Are you looking to understand your income tax return better and potentially increase your income through strategic partnerships? Understanding your tax return is crucial for effective financial planning and identifying opportunities for income growth. At income-partners.net, we help you decipher your tax information and connect you with partners to optimize your financial strategies. Let’s dive into this guide, exploring essential tax forms and income-boosting partnership opportunities.

1. Why Understanding Your Income Tax Return Matters

Understanding your income tax return is more than just knowing if you’ll get a refund or owe money. It offers a detailed snapshot of your financial health, reveals potential tax planning opportunities, and can even highlight areas where strategic partnerships could boost your income. According to a study by the University of Texas at Austin’s McCombs School of Business, individuals who actively understand their tax returns are more likely to engage in effective financial planning.

1.1. Unveiling Financial Insights

Your tax return contains a wealth of information about your income sources, deductions, and credits. By carefully reviewing each section, you can identify trends, understand your tax liabilities, and make informed decisions about your finances. A comprehensive review also helps in spotting any errors.

1.2. Identifying Tax Planning Opportunities

A deep understanding of your tax return enables you to identify areas for tax optimization. For instance, understanding how capital gains and losses are reported can inform your investment strategies, while knowing the details of your deductions can guide your financial planning.

1.3. Spotting Partnership Potential for Income Growth

Strategic partnerships can significantly impact your income and tax liabilities. Your tax return might reveal opportunities for collaboration with businesses that can offer tax-advantaged investments or help you optimize your business income. Leveraging these partnerships can lead to substantial financial benefits.

2. Key Forms To Focus On

Navigating the world of tax forms can be daunting. However, understanding the purpose and content of the most common forms can simplify the process. Here are the key forms you should focus on:

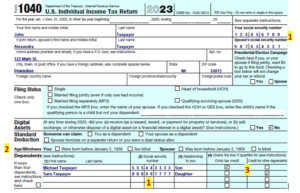

2.1. Form 1040: The Core of Your Tax Return

Form 1040 is the primary form used by individuals to file their federal income tax returns. It summarizes your income, deductions, credits, and tax liability for the year.

2.1.1. Identifying Information

Always verify that the personal information on your Form 1040 is accurate, including your Social Security number (SSN) and those of your dependents. Errors in this section can lead to processing delays or rejection of your return.

2.1.2. Filing Status

Confirm that your filing status (single, married filing jointly, head of household, etc.) accurately reflects your marital status and family situation. Your filing status affects your standard deduction and tax bracket.

2.1.3. Dependents

Ensure all eligible dependents are listed correctly, as this can impact your eligibility for tax credits such as the Child Tax Credit and the Credit for Other Dependents.

Form 1040

Form 1040

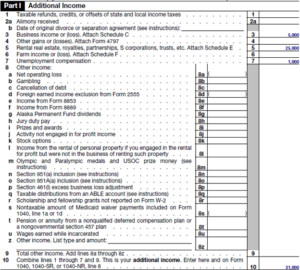

2.2. Schedule 1: Additional Income and Adjustments to Income

Schedule 1 is used to report income not included on Form 1040, such as business income, rental income, and unemployment compensation. It also includes adjustments to income, such as deductions for student loan interest and health savings account (HSA) contributions.

2.2.1. Business Income

If you have self-employment income or income from a side business, this is where you’ll report it. Accurate reporting of business income is essential for calculating your self-employment tax.

2.2.2. Rental Income

If you own rental properties, Schedule 1 is used to report your rental income and expenses. Keeping detailed records of your rental activities is crucial for accurate reporting.

2.2.3. Adjustments to Income

Common adjustments to income include deductions for contributions to a Health Savings Account (HSA), student loan interest, and alimony payments. These deductions can significantly reduce your adjusted gross income (AGI).

Schedule 1

Schedule 1

2.3. Schedule A: Itemized Deductions

Schedule A is used to itemize deductions, such as medical expenses, state and local taxes (SALT), and charitable contributions. Itemizing deductions can reduce your taxable income if your itemized deductions exceed the standard deduction.

2.3.1. Medical Expenses

You can deduct medical expenses that exceed 7.5% of your adjusted gross income (AGI). Keeping detailed records of your medical expenses is essential for claiming this deduction.

2.3.2. State and Local Taxes (SALT)

You can deduct state and local taxes, such as property taxes and either state income taxes or sales taxes, up to a limit of $10,000.

2.3.3. Charitable Contributions

You can deduct contributions to qualified charitable organizations. Make sure to keep records of your donations, including cash contributions, non-cash donations, and mileage driven for charitable purposes.

2.4. Schedule D: Capital Gains and Losses

Schedule D is used to report capital gains and losses from the sale of stocks, bonds, and other capital assets. Understanding your capital gains and losses is crucial for effective tax planning and investment strategies.

2.4.1. Short-Term vs. Long-Term Capital Gains

Short-term capital gains (assets held for one year or less) are taxed at your ordinary income tax rate, while long-term capital gains (assets held for more than one year) are taxed at lower rates.

2.4.2. Capital Loss Deductions

If your capital losses exceed your capital gains, you can deduct up to $3,000 of the excess loss each year. Any remaining losses can be carried forward to future years.

2.5. Form W-2: Wage and Tax Statement

Form W-2 reports your wages, salaries, and other compensation paid to you by your employer, as well as the amount of taxes withheld from your paychecks.

2.5.1. Verifying Income and Withholdings

Ensure that the income and tax withholdings reported on your W-2 are accurate. If you notice any discrepancies, contact your employer to request a corrected form.

2.5.2. Understanding Box Codes

Familiarize yourself with the various box codes on Form W-2, as they provide important information about your compensation and benefits.

2.6. Form 1099: Information Returns

Form 1099 reports various types of income you may have received, such as interest, dividends, and non-employee compensation.

2.6.1. Types of 1099 Forms

There are several types of 1099 forms, including 1099-INT (interest income), 1099-DIV (dividend income), 1099-NEC (non-employee compensation), and 1099-R (distributions from retirement accounts).

2.6.2. Reporting Income

Make sure to report all income reported on Form 1099 on your tax return. Failure to do so can result in penalties from the IRS.

3. Understanding Key Sections of Form 1040

Form 1040 is the cornerstone of your tax return. Let’s break down the key sections to help you understand what each part signifies.

3.1. Income

Lines 1-9 of Form 1040 are used to report your income sources for the year.

3.1.1. Line 1: Wages, Salaries, and Tips

This line reports your taxable wages from Form W-2, as well as income from deferred compensation payments and employer equity awards.

3.1.2. Line 2: Interest Income

This line reports interest income, including tax-exempt interest (typically from municipal bonds) and taxable interest from savings accounts, money markets, and bonds.

3.1.3. Line 3: Dividend Income

This line reports dividend income, including qualified dividends (taxed at lower rates) and total dividends.

3.1.4. Line 4: IRA Distributions

This line reports distributions from traditional IRAs, with the taxable amount depending on whether the contributions were pre-tax or after-tax.

3.1.5. Line 5: Pensions and Annuities

This line reports distributions from qualified employer retirement plans, such as 401(k)s, 403(b)s, and pensions, as well as distributions from annuities.

3.1.6. Line 6: Social Security Benefits

This line reports Social Security benefit payments, with the taxable amount depending on your other income.

3.1.7. Line 7: Capital Gains or Losses

This line reports your net capital gain or loss from the sale of stocks, bonds, and other capital assets.

3.1.8. Line 8: Other Income

This line reports other income not included on lines 1-7, such as rental income, royalties, and unemployment compensation.

3.1.9. Line 9: Total Income

This line is the sum of all income reported on lines 1-8.

3.2. Adjusted Gross Income (AGI)

Lines 10-11 of Form 1040 calculate your Adjusted Gross Income (AGI), which is your gross income less certain deductions.

3.2.1. Line 10: Adjustments to Income

This line includes deductions such as contributions to a Health Savings Account (HSA), student loan interest, and self-employment tax.

3.2.2. Line 11: Adjusted Gross Income (AGI)

This line is your gross income (Line 9) less adjustments to income (Line 10). AGI is an important number used for many purposes, including determining eligibility for certain deductions and credits.

3.3. Taxable Income

Lines 12-15 of Form 1040 calculate your taxable income, which is your AGI less your standard deduction or itemized deductions, and the qualified business income (QBI) deduction.

3.3.1. Line 12: Standard Deduction or Itemized Deductions

This line lists either the standard deduction (which varies based on your filing status) or your itemized deductions (if you choose to itemize).

3.3.2. Line 13: Qualified Business Income (QBI) Deduction

This line is used if you had a deduction for Qualified Business Income (QBI) from a pass-through entity, such as a partnership, S corporation, or sole proprietorship.

3.3.3. Line 15: Taxable Income

This line is your AGI (Line 11) less your standard deduction or itemized deductions (Line 12), and the QBI deduction (Line 13). Your taxable income is the amount used to calculate your tax liability.

3.4. Tax Liability

Lines 16-24 of Form 1040 calculate your tax liability, which is the amount of tax you owe based on your taxable income.

3.4.1. Line 16: Tax

This line is the amount of tax you owe based on your taxable income. The tax is calculated using the applicable tax rates for your filing status and income level.

3.4.2. Line 17: Other Taxes

This line includes other taxes such as self-employment tax, the additional tax on tax-favored accounts (10% early withdrawal penalty), and the 3.8% Medicare surtax on net investment income.

3.4.3. Line 24: Total Tax

This line is the total amount of your tax liability for the year.

3.5. Payments

Lines 25-33 of Form 1040 list the tax payments you made during the year, including withholdings from wages and estimated tax payments.

3.5.1. Line 25: Federal Income Tax Withheld

This line reports the amount of federal income tax withheld from your wages, salaries, and other compensation.

3.5.2. Line 26: Estimated Tax Payments

This line reports the amount of estimated tax payments you made during the year. Estimated tax payments are typically made by self-employed individuals and those with significant investment income.

3.5.3. Line 33: Total Payments

This line is the total of your tax payments made during the year.

3.6. Refund or Amount You Owe

Lines 34-38 of Form 1040 determine whether you are entitled to a refund or owe additional tax.

3.6.1. Line 34: Overpaid

If your tax payments (Line 33) exceed your total tax (Line 24), you are entitled to a refund. This line shows the amount of your refund.

3.6.2. Line 37: Amount You Owe

If your tax payments (Line 33) are less than your total tax (Line 24), you owe additional tax. This line shows the amount you owe.

3.6.3. Line 38: Estimated Tax Penalty

If you did not pay enough tax during the year, you may owe an underpayment penalty. This line shows the amount of the penalty.

4. Maximizing Deductions and Credits

One of the key benefits of understanding your tax return is the ability to identify deductions and credits that can reduce your tax liability. Here’s how to maximize these opportunities:

4.1. Itemizing Deductions

Decide whether to take the standard deduction or itemize. Itemizing is beneficial if your deductions exceed the standard deduction amount. Common itemized deductions include:

- Medical expenses exceeding 7.5% of your AGI

- State and local taxes (SALT) up to $10,000

- Home mortgage interest

- Charitable contributions

4.2. Taking Advantage of Tax Credits

Tax credits reduce your tax liability dollar-for-dollar and can be more valuable than deductions. Common tax credits include:

- Child Tax Credit

- Earned Income Tax Credit (EITC)

- Child and Dependent Care Credit

- Education Credits (American Opportunity Credit and Lifetime Learning Credit)

- Energy Credits

4.3. Utilizing Retirement Contributions

Contributing to retirement accounts not only helps you save for the future but also provides tax benefits. Traditional IRA and 401(k) contributions are often tax-deductible, reducing your taxable income.

4.4. Leveraging Health Savings Accounts (HSAs)

If you have a high-deductible health insurance plan, contributing to an HSA can provide tax advantages. Contributions are tax-deductible, earnings grow tax-free, and withdrawals for qualified medical expenses are tax-free.

5. Strategic Partnerships for Income Growth

Your tax return can reveal opportunities for strategic partnerships that can help you grow your income and optimize your tax situation. Here are some potential partnership opportunities to consider:

5.1. Real Estate Investments

Partnering with real estate professionals can provide opportunities to invest in rental properties, which can generate rental income and provide tax deductions for expenses such as mortgage interest, property taxes, and depreciation.

5.2. Business Ventures

Collaborating with other entrepreneurs can provide opportunities to start or expand a business, which can generate additional income and provide tax deductions for business expenses.

5.3. Investment Partnerships

Partnering with financial advisors and investment professionals can provide opportunities to invest in tax-advantaged investments, such as municipal bonds, which offer tax-exempt interest income.

5.4. Affiliate Marketing

Partnering with businesses to promote their products or services can generate affiliate income, which can supplement your existing income and provide tax deductions for marketing expenses.

According to Harvard Business Review, strategic partnerships can significantly increase revenue and market share for businesses of all sizes.

6. Common Mistakes To Avoid

Filing taxes accurately is essential to avoid penalties and ensure you receive the maximum refund possible. Here are some common mistakes to avoid:

6.1. Incorrect Social Security Numbers

Double-check the Social Security numbers (SSNs) for yourself, your spouse, and your dependents. Incorrect SSNs can lead to processing delays or rejection of your return.

6.2. Filing Status Errors

Make sure to choose the correct filing status based on your marital status and family situation. Choosing the wrong filing status can result in a higher tax liability.

6.3. Missing Deductions and Credits

Take the time to identify all deductions and credits you are eligible to claim. Missing deductions and credits can result in a lower refund or a higher tax liability.

6.4. Math Errors

Double-check all calculations on your tax return. Math errors can result in processing delays and inaccurate tax liabilities.

6.5. Failing to Report All Income

Report all income you received during the year, including wages, salaries, interest, dividends, and self-employment income. Failing to report all income can result in penalties from the IRS.

6.6. Not Keeping Adequate Records

Keep detailed records of your income, deductions, and credits. Adequate records are essential for preparing an accurate tax return and supporting your claims in case of an audit.

7. Seeking Professional Assistance

While understanding your tax return is essential, seeking professional assistance from a qualified tax advisor can provide additional benefits. Here’s why you might consider seeking professional help:

7.1. Complex Tax Situations

If you have a complex tax situation, such as self-employment income, rental income, or significant investment income, a tax advisor can help you navigate the complexities of the tax code and ensure you are taking advantage of all available deductions and credits.

7.2. Time Savings

Preparing your tax return can be time-consuming, especially if you have a complex tax situation. A tax advisor can save you time by preparing your tax return for you.

7.3. Accuracy

A tax advisor can help ensure your tax return is accurate and complete, reducing the risk of errors and penalties.

7.4. Tax Planning

A tax advisor can provide tax planning advice to help you minimize your tax liability and maximize your financial well-being.

According to Entrepreneur.com, working with a tax professional can lead to significant tax savings and improved financial outcomes.

8. Navigating Tax Law Changes

Tax laws are subject to change, which can impact your tax liability and financial planning strategies. Staying informed about tax law changes is essential for making informed decisions about your finances. Here are some resources for staying up-to-date on tax law changes:

8.1. IRS Website

The IRS website (www.irs.gov) provides information about tax law changes, as well as tax forms, publications, and other resources.

8.2. Tax Publications

Tax publications, such as those published by CCH and Thomson Reuters, provide in-depth analysis of tax law changes and their implications.

8.3. Tax Professionals

Tax professionals, such as CPAs and tax attorneys, can provide personalized advice about how tax law changes impact your specific tax situation.

9. Real-Life Examples of Income-Boosting Partnerships

To illustrate the potential of strategic partnerships, let’s look at a few real-life examples:

9.1. The Real Estate Investor and Property Manager

A real estate investor partners with a property manager to handle the day-to-day operations of their rental properties. This partnership allows the investor to focus on acquiring new properties, while the property manager ensures the properties are well-maintained and generate consistent rental income.

9.2. The E-commerce Entrepreneur and Marketing Agency

An e-commerce entrepreneur partners with a marketing agency to promote their products online. This partnership allows the entrepreneur to reach a wider audience and increase sales, while the marketing agency earns a commission on each sale.

9.3. The Financial Advisor and Insurance Agent

A financial advisor partners with an insurance agent to provide comprehensive financial planning services to their clients. This partnership allows the financial advisor to offer insurance products, while the insurance agent can offer investment advice.

10. Income-Partners.Net: Your Gateway to Strategic Alliances

At income-partners.net, we understand the power of strategic partnerships in driving income growth and financial success. We provide a platform for individuals and businesses to connect, collaborate, and create mutually beneficial relationships.

10.1. Discovering Partnership Opportunities

Our website features a wide range of partnership opportunities across various industries, including real estate, business ventures, and investment partnerships.

10.2. Building Effective Relationships

We provide resources and tools to help you build effective relationships with potential partners, including tips for networking, communication, and negotiation.

10.3. Maximizing Your Income Potential

Our goal is to help you maximize your income potential by connecting you with partners who can help you achieve your financial goals.

Ready to explore the world of strategic partnerships? Visit income-partners.net today and unlock your income potential.

Address: 1 University Station, Austin, TX 78712, United States.

Phone: +1 (512) 471-3434.

Website: income-partners.net.

FAQ: Your Income Tax Return Questions Answered

1. What is the purpose of Form 1040?

Form 1040 is the primary form used to calculate your federal income tax liability. It summarizes your income, deductions, and credits for the year.

2. How do I determine my filing status?

Your filing status depends on your marital status and family situation. Common filing statuses include single, married filing jointly, married filing separately, head of household, and qualifying widow(er).

3. What is the standard deduction?

The standard deduction is a set amount that you can deduct from your adjusted gross income (AGI) to reduce your taxable income. The amount of the standard deduction varies based on your filing status.

4. When should I itemize deductions?

You should itemize deductions if your itemized deductions exceed the standard deduction amount. Common itemized deductions include medical expenses, state and local taxes, and charitable contributions.

5. What is the difference between a tax deduction and a tax credit?

A tax deduction reduces your taxable income, while a tax credit reduces your tax liability dollar-for-dollar. Tax credits are generally more valuable than tax deductions.

6. How can I reduce my tax liability?

You can reduce your tax liability by taking advantage of deductions, credits, and other tax planning strategies. Common tax planning strategies include contributing to retirement accounts, leveraging health savings accounts (HSAs), and investing in tax-advantaged investments.

7. What should I do if I receive a notice from the IRS?

If you receive a notice from the IRS, it’s important to respond promptly. Read the notice carefully and follow the instructions provided. If you have questions or concerns, contact the IRS or seek assistance from a tax professional.

8. What are the penalties for filing taxes late?

The penalty for filing taxes late is typically 5% of the unpaid taxes for each month or part of a month that your return is late, up to a maximum of 25% of your unpaid taxes.

9. How long should I keep my tax records?

The IRS recommends keeping your tax records for at least three years from the date you filed your return or two years from the date you paid the tax, whichever is later.

10. Where can I find more information about taxes?

You can find more information about taxes on the IRS website (www.irs.gov), as well as in tax publications and from tax professionals.

By understanding your income tax return and exploring strategic partnership opportunities, you can unlock your income potential and achieve your financial goals. Visit income-partners.net to start your journey toward financial success today.