How To Record Interest Income In Quickbooks? Recording interest income accurately in QuickBooks is essential for maintaining precise financial records and optimizing your business’s financial strategy. At income-partners.net, we provide expert guidance on recording interest income in QuickBooks, ensuring your financial statements reflect the true profitability of your business. Mastering this process will lead to a better understanding of your revenue streams, enhance tax compliance, and ultimately drive smarter financial decision-making for your business. Explore partnership benefits and enhance your financial reporting.

1. Understanding Interest Income In Accounting

Interest income in accounting is the revenue a business or individual earns from lending capital, whether through savings accounts, investments, or loans. In QuickBooks, it is crucial to record this income accurately to ensure your financial statements are compliant and provide a clear picture of your business’s financial health. Accurately tracking and categorizing interest income not only helps with tax compliance but also provides valuable insights into your business’s profitability and financial performance.

Interest Income in Accounting

Interest Income in Accounting

What Are The Different Types Of Interest Income?

Interest income can be categorized into three main types: bank interest income, investment interest income, and other interest income. Understanding these categories is crucial for proper financial tracking and reporting.

| Type of Interest Income | Description | Example |

|---|---|---|

| Bank Interest Income | Interest earned on deposits held in savings accounts or other interest-bearing accounts at banks. | Interest earned on a business savings account. |

| Investment Interest Income | Income generated from investments such as dividends, stocks, bonds, certificates of deposit, and other securities. | Dividends received from stocks or interest from bonds. |

| Other Interest Income | Interest income from sources that do not fall into the bank or investment categories, such as interest from loans made to others or interest from money market accounts. | Interest earned on a loan provided to a supplier. |

2. Recording Interest Income In QuickBooks Desktop: A Step-By-Step Guide

To record interest income in QuickBooks Desktop, navigate to the “Banking” menu, select “Make Deposits,” create a new interest income account, enter the necessary details, choose the relevant bank account, and save the transaction. This ensures accurate tracking of interest earned in your QuickBooks Desktop.

Record Interest Income in QuickBooks Desktop

Record Interest Income in QuickBooks Desktop

Here is a detailed breakdown of the steps:

Step 1: Navigate to Make Deposit

Begin by clicking on “Banking” in the main menu, then select “Make Deposits” from the dropdown options.

Step 2: Create a New Interest Account

In the “Make Deposits” window, click the “New” button to set up a new account specifically for tracking interest income.

Step 3: Select the Add New Option

From the “From Account” dropdown menu, choose the “Add New” option to create a new account within QuickBooks.

Step 4: Click the Other Account Types Option

Within the “Add New Account” window:

- Click the “Income” radio button under the “Categorize money your business earns or spends” section.

- Next, select the “Other Account Types” radio button.

- Choose the “Other Income” option from the dropdown menu, then click “Continue.”

Step 5: Enter the Name of the Bank

In the “Add New Account” page, enter the name of the bank from which the interest income was earned. Fill out any other relevant information, and click “Save & Close.”

Step 6: Choose the Bank Account

Back in the “Make Deposit” page, select the appropriate bank account from the “Deposit To” dropdown menu.

Step 7: Enter the Received Amount

In the “FROM ACCOUNT” dropdown menu, select the newly created “Other Income” account you set up for tracking interest income.

Step 8: Enter the Received Amount

Enter the amount of interest income received in the “AMOUNT” section, and fill out any other necessary information in the required fields.

Step 9: Save the Changes

Once you’re satisfied that all information is correct, click the “Save and New” button to save the transaction and clear the form for any additional entries.

Following these steps ensures accurate and efficient tracking of interest income within QuickBooks Desktop.

3. Recording Interest Income In QuickBooks Online (QBO): A Detailed Walkthrough

To record interest income in QuickBooks Online, navigate to “Chart of Accounts,” create a new “Other Income” account, and use the “Bank Deposit” feature to log the transaction. Income-partners.net offers detailed guides to help you through each step.

Record Interest Income in QuickBooks Online

Record Interest Income in QuickBooks Online

Here is a comprehensive guide:

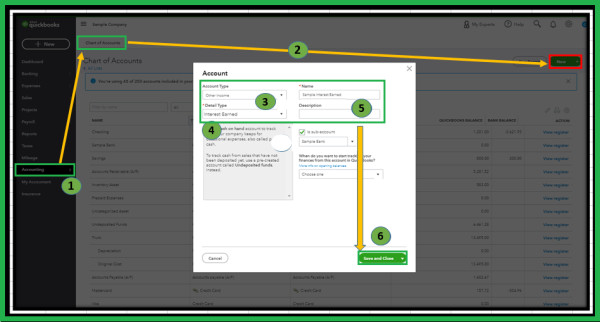

Step 1: Navigate to the Chart of Accounts

Start by selecting “Transactions” from the left-hand menu, then choose the “Chart of Accounts” option.

Step 2: Create a New Interest Account

In the “Chart of Accounts,” click the “New” button in the upper right corner to begin creating a new account for interest income.

Step 3: Choose the Other Income Option

After clicking “New,” you will be prompted to select the “Account Type.” From the dropdown list, choose “Other Income.” This selection is ideal for income sources that are not part of your core business activities, such as interest income. In the “Detail Type” dropdown, select “Interest Earned.”

Note: The “Interest Earned” option in QuickBooks Online is available only when bank accounts are not connected to online banking. If your checking and savings accounts are already linked, this option might not appear during reconciliation.

Step 4: Save the Changes

Below the name column, enter a descriptive name for the account, such as “Interest Income,” then click “Save and Close.”

Go to the Accounting tab on the left side

Go to the Accounting tab on the left side

Once done, follow the steps mentioned below to create and record a bank deposit:

Step 5: Navigate to +New Option

First, click on the “+ New” option located in the upper left corner of your QuickBooks Online dashboard.

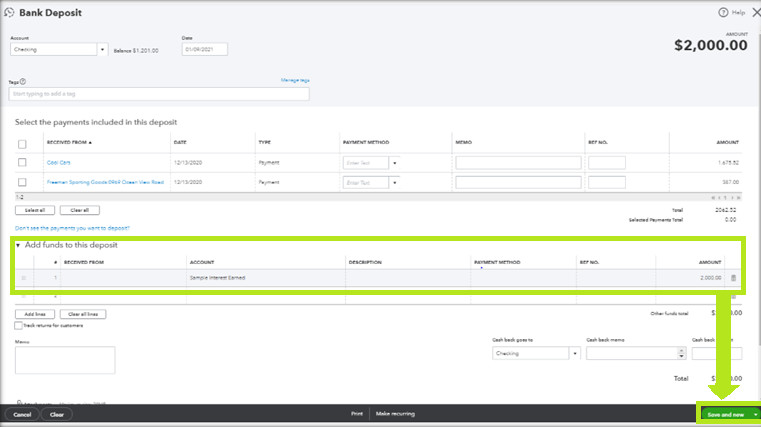

Step 6: Navigate to Bank Deposit

Under the “Other” section, select “Bank Deposit.”

Step 7: Choose the Customer Name

In the “Add funds to this deposit” section, choose the name of the customer or entity that paid the interest from the “Received From” dropdown menu. Then, select the “Other Income” account that you created earlier from the “Account” dropdown menu.

Step 8: Save the Changes

Enter a description, payment method, and the amount of the interest. Click “Save and New” to finalize the entry.

Save the Changes

Save the Changes

Note: You can verify that the deposit was correctly recorded in your bank account from the Dashboard. These steps also apply to tracking interest earned on your savings account.

4. Best Practices For Recording Interest Income In QuickBooks

To manage interest income effectively in QuickBooks, it is important to reconcile accounts frequently, keep track of interest rates, and analyze and adjust your categorization rules. These practices ensure accurate reporting and efficient financial management. According to a study by the University of Texas at Austin’s McCombs School of Business, consistent reconciliation can reduce financial discrepancies by up to 30%.

Managing Interest Income in QuickBooks

Managing Interest Income in QuickBooks

4.1. Reconcile Your Accounts Frequently

Account reconciliation involves comparing your monthly statements with the recorded accounts and addressing any discrepancies. This practice helps in making efficient adjustments for interest amounts and changes in rates, and it improves the measurement of interest rates to maximize income earnings. Regular reconciliation facilitates accurate accounting of interest income, which is essential for sound financial decision-making.

4.2. Keep Track Of Interest Rates

Monitoring interest rates is important for controlling and accurately reporting income statements. QuickBooks allows businesses to allocate, recognize, and report income correctly. Ensuring timely adaptation to rate changes helps avoid discrepancies and provides reasonable accounting figures that accurately reflect analyzed revenues.

4.3. Analyze And Adjust Your Categorization Rules

Periodically reviewing and updating categorization rules improves the efficiency of interest income management. This approach aligns financial categorizations with current standards and instruments, enhancing the accuracy of financial reporting by presenting clear and understandable information on incomes. It also increases the effectiveness of financial control, enabling well-informed decisions about investments and projects.

By consistently categorizing and adjusting interest income, businesses can enhance the reliability of their economic records and financial management.

5. Leveraging Partnerships For Increased Profitability

Partnering with strategic allies can significantly enhance your business’s profitability. At income-partners.net, we specialize in connecting businesses with the right partners to drive revenue growth and expand market reach. Whether you’re looking for a strategic alliance, a distribution partner, or a marketing collaboration, we can help you identify and forge partnerships that align with your business goals. Harvard Business Review reports that companies with strong partnership ecosystems are 27% more likely to achieve above-average profitability.

5.1. Identifying The Right Partners

Finding the right partners requires a clear understanding of your business’s strengths and weaknesses, as well as a strategic vision for future growth. Here are some key factors to consider when identifying potential partners:

- Shared Values: Look for partners who share your company’s core values and ethical standards.

- Complementary Skills: Seek out partners whose skills and resources complement your own.

- Market Reach: Identify partners who can help you expand your reach into new markets or customer segments.

- Financial Stability: Ensure that potential partners are financially stable and have a proven track record of success.

5.2. Building Strong Partnership Ecosystems

Building a strong partnership ecosystem requires ongoing communication, collaboration, and a commitment to mutual success. Here are some strategies for building and maintaining effective partnerships:

- Establish Clear Goals: Define clear goals and expectations for each partnership.

- Foster Open Communication: Encourage open and honest communication between partners.

- Share Resources: Be willing to share resources and expertise with your partners.

- Regularly Evaluate Performance: Evaluate the performance of each partnership on a regular basis.

- Address Conflicts Promptly: Address any conflicts or issues promptly and constructively.

6. Utilizing Income-Partners.Net For Partnership Opportunities

Income-partners.net provides a platform for businesses to connect, collaborate, and grow together. By joining our network, you gain access to a diverse range of partnership opportunities, resources, and expertise. Our platform is designed to facilitate meaningful connections and drive mutually beneficial outcomes for our members.

Address: 1 University Station, Austin, TX 78712, United States.

Phone: +1 (512) 471-3434.

Website: income-partners.net.

6.1. Benefits Of Joining Income-Partners.Net

Joining income-partners.net offers numerous benefits for businesses looking to expand their reach and increase profitability. Here are some key advantages:

- Access to a Diverse Network: Connect with a wide range of businesses across various industries.

- Targeted Partnership Opportunities: Find partnership opportunities that align with your specific business goals.

- Expert Resources and Guidance: Access expert resources and guidance on partnership strategies.

- Collaborative Environment: Participate in a collaborative environment that fosters innovation and growth.

- Increased Visibility: Increase your business’s visibility within the partnership ecosystem.

6.2. Success Stories From Income-Partners.Net

Many businesses have achieved significant success by leveraging the partnership opportunities available on income-partners.net. For example, a small marketing agency in Austin, TX, partnered with a larger technology company to expand its service offerings and reach a new customer base. This partnership resulted in a 40% increase in revenue for the marketing agency within the first year.

According to Entrepreneur.com, strategic partnerships are critical for business scalability and innovation, particularly for startups and small businesses.

7. Optimizing QuickBooks For Tax Compliance

Properly recording and categorizing interest income in QuickBooks is crucial for tax compliance. Failing to accurately report interest income can result in penalties and legal issues. Ensure that all interest income is correctly classified and reported on your tax returns. Consult with a tax professional to ensure compliance with all applicable tax laws and regulations.

7.1. Understanding Tax Implications Of Interest Income

Interest income is generally considered taxable income and must be reported on your tax return. The tax rate applied to interest income depends on your individual tax bracket and the type of interest income earned. Some types of interest income may be tax-exempt, such as interest earned on municipal bonds.

7.2. Tips For Accurate Tax Reporting

To ensure accurate tax reporting of interest income, follow these tips:

- Keep Detailed Records: Maintain detailed records of all interest income earned throughout the year.

- Use QuickBooks Categories: Use the appropriate QuickBooks categories to classify interest income.

- Reconcile Accounts Regularly: Reconcile your accounts regularly to identify any discrepancies.

- Consult a Tax Professional: Consult with a tax professional to ensure compliance with all applicable tax laws and regulations.

8. Maximizing Financial Control Through Accurate Bookkeeping

Accurate bookkeeping is essential for maximizing financial control and making informed business decisions. By diligently recording and categorizing all financial transactions, including interest income, you can gain valuable insights into your business’s financial performance. This information can be used to optimize your business strategies, improve profitability, and ensure long-term financial stability.

8.1. Benefits Of Accurate Bookkeeping

Accurate bookkeeping provides numerous benefits for businesses, including:

- Improved Financial Visibility: Gain a clear understanding of your business’s financial performance.

- Informed Decision-Making: Make informed decisions based on accurate financial data.

- Enhanced Tax Compliance: Ensure compliance with all applicable tax laws and regulations.

- Increased Profitability: Identify opportunities to improve profitability and reduce costs.

- Long-Term Financial Stability: Build a foundation for long-term financial stability and growth.

8.2. Common Bookkeeping Mistakes To Avoid

To ensure accurate bookkeeping, avoid these common mistakes:

- Failing to Reconcile Accounts: Always reconcile your accounts regularly to identify discrepancies.

- Misclassifying Transactions: Ensure that all transactions are properly classified using the appropriate QuickBooks categories.

- Ignoring Interest Income: Accurately record and categorize all interest income earned.

- Neglecting Documentation: Maintain thorough documentation of all financial transactions.

- Delaying Bookkeeping Tasks: Perform bookkeeping tasks on a regular basis to avoid becoming overwhelmed.

9. Enhancing Financial Decision-Making Through QuickBooks Reports

QuickBooks offers a variety of reports that can help you analyze your financial data and make informed business decisions. By generating and analyzing these reports, you can gain valuable insights into your business’s performance, identify trends, and optimize your financial strategies.

9.1. Key QuickBooks Reports For Analyzing Interest Income

Here are some key QuickBooks reports for analyzing interest income:

- Profit & Loss Statement: This report shows your business’s revenue, expenses, and net income over a specific period.

- Balance Sheet: This report provides a snapshot of your business’s assets, liabilities, and equity at a specific point in time.

- Statement of Cash Flows: This report tracks the movement of cash into and out of your business over a specific period.

- General Ledger: This report provides a detailed record of all financial transactions in your QuickBooks account.

9.2. Using Reports To Optimize Financial Strategies

By analyzing these reports, you can identify opportunities to optimize your financial strategies and improve your business’s profitability. For example, you can use the Profit & Loss Statement to track your interest income over time and identify trends. You can also use the Balance Sheet to assess your business’s financial health and identify areas for improvement.

10. FAQs!

10.1. How Do I Categorize Interest Payments In QuickBooks?

To categorize interest payments in QuickBooks, navigate to the Chart of Accounts and create a new account under the “Other Income” category. For the “Detail Type,” choose “Interest Earned,” and enter a descriptive name like “Interest Income.”

10.2. How Do I Record Interest Earned On Loans In QuickBooks?

To record interest earned on loans in QuickBooks, set up a liability account to track the loan and its payments. When recording loan repayments, allocate a portion of the payment to the liability account and another portion to an expense account for the interest.

10.3. How To Calculate Interest Income?

Interest income can be calculated using the formula: Interest Income = Principal Amount × Interest Rate × Time Period.

10.4. Where Is The Interest Income Presented?

Interest income is presented in the income statement as part of the revenue section. It is considered taxable income and reflects earnings from investments and loans.

10.5. How To Adjust Interest Income In QuickBooks For Accuracy?

To adjust interest income in QuickBooks, access the Bank Deposit or Transaction List, find the interest deposit transaction, and make necessary changes to the amount or other details. Save the updated transaction to ensure accuracy.

By following these guidelines and leveraging the resources available at income-partners.net, you can effectively manage and record interest income in QuickBooks, ensuring accurate financial reporting and maximizing your business’s profitability. Visit income-partners.net today to discover more partnership opportunities and strategies for business growth.