.

9.2 Collection Efforts

- Follow-Up Calls: Make follow-up calls to customers with overdue invoices.

- Payment Plans: Offer payment plans to customers who are struggling to pay.

- Collection Agency: Consider using a collection agency for accounts that are severely overdue.

9.3 Legal Action

- Small Claims Court: Pursue legal action in small claims court for smaller debts.

- Lawsuit: Consider filing a lawsuit for larger debts.

9.4 Maintaining Customer Relationships

- Empathy: Approach collection efforts with empathy and understanding.

- Negotiation: Be willing to negotiate payment terms and amounts.

- Customer Service: Provide excellent customer service throughout the collection process.

10. How to Leverage Technology to Manage Bad Debt Expense?

Leveraging technology can significantly improve the management of bad debt expense. AR automation software, data analytics, and customer relationship management (CRM) systems offer tools for streamlining credit and collection processes.

10.1 AR Automation Software

- Automated Invoicing: Automates the creation and delivery of invoices.

- Payment Reminders: Automatically sends payment reminders.

- Collection Workflows: Streamlines collection efforts with automated workflows.

- Reporting: Provides detailed reports on AR performance.

10.2 Data Analytics

- Predictive Analytics: Uses historical data to predict potential bad debts.

- Risk Scoring: Assigns risk scores to customers based on their payment behavior.

- Trend Analysis: Identifies trends and patterns in AR data.

10.3 CRM Systems

- Customer Information: Provides a centralized repository for customer information.

- Communication Tracking: Tracks all communication with customers.

- Integration: Integrates with accounting and AR systems.

10.4 Benefits of Technology

- Efficiency: Automates routine tasks and reduces manual effort.

- Accuracy: Minimizes errors and improves data quality.

- Visibility: Provides real-time visibility into AR performance.

- Decision Making: Supports data-driven decision making.

Income-partners.net is your strategic ally in navigating the complexities of financial management. We provide insights into the most effective methods to minimize bad debt expense and increase profitability. By offering customized partnership strategies, we help you create strong alliances that drive growth and stability.

Ready to discover how strategic partnerships can revolutionize your approach to revenue generation? Visit income-partners.net and take the first step toward financial success.

Address: 1 University Station, Austin, TX 78712, United States.

Phone: +1 (512) 471-3434.

FAQ: Bad Debt Expense

1. What is bad debt expense?

Bad debt expense is the portion of a company’s accounts receivable that is deemed uncollectible, reflecting a loss on potential revenue.

2. Where does bad debt expense appear on the income statement?

Bad debt expense typically appears as an operating expense under Sales, General, and Administrative Expenses (SG&A) on the income statement.

3. What accounting method requires recording bad debt expense?

The accrual accounting method requires recording bad debt expense to match expenses with related revenue in the same period.

4. What are the two main methods for recording bad debt expense?

The two main methods are the direct write-off method and the allowance method.

5. What is the direct write-off method?

The direct write-off method involves writing off a receivable as bad debt immediately when it is deemed uncollectible.

6. What is the allowance method?

The allowance method involves estimating uncollectible accounts at the end of each fiscal year and creating an allowance for doubtful accounts (AFDA).

7. What are the three methods for estimating bad debt expense using the allowance method?

The three methods are the percentage of sales, percentage of receivables, and accounts receivable aging.

8. How does collaborative accounts receivable minimize bad debt expense?

Collaborative AR enhances communication, aligns sales and AR teams, and automates routine tasks, reducing the likelihood of receivables becoming uncollectible.

9. What is a key performance indicator (KPI) for monitoring bad debt?

A key KPI is the bad debt expense ratio, which indicates the percentage of sales that are uncollectible.

10. How can technology help manage bad debt expense?

Technology such as AR automation software, data analytics, and CRM systems can streamline credit and collection processes, improving efficiency and decision-making.