Do you want to understand how to find net income from a balance sheet? Net income reveals a company’s financial performance. At income-partners.net, we guide you through understanding and leveraging this key metric for strategic partnerships and income growth. Dive in and unlock financial insights! We will explore key financial metrics, profitability analysis, and financial health assessment.

1. What is Net Income on a Balance Sheet?

Net income isn’t directly on the balance sheet but is crucial for understanding it. Net income reflects a company’s profitability after all expenses are deducted from revenue. It significantly impacts a company’s retained earnings, showing how much profit is reinvested versus distributed. In essence, net income demonstrates the financial health and operational efficiency of a business.

2. Connecting Balance Sheets with Financial Statements: Unveiling Net Income

The balance sheet, income statement, and cash flow statement are interconnected. Net income, derived from the income statement, ultimately impacts the balance sheet. This connection is vital for investors and stakeholders. Let’s look at how these statements intertwine to reveal a company’s financial story.

2.1. Understanding the Balance Sheet

The balance sheet provides a snapshot of a company’s financial health at a specific moment. It follows the basic accounting equation:

Assets = Liabilities + Shareholders’ Equity

- Assets: Resources a company owns, like cash, inventory, and equipment.

- Liabilities: Obligations or debts the company owes to others, like loans and accounts payable.

- Shareholders’ Equity: The owners’ stake in the company, including contributed capital and retained earnings.

Understanding a Balance Sheet

Understanding a Balance Sheet

2.2. Understanding the Income Statement

The income statement, also known as the profit and loss (P&L) statement, reports a company’s financial performance over a period. It calculates net income by subtracting expenses from revenues:

Net Income = Total Revenues – Total Expenses

Expenses include:

- Cost of Goods Sold (COGS)

- Operating Expenses (salaries, rent, etc.)

- Interest Expenses

- Taxes

2.3. Understanding the Interlinking Process

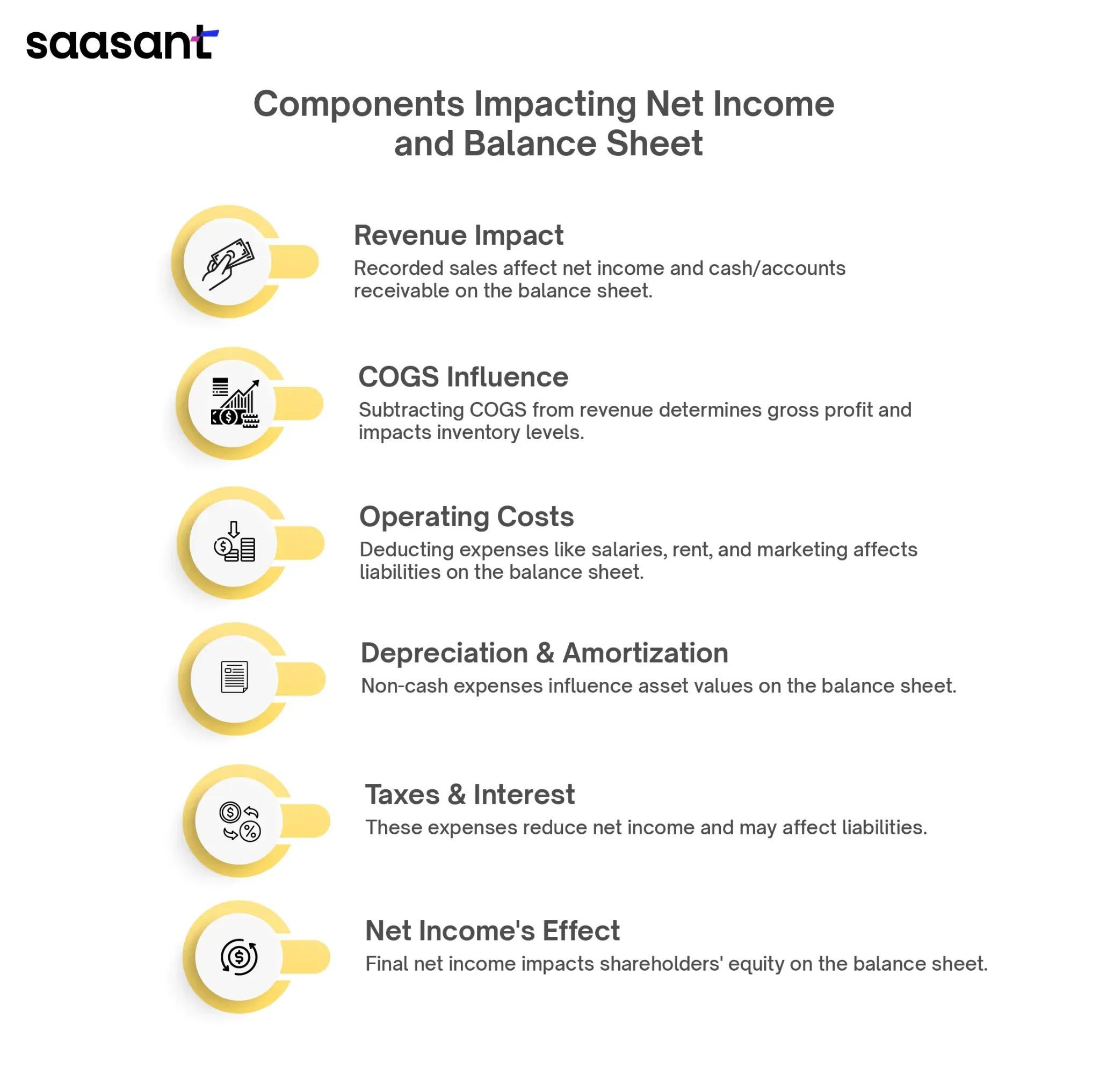

Net income connects the income statement to the balance sheet through retained earnings. The net income from the income statement increases the retained earnings in the shareholders’ equity section of the balance sheet. Here’s how the interlinking process works:

- Revenue Recognition: Revenue is recorded on the income statement, increasing net income. This can lead to increased cash or accounts receivable on the balance sheet.

- Cost of Goods Sold (COGS): COGS reduces revenue on the income statement to calculate gross profit. COGS affects inventory levels on the balance sheet.

- Operating Expenses: Expenses like salaries are deducted from gross profit on the income statement. They are often reflected as liabilities or prepaid expenses on the balance sheet.

- Depreciation and Amortization: These non-cash expenses reduce net income but are reflected on the balance sheet as accumulated depreciation, affecting asset values.

- Taxes and Interest: These expenses reduce net income and can impact liabilities on the balance sheet.

- Net Income Impact: The net income figure flows into the retained earnings section of the shareholders’ equity on the balance sheet. Positive net income increases equity, while negative net income decreases it.

3. Understanding the Balance Sheet Components in Detail

The balance sheet is a snapshot of a company’s financial state at a specific time. It balances assets with the sum of liabilities and shareholders’ equity. According to research from the University of Texas at Austin’s McCombs School of Business, efficient asset utilization and strategic liability management significantly enhance income generation.

3.1. Exploring Assets

Assets are resources a company owns that have economic value and can generate future benefits. They’re categorized into current and non-current assets:

- Current Assets: Include cash, accounts receivable, and inventory.

- Non-Current Assets: Include property, plant, equipment (PP&E), and intangible assets.

Assets are vital for income generation because they are used in daily operations and revenue-generating activities. Inventory is necessary to produce goods for sale, while equipment is essential for manufacturing processes.

3.2. Exploring Liabilities

Liabilities represent a company’s obligations or debts to external parties. They are categorized into current and non-current liabilities:

- Current Liabilities: Include accounts payable and short-term loans.

- Non-Current Liabilities: Include long-term loans and deferred tax liabilities.

Liabilities impact income generation by influencing a company’s financial obligations. Interest payments on loans reduce net income. Strategic use of liabilities, such as financing expansion projects, can increase future revenue.

3.3. Exploring Shareholders’ Equity

Shareholders’ equity represents the owners’ stake in the company after deducting liabilities from assets. It includes:

- Contributed Capital: Common stock.

- Retained Earnings: Profits reinvested in the business.

Shareholders’ equity reflects the company’s financial health and shareholders’ stake in its success. Higher equity can provide more leverage and flexibility to pursue growth opportunities and generate income.

3.4. Understanding the Relationship to Income Generation

The balance sheet’s components directly influence income generation:

- Asset Utilization: Efficient use of assets, like inventory and equipment, is essential for generating revenue.

- Liability Management: Managing debt levels and interest payments impacts profitability. Too much debt can increase interest expenses, reducing net income, while strategic debt usage can fuel growth.

- Shareholders’ Equity Impact: Shareholders’ equity reflects a company’s financial stability and ability to generate returns. A strong equity position can attract investors and provide resources for income-generating activities.

4. Core Concepts Needed to Calculate Net Income

Before calculating net income, understanding the difference between gross income, net income, and operating income is essential. These metrics offer different perspectives on a company’s financial performance. Let’s delve into these concepts and related key terms.

4.1. Understanding Gross Income vs. Net Income

- Gross Income: Total revenue a company generates before deducting any expenses. It includes all sources of income like sales and interest.

- Net Income: Also known as net profit or the bottom line, this is the income remaining after deducting all expenses from gross income, including COGS, operating expenses, taxes, and interest.

4.2. Understanding Operational Income

Operational income, or operating profit, focuses on the profitability of core business operations. It excludes non-operating income and expenses like gains or losses from asset sales or interest income/expenses.

Operating income is calculated by subtracting operating expenses (including COGS) from gross income.

4.3. Key Terms for Calculating Net Income

Key Terms for Net Income

Key Terms for Net Income

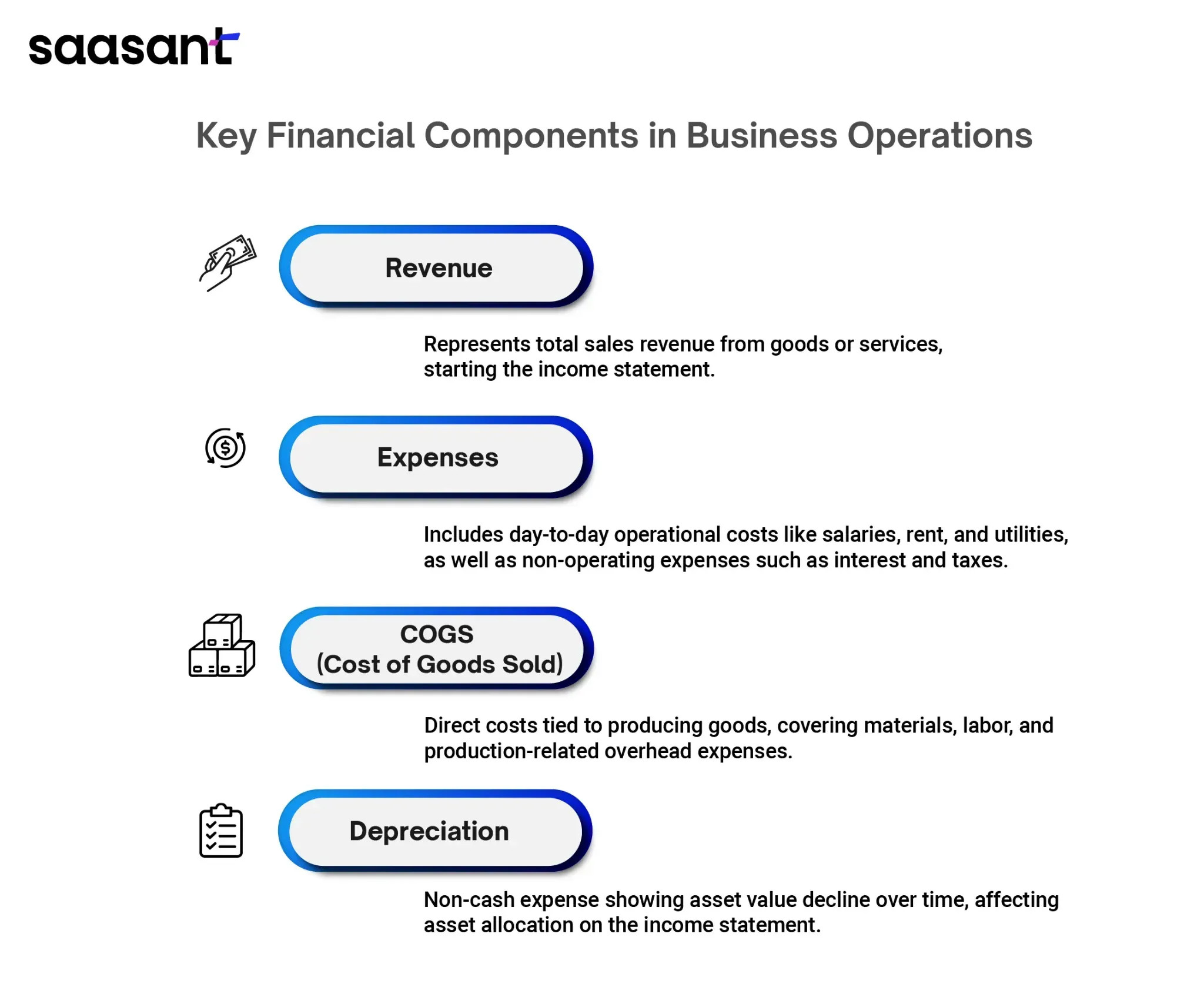

- Revenue: Total money generated from selling goods or services, also known as sales or turnover.

- Expenses: Costs incurred by a company in its daily operations, categorized into operating (salaries, rent) and non-operating (interest, taxes) expenses.

- COGS (Cost of Goods Sold): Direct costs associated with producing or purchasing a company’s goods, including materials, labor, and overhead directly related to production.

- Depreciation: A non-cash expense reflecting the decrease in the value of tangible assets (buildings, equipment) over their useful life.

4.4. Understanding the Formulas

Net income is calculated using the following formula:

Net Income = Revenue – Expenses

Where:

- Revenue includes all sources of income.

- Expenses include operating expenses, COGS, depreciation, interest, and taxes.

5. Step-by-Step Guide to Calculating Net Income

Calculating net income accurately requires identifying relevant information and applying the correct formulas. This step-by-step guide ensures precision.

5.1. Identifying Relevant Information

5.1.1. Finding Total Revenues

Locate the total revenue figure on the income statement, typically listed as “Total Revenue” or “Net Sales.” Ensure all revenue streams are included if there are multiple sources.

5.1.2. Gathering Expenses

Identify all expenses incurred, found in different sections of the income statement, such as COGS, operating expenses, interest expenses, and taxes. Ensure both operating and non-operating expenses are accounted for accurately.

5.1.3. Other Necessary Details

Include any non-operating income or gains and consider extraordinary items, one-time charges, or adjustments. Review accompanying notes or disclosures for additional details.

5.2. Using Formulas

5.2.1. Direct Formula Approach

Use the formula:

Net Income = Total Revenues – Total Expenses

Subtract total expenses from total revenues.

5.2.2. Indirect Approach via Gross Profit

First, calculate gross profit:

Gross Profit = Total Revenues – COGS

Then, subtract operating expenses:

Net Income = Gross Profit – Operating Expenses

5.2.3. Conservative Calculation Method

Incorporate allowances or reserves for unforeseen expenses or potential losses. Deduct these allowances from total revenues before subtracting expenses. This provides a more cautious estimate of net income.

6. Understanding Retained Earnings

Retained earnings are a critical part of a company’s financial statement. They represent the cumulative net income retained after distributing dividends to shareholders.

6.1. Definition of Retained Earnings

Retained earnings are the portion of net income that a company reinvests in its operations rather than distributing as dividends. They accumulate over time, contributing to the company’s equity and reflecting its profitability and reinvestment strategies.

6.2. Calculation

Retained earnings are calculated as follows:

Ending Retained Earnings = Beginning Retained Earnings + Net Income – Dividends

Retained earnings at the beginning of a period are added to the net income generated, and dividends paid to shareholders are subtracted.

6.3. Role in Calculating Net Income

Retained earnings play a significant role in calculating net income because they represent profits reinvested into the company. Net income, dividends, and any company equity adjustments directly impact retained earnings.

6.4. Method to Extract Net Income from Changes in Retained Earnings

6.4.1. Start with Retained Earnings Changes

Calculate the change in retained earnings during a specific period. This change can be found in the statement of retained earnings or derived from the balance sheet.

6.4.2. Adjust for Dividends

Subtract any dividends paid to shareholders from the change in retained earnings.

6.4.3. Consider Other Equity Adjustments

Account for any other equity adjustments, such as stock issuances or share buybacks.

6.4.4. Extract Net Income

After considering dividends and other equity changes, the net result represents the period’s net income. This method indirectly extracts net income from changes in retained earnings and other equity-related transactions.

7. Analyzing the Impact of Net Income

Net income has significant implications for business decisions and investor perspectives. Understanding these impacts is vital for strategic planning and financial health assessment.

7.1. Influence on Business Decisions and Investor Perspective

7.1.1. Business Decisions

- Investment Decisions: Higher net income attracts investors and supports fundraising for expansion or new projects.

- Operational Decisions: Businesses use net income to evaluate the success of operational strategies and assess cost control and revenue generation.

7.1.2. Investor Perspective

- Profitability Assessment: Investors assess a company’s profitability and financial health using net income figures.

- Dividend Potential: Net income influences dividend decisions, attracting income-seeking investors.

7.2. Implications of Net Income Trends Over Time

7.2.1. Positive Trends

- Investor Confidence: Consistent increases in net income enhance investor confidence and signal sustainable growth.

- Market Perception: Positive trends can improve a company’s stock price and market perception.

7.2.2. Negative Trends

- Investor Concerns: Declining or negative trends raise concerns about financial stability and performance.

- Risk Assessment: Investors may view companies with declining net income as riskier, leading to reduced interest and stock price declines.

7.2.3. Strategic Implications

- Strategic Planning: Net income trends inform strategic planning, with positive trends supporting expansion and negative trends prompting cost-cutting.

- Capital Allocation: Net income impacts capital allocation decisions, with solid income supporting R&D and debt repayment.

7.2.4. Long-Term Impact

- Sustainability: Sustainable net income growth reflects a company’s ability to adapt and maintain competitive advantages.

- Investor Loyalty: Consistent positive trends build investor loyalty and trust.

8. Income-Partners.net: Your Partner in Financial Success

At income-partners.net, we understand the challenges you face in finding the right partnerships to boost your income. Our platform is designed to provide you with the information, strategies, and connections you need to succeed. Here’s how we address your key challenges:

- Finding the Right Partners: We offer a diverse range of business partnership types, from strategic alliances to distribution partnerships, all in one place.

- Building Trustworthy Relationships: We share proven strategies for building and maintaining effective partnerships.

- Negotiating Favorable Agreements: Access templates and guides to help you create partnership agreements that benefit all parties involved.

- Managing Long-Term Partnerships: Our resources provide advice on how to manage and sustain your partnerships over the long term.

- Measuring Partnership Effectiveness: We offer tools and methods to measure the impact of your partnerships on your bottom line.

- Discovering New Opportunities: Stay updated with the latest trends and opportunities in the partnership landscape.

Don’t let the complexities of net income calculation and partnership building hold you back. Visit income-partners.net today to explore partnership opportunities, learn effective strategies, and connect with potential partners in the USA.

Address: 1 University Station, Austin, TX 78712, United States

Phone: +1 (512) 471-3434

Website: income-partners.net

9. Conclusion

Calculating net income from the balance sheet is essential for understanding a company’s profitability and financial health. Accurate net income calculations inform better financial planning, strategic decisions, and investor attraction.

10. FAQs

10.1. Can you calculate net income directly from the balance sheet?

No, net income cannot be calculated directly from the balance sheet. The balance sheet provides a snapshot of a company’s assets, liabilities, and equity at a specific time. Net income is derived from the income statement, which reflects performance over a period.

10.2. How does the balance sheet relate to calculating net income?

The balance sheet offers context for interpreting net income by showing changes in equity and reflecting the impact of expenses like depreciation.

10.3. What information from the income statement is needed to calculate net income?

You need total revenue, COGS, operating expenses, interest expense, and taxes.

10.4. Is there a formula to calculate net income using the income statement?

Yes, the formula is:

Net Income = Total Revenue – Total Expenses

10.5. How can I find the income statement to calculate net income?

The income statement is typically in a company’s annual report or financial filings, available on their investor relations website or financial databases.