Are you looking to understand your business’s profitability? How To Create An Income Statement In Excel is essential for tracking revenue, expenses, and overall financial performance. At income-partners.net, we provide the tools and knowledge you need to create accurate income statements and connect with strategic partners to boost your income. By mastering income statement creation, you’ll be better equipped to make informed decisions and drive growth. Discover the power of financial statements and how they can lead to lucrative partnerships today!

1. Understanding the Income Statement

What is an income statement and why is it important for businesses? An income statement, also known as a profit and loss (P&L) statement or revenue statement, summarizes a company’s financial performance over a specific period, typically a month, quarter, or year. It is crucial for assessing profitability and making informed business decisions. According to research from the University of Texas at Austin’s McCombs School of Business, businesses that regularly analyze their income statements are better equipped to identify trends, manage costs, and improve overall financial health.

The income statement provides a dynamic view of financial activities, showing revenue, expenses, gains, and losses. Unlike a balance sheet, which offers a snapshot of a company’s financial position at a single point in time, the income statement shows activity over a period, allowing for period-over-period comparisons.

Key benefits of producing an income statement include:

- Tracking sales improvements and their impact on profitability.

- Identifying increases in the cost of goods relative to sales.

- Evaluating the effects of expense cuts on profitability.

- Pinpointing areas for spending reductions and growth opportunities.

- Assessing overall profit improvement.

For management, it provides a clear picture of revenue and expenses, helping to manage costs better. Investors use it to assess profitability and operational efficiency, while lenders determine the company’s ability to cover debt obligations.

2. Income Statement Template: Your Starting Point

Need a reliable tool? Download our free income statement templates to simplify your financial reporting process. These templates are designed to help you quickly and accurately create income statements, whether you’re a small business owner or a seasoned financial professional.

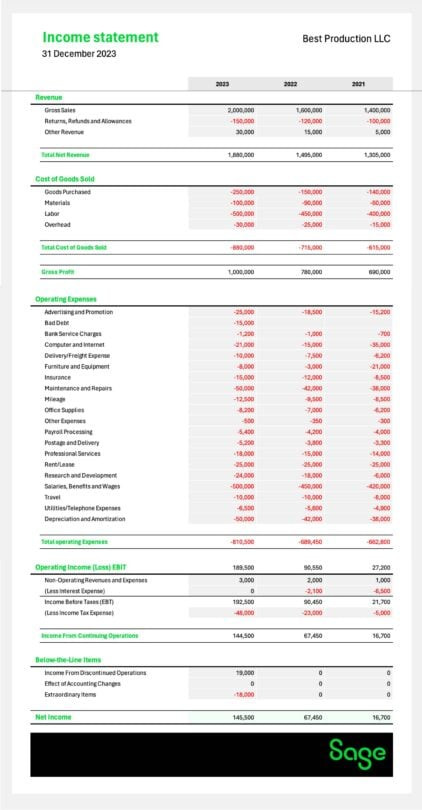

Example of an income statement template

Example of an income statement template

Alt Text: A single-step income statement template showing revenue, expenses, and net income calculations.

3. Key Components of an Income Statement

What elements are essential in an income statement? An income statement typically includes several key components: revenue, cost of goods sold (COGS), gross profit, operating expenses, depreciation & amortization expense, operating income (EBIT), non-operating revenues/expenses, earnings before tax (EBT), income from continuing operations, below-the-line items, and net income. Each component provides valuable insights into a company’s financial performance.

Let’s break down each component:

| Component | Description |

|---|---|

| Revenue | The total income earned from the company’s primary business activities before any deductions. |

| Cost of Goods Sold (COGS) | Direct costs related to producing goods or services, including materials and direct labor. |

| Gross Profit | Revenue minus COGS, showing profit before operating expenses. |

| Operating Expenses | Costs for general business operations, such as salaries, marketing, and rent. |

| Depreciation & Amortization | The decrease in value of tangible assets (depreciation) and intangible assets (amortization) over time. |

| Operating Income (EBIT) | Earnings Before Interest and Taxes, calculated by subtracting operating expenses from gross profit. |

| Non-Operating Revenues/Expenses | Income or expenses from activities outside the primary business, such as investments or interest payments. |

| Earnings Before Tax (EBT) | Income from all operations minus all expenses before taxes. |

| Income from Continuing Operations | Profit after tax from the company’s regular business activity, excluding discontinued operations or extraordinary items. |

| Below-the-Line Items | Extraordinary costs not part of the core business, such as income from discontinued operations or the effect of accounting changes. |

| Net Income | The final profit or loss after deducting all expenses and taxes, representing the total profit recorded during the period. |

4. Diving Deeper: Key Income Statement Components Explained

What details should you know about each component? To effectively analyze an income statement, understanding the intricacies of each component is essential. Here’s an in-depth look at each:

4.1. Revenue: The Top Line

What does revenue represent on the income statement? Revenue, often referred to as sales or income received, is the starting point of the income statement. It represents the total amount of money a company earns from its primary business activities, such as selling goods or providing services, before any costs or expenses are deducted.

Key Considerations for Revenue:

- Primary Business Activity: Revenue should primarily reflect income from the company’s core operations.

- Before Deductions: It is the gross amount, not accounting for any returns, discounts, or allowances.

- Non-Operating Revenue: In some cases, other revenues like interest income might be listed here, particularly in a single-step income statement. In a multi-step statement, these are shown after Operating Income (EBIT).

4.2. Cost of Goods Sold (COGS): Direct Production Costs

What does COGS entail, and why is it significant? Cost of Goods Sold (COGS) includes all direct costs associated with the production of goods or services. This is a critical component in a multi-step income statement, providing insights into the efficiency of production.

Key Components of COGS:

- Direct Materials: Raw materials used in production.

- Direct Labor: Wages paid to workers directly involved in the production process.

- Manufacturing Overhead: Indirect costs such as factory rent, utilities, and depreciation of production equipment.

For Service-Based Companies:

- COGS may include costs related to external contractors or direct service delivery expenses.

Understanding COGS is vital for calculating gross profit, which reflects how efficiently a company manages its production costs.

4.3. Gross Profit: The Core Business Earnings

How is gross profit calculated, and what does it reveal? Gross Profit is calculated by subtracting COGS from revenue. This figure shows how much a company earns from its core business operations before considering operating expenses.

Formula:

Gross Profit = Revenue - COGSImportance of Gross Profit:

- Efficiency Indicator: Gross profit indicates how efficiently a company manages its production costs.

- Core Business Performance: It reflects earnings from the primary business activities, excluding overhead and administrative costs.

4.4. Operating Expenses: Day-to-Day Business Costs

What costs are included in operating expenses? Operating expenses encompass all business costs not directly related to the production of goods or services. These are necessary for the general operation of the business and include:

- Salaries: Wages of non-production staff.

- Marketing Expenses: Costs associated with advertising and promotional activities.

- Rent: Payment for office or facility space.

- Utilities: Expenses for electricity, water, and other utilities.

- Administrative Costs: General office supplies and administrative support expenses.

4.5. Depreciation & Amortization Expense: Accounting for Asset Value

How do depreciation and amortization impact the income statement? Depreciation and amortization account for the decrease in the value of tangible and intangible assets over time.

Depreciation:

- Definition: The allocation of the cost of a tangible asset (e.g., buildings, machinery) over its useful life.

- Purpose: To match the cost of the asset with the revenue it generates over its lifespan.

- Methods: Straight-line, declining balance, units of production.

Amortization:

- Definition: The process of spreading the cost of intangible assets (e.g., patents, copyrights, software) over their useful life.

- Example: A patent valid for ten years would have its cost divided by ten, with each portion charged over the ten-year period.

Significance:

- Provide a more accurate financial view by considering the cost of long-term assets.

- Reduce taxable income as these expenses are tax-deductible.

4.6. Operating Income (EBIT): Management Efficiency Indicator

What does EBIT tell you about a company’s performance? Operating Income, or Earnings Before Interest and Taxes (EBIT), is calculated by subtracting operating expenses from gross profit.

Formula:

EBIT = Gross Profit - Operating ExpensesImportance of EBIT:

- Management Efficiency: It reflects how efficiently management is running the company profitably.

- Core Business Profitability: It shows how much gross profit is consumed by operating expenses.

4.7. Non-Operating Revenues, Expenses, Gains, Losses: Secondary Activities

What falls under non-operating items on the income statement? Non-operating revenues and expenses include income and costs from activities outside the company’s primary business operations.

Non-Operating Revenues:

- Investment Income: Income from investments in stocks, bonds, or other securities.

- Rental Income: Income from renting out properties.

- Gains from Asset Sales: Profits from selling assets not used in the main line of business.

Non-Operating Expenses:

- Interest Paid on Debt: Costs of borrowing money.

- Losses from Lawsuits: Expenses incurred from legal battles.

- Losses on Disposal of Assets: Losses from selling assets.

Gains and Losses:

- Events such as the sale of investment securities or real estate, foreign exchange differences, or restructuring costs.

These items are listed separately to provide a clear distinction between core business activities and incidental financial activities.

4.8. Earnings Before Tax (EBT): Pre-Tax Profitability

How does EBT help in comparing company profitability? Earnings Before Tax (EBT), or Pre-Tax Income, represents the income from the company’s main and other operations minus all expenses before taxes are deducted.

Formula:

EBT = Total Revenue - Total Expenses (including operating and non-operating)Importance of EBT:

- Profitability Comparison: Useful for comparing the profitability of companies, especially when tax rates differ.

- Income Tax Calculation: Serves as the starting point for calculating income tax expense and net income.

4.9. Income from Continuing Operations: Core Business Sustainability

What does this line item signify for a company’s future? Income from Continuing Operations shows the profit after tax and the net income from the company’s regular business activity. It excludes profits or losses from discontinued operations, extraordinary items, and other non-recurring events.

Significance:

- Sustainability Indicator: Reflects the profitability and sustainability of the company’s primary business activities.

- Excludes Irregular Items: Provides a clear view of the company’s ongoing operational success.

4.10. Below-the-Line Items: Extraordinary Costs

Why are below-the-line items separated on the income statement? Below-the-Line items include any extraordinary costs for a business that are not a part of the core activities of the business. These are highlighted separately to avoid skewing the perception of the company’s operational effectiveness.

Key Items:

- Income from Discontinued Operations: Income from goods or services that were discontinued during the accounting period.

- Effect of Accounting Changes: Changes in accounting policy or tax laws during the period.

- Extraordinary Items: Irregular items such as paying a penalty to exit a contract.

4.11. Net Income: The Bottom Line

What does net income ultimately represent for a business? Net Income is the bottom line of the income statement, calculated by taking the operating income and adding/subtracting any other income/expenses. Taxes are then deducted to arrive at the net income, representing the total profit or loss the company recorded during the period.

Formula:

Net Income = EBT - Income Tax ExpenseImportance:

- Total Profitability: Represents the overall financial performance of the company during the period.

- Key Metric: Widely used by investors, analysts, and stakeholders to assess a company’s financial health.

Understanding these key components is crucial for accurately creating and interpreting income statements. Let’s explore the practical steps of creating an income statement in Excel.

5. Step-by-Step Guide: Creating an Income Statement in Excel

How can you create an income statement in Excel using our template? Creating an income statement in Excel can be straightforward with the right template and guidance. Here’s a step-by-step guide to help you through the process.

5.1. Select a Template: Multi-Step or Single-Step

Which template suits your business needs best? Depending on your business size and complexity, choose either a multi-step or single-step income statement template from our downloadable resource.

- Multi-Step Income Statement: Ideal for larger companies with complex operations. It provides a detailed breakdown of revenues and expenses.

- Single-Step Income Statement: Suitable for smaller businesses, offering a simpler, more straightforward view of financial performance.

5.2. Set Up the Excel Sheet

How do you prepare the Excel sheet for your income statement? Open the selected template in Excel. You’ll notice pre-formatted rows and columns. The gray boxes are where you’ll input your data; other boxes contain formulas that automatically calculate results.

Key Preparations:

- Reporting Period: At the top of the statement, specify the reporting period (year, quarter, or month).

- Columns: Copy and paste the column for additional periods if you want to compare performance over time.

5.3. Input Revenue Data

Where do you enter your revenue figures in the template? In the revenue section, input all revenue and sales figures. You can create a statement for a specific area or product.

Example:

| Revenue Source | Amount |

|---|---|

| Sales Revenue | $500,000 |

| Service Revenue | $200,000 |

| Total Revenue | $700,000 |

Note: Returns, Refunds, and Allowances are entered as negative numbers to reduce total revenue accurately.

5.4. Calculate Cost of Goods Sold (COGS) (Multi-Step Only)

How do you break down COGS in a multi-step income statement? If you’re using a multi-step income statement, input the COGS divided into categories such as purchases, materials, labor, and overhead.

Example:

| COGS Category | Amount |

|---|---|

| Purchases | $150,000 |

| Materials | $50,000 |

| Labor | $100,000 |

| Overhead | $25,000 |

| Total COGS | $325,000 |

5.5. Compute Gross Profit (Multi-Step Only)

How does Excel automatically calculate gross profit? Gross Profit is automatically calculated by subtracting the total cost of goods sold from the total net revenue. The formula in Excel will handle this calculation for you.

Excel Formula Example:

=SUM(Total Revenue - Total COGS)5.6. Enter Operating Expenses

Where do you list all your operating expenses? Input all operating expenses into the relevant categories. You can add extra rows or rename rows as needed to fit your business’s specific expenses.

Example:

| Operating Expense | Amount |

|---|---|

| Salaries | $80,000 |

| Rent | $20,000 |

| Marketing | $15,000 |

| Utilities | $5,000 |

| Total Operating Expenses | $120,000 |

5.7. Calculate Operating Income (EBIT) (Multi-Step Only)

How is EBIT derived from gross profit and operating expenses? Operating Income (EBIT) is calculated by subtracting total operating expenses from gross profit.

Excel Formula Example:

=SUM(Gross Profit - Total Operating Expenses)5.8. Input Non-Operating Revenues and Expenses (Multi-Step Only)

What items are included in the non-operating section? Input income from investments, rental income, or gains from the sale of assets not used in the main line of business, along with interest paid on debt, losses from lawsuits, or losses on the disposal of assets.

Example:

| Non-Operating Item | Amount |

|---|---|

| Investment Income | $10,000 |

| Interest Expense | ($5,000) |

| Total Non-Operating Items | $5,000 |

5.9. Determine Income Before Taxes (EBT) (Multi-Step Only)

How is EBT calculated in the multi-step template? Income Before Taxes (EBT) is calculated by subtracting non-operating revenues and expenses and interest expense from operating income EBIT.

Excel Formula Example:

=SUM(Operating Income + Total Non-Operating Items)5.10. Calculate Income from Continuing Operations

How do you arrive at income from continuing operations? Income from continuing operations is calculated by subtracting income tax expense from Income Before Taxes.

Excel Formula Example:

=SUM(Income Before Taxes - Income Tax Expense)5.11. Add Below-the-Line Items

What specific entries are included below the line? Input the following below-the-line items:

- Income from Discontinued Operations: Income from goods or services that were discontinued.

- Effect of Accounting Changes: Any changes in accounting policy or tax laws.

- Extraordinary Items: Irregular items such as penalties.

Example:

| Below-the-Line Item | Amount |

|---|---|

| Discontinued Operations | $2,000 |

| Accounting Changes | ($1,000) |

| Total Below-the-Line Items | $1,000 |

5.12. Compute Net Income

What is the final step in completing the income statement? Net Income is calculated by adding together all Income from Continuing Operations and all Below-The-Line items.

Excel Formula Example:

=SUM(Income from Continuing Operations + Total Below-the-Line Items)5.13. For Single-Step Income Statement Users

How does the process differ for a single-step income statement? If you’re using the single-step income statement template, the process is similar but streamlined:

- Input all revenues: Include sales, services, and interest.

- Calculate Total Net Revenue: Sum all revenue and subtract returns, refunds, and allowances.

- Enter Operating Expenses: List all expenses in the appropriate categories.

- Calculate Net Income Before Taxes: Subtract total operating expenses from total net revenue.

- Determine Income from Continuing Operations: Subtract income tax expense from income before taxes.

- Add Below-the-Line Items: Include discontinued operations, accounting changes, and extraordinary items.

- Compute Net Income: Add income from continuing operations and total below-the-line items.

Following these steps, you can effectively create an income statement in Excel, providing you with valuable insights into your company’s financial performance.

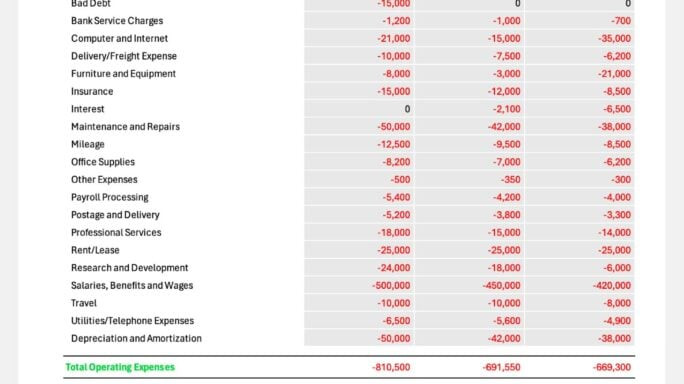

Example of a multi-step income statement template

Example of a multi-step income statement template

Alt Text: A multi-step income statement template showcasing revenue, COGS, gross profit, operating expenses, and net income.

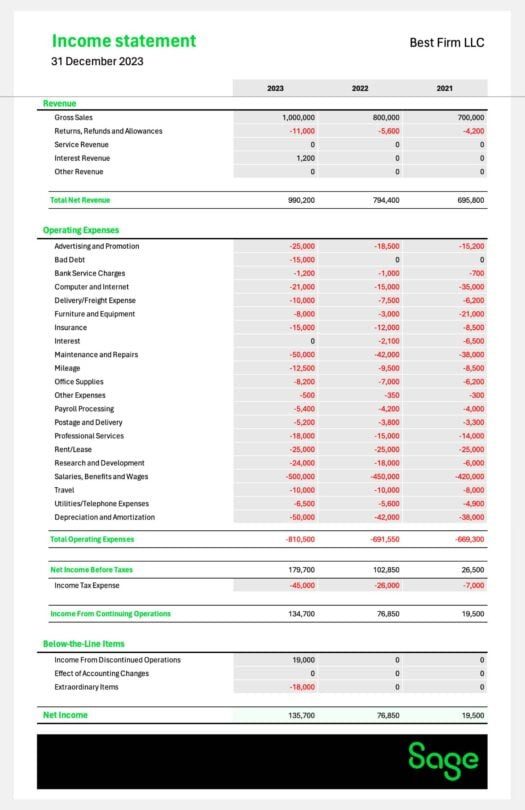

Example of a single-step income statement template

Example of a single-step income statement template

Alt Text: A single-step income statement template illustrating a straightforward calculation of net income.

6. Navigating Differences: Income Statement Variations

What are the key differences to consider when preparing income statements? Several variations exist in how income statements can be prepared and presented. Understanding these differences is crucial for accurate financial reporting. Let’s explore the key variations:

6.1. Income Statement vs. Statement of Comprehensive Income

What additional information does a statement of comprehensive income provide? A statement of comprehensive income can be presented as one single document or as two separate statements: the income statement and a comprehensive income statement.

- Single Statement: A continuous statement of income.

- Two Separate Statements: An income statement and a separate statement of comprehensive income.

The statement of comprehensive income includes other revenue and expenses not yet realized, providing a fuller picture of a company’s total financial performance. This extended statement offers a more in-depth view of a company’s financial position.

6.2. Nature vs. Function: Classifying Operating Expenses

How can operating expenses be categorized differently on the income statement? In the income statement, operating expenses can be categorized as either “nature” or “function.” Each method provides a different perspective and can be more useful for certain types of financial analysis or businesses.

- Function: Relates to cost of sales, distribution costs, and administrative expenses. It offers insights into operational efficiency by showing how expenses relate to specific operational areas.

- Nature: Relates to raw materials, wages, and depreciation. It provides clarity about the actual economic elements impacting financial results.

6.3. Single-Step vs. Multi-Step Income Statement: Presentation Styles

Which format—single-step or multi-step—best suits your business? An income statement can be presented in two ways: single-step or multi-step. Both provide the net income, but they differ slightly in layout and detail.

- Single-Step Income Statement: More straightforward, showing revenue and expenses with a simple one-step equation. Typically used by smaller businesses.

- Multi-Step Income Statement: Provides a more detailed view by breaking down operating and non-operating revenues and expenses, highlighting key financial performance components such as gross profit, operating income, and net income. Preferred by larger companies with more complex business operations.

7. Best Practices and Tips

What are some best practices for creating accurate and insightful income statements? Creating an income statement isn’t just about filling in numbers; it’s about understanding the story those numbers tell. Here are some best practices and tips to ensure accuracy and insightfulness:

- Consistency: Use consistent accounting methods and reporting periods to ensure comparability.

- Accuracy: Double-check all data entries to minimize errors.

- Regular Review: Review income statements regularly (monthly, quarterly, annually) to identify trends and potential issues.

- Benchmarking: Compare your income statement with industry benchmarks to assess your company’s performance relative to competitors.

- Professional Advice: Consult with a qualified accountant or financial advisor for complex issues or if you’re unsure about any aspect of income statement preparation.

- Stay Updated: Keep abreast of changes in accounting standards and regulations to ensure compliance.

- Use Technology: Leverage accounting software like Sage Intacct for automated and accurate income statement preparation.

By following these best practices, you can ensure that your income statements are reliable, accurate, and provide valuable insights for decision-making.

8. How income-partners.net Can Help You

Looking for partnership opportunities to boost your income? At income-partners.net, we offer a range of resources and opportunities to help you enhance your financial performance:

- Strategic Partnerships: Connect with businesses and entrepreneurs to create mutually beneficial partnerships.

- Financial Insights: Access expert advice and resources on financial management and reporting.

- Customized Solutions: Tailored strategies to meet your specific business needs and goals.

Visit income-partners.net to explore partnership opportunities, discover effective relationship-building strategies, and connect with potential partners across the USA. Maximize your income potential and drive sustainable growth with our comprehensive resources.

Address: 1 University Station, Austin, TX 78712, United States

Phone: +1 (512) 471-3434

Website: income-partners.net

9. FAQs: Income Statement Essentials

What are some frequently asked questions about income statements? Here are some FAQs to provide further clarity on income statements:

9.1. Do all businesses have to produce an income statement?

Is an income statement mandatory for all types of businesses? Almost all businesses are expected to produce an income statement, though the specific requirements can vary depending on the size and legal structure of the business. Even when not legally required, maintaining an income statement is a best practice for effective business management.

9.2. Income Statement vs. Balance Sheet: What’s the Difference?

How do these two financial statements differ in purpose and scope? An income statement measures a company’s financial performance over a specific period, while a balance sheet provides a snapshot of a company’s financial condition at a particular point in time.

9.3. What is the difference between operating revenue and non-operating revenue?

How do these revenue types impact the overall financial picture? Operating revenue comes from a company’s core activities, such as the sale of products or services. Non-operating revenue comes from other sources, like interest income or rental income.

9.4. What are the differences between US GAAP and IFRS for income statements?

How do these accounting standards affect income statement presentation? While similar, GAAP and IFRS have some important differences, including layout requirements, expense classification, and how unusual items are treated.

9.5. How often should a business prepare an income statement?

What is the recommended frequency for income statement preparation? Businesses should ideally prepare income statements at least quarterly, if not monthly, to stay on top of their financial performance.

9.6. What if I have discontinued operations?

How do I handle discontinued operations on my income statement? Discontinued operations should be listed as a below-the-line item to avoid skewing the perception of the company’s ongoing operational effectiveness.

9.7. How can an income statement help in securing business loans?

Why is an income statement important when applying for loans? Lenders often require an income statement to assess a company’s ability to generate enough profit to cover debt obligations.

9.8. Is it necessary to include non-cash expenses like depreciation in the income statement?

Why are non-cash expenses included in the income statement? Yes, depreciation and amortization are essential to show an accurate financial view of a company by considering the cost of long-term assets.

9.9. What is the significance of the gross profit margin?

Why is it important to calculate and track the gross profit margin? The gross profit margin (Gross Profit / Revenue) indicates how efficiently a company manages its production costs and is a key metric for assessing profitability.

9.10. What are the implications of negative net income?

What does it mean if a company reports a net loss? A negative net income (net loss) indicates that a company’s expenses exceeded its revenues during the reporting period, which could signal financial distress.

10. Take Action: Enhance Your Financial Strategy Today

Ready to elevate your business’s financial strategy? Discover the power of strategic partnerships and financial insights at income-partners.net. Explore our resources, connect with potential partners, and take your business to new heights. Visit our website today to get started!

By understanding and utilizing income statements, you can gain valuable insights into your business’s financial health and make informed decisions that drive growth and success. Whether you’re a small business owner or a seasoned financial professional, mastering the art of income statement creation is essential for achieving your financial goals. Let income-partners.net be your guide on this journey.