Splitting bills based on income is a fair and practical way for couples to manage their finances, especially when there’s an income disparity. At income-partners.net, we understand the importance of financial harmony in partnerships and relationships. By calculating each person’s contribution based on their income percentage, couples can ensure a balanced approach to shared expenses, fostering transparency and equity. Explore collaborative finance, shared expenses management, and income-based budgeting for stronger financial partnerships.

1. What Is The Best Way To Split Bills Based On Income?

The best way to split bills based on income involves calculating each partner’s contribution based on their percentage of the total household income. This approach ensures fairness, especially when there is a significant income difference between partners. According to a study by the University of Texas at Austin’s McCombs School of Business, couples who split bills proportionally to their income report higher levels of financial satisfaction and lower stress related to money management. The proportional method acknowledges that individuals with higher incomes can contribute more without significantly impacting their financial well-being, while those with lower incomes are not overburdened. This method involves several steps, including calculating the total household income, determining each partner’s income percentage, and applying these percentages to the total shared expenses.

1.1. Why Is Splitting Bills Based On Income Important?

Splitting bills based on income is crucial because it promotes fairness and reduces financial strain in relationships. When partners contribute proportionally, it reflects their ability to pay and ensures that no one is overburdened. This approach is supported by research from financial experts at Harvard Business Review, which emphasizes that transparent and equitable financial practices lead to stronger, more resilient partnerships. Unequal contributions can lead to resentment and financial stress, especially if one partner feels they are carrying a disproportionate share of the financial burden. A fair system fosters open communication and mutual respect, which are vital for a healthy relationship.

1.2. How Does This Approach Differ From Other Methods?

Splitting bills based on income differs significantly from other methods, such as the 50/50 split or one person paying all the bills. The 50/50 split can be unfair when incomes are not equal, potentially burdening the lower-income partner. According to Entrepreneur.com, a proportional split is more equitable because it aligns contributions with each partner’s financial capacity. In contrast, having one person cover all expenses can lead to a lack of financial independence and potential power imbalances within the relationship. Income-based splitting acknowledges financial disparities and adjusts contributions accordingly, promoting a sense of balance and shared responsibility.

2. What Are The Steps For Splitting Bills Based On Income?

Splitting bills based on income involves a straightforward process that ensures fairness and transparency. The process can be broken down into three primary steps: calculating the total household income, determining each partner’s percentage contribution, and calculating individual contributions to shared expenses. Following these steps allows couples to create a balanced and equitable financial arrangement.

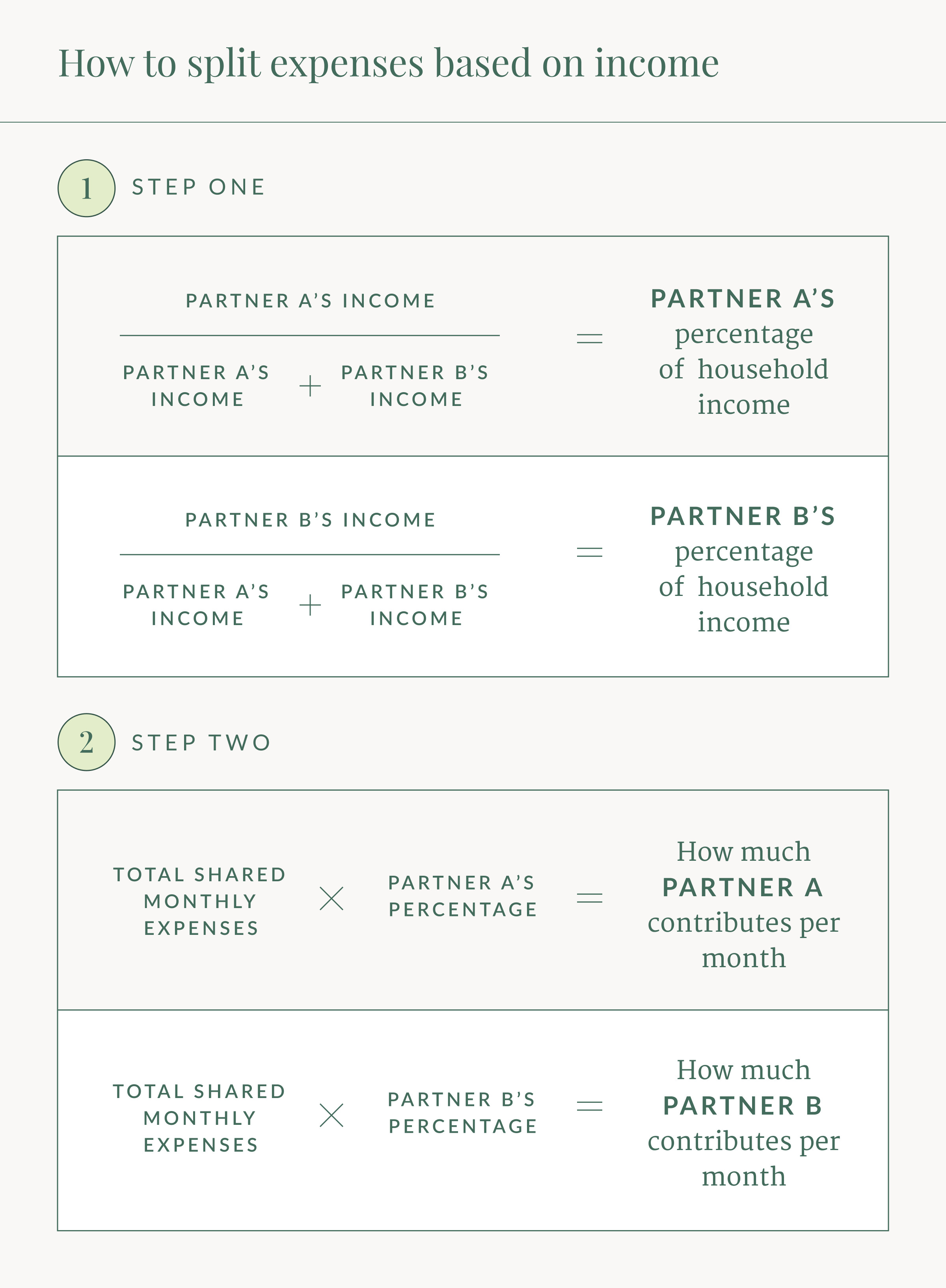

2.1. Step 1: Calculate Total Household Income

The first step is to calculate the total household income by adding each partner’s gross income. This total represents the combined financial resources available to the couple. For example, if Partner A earns $60,000 annually and Partner B earns $40,000 annually, the total household income is $100,000. Accurate calculation is essential as it forms the basis for determining each partner’s contribution percentage.

2.2. Step 2: Determine Each Partner’s Percentage Contribution

Next, calculate each partner’s percentage contribution to the total household income. This is done by dividing each partner’s individual income by the total household income. Using the previous example, Partner A’s contribution is ($60,000 / $100,000) = 60%, and Partner B’s contribution is ($40,000 / $100,000) = 40%. These percentages will be used to determine how much each partner pays toward shared expenses.

2.3. Step 3: Calculate Individual Contributions To Shared Expenses

The final step is to apply each partner’s percentage to the total shared expenses. First, determine the total monthly shared expenses, including rent, utilities, groceries, and other shared costs. Then, multiply the total shared expenses by each partner’s percentage. For instance, if the total monthly shared expenses are $2,500, Partner A would contribute ($2,500 60%) = $1,500, and Partner B would contribute ($2,500 40%) = $1,000. This method ensures that contributions are proportional to income, promoting fairness.

3. How To Set Up A Joint Account For Shared Expenses?

Setting up a joint account for shared expenses simplifies the process of bill splitting and promotes financial transparency. This account is used exclusively for shared expenses, making it easier to track and manage contributions. To set up a joint account, consider the following steps and tips to ensure a smooth and effective process.

3.1. Opening A Joint Checking Account

Opening a joint checking account is a practical way to manage shared expenses. Both partners have access to the account and can deposit funds and pay bills. To open an account, visit a local bank or credit union and provide the necessary documentation, including identification and proof of address. According to financial advisors, choosing a bank with no monthly fees and convenient online banking can further streamline the process. Once the account is open, both partners can set up automatic transfers to deposit their contributions.

3.2. Automating Transfers Into The Joint Account

Automating transfers into the joint account ensures that contributions are made consistently and on time. Most banks allow you to set up recurring transfers from individual accounts to the joint account. Schedule these transfers to coincide with payday to simplify the process. For example, if Partner A needs to contribute $1,500 per month, they can set up two transfers of $750 each, coinciding with their bi-weekly paychecks. Automation minimizes the risk of missed payments and keeps the joint account adequately funded.

3.3. Managing And Tracking Shared Expenses

Effectively managing and tracking shared expenses is essential for maintaining financial transparency and avoiding disputes. Use budgeting apps or spreadsheets to monitor income and expenses. Tools like Mint, YNAB (You Need a Budget), or a simple Google Sheets document can help track where money is being spent and ensure that both partners are aware of the financial status. Regularly reviewing the joint account and shared expenses allows couples to make necessary adjustments and stay aligned on their financial goals.

4. What Are Some Real-World Examples Of Splitting Bills Based On Income?

Real-world examples can illustrate how splitting bills based on income works in practice. Let’s consider a few scenarios with different income levels and expense amounts to demonstrate the flexibility and fairness of this approach. These examples highlight how couples can adapt the method to their specific financial situations.

4.1. Example 1: A Couple With A Significant Income Disparity

Consider a couple where Partner A earns $80,000 per year and Partner B earns $30,000 per year. Their total household income is $110,000. Partner A’s contribution is ($80,000 / $110,000) = 72.7%, and Partner B’s contribution is ($30,000 / $110,000) = 27.3%. If their total monthly shared expenses are $3,000, Partner A would contribute ($3,000 72.7%) = $2,181, and Partner B would contribute ($3,000 27.3%) = $819. This example shows how the higher-earning partner contributes more, but the lower-earning partner’s contribution is still manageable.

4.2. Example 2: A Couple With Moderate Income Differences

In another scenario, Partner A earns $55,000 per year and Partner B earns $45,000 per year, making their total household income $100,000. Partner A’s contribution is ($55,000 / $100,000) = 55%, and Partner B’s contribution is ($45,000 / $100,000) = 45%. If their total monthly shared expenses are $2,000, Partner A would contribute ($2,000 55%) = $1,100, and Partner B would contribute ($2,000 45%) = $900. Even with moderate income differences, the proportional split ensures fairness.

4.3. Example 3: A Couple Who Includes Savings Goals

Suppose Partner A earns $70,000 per year and Partner B earns $50,000 per year, with a total household income of $120,000. Partner A’s contribution is ($70,000 / $120,000) = 58.3%, and Partner B’s contribution is ($50,000 / $120,000) = 41.7%. Their total monthly shared expenses, including rent, utilities, and a $500 savings goal, amount to $3,000. Partner A contributes ($3,000 58.3%) = $1,749, and Partner B contributes ($3,000 41.7%) = $1,251. This example illustrates how savings goals can be incorporated into the shared expenses, promoting joint financial planning.

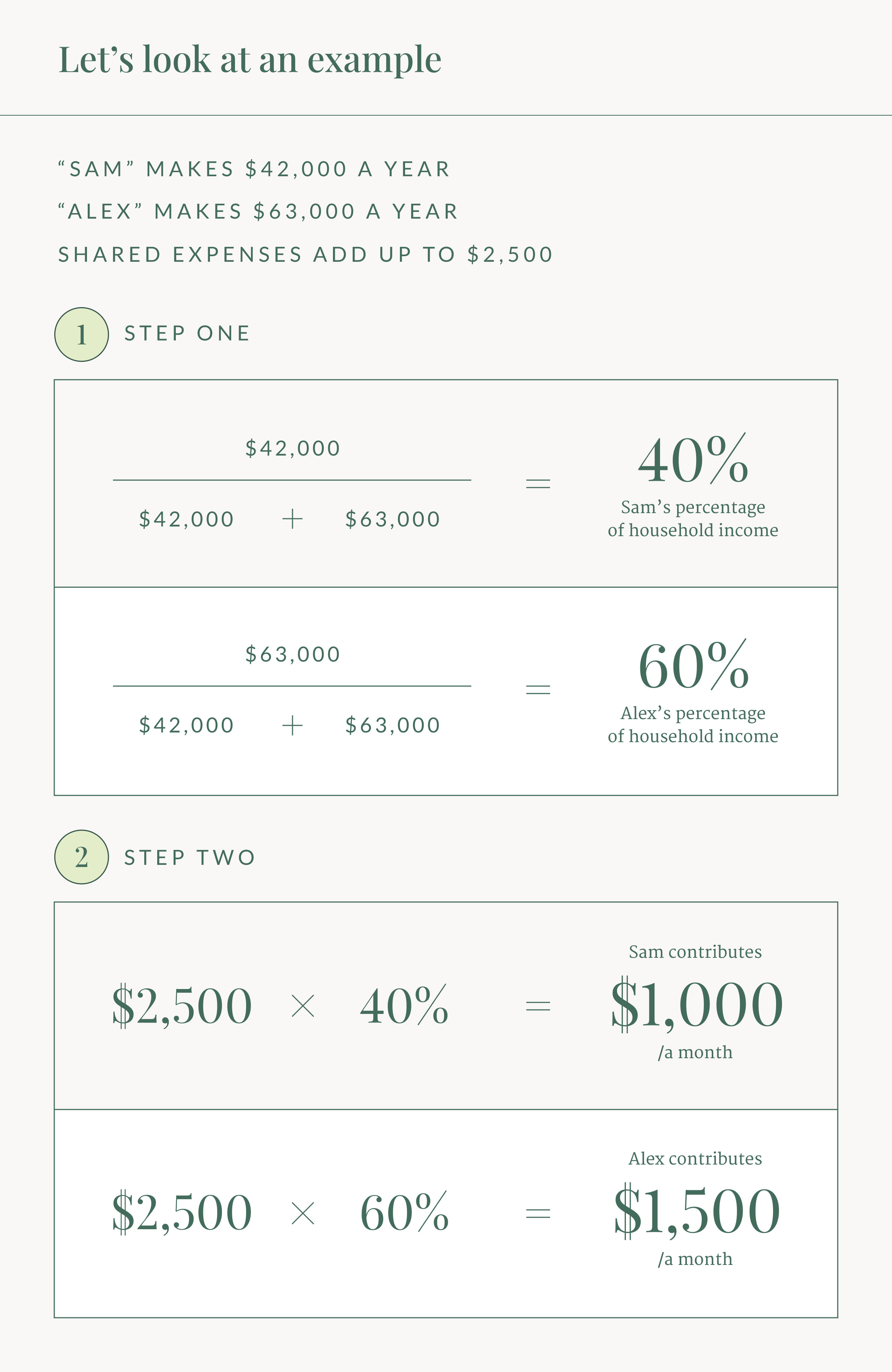

A visual, mathematical representation of the example calculations described in this section. Slide format.

A visual, mathematical representation of the example calculations described in this section. Slide format.

5. What Expenses Should Be Included When Splitting Bills Based On Income?

Deciding which expenses to include when splitting bills based on income requires careful consideration and open communication. The goal is to identify expenses that benefit both partners and contribute to their shared life. Common categories include housing, utilities, groceries, transportation, and shared entertainment. However, couples can customize the list based on their unique circumstances and preferences.

5.1. Core Shared Expenses (Rent, Utilities, Groceries)

Core shared expenses typically include rent or mortgage payments, utilities (electricity, water, gas, internet), and groceries. These are fundamental costs associated with maintaining a household and are usually shared equally. Including these expenses ensures that both partners contribute to the basic necessities of their shared living space.

5.2. Other Shared Expenses (Transportation, Entertainment, Savings Goals)

Beyond the core expenses, consider including transportation costs (car payments, public transit), entertainment (streaming services, dining out), and savings goals (vacations, emergency fund). If both partners use a car, including car payments and insurance can be fair. Shared entertainment expenses should also be included to promote a balanced lifestyle. Additionally, incorporating savings goals ensures that both partners are contributing to their future financial security.

5.3. Personal vs. Shared Expenses: How To Draw The Line

Drawing the line between personal and shared expenses is crucial for maintaining financial clarity. Personal expenses are those that benefit only one partner, such as personal car payments, clothing, hobbies, and individual debts. It’s generally best to keep these separate and not include them in the shared expenses calculation. However, couples can make exceptions based on their specific circumstances. For example, if one partner has significantly higher student loan payments, they might agree to include a portion of those payments in the shared expenses to balance the financial burden.

6. How To Handle Changes In Income When Splitting Bills Based On Income?

Changes in income are inevitable, whether due to promotions, job losses, or career changes. When splitting bills based on income, it’s essential to have a plan for adjusting contributions to reflect these changes. Regular reviews and open communication are key to maintaining fairness and preventing financial strain.

6.1. Regularly Reviewing And Adjusting Contributions

Regularly reviewing and adjusting contributions ensures that the bill-splitting arrangement remains fair and equitable. Schedule a monthly or quarterly meeting to review income and expenses. During these meetings, recalculate each partner’s percentage contribution based on their current income. This proactive approach prevents financial imbalances and promotes transparency.

6.2. What Happens If One Partner’s Income Decreases?

If one partner’s income decreases, it’s essential to adjust contributions to reflect the new financial situation. This might mean that the other partner temporarily contributes a higher percentage of the shared expenses. Open communication is critical during these times. Discuss the situation openly and collaboratively to find a solution that works for both partners. According to financial experts, being flexible and supportive can strengthen the relationship and prevent financial stress from causing conflict.

6.3. What Happens If One Partner’s Income Increases?

Conversely, if one partner’s income increases, their contribution to shared expenses should also increase. This ensures that the financial burden remains balanced and fair. The higher-earning partner should be willing to contribute a larger percentage, which can also free up funds for shared savings goals or other financial priorities. Adjusting contributions in response to income changes maintains the integrity of the income-based bill-splitting arrangement.

7. What Are The Benefits Of Using A Proportional Approach?

Using a proportional approach to splitting bills based on income offers numerous benefits, promoting financial fairness, reducing stress, and fostering open communication. This method acknowledges income disparities and ensures that contributions align with each partner’s financial capacity. By adopting a proportional approach, couples can create a more harmonious and equitable financial relationship.

7.1. Fairness And Equity In Financial Contributions

Fairness and equity are central to the proportional approach. By aligning contributions with income, couples ensure that neither partner is overburdened. This method acknowledges that those with higher incomes have a greater capacity to contribute without experiencing financial strain. The lower-earning partner is not forced to contribute an amount that compromises their financial well-being. This sense of fairness promotes mutual respect and strengthens the relationship.

7.2. Reduced Financial Stress And Conflict

Splitting bills proportionally can significantly reduce financial stress and conflict. When contributions are equitable, partners are less likely to feel resentment or financial pressure. Open communication about finances becomes easier, as both partners feel that the arrangement is fair. According to relationship experts, addressing financial issues proactively can prevent them from escalating into larger conflicts.

7.3. Enhanced Communication And Transparency

The proportional approach encourages enhanced communication and transparency. Regularly reviewing income and expenses requires open dialogue and honesty. This process fosters a deeper understanding of each partner’s financial situation and promotes joint financial planning. Transparency builds trust and strengthens the financial foundation of the relationship.

8. What Are Some Potential Challenges And How To Overcome Them?

While splitting bills based on income offers numerous benefits, it’s not without potential challenges. These challenges can range from reluctance to share financial information to disagreements over which expenses should be included. Addressing these challenges proactively and communicating openly is key to maintaining a successful bill-splitting arrangement.

8.1. Reluctance To Share Financial Information

One of the most significant challenges is reluctance to share financial information. Some partners may feel uncomfortable disclosing their income or financial details. Overcoming this requires building trust and creating a safe space for open communication. Emphasize that sharing financial information is essential for creating a fair and equitable arrangement. Reassure your partner that the information will be used responsibly and with respect.

8.2. Disagreements Over Which Expenses To Include

Disagreements over which expenses to include are another common challenge. One partner may feel that certain expenses should be considered personal, while the other believes they should be shared. Resolving these disagreements requires compromise and a willingness to see the other person’s perspective. Discuss the benefits and drawbacks of including each expense and come to a mutual agreement. Remember, the goal is to create a system that is fair and works for both partners.

8.3. Difficulty Tracking And Managing Expenses

Tracking and managing expenses can be time-consuming and challenging. Using budgeting apps or spreadsheets can simplify the process. These tools help track income and expenses, making it easier to see where money is going and ensure that contributions are accurate. Regularly reviewing these records together can also promote transparency and prevent misunderstandings.

9. How Does Splitting Bills Based On Income Affect Financial Independence?

Splitting bills based on income can have both positive and negative effects on financial independence. While it promotes fairness and shared responsibility, it’s essential to strike a balance that allows each partner to maintain some level of financial autonomy. Consider the potential impacts on individual spending, saving, and debt management.

9.1. Maintaining Individual Spending Habits

One of the benefits of splitting bills proportionally is that it allows each partner to maintain some level of individual spending habits. After contributing to shared expenses, each partner has the freedom to spend the remaining money as they choose. This can help maintain a sense of independence and prevent feelings of resentment. However, it’s essential to be mindful of how individual spending habits might impact the overall financial health of the relationship.

9.2. Balancing Shared And Individual Savings Goals

Balancing shared and individual savings goals is crucial for maintaining financial independence. While contributing to shared savings goals is important, each partner should also have the opportunity to save for their own individual goals. This might include saving for retirement, a down payment on a house, or other personal investments. Striking a balance between shared and individual savings goals ensures that both partners feel financially secure and independent.

9.3. Managing Individual Debt Responsibilities

Managing individual debt responsibilities is another important aspect of financial independence. Each partner should be responsible for managing their own debt, such as student loans or credit card debt. While some couples might choose to include a portion of debt payments in shared expenses, it’s generally best to keep these separate. This ensures that each partner maintains control over their own financial obligations and prevents debt from becoming a source of conflict in the relationship.

10. What Are The Tax Implications Of Splitting Bills Based On Income?

Splitting bills based on income generally has minimal direct tax implications, as it primarily involves managing shared household expenses. However, there are a few indirect considerations that couples should be aware of, particularly when it comes to deductions, tax credits, and record-keeping. Understanding these implications can help couples optimize their tax planning.

10.1. Understanding Potential Deductions And Credits

While splitting bills doesn’t directly impact taxes, some expenses might qualify for deductions or credits. For example, if the couple owns a home, they can deduct mortgage interest and property taxes. These deductions can be claimed by the partner who pays the expenses or split based on their ownership percentage. Additionally, if the couple has children, they might be eligible for child tax credits or dependent care credits. Understanding these potential deductions and credits can help reduce their overall tax liability.

10.2. How To Handle Joint vs. Individual Tax Responsibilities

When it comes to joint vs. individual tax responsibilities, it’s essential to understand the implications of filing jointly or separately. Filing jointly can often result in lower taxes, as it allows couples to take advantage of certain tax breaks and deductions that are not available to those filing separately. However, it also means that both partners are jointly liable for any tax obligations. Filing separately might be beneficial in certain situations, such as when one partner has significant medical expenses or business losses. Consulting with a tax professional can help couples determine the best filing strategy for their individual circumstances.

10.3. The Importance Of Keeping Accurate Records

Keeping accurate records is crucial for managing taxes effectively. This includes tracking income, expenses, and any relevant deductions or credits. Using accounting software or spreadsheets can simplify the process and ensure that all financial information is readily available when it’s time to file taxes. Accurate record-keeping not only makes tax preparation easier but also helps couples stay organized and informed about their overall financial situation.

By implementing these strategies, couples can successfully split bills based on income, promoting fairness, reducing stress, and fostering open communication. Remember, the goal is to create a system that works for both partners and supports their long-term financial well-being. For more information and resources on managing finances as a couple, visit income-partners.net.

A visual, mathematic representation of the calculations described in the second step of this section. Slide format.

A visual, mathematic representation of the calculations described in the second step of this section. Slide format.

Are you ready to take control of your financial future and build stronger, more equitable partnerships? Visit income-partners.net today to discover valuable resources, expert advice, and collaborative tools that will help you navigate the complexities of shared finances. Don’t wait – start building your path to financial success together now!

Address: 1 University Station, Austin, TX 78712, United States

Phone: +1 (512) 471-3434

Website: income-partners.net

FAQ: Splitting Bills Based on Income

-

What is the most equitable way to split bills in a relationship with unequal incomes?

Splitting bills proportionally based on income is the most equitable approach. It ensures each partner contributes according to their financial capacity, fostering fairness and reducing financial stress. -

How do you calculate the percentage each partner should contribute?

Calculate each partner’s contribution by dividing their individual income by the total household income. This percentage is then applied to the total shared expenses. -

What expenses should be included when splitting bills based on income?

Include core shared expenses like rent, utilities, and groceries, as well as other shared expenses like transportation, entertainment, and savings goals. Personal expenses should generally be kept separate. -

What happens if one partner’s income decreases?

If one partner’s income decreases, contributions should be adjusted to reflect the new financial situation. The other partner may temporarily contribute a higher percentage of the shared expenses. -

How often should contributions be reviewed and adjusted?

Contributions should be reviewed and adjusted regularly, ideally monthly or quarterly, to account for any changes in income or expenses. -

What are the benefits of using a proportional approach?

The benefits include fairness and equity in financial contributions, reduced financial stress and conflict, and enhanced communication and transparency. -

What are some potential challenges and how can they be overcome?

Challenges include reluctance to share financial information and disagreements over which expenses to include. Overcoming these requires building trust, open communication, and compromise. -

How does splitting bills based on income affect financial independence?

While promoting fairness, it’s essential to strike a balance that allows each partner to maintain some level of financial autonomy. Manage individual spending habits and balance shared and individual savings goals. -

What are the tax implications of splitting bills based on income?

Splitting bills generally has minimal direct tax implications, but couples should be aware of potential deductions, tax credits, and the importance of keeping accurate records. -

Where can I find more resources on managing finances as a couple?

Visit income-partners.net for valuable resources, expert advice, and collaborative tools to help you navigate shared finances and build stronger, more equitable partnerships.