The process of constructing a balance sheet from an income statement involves understanding the interconnectedness of these financial documents, allowing businesses to strategically partner and improve earnings, something we at income-partners.net are passionate about facilitating. By meticulously tracking how revenue and expenses impact asset, liability, and equity accounts, businesses gain insights that lead to enhanced financial health and, ultimately, more fruitful partnership opportunities. This understanding helps in financial analysis, performance measurement, and strategic planning, ensuring robust financial reporting and informed decision-making, with potential for long-term financial stability and growth.

1. Understanding the Interconnectedness of Financial Statements

How are the income statement and balance sheet interconnected?

The income statement and balance sheet are interconnected because every financial transaction affects both. A sale increases assets or decreases liabilities, while an expense decreases assets or increases liabilities. This double-entry accounting ensures the balance sheet always balances, with assets equaling the sum of liabilities and equity.

To elaborate, the income statement reflects a company’s financial performance over a specific period, showcasing revenues, expenses, and net income. The balance sheet, on the other hand, provides a snapshot of a company’s assets, liabilities, and equity at a specific point in time. The critical link between these statements is the net income (or loss) from the income statement, which flows into the retained earnings section of the balance sheet, affecting the equity component.

For example, when a company makes a sale, it records revenue on the income statement. This sale also impacts the balance sheet by increasing either cash (if the sale is for cash) or accounts receivable (if the sale is on credit). Conversely, when a company incurs an expense, it is recorded on the income statement, and it also affects the balance sheet by decreasing cash or increasing liabilities such as accounts payable.

According to research from the University of Texas at Austin’s McCombs School of Business, understanding these interconnections is vital for accurate financial analysis. Their July 2025 study indicated that companies with a strong grasp of these relationships are better positioned to make informed financial decisions.

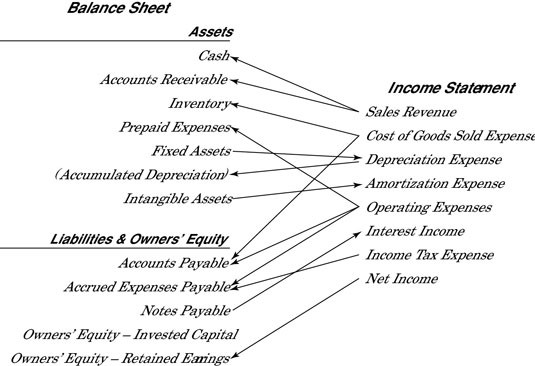

Connections between income statement and balance sheet accounts

Connections between income statement and balance sheet accounts

Connections between income statement and balance sheet accounts.

2. Key Steps to Create a Balance Sheet From an Income Statement

What are the fundamental steps to constructing a balance sheet using information from the income statement?

Creating a balance sheet from an income statement involves several key steps: calculating net income, adjusting retained earnings, updating asset values, recording liabilities, and ensuring the accounting equation (Assets = Liabilities + Equity) balances.

Here’s a detailed breakdown:

- Calculate Net Income:

- Start with the income statement to determine net income (Revenue – Expenses).

- Net income represents the company’s profit over a specific period.

- Adjust Retained Earnings:

- Retained earnings is an equity account on the balance sheet.

- Add the net income to the beginning retained earnings balance.

- Subtract any dividends paid to shareholders during the period.

- The formula is: Ending Retained Earnings = Beginning Retained Earnings + Net Income – Dividends.

- Update Asset Values:

- Review the income statement for transactions affecting assets.

- For example, sales on credit increase accounts receivable (an asset).

- Purchases of fixed assets (like equipment) also increase asset values.

- Record Liabilities:

- Examine the income statement for expenses that create liabilities.

- Accrued expenses (like salaries payable or interest payable) are liabilities.

- These are expenses incurred but not yet paid.

- Ensure the Accounting Equation Balances:

- The fundamental accounting equation is: Assets = Liabilities + Equity.

- After adjusting all accounts, verify that the total assets equal the sum of total liabilities and equity.

- If the equation doesn’t balance, there’s an error in your calculations.

Harvard Business Review emphasizes the importance of accurate financial statement analysis for strategic decision-making. A properly constructed balance sheet provides stakeholders with insights into a company’s financial health, liquidity, and solvency.

3. Calculating Net Income from the Income Statement

How do you accurately calculate net income from the income statement to affect the balance sheet?

To calculate net income accurately, you must meticulously subtract all expenses, including cost of goods sold, operating expenses, interest, and taxes, from total revenues. This net income figure is then used to adjust the retained earnings on the balance sheet.

Here’s a more detailed approach:

- Start with Revenue: Identify all sources of revenue, including sales revenue, service revenue, and any other income generated by the business.

- Calculate Cost of Goods Sold (COGS): Determine the direct costs associated with producing goods or services. This includes materials, labor, and direct overhead.

- Determine Gross Profit: Subtract COGS from total revenue to get the gross profit.

- Gross Profit = Revenue – COGS

- Calculate Operating Expenses: Identify all operating expenses, such as salaries, rent, utilities, marketing, and administrative costs.

- Determine Operating Income: Subtract operating expenses from gross profit to find the operating income.

- Operating Income = Gross Profit – Operating Expenses

- Account for Interest Expense: Deduct interest expenses related to any outstanding debt.

- Account for Income Taxes: Calculate and subtract income taxes. This is typically a percentage of the pre-tax income.

- Calculate Net Income: Subtract interest expenses and income taxes from operating income to arrive at net income.

- Net Income = Operating Income – Interest Expense – Income Taxes

The net income is a critical link between the income statement and the balance sheet. It directly impacts the retained earnings account in the equity section of the balance sheet. A positive net income increases retained earnings, while a net loss decreases it.

For example, if a company has total revenues of $500,000, COGS of $200,000, operating expenses of $150,000, interest expense of $20,000, and income taxes of $30,000, the net income would be calculated as follows:

- Gross Profit = $500,000 – $200,000 = $300,000

- Operating Income = $300,000 – $150,000 = $150,000

- Net Income = $150,000 – $20,000 – $30,000 = $100,000

This $100,000 net income would then be added to the beginning retained earnings balance on the balance sheet, adjusting the equity section accordingly.

4. Adjusting Retained Earnings on the Balance Sheet

How does net income from the income statement adjust the retained earnings section of the balance sheet?

Net income increases retained earnings, while net losses and dividend payments decrease them. The ending retained earnings balance is calculated by adding net income to the beginning retained earnings and subtracting any dividends paid to shareholders.

Here’s a step-by-step explanation:

- Beginning Retained Earnings: Start with the retained earnings balance from the previous period’s balance sheet. This is the cumulative net income of the company from prior years that has not been distributed to shareholders.

- Add Net Income: Add the net income calculated from the current period’s income statement to the beginning retained earnings. This increases the equity in the company.

- Subtract Dividends: If the company paid any dividends to shareholders during the period, subtract these from the sum of beginning retained earnings and net income. Dividends represent a distribution of profits to the owners and reduce the retained earnings.

- Calculate Ending Retained Earnings: The result of this calculation is the ending retained earnings balance, which is reported on the balance sheet for the current period.

The formula for calculating ending retained earnings is:

Ending Retained Earnings = Beginning Retained Earnings + Net Income - Dividends

For example, suppose a company has a beginning retained earnings balance of $500,000. During the year, it generates a net income of $100,000 and pays out dividends of $30,000. The ending retained earnings would be calculated as follows:

Ending Retained Earnings = $500,000 + $100,000 - $30,000 = $570,000

This $570,000 would be the retained earnings balance reported on the current period’s balance sheet. This adjustment ensures that the balance sheet reflects the cumulative impact of the company’s profitability and distribution of profits over time.

5. Impact of Sales and Expenses on Assets and Liabilities

How do sales and expenses, as reflected in the income statement, directly impact the asset and liability sections of the balance sheet?

Sales increase assets or decrease liabilities, while expenses decrease assets or increase liabilities. For example, a cash sale increases cash (an asset), and a credit sale increases accounts receivable (another asset). Expenses like rent paid in cash decrease cash or increase accounts payable if unpaid.

To break it down further:

- Sales Impact:

- Cash Sales: When a sale is made for cash, the company receives cash immediately, which increases the cash account (an asset) on the balance sheet.

- Credit Sales: When a sale is made on credit, the company does not receive cash immediately but creates an account receivable (an asset), representing the amount owed by the customer.

- Sales Returns and Allowances: If customers return goods or receive allowances due to defects, this reduces sales revenue on the income statement and also decreases either cash (if a refund is given) or accounts receivable (if the customer’s balance is reduced) on the balance sheet.

- Expenses Impact:

- Cash Expenses: When an expense is paid in cash, such as rent or salaries, the company’s cash account (an asset) decreases.

- Accrued Expenses: Some expenses are incurred but not yet paid, such as salaries payable or interest payable. These create liabilities on the balance sheet, representing the company’s obligation to pay these amounts in the future.

- Depreciation Expense: Depreciation is the allocation of the cost of a fixed asset (like equipment) over its useful life. While depreciation expense appears on the income statement, it also impacts the balance sheet by increasing accumulated depreciation, which is a contra-asset account that reduces the book value of the related fixed asset.

For example, consider a company that makes a cash sale of $1,000. This transaction increases the cash account on the balance sheet by $1,000. If the company then pays $500 in rent, the cash account decreases by $500.

Another example is when a company incurs $200 in salaries but hasn’t paid them yet. This creates a liability called salaries payable of $200 on the balance sheet.

These interconnections highlight the importance of double-entry accounting, where every transaction affects at least two accounts, ensuring that the accounting equation (Assets = Liabilities + Equity) always balances.

6. Managing Accounts Receivable and Payable

How do accounts receivable and accounts payable, stemming from income statement activities, affect the balance sheet?

Accounts receivable (from credit sales) are assets representing money owed to the company, while accounts payable (from credit purchases) are liabilities representing money the company owes to suppliers. Efficient management of these accounts is crucial for maintaining liquidity and financial health.

Here’s an in-depth look:

- Accounts Receivable (AR):

- Creation: AR is created when a company makes a sale on credit. This means the customer receives the goods or services immediately but pays for them later, usually within a specified period (e.g., 30 days).

- Balance Sheet Impact: AR is an asset on the balance sheet, representing the amount of money owed to the company by its customers.

- Management: Effective management of AR involves:

- Setting credit policies to determine which customers are eligible for credit.

- Invoicing customers promptly and accurately.

- Monitoring AR balances to identify overdue accounts.

- Implementing collection procedures to ensure timely payment.

- Impact on Liquidity: High levels of AR can strain a company’s cash flow if customers are slow to pay.

- Accounts Payable (AP):

- Creation: AP is created when a company purchases goods or services on credit from its suppliers. The company receives the goods or services immediately but pays for them later, usually within a specified period.

- Balance Sheet Impact: AP is a liability on the balance sheet, representing the amount of money the company owes to its suppliers.

- Management: Effective management of AP involves:

- Negotiating favorable payment terms with suppliers.

- Processing invoices accurately and promptly.

- Monitoring AP balances to ensure timely payment.

- Taking advantage of early payment discounts when available.

- Impact on Cash Flow: Managing AP effectively allows a company to conserve cash and maintain good relationships with its suppliers.

For example, if a company makes credit sales totaling $50,000, this creates accounts receivable of $50,000 on the balance sheet. If the company then purchases inventory on credit for $30,000, this creates accounts payable of $30,000 on the balance sheet.

Efficient management of AR and AP is critical for maintaining a healthy cash conversion cycle, which is the time it takes for a company to convert its investments in inventory and other resources into cash.

7. Handling Depreciation and Amortization Expenses

How do depreciation and amortization expenses from the income statement affect the asset side of the balance sheet?

Depreciation (for tangible assets) and amortization (for intangible assets) reduce the book value of assets on the balance sheet. Depreciation is recorded in the accumulated depreciation account, a contra-asset account that lowers the net value of fixed assets. Amortization directly reduces the value of intangible assets.

Here’s a detailed explanation:

- Depreciation:

- Definition: Depreciation is the systematic allocation of the cost of a tangible asset (such as equipment, buildings, or vehicles) over its useful life.

- Income Statement Impact: Depreciation expense is recorded on the income statement, reducing net income.

- Balance Sheet Impact:

- Depreciation increases the accumulated depreciation account, which is a contra-asset account.

- Accumulated depreciation reduces the book value of the related asset on the balance sheet.

- The book value is calculated as: Book Value = Original Cost – Accumulated Depreciation.

- Example: Suppose a company purchases a machine for $100,000 with an estimated useful life of 10 years and no salvage value. Using the straight-line method, the annual depreciation expense would be $10,000. Each year, the depreciation expense is recorded on the income statement, and the accumulated depreciation account on the balance sheet increases by $10,000. After 5 years, the accumulated depreciation would be $50,000, and the book value of the machine would be $50,000.

- Amortization:

- Definition: Amortization is the systematic allocation of the cost of an intangible asset (such as patents, copyrights, or trademarks) over its useful life.

- Income Statement Impact: Amortization expense is recorded on the income statement, reducing net income.

- Balance Sheet Impact:

- Amortization directly reduces the carrying value of the intangible asset on the balance sheet.

- There is no contra-asset account for amortization; instead, the asset’s value is directly reduced.

- Example: Suppose a company purchases a patent for $50,000 with a legal life of 20 years but an estimated useful life of 10 years. Using the straight-line method, the annual amortization expense would be $5,000. Each year, the amortization expense is recorded on the income statement, and the carrying value of the patent on the balance sheet is reduced by $5,000. After 5 years, the carrying value of the patent would be $25,000.

Both depreciation and amortization reflect the decline in value of assets over time, and they are important for accurately representing a company’s financial position on the balance sheet.

8. Managing Prepaid and Accrued Expenses

How do prepaid expenses and accrued expenses, recognized through income statement adjustments, get reflected on the balance sheet?

Prepaid expenses are assets representing payments made for goods or services not yet received, while accrued expenses are liabilities representing expenses incurred but not yet paid. These require careful tracking and adjustment to accurately reflect a company’s financial position.

Here’s an in-depth explanation:

- Prepaid Expenses:

- Definition: Prepaid expenses are payments made in advance for goods or services that will be used or consumed in the future.

- Balance Sheet Impact: Prepaid expenses are recorded as assets on the balance sheet.

- Income Statement Impact: As the goods or services are used or consumed, the prepaid expense is recognized as an expense on the income statement.

- Example: Suppose a company pays $12,000 for a one-year insurance policy on January 1. The initial entry is to debit prepaid insurance (an asset) and credit cash for $12,000. Each month, $1,000 of the prepaid insurance is recognized as insurance expense on the income statement, and the prepaid insurance asset is reduced by $1,000 on the balance sheet.

- Accrued Expenses:

- Definition: Accrued expenses are expenses that have been incurred but not yet paid as of the balance sheet date.

- Balance Sheet Impact: Accrued expenses are recorded as liabilities on the balance sheet.

- Income Statement Impact: The expense is recognized on the income statement in the period it is incurred, regardless of when it is paid.

- Example: Suppose a company has salaries of $5,000 that have been earned by employees but not yet paid as of the end of the month. The company would accrue the salaries by debiting salaries expense on the income statement and crediting salaries payable (a liability) on the balance sheet for $5,000. When the salaries are paid in the following month, the salaries payable account is debited, and cash is credited.

Properly managing prepaid and accrued expenses is essential for accurate financial reporting. It ensures that expenses are recognized in the correct period, which is crucial for matching revenues and expenses and for providing a true and fair view of a company’s financial performance.

9. Impact of Borrowing and Interest Expenses

How does borrowing money (notes payable) and related interest expenses affect both the income statement and the balance sheet?

Borrowing money increases cash (an asset) and notes payable (a liability). Interest expense, accrued over time, reduces net income on the income statement and increases accrued interest payable on the balance sheet.

Here’s a detailed breakdown:

- Borrowing Money (Notes Payable):

- Balance Sheet Impact: When a company borrows money by issuing a note payable, the cash account (an asset) increases, and the notes payable account (a liability) also increases.

- Example: If a company borrows $100,000 by issuing a note payable, the balance sheet will show an increase of $100,000 in cash and an increase of $100,000 in notes payable.

- Interest Expense:

- Income Statement Impact: Interest expense is the cost of borrowing money and is recorded on the income statement, reducing net income.

- Balance Sheet Impact:

- As interest accrues over time but is not yet paid, it creates an accrued interest payable liability on the balance sheet.

- When the interest is paid, the cash account decreases, and the accrued interest payable account decreases.

- Example: Suppose a company has a note payable with an annual interest rate of 5%. If the company has not paid the interest at the end of the year, it must accrue the interest expense. The accrued interest expense would be calculated as:

- Interest Expense = Principal x Interest Rate x Time

- Interest Expense = $100,000 x 5% x 1 year = $5,000

- The company would debit interest expense on the income statement and credit accrued interest payable (a liability) on the balance sheet for $5,000.

The relationship between borrowing and interest expenses highlights the importance of managing debt effectively. While borrowing can provide companies with the capital they need to grow, it also creates an obligation to repay the debt and pay interest, which can impact profitability and cash flow.

10. Completing the Balance Sheet: Ensuring Accuracy and Balance

What are the final steps to ensure the balance sheet is accurate and balanced after incorporating information from the income statement?

The final steps involve verifying that total assets equal the sum of total liabilities and equity, reviewing all account balances for accuracy, and ensuring consistency with accounting principles. This ensures the balance sheet provides a true and fair view of the company’s financial position.

Here’s a detailed checklist:

- Verify the Accounting Equation: Ensure that the basic accounting equation (Assets = Liabilities + Equity) holds true. This is the fundamental principle of double-entry accounting.

- Total Assets should equal the sum of Total Liabilities and Total Equity.

- Review Account Balances:

- Assets: Review all asset accounts, including cash, accounts receivable, inventory, prepaid expenses, and fixed assets. Ensure that the balances are accurate and that any necessary adjustments (such as depreciation) have been made.

- Liabilities: Review all liability accounts, including accounts payable, accrued expenses, notes payable, and deferred revenue. Ensure that the balances are accurate and that all obligations are properly recorded.

- Equity: Review the equity section, including common stock, retained earnings, and additional paid-in capital. Ensure that the retained earnings balance is correctly calculated based on the net income from the income statement and any dividends paid.

- Check for Consistency:

- Ensure that the balances reported on the balance sheet are consistent with the information reported on the income statement and the statement of cash flows.

- Verify that the accounting methods used are consistent with prior periods and in accordance with generally accepted accounting principles (GAAP) or International Financial Reporting Standards (IFRS).

- Review Disclosures:

- Ensure that all required disclosures are included in the notes to the financial statements. These disclosures provide additional information about the company’s accounting policies, significant transactions, and other important matters.

- Obtain Independent Review:

- Consider having the balance sheet reviewed by an independent accountant or auditor to ensure its accuracy and compliance with accounting standards.

By following these steps, companies can ensure that their balance sheets are accurate and provide a reliable basis for making informed financial decisions.

Key Considerations for Accurate Financial Reporting

What crucial factors should be considered to ensure accurate financial reporting when creating a balance sheet from an income statement?

Maintaining meticulous records, adhering to accounting standards, ensuring consistent application of accounting policies, and conducting regular internal audits are crucial for accurate financial reporting.

Here’s an expanded view:

- Meticulous Record-Keeping:

- Importance: Accurate and detailed records are the foundation of reliable financial reporting. Every transaction should be properly documented and recorded in a timely manner.

- Best Practices:

- Use a robust accounting system to track all financial transactions.

- Maintain organized and easily accessible records.

- Implement internal controls to ensure the accuracy and integrity of the data.

- Adherence to Accounting Standards:

- Importance: Compliance with accounting standards (such as GAAP or IFRS) ensures that financial statements are prepared consistently and are comparable across different companies.

- Best Practices:

- Stay up-to-date on the latest accounting standards.

- Consult with accounting professionals to ensure compliance.

- Document all accounting policies and procedures.

- Consistent Application of Accounting Policies:

- Importance: Consistency in the application of accounting policies from period to period ensures that financial statements are comparable over time.

- Best Practices:

- Document all accounting policies and procedures.

- Apply the same policies consistently unless there is a valid reason to change them.

- Disclose any changes in accounting policies in the notes to the financial statements.

- Regular Internal Audits:

- Importance: Internal audits help to identify errors, omissions, and inconsistencies in the financial reporting process.

- Best Practices:

- Conduct regular internal audits of financial records and processes.

- Implement corrective actions to address any identified issues.

- Ensure that internal auditors are independent and objective.

By focusing on these key considerations, companies can enhance the accuracy and reliability of their financial reporting, which is essential for making informed decisions and for maintaining the trust of stakeholders.

11. Utilizing Financial Ratios for Analysis

How can financial ratios derived from the balance sheet and income statement be used for financial analysis?

Financial ratios provide insights into a company’s profitability, liquidity, solvency, and efficiency. Key ratios include profitability ratios (e.g., net profit margin), liquidity ratios (e.g., current ratio), solvency ratios (e.g., debt-to-equity ratio), and efficiency ratios (e.g., inventory turnover ratio).

Here’s an elaboration:

- Profitability Ratios:

- Net Profit Margin: Measures the percentage of revenue that remains after deducting all expenses.

- Formula: Net Profit Margin = (Net Income / Revenue) x 100

- Interpretation: A higher net profit margin indicates that the company is more efficient at controlling costs and generating profits.

- Gross Profit Margin: Measures the percentage of revenue that remains after deducting the cost of goods sold.

- Formula: Gross Profit Margin = (Gross Profit / Revenue) x 100

- Interpretation: A higher gross profit margin indicates that the company is more efficient at managing its production costs.

- Net Profit Margin: Measures the percentage of revenue that remains after deducting all expenses.

- Liquidity Ratios:

- Current Ratio: Measures a company’s ability to pay its short-term obligations with its current assets.

- Formula: Current Ratio = Current Assets / Current Liabilities

- Interpretation: A current ratio of 1.5 to 2 is generally considered healthy, indicating that the company has enough liquid assets to cover its short-term liabilities.

- Quick Ratio (Acid-Test Ratio): Measures a company’s ability to pay its short-term obligations with its most liquid assets (excluding inventory).

- Formula: Quick Ratio = (Current Assets – Inventory) / Current Liabilities

- Interpretation: A quick ratio of 1 or higher is generally considered healthy, indicating that the company has enough liquid assets to cover its short-term liabilities without relying on the sale of inventory.

- Current Ratio: Measures a company’s ability to pay its short-term obligations with its current assets.

- Solvency Ratios:

- Debt-to-Equity Ratio: Measures the proportion of a company’s financing that comes from debt compared to equity.

- Formula: Debt-to-Equity Ratio = Total Debt / Total Equity

- Interpretation: A lower debt-to-equity ratio indicates that the company is less reliant on debt financing and is therefore less risky.

- Times Interest Earned Ratio: Measures a company’s ability to cover its interest expense with its operating income.

- Formula: Times Interest Earned Ratio = Operating Income / Interest Expense

- Interpretation: A higher times interest earned ratio indicates that the company is more capable of meeting its interest obligations.

- Debt-to-Equity Ratio: Measures the proportion of a company’s financing that comes from debt compared to equity.

- Efficiency Ratios:

- Inventory Turnover Ratio: Measures how quickly a company is selling its inventory.

- Formula: Inventory Turnover Ratio = Cost of Goods Sold / Average Inventory

- Interpretation: A higher inventory turnover ratio indicates that the company is efficiently managing its inventory.

- Accounts Receivable Turnover Ratio: Measures how quickly a company is collecting its accounts receivable.

- Formula: Accounts Receivable Turnover Ratio = Revenue / Average Accounts Receivable

- Interpretation: A higher accounts receivable turnover ratio indicates that the company is efficiently collecting its receivables.

- Inventory Turnover Ratio: Measures how quickly a company is selling its inventory.

By analyzing these and other financial ratios, stakeholders can gain a deeper understanding of a company’s financial performance and position.

12. Common Pitfalls to Avoid

What are common mistakes to avoid when creating a balance sheet from an income statement?

Common pitfalls include neglecting accrual accounting principles, misclassifying assets or liabilities, overlooking depreciation and amortization, and failing to reconcile intercompany transactions.

Here’s a more detailed explanation:

- Neglecting Accrual Accounting Principles:

- Mistake: Failing to recognize revenues when earned and expenses when incurred, regardless of when cash changes hands.

- Impact: This can lead to an inaccurate representation of a company’s financial performance and position.

- Solution: Adhere to accrual accounting principles, which require recognizing revenues and expenses in the periods to which they relate.

- Misclassifying Assets or Liabilities:

- Mistake: Incorrectly classifying an asset as a liability or vice versa.

- Impact: This can distort the balance sheet and lead to incorrect financial ratios and analyses.

- Solution: Understand the definitions of assets and liabilities and classify them accordingly.

- Overlooking Depreciation and Amortization:

- Mistake: Failing to properly account for depreciation of tangible assets and amortization of intangible assets.

- Impact: This can overstate the value of assets and understate expenses.

- Solution: Calculate depreciation and amortization accurately and record them in the appropriate accounts.

- Failing to Reconcile Intercompany Transactions:

- Mistake: Not reconciling transactions between different entities within the same company.

- Impact: This can lead to double-counting of revenues and expenses and inaccurate financial statements.

- Solution: Reconcile intercompany transactions regularly to ensure that they are properly eliminated in the consolidated financial statements.

- Ignoring the Impact of Inventory:

- Mistake: Failing to properly value and account for inventory.

- Impact: This can affect both the income statement (cost of goods sold) and the balance sheet (inventory asset).

- Solution: Use a consistent inventory costing method (such as FIFO, LIFO, or weighted-average) and regularly monitor inventory levels.

- Not Properly Accounting for Deferred Taxes:

- Mistake: Ignoring the tax implications of temporary differences between taxable income and accounting income.

- Impact: This can result in an inaccurate representation of a company’s tax liabilities and assets.

- Solution: Calculate and record deferred tax assets and liabilities in accordance with accounting standards.

By avoiding these common pitfalls, companies can improve the accuracy and reliability of their financial statements and make better-informed decisions.

13. Real-World Examples of Balance Sheet Impact

Can you provide real-world examples illustrating how income statement transactions affect the balance sheet?

Certainly, consider these examples: Apple’s revenue impacting cash reserves, Amazon’s inventory management affecting current assets, and Tesla’s depreciation of manufacturing equipment influencing fixed assets.

Let’s delve deeper into each example:

- Apple Inc.:

- Income Statement Transaction: Apple generates significant revenue from the sale of iPhones, iPads, and other products and services.

- Balance Sheet Impact: This revenue increases Apple’s cash reserves (an asset) on the balance sheet. Apple can then use this cash to invest in research and development, acquire other companies, or return capital to shareholders through dividends or stock buybacks.

- Example: In its fiscal year 2023, Apple reported revenue of $383.9 billion. This increased the company’s cash and marketable securities by a significant amount, allowing it to continue investing in new products and technologies.

- Amazon.com Inc.:

- Income Statement Transaction: Amazon incurs significant costs related to managing its vast inventory of products.

- Balance Sheet Impact: Efficient inventory management can improve Amazon’s current assets (inventory) and reduce its cost of goods sold. Amazon’s ability to quickly turn over its inventory is a key factor in its profitability and cash flow.

- Example: Amazon’s inventory turnover ratio is consistently high compared to its competitors, indicating that it is effectively managing its inventory and minimizing holding costs.

- Tesla, Inc.:

- Income Statement Transaction: Tesla incurs depreciation expense on its manufacturing equipment used to produce electric vehicles.

- Balance Sheet Impact: Depreciation expense reduces Tesla’s net income on the income statement and also reduces the book value of its fixed assets (such as manufacturing equipment) on the balance sheet. The accumulated depreciation account increases over time, reflecting the wear and tear of the equipment.

- Example: Tesla’s investment in its Gigafactory and other manufacturing facilities results in significant depreciation expense each year. This expense is reflected on the income statement and reduces the carrying value of its fixed assets on the balance sheet.

These real-world examples illustrate the direct and significant impact of income statement transactions on the balance sheet. By understanding these interconnections, companies can better manage their financial performance and make informed decisions.

14. The Role of Technology and Software

How can accounting software and technology streamline the process of creating a balance sheet from an income statement?

Accounting software automates data entry, performs calculations, ensures accuracy, and generates financial reports, saving time and reducing errors. Cloud-based solutions offer real-time data access and collaboration, further streamlining the process.

Here’s a more detailed explanation:

- Automation of Data Entry:

- Accounting software automates the process of recording financial transactions, reducing the need for manual data entry.

- Transactions are automatically classified and categorized, ensuring consistency and accuracy.

- Automated Calculations:

- Accounting software performs complex calculations, such as depreciation, amortization, and tax calculations, automatically.

- This eliminates the risk of human error and ensures that calculations are performed consistently.

- Real-Time Data Access:

- Cloud-based accounting software provides real-time access to financial data from anywhere with an internet connection.

- This allows stakeholders to monitor financial performance and position on a timely basis.

- Improved Collaboration:

- Cloud-based accounting software enables multiple users to access and collaborate on financial data simultaneously.

- This streamlines the financial reporting process and improves communication among team members.

- Automated Report Generation:

- Accounting software can generate a wide range of financial reports, including the income statement, balance sheet, and statement of cash flows, automatically.

- This saves time and effort and ensures that reports are prepared in a consistent and accurate manner.

- Data Analytics and Visualization:

- Some accounting software includes data analytics and visualization tools that can help companies gain insights into their financial performance.

- These tools can help identify trends, patterns, and anomalies in the data, allowing companies to make better-informed decisions.

Popular accounting software packages, such as QuickBooks, Xero, and NetSuite, offer a wide range of features to streamline the process of creating a balance sheet from an income statement.

15. Strategic Partnership Opportunities via Financial Statement Analysis

How does understanding the link between the income statement and balance sheet help in identifying strategic partnership opportunities?

A thorough understanding of financial statements enables companies to identify potential partners with complementary strengths, assess financial stability, and negotiate favorable terms, enhancing the likelihood of successful and profitable partnerships.

Here’s how:

- Identifying Complementary Strengths:

- By analyzing the financial statements of potential partners, companies can identify areas where their strengths complement each other.

- For example, one company may have strong sales and marketing capabilities, while another may have strong research and development capabilities. By partnering, these companies can leverage each other’s strengths and achieve greater success.

- Assessing Financial Stability:

- Analyzing the financial statements of potential partners can help companies assess their financial stability and creditworthiness.

- This is important for minimizing the risk of partnering with a company that is financially unstable or may not be able to meet its obligations.

- Negotiating Favorable Terms:

- Understanding the financial statements of potential partners can help companies negotiate favorable terms for the partnership.

- For example, if a company knows that a potential partner is struggling financially, it may be able to negotiate