Taxable income is the foundation upon which your tax liability is calculated, impacting everything from your personal finances to your business strategies. This guide, brought to you by income-partners.net, will explore exactly How To Get Taxable Income, differentiating it from gross income and outlining key deductions and exemptions. Let’s explore how you can use this knowledge to optimize your income and potentially uncover strategic partnerships that enhance your financial standing. We’ll cover strategies, opportunities, and proactive steps.

1. Understanding Taxable Income: The Basics

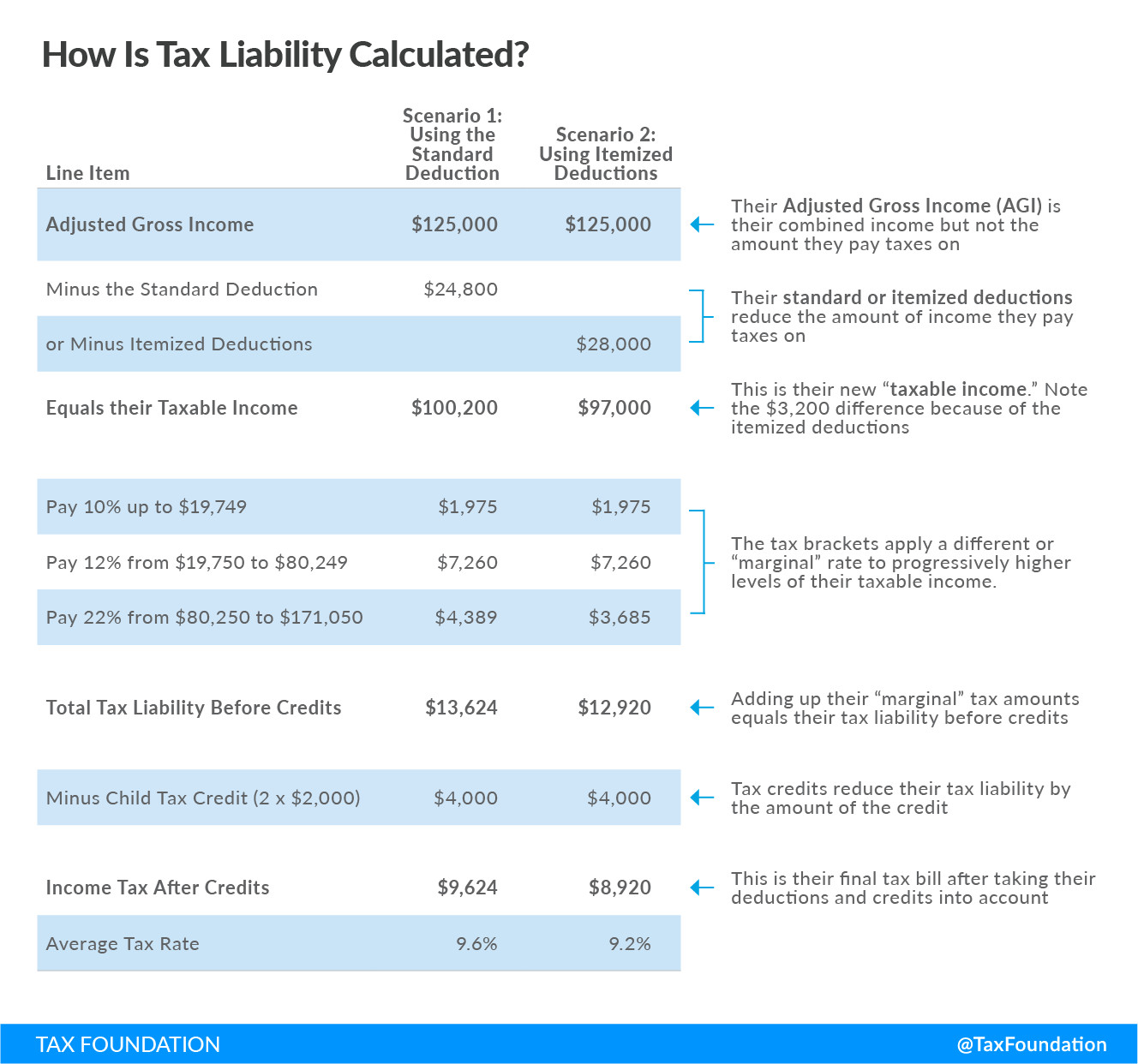

So, what exactly is taxable income?

Taxable income is the portion of your gross income that is subject to taxation by federal, state, and local governments. It’s not the same as your gross income, which is the total amount of money you earn. Instead, it’s what remains after you’ve subtracted certain deductions and exemptions.

1.1. Decoding Gross Income: Your Starting Point

What does gross income include, and how is it different from taxable income?

Gross income is the total income you receive before any deductions or taxes are taken out. According to the IRS, gross income includes wages, salaries, tips, interest, dividends, rents, royalties, and profits from businesses. Understanding your gross income is the first step in calculating your taxable income.

1.2. Deductions vs. Exemptions: What’s the Difference?

How do deductions and exemptions reduce your taxable income, and why are they important?

Deductions and exemptions are both used to lower your taxable income, but they work differently. Deductions reduce the amount of income that is subject to tax, while exemptions are fixed amounts that you can subtract from your gross income. Understanding the difference is crucial for maximizing tax savings.

1.3. AGI: The Bridge Between Gross and Taxable Income

What is Adjusted Gross Income (AGI), and how does it help in calculating taxable income?

Adjusted Gross Income (AGI) is your gross income minus certain “above-the-line” deductions, such as contributions to traditional IRAs, student loan interest payments, and alimony payments. AGI is an important figure because it’s used to determine eligibility for many other deductions and credits.

Tax Basics – How Is Tax Liability Calculated, adjusted gross income, average tax rate, child tax credit, earned income tax credit, individual income tax, itemized deduction, marginal tax rate, standard deduction, tax credit, tax deduction, taxable income

Tax Basics – How Is Tax Liability Calculated, adjusted gross income, average tax rate, child tax credit, earned income tax credit, individual income tax, itemized deduction, marginal tax rate, standard deduction, tax credit, tax deduction, taxable income

2. Calculating Taxable Income for Individuals

How do individuals calculate their taxable income, and what factors influence this calculation?

Calculating your taxable income as an individual involves several steps, starting with determining your gross income and then subtracting applicable deductions and exemptions. Your filing status (single, married filing jointly, etc.) and age also play a role.

2.1. Standard Deduction vs. Itemized Deductions: Which Is Right for You?

Should you take the standard deduction or itemize? What are the pros and cons of each?

You have two options when it comes to reducing your taxable income: taking the standard deduction or itemizing deductions. The standard deduction is a fixed amount that varies depending on your filing status. Itemizing involves listing out individual deductions, such as medical expenses, mortgage interest, and charitable contributions. You should choose the option that results in the lower taxable income.

2.2. Common Deductions for Individuals: A Detailed Overview

What are some common deductions that individuals can claim to reduce their taxable income?

- Medical Expenses: You can deduct medical expenses that exceed 7.5% of your AGI.

- State and Local Taxes (SALT): You can deduct up to $10,000 for state and local taxes, including property taxes and either state income taxes or sales taxes.

- Mortgage Interest: If you own a home, you can deduct the interest you pay on your mortgage.

- Charitable Contributions: You can deduct contributions to qualified charitable organizations.

- Retirement Contributions: Contributions to traditional IRAs and 401(k)s are often deductible.

According to a study by the University of Texas at Austin’s McCombs School of Business, taxpayers who itemize deductions save significantly more on their taxes compared to those who take the standard deduction.

2.3. Tax Credits: A Direct Reduction of Your Tax Liability

How do tax credits differ from deductions, and what are some valuable tax credits for individuals?

Tax credits directly reduce the amount of tax you owe, whereas deductions reduce your taxable income. Tax credits are generally more valuable than deductions. Some valuable tax credits for individuals include the Child Tax Credit, the Earned Income Tax Credit, and the American Opportunity Tax Credit.

3. Calculating Taxable Income for Businesses

How do businesses determine their taxable income, and what expenses are deductible?

Calculating taxable income for businesses involves subtracting business expenses from gross income. The IRS has specific rules about what expenses are deductible.

3.1. Deductible Business Expenses: What Can You Write Off?

What types of business expenses can be deducted to reduce taxable income?

- Cost of Goods Sold (COGS): This includes the direct costs of producing or acquiring goods that you sell.

- Salaries and Wages: You can deduct the salaries and wages you pay to employees.

- Rent: If you rent office space or equipment, you can deduct the rent you pay.

- Utilities: You can deduct the cost of utilities, such as electricity, gas, and water.

- Depreciation: You can deduct a portion of the cost of assets, such as equipment and buildings, over their useful life.

3.2. The Qualified Business Income (QBI) Deduction: A Key Benefit for Small Businesses

What is the QBI deduction, and how can it benefit small business owners?

The Qualified Business Income (QBI) deduction allows eligible self-employed individuals and small business owners to deduct up to 20% of their qualified business income. This deduction can significantly reduce your taxable income.

3.3. Corporate Taxable Income: Specific Considerations

How does calculating taxable income differ for corporations compared to other business structures?

Corporations calculate their taxable income by subtracting deductions from their gross income, similar to individuals and other businesses. However, corporations face unique tax rules and considerations, such as the corporate tax rate and rules around dividends.

4. Tax Planning Strategies to Reduce Taxable Income

What strategies can individuals and businesses use to proactively reduce their taxable income?

Effective tax planning involves taking advantage of all available deductions, exemptions, and credits to minimize your tax liability. This requires careful record-keeping and a thorough understanding of tax laws.

4.1. Maximize Retirement Contributions: Secure Your Future and Reduce Taxes

How can contributing to retirement accounts lower your taxable income?

Contributing to tax-advantaged retirement accounts, such as 401(k)s and traditional IRAs, can significantly reduce your taxable income. The contributions are often tax-deductible, and the earnings grow tax-deferred until retirement.

4.2. Health Savings Accounts (HSAs): A Triple Tax Advantage

What are the benefits of using an HSA, and how can it help lower your taxable income?

Health Savings Accounts (HSAs) offer a triple tax advantage: contributions are tax-deductible, earnings grow tax-free, and withdrawals for qualified medical expenses are tax-free. If you have a high-deductible health insurance plan, an HSA can be a valuable tool for reducing your taxable income and saving for healthcare expenses.

4.3. Tax-Loss Harvesting: Turning Investment Losses Into Tax Savings

How can you use tax-loss harvesting to offset capital gains and reduce your taxable income?

Tax-loss harvesting involves selling investments that have lost value to offset capital gains. This can reduce your overall tax liability. You can also use up to $3,000 in net capital losses to offset ordinary income.

5. Common Mistakes to Avoid When Calculating Taxable Income

What are some common errors people make when calculating their taxable income, and how can you avoid them?

Calculating your taxable income accurately is crucial to avoid penalties and interest. Here are some common mistakes to avoid:

5.1. Not Keeping Accurate Records: The Importance of Documentation

Why is it essential to keep detailed records of income and expenses for tax purposes?

Accurate record-keeping is essential for claiming deductions and credits. Keep receipts, invoices, and other documentation to support your claims.

5.2. Missing Deadlines: Staying on Top of Tax Filing Dates

What are the key tax deadlines, and what happens if you miss them?

Missing tax deadlines can result in penalties and interest. Be sure to file your taxes on time, or request an extension if needed.

5.3. Overlooking Deductions and Credits: Maximizing Your Tax Savings

How can you ensure you’re not missing out on valuable deductions and credits?

Review the tax laws and regulations carefully to identify all the deductions and credits you’re eligible for. Consult with a tax professional if needed.

6. Navigating State and Local Taxable Income

How do state and local taxes factor into your overall taxable income picture?

In addition to federal income taxes, you may also be subject to state and local income taxes. The rules and rates vary widely by location.

6.1. State Income Tax: Key Differences and Considerations

What are some key differences between state and federal income tax systems?

Some states have a flat income tax rate, while others have a progressive tax system like the federal government. Some states also have different deductions and credits.

6.2. Local Income Tax: Understanding Municipal Tax Obligations

Do you need to pay local income taxes? How do they impact your overall tax burden?

Some cities and counties impose local income taxes. These taxes are typically a percentage of your income and can impact your overall tax burden.

6.3. State and Local Tax Planning: Strategies for Minimizing Your Tax Liability

How can you plan for state and local taxes to minimize your overall tax liability?

Consider the state and local tax implications when making financial decisions, such as where to live and work. Take advantage of any available deductions and credits.

7. Nontaxable Income: What Doesn’t Get Taxed?

What types of income are generally considered nontaxable by the IRS?

Not all income is taxable. Some common examples of nontaxable income include:

7.1. Gifts and Inheritances: Understanding Tax Implications

Are gifts and inheritances taxable? What are the rules around gift and estate taxes?

Generally, gifts and inheritances are not considered taxable income to the recipient. However, large gifts may be subject to gift tax, and large estates may be subject to estate tax.

7.2. Life Insurance Payouts: Tax-Free Benefits for Beneficiaries

Are life insurance payouts taxable? What are the tax implications for beneficiaries?

Life insurance payouts are generally not taxable to the beneficiary. This can provide financial security for your loved ones without tax implications.

7.3. Certain Retirement Account Distributions: Navigating Tax-Free Withdrawals

Under what circumstances can you withdraw money from retirement accounts tax-free?

Distributions from Roth IRAs and Roth 401(k)s are generally tax-free in retirement, as long as certain conditions are met. Distributions from traditional retirement accounts are taxed as ordinary income.

8. The Impact of Tax Law Changes on Taxable Income

How do changes in tax laws affect how you calculate your taxable income?

Tax laws are constantly changing, so it’s important to stay informed about the latest updates and how they may affect your taxable income.

8.1. Recent Tax Reforms: Key Provisions Affecting Individuals and Businesses

What are some of the most significant changes to tax laws in recent years?

Recent tax reforms have made significant changes to individual and business tax rates, deductions, and credits.

8.2. Future Tax Law Changes: Staying Ahead of the Curve

What potential tax law changes are on the horizon, and how might they impact your tax planning?

Stay informed about proposed tax law changes and how they may affect your tax planning.

8.3. Adapting Your Tax Strategy: Staying Compliant and Maximizing Savings

How can you adapt your tax strategy to stay compliant with changing tax laws and maximize your tax savings?

Review your tax strategy regularly to ensure it’s aligned with the latest tax laws. Consult with a tax professional if needed.

9. Finding Strategic Partnerships to Increase Taxable Income

How can strategic partnerships positively impact your taxable income?

Strategic partnerships can open new revenue streams, reduce expenses, and provide access to resources that can ultimately increase your taxable income.

9.1. Exploring Partnership Opportunities: Identifying Synergies and Shared Goals

What types of partnerships should you consider, and how do you find partners with complementary skills and goals?

Consider partnerships with businesses that offer complementary products or services, or that can help you reach new markets. Look for partners who share your values and have a track record of success.

9.2. Structuring Partnerships for Tax Efficiency: Legal and Financial Considerations

How can you structure partnerships to maximize tax benefits and minimize liabilities?

Work with legal and financial professionals to structure your partnerships in a way that maximizes tax benefits and minimizes liabilities.

9.3. Maximizing Partnership Benefits: Strategies for Growth and Profitability

How can you ensure your partnerships are successful and contribute to increased taxable income?

Establish clear goals and expectations for your partnerships. Communicate regularly with your partners and be willing to adapt your strategies as needed.

10. Resources for Calculating and Optimizing Taxable Income

Where can you find reliable information and tools to help you calculate and optimize your taxable income?

There are many resources available to help you calculate and optimize your taxable income, including:

10.1. IRS Resources: Official Guidance and Publications

What resources does the IRS offer to help taxpayers understand and comply with tax laws?

The IRS website offers a wealth of information, including publications, forms, and online tools.

10.2. Tax Software: Streamlining the Filing Process

What are the benefits of using tax software, and which programs are recommended?

Tax software can help you calculate your taxable income, identify deductions and credits, and file your taxes electronically.

10.3. Tax Professionals: When to Seek Expert Advice

When should you consider hiring a tax professional, and what are the benefits of doing so?

Consider hiring a tax professional if you have complex tax situations or need help navigating the tax laws. A tax professional can provide personalized advice and help you optimize your tax strategy.

By understanding how to get taxable income and implementing effective tax planning strategies, you can minimize your tax liability and maximize your financial well-being. Income-partners.net can help you explore strategic partnerships to further enhance your financial standing.

Ready to take control of your taxable income and explore strategic partnerships? Visit income-partners.net today to discover a wealth of information, resources, and opportunities. Connect with potential partners, learn about effective relationship-building strategies, and unlock new avenues for growth and profitability. Don’t wait – start building your path to financial success now!

Frequently Asked Questions (FAQ)

1. What is the difference between gross income and taxable income?

Gross income is the total income you receive before any deductions or taxes are taken out. Taxable income is the portion of your gross income that is subject to taxation after deductions and exemptions.

2. What are some common deductions that individuals can claim?

Common deductions include medical expenses, state and local taxes (SALT), mortgage interest, charitable contributions, and retirement contributions.

3. How does the standard deduction work?

The standard deduction is a fixed amount that varies depending on your filing status. It reduces your taxable income.

4. Should I take the standard deduction or itemize?

Choose the option that results in the lower taxable income. If your itemized deductions exceed the standard deduction, itemizing is the better choice.

5. What is the Qualified Business Income (QBI) deduction?

The QBI deduction allows eligible self-employed individuals and small business owners to deduct up to 20% of their qualified business income.

6. How can I reduce my taxable income?

Strategies to reduce your taxable income include maximizing retirement contributions, using Health Savings Accounts (HSAs), and tax-loss harvesting.

7. Are gifts and inheritances taxable?

Generally, gifts and inheritances are not considered taxable income to the recipient, but large gifts may be subject to gift tax, and large estates may be subject to estate tax.

8. How do state and local taxes affect my taxable income?

State and local taxes can impact your overall tax burden. Some states and localities impose income taxes, which are in addition to federal income taxes.

9. Where can I find reliable information about tax laws?

The IRS website offers a wealth of information, including publications, forms, and online tools. You can also consult with a tax professional.

10. How can strategic partnerships increase my taxable income?

Strategic partnerships can open new revenue streams, reduce expenses, and provide access to resources that can ultimately increase your taxable income.

Address: 1 University Station, Austin, TX 78712, United States.

Phone: +1 (512) 471-3434.

Website: income-partners.net.