Are you feeling overwhelmed by your income tax return? Understanding how to read an income tax return is crucial for financial planning and making informed decisions about potential partnership opportunities that can boost your income, which is what we at income-partners.net aim to help you with. By demystifying the process, you can better understand your financial situation and leverage strategies like tax-advantaged investments and business partnerships. This detailed guide covers everything from Form 1040 to key schedules, offering tax insights and strategies for financial growth, including exploring strategic collaborations for enhanced income streams.

1. Why Is Understanding Your Tax Return Important?

Understanding your tax return is more than just knowing whether you owe money or are getting a refund. It’s about gaining insight into your financial health, identifying potential tax-saving opportunities, and making informed decisions that can impact your income and investment strategies. It also helps ensure accuracy and compliance, preventing potential issues with the IRS.

Here’s why it matters:

- Financial Awareness: Provides a clear snapshot of your income, deductions, and tax liabilities.

- Tax Planning: Helps you identify opportunities to reduce your tax burden through strategic planning.

- Accuracy and Compliance: Ensures that your return is accurate and compliant with tax laws, minimizing the risk of penalties or audits.

- Informed Decision-Making: Empowers you to make better financial decisions related to investments, business partnerships, and other income-generating activities.

- Partnership Insights: Understanding your tax situation can help you identify potential areas where partnerships can provide financial benefits.

2. What Are the Key Components of an Income Tax Return?

An income tax return consists of several forms and schedules, each providing specific details about your financial situation. The main form is Form 1040, which summarizes your income, deductions, credits, and tax liability. Supporting schedules provide additional information and calculations that feed into Form 1040.

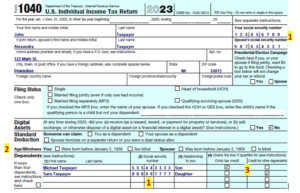

2.1. Form 1040: U.S. Individual Income Tax Return

Form 1040 is the primary form used to calculate your income tax liability. It gathers information about your income sources, deductions, and credits to determine whether you owe taxes or are entitled to a refund.

- Personal Information: Includes your name, Social Security number, address, and filing status.

- Income: Reports various sources of income, such as wages, salaries, interest, dividends, and business income.

- Adjustments to Income: Deductions that reduce your gross income, such as contributions to health savings accounts (HSAs) and student loan interest payments.

- Deductions: Either the standard deduction or itemized deductions, whichever is greater.

- Tax Credits: Reduce your tax liability and can be either refundable or nonrefundable.

- Tax Payments: Includes amounts withheld from your paycheck, estimated tax payments, and prior-year overpayments applied to the current tax year.

- Refund or Amount Owed: Indicates whether you are due a refund or owe additional taxes.

Form 1040 Sample

Form 1040 Sample

2.2. Schedule 1: Additional Income and Adjustments to Income

Schedule 1 is used to report additional income not included on Form 1040, as well as certain deductions that reduce your gross income. This form is essential for self-employed individuals and those with various income sources.

- Additional Income: Includes income from sources like self-employment, rental properties, unemployment compensation, and alimony.

- Adjustments to Income: Deductions such as contributions to health savings accounts (HSAs), self-employment tax, student loan interest, and alimony paid.

2.3. Schedule A: Itemized Deductions

Schedule A is used to list itemized deductions, which can reduce your taxable income if they exceed the standard deduction. Common itemized deductions include medical expenses, state and local taxes (SALT), and charitable contributions.

- Medical Expenses: Deductible medical expenses exceeding 7.5% of your adjusted gross income (AGI).

- State and Local Taxes (SALT): Limited to $10,000 per household, including property taxes, state and local income taxes, or sales taxes.

- Charitable Contributions: Donations to qualified charitable organizations, subject to certain limitations based on your AGI.

2.4. Schedule D: Capital Gains and Losses

Schedule D is used to report capital gains and losses from the sale of stocks, bonds, and other capital assets. These gains and losses are classified as either short-term (held for one year or less) or long-term (held for more than one year), with different tax rates applying to each.

- Short-Term Capital Gains and Losses: Result from assets held for one year or less, taxed at your ordinary income tax rate.

- Long-Term Capital Gains and Losses: Result from assets held for more than one year, taxed at preferential rates, generally lower than ordinary income tax rates.

2.5. Schedule E: Supplemental Income and Loss

Schedule E is used to report income or loss from rental real estate, partnerships, S corporations, estates, and trusts. This schedule provides a detailed breakdown of income and expenses associated with these activities.

- Rental Real Estate: Income and expenses from rental properties, including rental income, mortgage interest, property taxes, and depreciation.

- Partnerships and S Corporations: Your share of income, deductions, and credits from partnerships and S corporations.

2.6. Other Important Forms

Depending on your financial situation, you may need to file other forms and schedules in addition to the ones listed above. Some common examples include:

- Form W-2: Reports wages, salaries, and other compensation paid to employees.

- Form 1099-INT: Reports interest income.

- Form 1099-DIV: Reports dividend income.

- Form 1099-R: Reports distributions from retirement accounts.

- Form 1099-NEC: Reports payments to independent contractors.

- Form SSA-1099: Reports Social Security benefits.

3. Understanding Form 1040: A Detailed Walkthrough

Form 1040 is the foundation of your tax return. Understanding each section of this form is crucial for accurately reporting your income, deductions, and credits.

3.1. Personal Information

The top section of Form 1040 collects your personal information, including your name, Social Security number, address, and filing status.

- Name and Social Security Number (SSN): Ensure this information is accurate to avoid processing delays or rejection of your return.

- Address: Use your current address to receive important correspondence from the IRS.

- Filing Status: Choose the filing status that best describes your situation, such as single, married filing jointly, married filing separately, head of household, or qualifying widow(er). Your filing status affects your standard deduction, tax brackets, and eligibility for certain credits and deductions.

3.2. Income Section (Lines 1-9)

This section reports various sources of income, including wages, salaries, interest, dividends, and retirement distributions.

- Line 1: Wages, Salaries, Tips, etc.: Report your taxable wages from Form W-2.

- Line 2a: Tax-Exempt Interest: Report tax-exempt interest, typically from municipal bonds. This interest is not taxable under regular tax calculations but may affect your liability under the Alternative Minimum Tax (AMT) or your Medicare premium.

- Line 2b: Taxable Interest: Report taxable interest from sources like savings accounts, CDs, and bonds.

- Line 3a: Qualified Dividends: Report qualified dividends, which are taxed at lower rates.

- Line 3b: Ordinary Dividends: Report total dividends, including those that are not qualified.

- Line 4a: IRA Distributions: Report the gross amount of distributions from your IRA.

- Line 4b: Taxable Amount: Report the taxable portion of your IRA distributions. If you made a qualified charitable distribution (QCD), ensure the QCD amount is correctly excluded from this line.

- Line 5a: Pensions and Annuities: Report the gross amount of distributions from pensions and annuities.

- Line 5b: Taxable Amount: Report the taxable portion of your pension and annuity distributions.

- Line 6a: Social Security Benefits: Report the gross amount of Social Security benefits received.

- Line 6b: Taxable Amount: Report the taxable portion of your Social Security benefits. The amount of Social Security benefits subject to tax depends on your total income.

- Line 7: Capital Gain or (Loss): Report your net capital gain or loss from Schedule D. This reflects gains and losses from the sale of stocks, bonds, and other capital assets.

- Line 8: Other Income: Report other sources of income, such as rental income, royalties, and business income.

- Line 9: Total Income: This is the sum of all income items reported on lines 1 through 8.

3.3. Adjusted Gross Income (AGI) (Lines 10-11)

This section calculates your adjusted gross income (AGI), which is your gross income less certain deductions. AGI is an important figure used to determine eligibility for various tax deductions and credits.

- Line 10: Adjustments to Income: Report deductions such as contributions to health savings accounts (HSAs), student loan interest payments, and self-employment tax.

- Line 11: Adjusted Gross Income: This is your gross income (line 9) less adjustments to income (line 10).

3.4. Taxable Income (Lines 12-15)

This section calculates your taxable income, which is the amount subject to income tax.

- Line 12a: Standard Deduction or Itemized Deductions: Enter the amount of your standard deduction or itemized deductions from Schedule A, whichever is greater. The standard deduction varies based on your filing status and is adjusted annually for inflation.

- Line 13: Qualified Business Income (QBI) Deduction: If you are a small business owner, you may be eligible for the QBI deduction, which allows you to deduct up to 20% of your qualified business income.

- Line 15: Taxable Income: This is your AGI (line 11) less the standard deduction or itemized deductions (line 12a) and the QBI deduction (line 13).

3.5. Tax and Credits (Lines 16-24)

This section calculates your tax liability and any tax credits you are eligible to claim.

- Line 16: Tax: Calculate your tax liability based on your taxable income (line 15) using the appropriate tax rates for your filing status. This can be done manually or using tax preparation software.

- Line 17: Alternative Minimum Tax (AMT): If you are subject to the AMT, include the amount from Schedule 2.

- Line 18: Excess Advance Premium Tax Credit Repayment: If you received advance payments of the premium tax credit for health insurance purchased through the Marketplace, you may need to repay some or all of the excess amount.

- Line 19: Child Tax Credit or Credit for Other Dependents: If you have qualifying children or other dependents, you may be eligible for the child tax credit or the credit for other dependents.

- Line 20: Other Credits from Schedule 3: Report any other tax credits you are eligible to claim from Schedule 3.

- Line 23: Other Taxes: Include other taxes, such as self-employment tax, additional tax on IRAs, and household employment taxes.

- Line 24: Total Tax: This is the sum of all tax amounts reported on lines 16 through 23.

3.6. Payments (Lines 25-33)

This section reports the amount of tax you have already paid through withholding, estimated tax payments, and refundable credits.

- Line 25a: Federal Income Tax Withheld from Forms W-2 and 1099: Report the amount of federal income tax withheld from your wages and other income.

- Line 25b: Federal Income Tax Withheld from all other forms (1099, etc.): Report the amount of federal income tax withheld from other sources, such as retirement distributions and Social Security benefits.

- Line 26: Estimated Tax Payments: Report the amount of estimated tax payments you made during the year.

- Line 27: Excess Social Security and Tier 1 RRTA Tax Withheld: If you had more than one employer and your total Social Security and Tier 1 RRTA taxes withheld exceeded the annual limit, you may be able to claim a credit for the excess amount.

- Line 28: Refundable Credits from Schedule 3: Report any refundable tax credits you are eligible to claim from Schedule 3.

- Line 32: Amount Paid with Request for Extension to File: If you requested an extension to file your tax return and made a payment with your request, include the amount paid.

- Line 33: Total Payments: This is the sum of all payments reported on lines 25a through 32.

3.7. Refund or Amount You Owe (Lines 34-38)

This section calculates whether you are due a refund or owe additional taxes.

- Line 34: Overpaid: If your total payments (line 33) exceed your total tax (line 24), you have overpaid your taxes and are due a refund.

- Line 35a: Amount of Overpayment to be Refunded to You: Enter the amount of your overpayment that you want to be refunded to you.

- Line 36: Amount of Overpayment to be Applied to Your 2024 Estimated Tax: Enter the amount of your overpayment that you want to be applied to your 2024 estimated tax.

- Line 37: Amount You Owe: If your total tax (line 24) exceeds your total payments (line 33), you owe additional taxes.

- Line 38: Estimated Tax Penalty: If you did not pay enough tax during the year, you may owe an estimated tax penalty.

4. Key Schedules and Their Impact

Understanding the schedules that accompany Form 1040 is crucial for a comprehensive view of your tax situation. These schedules provide detailed information on various aspects of your income, deductions, and credits.

4.1. Schedule 1: Additional Income and Adjustments to Income

Schedule 1 reports income not included on Form 1040 and adjustments that reduce your gross income, impacting your AGI.

- Business Income or Loss (Schedule C): Income or loss from a business you operated as a sole proprietor.

- Rental Real Estate, Royalties, Partnerships, S Corporations, Trusts, etc. (Schedule E): Income or loss from these sources.

- Other Income: Including unemployment compensation, gambling winnings, and cancellation of debt.

- Adjustments to Income: Deductions that can significantly lower your AGI, such as contributions to a Health Savings Account (HSA), self-employment tax, and student loan interest.

4.2. Schedule A: Itemized Deductions

Schedule A allows you to claim itemized deductions, reducing your taxable income if they exceed the standard deduction.

- Medical and Dental Expenses: Deductible expenses exceeding 7.5% of your AGI.

- State and Local Taxes (SALT): Limited to $10,000, including property taxes and state and local income or sales taxes.

- Home Mortgage Interest: Deductible interest on home loans.

- Charitable Contributions: Donations to qualified charitable organizations.

4.3. Schedule C: Profit or Loss from Business (Sole Proprietorship)

Schedule C is used by sole proprietors to report income and expenses from their business.

- Gross Receipts or Sales: Total income from your business.

- Business Expenses: Including costs for goods sold, salaries, rent, and depreciation.

- Net Profit or Loss: Calculated by subtracting total expenses from gross income.

4.4. Schedule D: Capital Gains and Losses

Schedule D reports gains and losses from the sale of capital assets.

- Short-Term Capital Gains and Losses: From assets held for one year or less.

- Long-Term Capital Gains and Losses: From assets held for more than one year, often taxed at lower rates.

4.5. Schedule E: Supplemental Income and Loss

Schedule E reports income and losses from rental real estate, partnerships, S corporations, estates, and trusts.

- Rental Income and Expenses: Income from rental properties, including rental income, mortgage interest, property taxes, and depreciation.

- Income or Loss from Partnerships and S Corporations: Your share of income, deductions, and credits from these entities.

5. Common Tax Situations and Their Implications

Different tax situations can significantly impact your tax liability and financial planning. Here are a few common scenarios and their implications.

5.1. Self-Employment Income

If you are self-employed, you need to report your income and expenses on Schedule C. You will also need to pay self-employment tax, which covers both Social Security and Medicare taxes.

- Self-Employment Tax: The combined tax rate for Social Security and Medicare is 15.3%. You can deduct one-half of your self-employment tax from your gross income.

- Business Expenses: Deductible expenses can significantly reduce your taxable income.

- Qualified Business Income (QBI) Deduction: May be eligible to deduct up to 20% of your qualified business income.

5.2. Investment Income

Investment income, such as dividends and capital gains, is reported on Schedule B and Schedule D.

- Dividends: Qualified dividends are taxed at lower rates than ordinary income.

- Capital Gains: Long-term capital gains are generally taxed at lower rates than short-term gains.

- Capital Losses: Can be used to offset capital gains, with any excess losses deductible up to $3,000 per year.

5.3. Retirement Income

Distributions from retirement accounts, such as 401(k)s and IRAs, are reported on Form 1099-R and Form 1040.

- Taxable Distributions: Distributions from traditional retirement accounts are generally taxable as ordinary income.

- Qualified Distributions: Distributions from Roth IRAs are generally tax-free if certain conditions are met.

- Required Minimum Distributions (RMDs): Individuals age 73 or older must take RMDs from their retirement accounts, which are taxable.

5.4. Rental Income

If you own rental properties, you need to report your rental income and expenses on Schedule E.

- Rental Income: Total income from rental properties.

- Rental Expenses: Including mortgage interest, property taxes, insurance, and depreciation.

- Depreciation: A non-cash expense that allows you to deduct a portion of the cost of the property over its useful life.

6. Tax Planning Tips for Individuals and Businesses

Effective tax planning can help you minimize your tax liability and maximize your financial well-being. Here are some tax planning tips for individuals and businesses.

6.1. Maximize Retirement Contributions

Contributing to retirement accounts can provide significant tax benefits.

- 401(k) Plans: Contribute to a 401(k) plan to reduce your taxable income and save for retirement.

- Traditional IRAs: Contributions may be tax-deductible, depending on your income and whether you are covered by a retirement plan at work.

- Roth IRAs: Contributions are not tax-deductible, but qualified distributions are tax-free in retirement.

6.2. Take Advantage of Tax Credits

Tax credits can directly reduce your tax liability.

- Child Tax Credit: For qualifying children under age 17.

- Earned Income Tax Credit (EITC): For low- to moderate-income individuals and families.

- Education Credits: Such as the American Opportunity Tax Credit and the Lifetime Learning Credit, for eligible education expenses.

6.3. Itemize Deductions When Possible

If your itemized deductions exceed the standard deduction, itemizing can reduce your taxable income.

- Medical Expenses: Keep track of medical expenses that exceed 7.5% of your AGI.

- Charitable Contributions: Donate to qualified charitable organizations and keep records of your donations.

- State and Local Taxes (SALT): Maximize your SALT deductions, subject to the $10,000 limit.

6.4. Utilize Tax-Loss Harvesting

Tax-loss harvesting involves selling investments that have decreased in value to offset capital gains.

- Offset Capital Gains: Use capital losses to offset capital gains, reducing your tax liability.

- Deduct Excess Losses: If your capital losses exceed your capital gains, you can deduct up to $3,000 of the excess losses per year.

6.5. Consider a Health Savings Account (HSA)

If you have a high-deductible health insurance plan, consider contributing to an HSA.

- Tax-Deductible Contributions: Contributions to an HSA are tax-deductible.

- Tax-Free Growth: Earnings in an HSA grow tax-free.

- Tax-Free Withdrawals: Withdrawals for qualified medical expenses are tax-free.

6.6. Business Owners: Maximize Deductions

If you own a business, maximize your deductible expenses to reduce your taxable income.

- Business Expenses: Deductible expenses include costs for goods sold, salaries, rent, and depreciation.

- Home Office Deduction: If you use a portion of your home exclusively for business, you may be able to deduct home-related expenses.

- Qualified Business Income (QBI) Deduction: May be eligible to deduct up to 20% of your qualified business income.

7. Resources for Further Learning

Navigating the complexities of tax returns can be challenging. Fortunately, numerous resources are available to help you better understand your tax obligations and plan effectively.

7.1. IRS Website

The IRS website (www.irs.gov) is a comprehensive resource for tax information.

- Forms and Publications: Access to all IRS forms and publications.

- Tax Information: Detailed information on various tax topics.

- Online Tools: Including calculators and interactive guides.

7.2. Tax Preparation Software

Tax preparation software can help you prepare and file your tax return accurately.

- User-Friendly Interface: Guides you through the tax preparation process step-by-step.

- Error Checking: Helps you identify and correct errors on your return.

- E-Filing: Allows you to electronically file your return with the IRS.

7.3. Tax Professionals

Consulting with a tax professional can provide personalized advice and guidance.

- Certified Public Accountants (CPAs): Can help you with tax planning and preparation.

- Enrolled Agents (EAs): Licensed by the IRS to represent taxpayers before the IRS.

- Tax Attorneys: Can provide legal advice on tax matters.

7.4. Educational Resources

Various educational resources can help you learn more about taxes.

- Online Courses: Offered by universities and professional organizations.

- Seminars and Workshops: Provided by local community centers and tax professionals.

- Books and Articles: Available at libraries and online.

8. Potential Partnership Opportunities to Boost Income

Understanding your income tax return can also help you identify areas where partnerships can provide financial benefits. At income-partners.net, we specialize in connecting individuals and businesses to create mutually beneficial collaborations.

8.1. Strategic Alliances

Partnering with complementary businesses can expand your market reach and increase your revenue.

- Joint Ventures: Collaborating on specific projects to share resources and expertise.

- Marketing Partnerships: Cross-promoting products or services to reach new customers.

8.2. Investment Partnerships

Pooling resources with other investors can provide access to larger investment opportunities.

- Real Estate Partnerships: Investing in real estate projects together to share the costs and risks.

- Venture Capital Partnerships: Investing in startup companies with high growth potential.

8.3. Distribution Partnerships

Partnering with distributors can expand your product distribution network.

- Wholesale Partnerships: Selling your products through wholesale distributors to reach retailers.

- Retail Partnerships: Selling your products in retail stores to reach consumers directly.

8.4. Service Partnerships

Collaborating with service providers can enhance your service offerings and increase customer satisfaction.

- Technology Partnerships: Integrating your services with technology providers to offer innovative solutions.

- Consulting Partnerships: Partnering with consultants to provide specialized expertise to clients.

8.5. Tax Benefits of Partnerships

Engaging in strategic partnerships can also provide tax benefits.

- Pass-Through Taxation: Income from partnerships is typically taxed at the individual partner level, avoiding double taxation.

- Deductible Expenses: Expenses incurred through partnerships are generally deductible, reducing taxable income.

- Tax Credits: Partners may be eligible for various tax credits, depending on the nature of the partnership.

8.6. How income-partners.net Can Help

At income-partners.net, we provide a platform to connect with potential partners, explore collaboration opportunities, and access resources to help you build successful partnerships.

- Networking Opportunities: Connect with individuals and businesses seeking partnership opportunities.

- Partnership Resources: Access to tools and resources to help you structure and manage partnerships.

- Expert Advice: Guidance from experienced professionals on partnership strategies and tax implications.

9. Real-World Examples of Successful Partnerships

Examining real-world examples can provide valuable insights into the benefits of strategic partnerships.

9.1. Starbucks and Spotify

Starbucks partnered with Spotify to integrate music into its coffee shops, enhancing the customer experience and promoting Spotify’s music streaming service.

9.2. Apple and Nike

Apple and Nike collaborated to create the Nike+iPod Sport Kit, which allowed runners to track their workouts using their iPods, combining technology and fitness.

9.3. Uber and Spotify

Uber and Spotify partnered to allow Uber riders to control the music in their Uber rides, enhancing the ride experience and promoting Spotify’s music streaming service.

9.4. Airbnb and Flipboard

Airbnb and Flipboard partnered to provide travel inspiration and booking options directly within Flipboard’s magazine-style app.

These examples demonstrate how strategic partnerships can create mutually beneficial outcomes and enhance the value proposition for customers.

10. Frequently Asked Questions (FAQs) about Income Tax Returns

10.1. What is the standard deduction for 2023?

The standard deduction for 2023 varies depending on your filing status:

- Single: $13,850

- Married Filing Jointly: $27,700

- Head of Household: $20,800

10.2. What is the deadline for filing my tax return?

The deadline for filing your tax return is typically April 15th of each year. If you need more time, you can request an extension to file by October 15th.

10.3. How do I file an amended tax return?

To file an amended tax return, use Form 1040-X, Amended U.S. Individual Income Tax Return.

10.4. What is the difference between a tax credit and a tax deduction?

A tax credit directly reduces your tax liability, while a tax deduction reduces your taxable income.

10.5. How do I calculate my capital gains and losses?

Capital gains and losses are calculated by subtracting the basis (cost) of an asset from the sale price.

10.6. What is the Qualified Business Income (QBI) deduction?

The QBI deduction allows eligible self-employed individuals and small business owners to deduct up to 20% of their qualified business income.

10.7. What are the tax implications of working remotely?

If you work remotely, your tax obligations may depend on where you live and where your employer is located. You may need to pay taxes in both states.

10.8. How can I reduce my tax liability as a business owner?

As a business owner, you can reduce your tax liability by maximizing deductible expenses, taking advantage of tax credits, and utilizing tax-advantaged retirement plans.

10.9. What is the Alternative Minimum Tax (AMT)?

The Alternative Minimum Tax (AMT) is a separate tax system that applies to high-income individuals and corporations that take advantage of certain tax breaks.

10.10. Where can I find help preparing my tax return?

You can find help preparing your tax return from tax professionals, tax preparation software, and the IRS website.

Understanding how to read an income tax return is essential for effective financial planning and making informed decisions. By familiarizing yourself with the key components of Form 1040 and related schedules, you can gain valuable insights into your financial situation and identify opportunities to reduce your tax liability. Additionally, exploring strategic partnership opportunities can further enhance your income and financial well-being. Visit income-partners.net to discover how we can help you connect with potential partners and unlock new avenues for growth. For further assistance, you can contact us at Address: 1 University Station, Austin, TX 78712, United States. Phone: +1 (512) 471-3434.