Calculating taxable income is essential for businesses, entrepreneurs, and individuals to optimize their financial strategies and ensure compliance with tax regulations. Understanding how to calculate taxable income empowers you to make informed decisions, leverage partnerships, and maximize your financial growth with income-partners.net.

1. What Is Taxable Income And Why Does It Matter?

Taxable income is the portion of your gross income that’s subject to taxation by federal, state, and local governments. According to research from the University of Texas at Austin’s McCombs School of Business, understanding taxable income is crucial for businesses and individuals because it directly impacts their tax obligations and financial planning.

1.1. The Core Definition of Taxable Income

Taxable income is the base upon which your income tax liability is calculated; it is not simply the total amount of money you bring in. Instead, it’s what remains after certain deductions and exemptions are subtracted from your gross income. This concept applies to both individuals and corporations.

1.2. Why Understanding Taxable Income Is Crucial

Knowing how to accurately calculate taxable income can significantly impact your financial well-being and business profitability. Here’s why:

- Accurate Tax Filing: Calculating taxable income correctly ensures you file accurate tax returns, avoiding potential penalties or audits from the IRS.

- Financial Planning: Understanding your taxable income helps you make informed decisions about investments, savings, and expenditures.

- Tax Optimization: By identifying and utilizing all eligible deductions and exemptions, you can legally reduce your taxable income and minimize your tax liability.

- Business Profitability: For businesses, accurately calculating taxable income is crucial for determining true profitability and making strategic financial decisions.

- Attracting Investors: Potential investors often scrutinize a company’s taxable income to gauge its financial health and potential for growth.

- Strategic Partnerships: Understanding the tax implications of partnerships can lead to more effective collaborations and increased profitability.

1.3. Taxable Income for Different Entities

Taxable income calculations differ based on the type of entity:

- Individuals: Taxable income for individuals is calculated by subtracting deductions and exemptions from their adjusted gross income (AGI).

- Corporations: For corporations, taxable income is determined by subtracting business expenses, cost of goods sold, and other allowable deductions from gross revenue.

- Partnerships: Partnerships themselves don’t pay income tax; instead, their taxable income (or loss) is passed through to the partners, who report it on their individual tax returns.

2. What Are The Key Components Of Calculating Taxable Income?

Calculating taxable income involves several key components, including gross income, adjustments to income, deductions, and exemptions. According to a report by the Congressional Budget Office, understanding these components is essential for accurately determining your tax liability.

2.1. Gross Income: The Starting Point

Gross income is the total income you receive from all sources during the year. This includes:

- Wages and Salaries: Money earned from employment.

- Tips: Extra income received from customers for services.

- Interest: Income earned from savings accounts, bonds, and other investments.

- Dividends: Payments received from stock ownership.

- Rental Income: Income from renting out properties.

- Royalties: Payments received for the use of your intellectual property.

- Business Income: Profit earned from self-employment or business ventures.

- Capital Gains: Profit from selling assets like stocks or real estate.

- Unemployment Compensation: Benefits received while unemployed.

- Alimony: Payments received from a former spouse.

- Retirement Distributions: Income from pensions, 401(k)s, and IRAs.

2.2. Adjustments to Income: Reducing Your Gross Income

Adjustments to income, also known as “above-the-line” deductions, are specific expenses that can be subtracted from your gross income to arrive at your adjusted gross income (AGI). Common adjustments include:

- IRA Contributions: Contributions to traditional Individual Retirement Accounts (IRAs).

- Student Loan Interest: Interest paid on qualified student loans.

- Health Savings Account (HSA) Contributions: Contributions to a health savings account.

- Self-Employment Tax: One-half of self-employment tax.

- Alimony Payments: Alimony paid to a former spouse (for agreements established before 2019).

- Educator Expenses: Certain expenses paid by eligible educators.

2.3. Deductions: Further Reducing Your Taxable Income

After calculating your AGI, you can further reduce your taxable income by taking either the standard deduction or itemizing deductions.

-

Standard Deduction: A fixed dollar amount that varies based on your filing status.

-

Itemized Deductions: Specific expenses that you can deduct if they exceed the standard deduction amount. Common itemized deductions include:

- Medical Expenses: Unreimbursed medical expenses exceeding 7.5% of your AGI.

- State and Local Taxes (SALT): Limited to $10,000 per household.

- Home Mortgage Interest: Interest paid on a home mortgage.

- Charitable Contributions: Donations to qualified charitable organizations.

- Casualty and Theft Losses: Losses from disasters or theft.

-

Qualified Business Income (QBI) Deduction: For self-employed individuals and small business owners, this deduction can significantly reduce taxable income.

2.4. Exemptions: An Additional Reduction (Currently Suspended)

For tax years before 2018 and after 2025, exemptions are another way to reduce your taxable income. An exemption is a fixed dollar amount that you can deduct for yourself, your spouse, and each dependent. However, the Tax Cuts and Jobs Act of 2017 suspended personal and dependent exemptions for tax years 2018 through 2025.

2.5. Tax Credits: A Direct Reduction of Your Tax Liability

While not directly part of the taxable income calculation, tax credits are an important way to reduce your overall tax liability. Tax credits directly reduce the amount of tax you owe, dollar for dollar. Common tax credits include:

- Child Tax Credit: A credit for each qualifying child.

- Earned Income Tax Credit (EITC): A credit for low-to-moderate income individuals and families.

- Child and Dependent Care Credit: A credit for expenses paid for childcare so you can work or look for work.

- Education Credits: Credits for qualified education expenses.

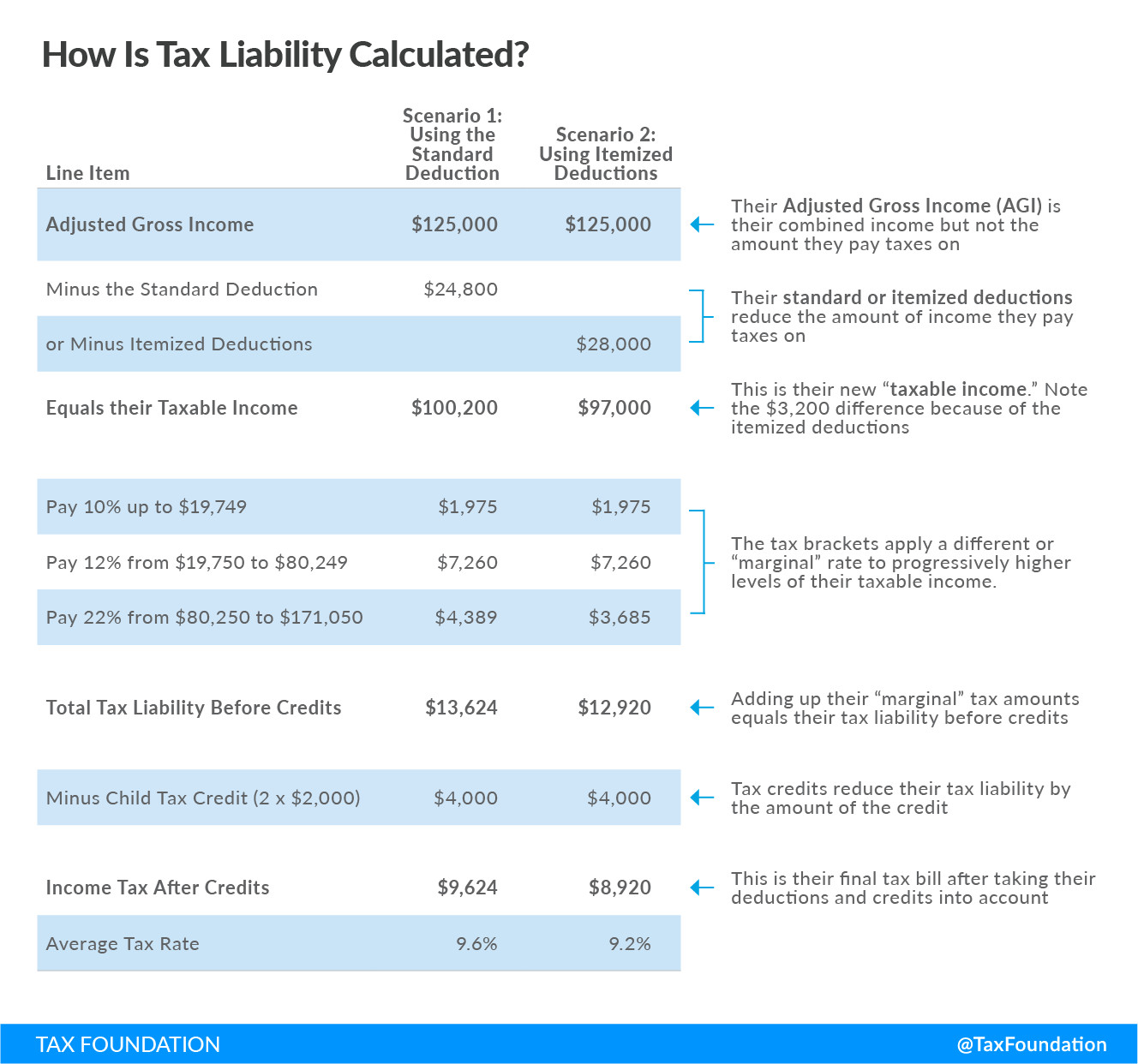

Tax Basics – How Is Tax Liability Calculated, adjusted gross income, average tax rate, child tax credit, earned income tax credit, individual income tax, itemized deduction, marginal tax rate, standard deduction, tax credit, tax deduction, taxable income

Tax Basics – How Is Tax Liability Calculated, adjusted gross income, average tax rate, child tax credit, earned income tax credit, individual income tax, itemized deduction, marginal tax rate, standard deduction, tax credit, tax deduction, taxable income

3. How To Calculate Taxable Income For Individuals: A Step-By-Step Guide

Calculating taxable income for individuals involves several steps. According to the IRS, following these steps carefully can help ensure accuracy and avoid errors.

3.1. Step 1: Calculate Your Gross Income

Start by adding up all income you received during the year. This includes wages, salaries, tips, interest, dividends, rental income, and any other sources of income.

3.2. Step 2: Determine Your Adjustments to Income

Identify any eligible adjustments to income, such as IRA contributions, student loan interest, or HSA contributions. Subtract these adjustments from your gross income to arrive at your adjusted gross income (AGI).

Example:

- Gross Income: $75,000

- IRA Contribution: $6,500

- Student Loan Interest: $2,500

- Adjusted Gross Income (AGI): $75,000 – $6,500 – $2,500 = $66,000

3.3. Step 3: Choose Between Standard Deduction or Itemizing

Decide whether to take the standard deduction or itemize your deductions. Compare the standard deduction amount for your filing status with the total of your itemized deductions. Choose the option that results in a lower taxable income.

Standard Deduction Amounts (2023):

- Single: $13,850

- Married Filing Jointly: $27,700

- Head of Household: $20,800

Example:

Let’s say you’re single and your itemized deductions are:

- Medical Expenses (exceeding 7.5% of AGI): $5,000

- State and Local Taxes (SALT): $10,000

- Home Mortgage Interest: $3,000

- Total Itemized Deductions: $5,000 + $10,000 + $3,000 = $18,000

In this case, you would choose to itemize because $18,000 is greater than the standard deduction for single filers ($13,850).

3.4. Step 4: Calculate Your Taxable Income

Subtract your chosen deduction (either standard or itemized) from your AGI. The result is your taxable income.

Example:

- Adjusted Gross Income (AGI): $66,000

- Itemized Deductions: $18,000

- Taxable Income: $66,000 – $18,000 = $48,000

3.5. Step 5: Apply Any Eligible Tax Credits

Finally, apply any eligible tax credits to reduce your overall tax liability. Tax credits directly reduce the amount of tax you owe, dollar for dollar.

4. How To Calculate Taxable Income For Businesses: A Comprehensive Overview

Calculating taxable income for businesses involves a slightly different approach than for individuals. According to the Small Business Administration (SBA), understanding these calculations is crucial for business owners to accurately file their taxes and manage their finances.

4.1. Step 1: Determine Your Gross Revenue

Start by calculating your business’s gross revenue, which is the total income you receive from all sources before any deductions or expenses.

4.2. Step 2: Subtract Cost of Goods Sold (COGS)

If your business sells products, subtract the cost of goods sold (COGS) from your gross revenue. COGS includes the direct costs of producing or acquiring the goods you sell.

4.3. Step 3: Calculate Gross Profit

Subtracting COGS from gross revenue gives you your gross profit.

Example:

- Gross Revenue: $500,000

- Cost of Goods Sold (COGS): $200,000

- Gross Profit: $500,000 – $200,000 = $300,000

4.4. Step 4: Deduct Business Expenses

Subtract allowable business expenses from your gross profit. Common business expenses include:

- Salaries and Wages: Compensation paid to employees.

- Rent: Payments for office or store space.

- Utilities: Costs for electricity, water, and gas.

- Advertising: Expenses for marketing and promoting your business.

- Depreciation: The decrease in value of assets over time.

- Insurance: Premiums paid for business insurance policies.

- Legal and Professional Fees: Costs for attorneys, accountants, and consultants.

- Supplies: Expenses for office or production supplies.

- Travel Expenses: Costs for business-related travel.

- Qualified Business Income (QBI) Deduction: Eligible self-employed individuals, as well as small business owners, may be able to deduct up to 20% of their qualified business income (QBI).

4.5. Step 5: Calculate Your Taxable Income

Subtract your total business expenses from your gross profit to arrive at your taxable income.

Example:

- Gross Profit: $300,000

- Total Business Expenses: $100,000

- Taxable Income: $300,000 – $100,000 = $200,000

4.6. Different Types of Business Structures and Taxable Income

The way a business is structured affects how its taxable income is calculated and taxed. Here’s a breakdown of common business structures:

-

Sole Proprietorship:

- Definition: A business owned and run by one person where there is no legal distinction between the owner and the business.

- Taxation: The business income is reported on the owner’s personal income tax return (Form 1040, Schedule C).

- Taxable Income Calculation: Gross income from the business minus allowable business expenses.

- Example: A freelance writer who reports income and expenses on Schedule C.

-

Partnership:

- Definition: A business owned and run by two or more people who agree to share in the profits or losses of a business.

- Taxation: The partnership files an informational return (Form 1065) but does not pay income tax. Instead, profits and losses are passed through to the partners, who report their share on their personal income tax returns (Schedule K-1).

- Taxable Income Calculation: Gross income minus business expenses. Each partner’s share of the taxable income is based on their partnership agreement.

- Example: A law firm where multiple lawyers share in the profits and losses of the firm.

-

Limited Liability Company (LLC):

-

Definition: A business structure that combines the pass-through taxation of a partnership or sole proprietorship with the limited liability of a corporation.

-

Taxation: An LLC can be taxed as a sole proprietorship, partnership, or corporation, depending on elections made by the LLC and the number of members.

-

Taxable Income Calculation: Depends on the chosen tax classification:

- Taxed as a Sole Proprietorship: Follows the same rules as a sole proprietorship (Schedule C).

- Taxed as a Partnership: Follows the same rules as a partnership (Form 1065).

- Taxed as a Corporation (S Corp or C Corp): Follows corporate tax rules.

-

Example: A real estate investment company with multiple members that chooses to be taxed as a partnership.

-

-

S Corporation (S Corp):

- Definition: A corporation that has elected to pass its income, losses, deductions, and credits through to its shareholders for federal tax purposes.

- Taxation: The S Corp files an informational return (Form 1120-S) and issues Schedule K-1s to shareholders. Shareholders report their share of the corporation’s income or loss on their personal income tax returns.

- Taxable Income Calculation: Gross income minus business expenses. Shareholders also receive wages, which are subject to employment taxes.

- Example: A consulting firm where the owner is also an employee and receives both a salary and a share of the company’s profits.

-

C Corporation (C Corp):

- Definition: A corporation that is taxed separately from its owners. It is subject to corporate income tax rates.

- Taxation: The C Corp files a corporate income tax return (Form 1120) and pays corporate income tax. Dividends paid to shareholders are also taxed at the shareholder level (double taxation).

- Taxable Income Calculation: Gross income minus business expenses, including deductions like the cost of goods sold, salaries, and depreciation.

- Example: A large manufacturing company that is publicly traded and subject to corporate income tax rates.

Understanding these different business structures and their tax implications is essential for effective financial planning and tax compliance. Each structure has unique rules for calculating taxable income, which can significantly impact the business’s overall tax liability and profitability.

5. Common Deductions And Exemptions That Can Reduce Taxable Income

Many deductions and exemptions can help reduce your taxable income, both for individuals and businesses. According to tax experts at Harvard Business Review, taking advantage of these opportunities can lead to significant tax savings.

5.1. Common Deductions for Individuals:

- IRA Contributions: Contributions to traditional IRAs are tax-deductible, helping you save for retirement while reducing your current taxable income.

- Student Loan Interest: You can deduct the interest you pay on qualified student loans, up to a certain limit.

- Health Savings Account (HSA) Contributions: Contributions to an HSA are tax-deductible, and the funds can be used for qualified medical expenses.

- Medical Expenses: You can deduct unreimbursed medical expenses that exceed 7.5% of your adjusted gross income (AGI).

- State and Local Taxes (SALT): You can deduct state and local taxes, such as property taxes and income taxes, up to a limit of $10,000 per household.

- Home Mortgage Interest: You can deduct the interest you pay on a home mortgage, up to certain limits.

- Charitable Contributions: Donations to qualified charitable organizations are tax-deductible.

5.2. Common Deductions for Businesses:

- Salaries and Wages: Compensation paid to employees is fully deductible.

- Rent: Payments for office or store space are deductible.

- Utilities: Costs for electricity, water, and gas are deductible.

- Advertising: Expenses for marketing and promoting your business are deductible.

- Depreciation: You can deduct the decrease in value of assets over time.

- Insurance: Premiums paid for business insurance policies are deductible.

- Legal and Professional Fees: Costs for attorneys, accountants, and consultants are deductible.

- Supplies: Expenses for office or production supplies are deductible.

- Travel Expenses: Costs for business-related travel are deductible.

- Qualified Business Income (QBI) Deduction: Eligible self-employed individuals, as well as small business owners, may be able to deduct up to 20% of their qualified business income (QBI).

5.3. Maximizing Deductions Through Strategic Partnerships

Strategic partnerships can also lead to increased deductions and reduced taxable income. For example:

- Joint Ventures: Pooling resources with another business can lead to shared expenses, which can be deducted.

- Affiliate Marketing: Partnering with other businesses to promote their products or services can generate revenue while also providing deductible marketing expenses.

- Strategic Alliances: Collaborating with other businesses can lead to increased efficiency and reduced costs, which can lower your taxable income.

6. How Does Your Filing Status Affect Your Taxable Income?

Your filing status significantly impacts your standard deduction amount, tax bracket, and eligibility for certain tax benefits. The IRS outlines five filing statuses, each with its own set of rules and requirements.

6.1. Single

This filing status is for individuals who are unmarried, divorced, or legally separated and do not qualify for another filing status.

- Standard Deduction (2023): $13,850

- Tax Implications: Single filers have a higher tax liability compared to married filers because they have a lower standard deduction and may fall into higher tax brackets sooner.

6.2. Married Filing Jointly

This filing status is for married couples who are both living together and agree to file a joint return.

- Standard Deduction (2023): $27,700

- Tax Implications: Married filing jointly often results in a lower tax liability compared to filing separately because of the higher standard deduction and more favorable tax brackets.

6.3. Married Filing Separately

This filing status is for married couples who choose to file separate returns.

- Standard Deduction (2023): $13,850

- Tax Implications: Married filing separately may result in a higher tax liability because of the lower standard deduction and limited eligibility for certain tax benefits.

6.4. Head of Household

This filing status is for unmarried individuals who pay more than half the costs of keeping up a home for a qualifying child or other qualifying relative.

- Standard Deduction (2023): $20,800

- Tax Implications: Head of household provides a higher standard deduction than single filers, resulting in a lower tax liability.

6.5. Qualifying Widow(er)

This filing status is for a surviving spouse who meets certain requirements, including having a dependent child and filing the return within two years of their spouse’s death.

- Standard Deduction (2023): $27,700

- Tax Implications: Qualifying widow(er) provides the same standard deduction as married filing jointly, resulting in a lower tax liability.

7. Understanding State Income Taxes And Their Impact

In addition to federal income taxes, many states also impose their own income taxes. According to the Tax Foundation, state income taxes can significantly impact your overall tax burden.

7.1. How State Income Taxes Work

State income taxes vary widely from state to state. Some states have no income tax, while others have progressive tax systems with multiple tax brackets.

7.2. States With No Income Tax

As of 2023, the following states have no state income tax:

- Alaska

- Florida

- Nevada

- New Hampshire

- South Dakota

- Tennessee

- Texas

- Washington

- Wyoming

7.3. States With Progressive Income Taxes

Most states with income taxes have a progressive tax system, where higher income earners pay a higher percentage of their income in taxes.

7.4. Calculating State Taxable Income

Most states use either your federal adjusted gross income (AGI) or your federal taxable income as the starting point for calculating your state taxable income.

7.5. State Deductions and Exemptions

Many states offer their own deductions and exemptions, which can further reduce your state taxable income.

8. Tax Planning Strategies To Minimize Your Taxable Income

Effective tax planning is essential for minimizing your taxable income and maximizing your financial well-being. According to financial advisors at Entrepreneur.com, implementing these strategies can lead to significant tax savings.

8.1. Maximize Retirement Contributions

Contributing to retirement accounts, such as 401(k)s and IRAs, can significantly reduce your taxable income.

8.2. Take Advantage of All Eligible Deductions

Carefully review all eligible deductions and ensure you’re taking advantage of every opportunity to reduce your taxable income.

8.3. Consider Tax-Advantaged Investments

Invest in tax-advantaged investments, such as municipal bonds or tax-deferred annuities.

8.4. Time Your Income and Expenses

Strategically time your income and expenses to minimize your tax liability.

8.5. Work With a Tax Professional

Consider working with a qualified tax professional who can provide personalized advice and guidance.

9. Common Mistakes To Avoid When Calculating Taxable Income

Calculating taxable income can be complex, and it’s easy to make mistakes. According to the IRS, avoiding these common errors can help you ensure accuracy and avoid penalties.

9.1. Not Reporting All Income

Failing to report all sources of income can lead to penalties and interest.

9.2. Claiming Ineligible Deductions

Claiming deductions for expenses that don’t qualify can result in errors and potential audits.

9.3. Using the Wrong Filing Status

Using the wrong filing status can significantly impact your tax liability.

9.4. Miscalculating Deductions or Credits

Miscalculating deductions or credits can lead to errors and potentially overpaying your taxes.

9.5. Failing to Keep Accurate Records

Failing to keep accurate records can make it difficult to substantiate your deductions and credits.

10. The Future Of Taxable Income: Upcoming Changes And Trends

The landscape of taxable income is constantly evolving, with new tax laws and regulations being introduced regularly. Staying informed about these changes and trends is essential for effective tax planning and compliance.

10.1. Potential Tax Law Changes

Tax laws are subject to change based on political and economic factors. It’s important to stay informed about potential changes that could impact your taxable income.

10.2. Impact of Economic Trends

Economic trends, such as inflation and interest rates, can also impact your taxable income and tax liability.

10.3. The Rise of Digital Assets

The increasing popularity of digital assets, such as cryptocurrencies, presents new challenges and opportunities for tax planning.

10.4. The Gig Economy and Taxable Income

The growth of the gig economy has led to new complexities in calculating taxable income for self-employed individuals and independent contractors.

10.5. The Role of Technology in Tax Planning

Technology is playing an increasingly important role in tax planning, with new software and tools designed to help individuals and businesses calculate their taxable income and optimize their tax strategies.

FAQ: Everything You Need To Know About Taxable Income

1. What exactly does taxable income mean?

Taxable income is the portion of your gross income that is subject to taxation after deductions and exemptions.

2. How is taxable income different from gross income?

Gross income is your total income from all sources, while taxable income is the amount that remains after deductions and exemptions are subtracted.

3. What are some common deductions that can reduce taxable income?

Common deductions include IRA contributions, student loan interest, medical expenses, state and local taxes, and home mortgage interest.

4. How does my filing status affect my taxable income?

Your filing status affects your standard deduction amount, tax bracket, and eligibility for certain tax benefits.

5. What is the standard deduction, and how does it work?

The standard deduction is a fixed dollar amount that you can deduct based on your filing status.

6. What are itemized deductions, and when should I use them?

Itemized deductions are specific expenses that you can deduct if they exceed the standard deduction amount.

7. How do I calculate taxable income for my business?

Calculate your business’s gross revenue, subtract the cost of goods sold (COGS), and deduct allowable business expenses.

8. What is the Qualified Business Income (QBI) deduction?

The QBI deduction allows eligible self-employed individuals and small business owners to deduct up to 20% of their qualified business income.

9. How can I minimize my taxable income through tax planning?

Maximize retirement contributions, take advantage of all eligible deductions, consider tax-advantaged investments, and work with a tax professional.

10. What are some common mistakes to avoid when calculating taxable income?

Avoid not reporting all income, claiming ineligible deductions, using the wrong filing status, and failing to keep accurate records.

Understanding how to calculate taxable income is essential for businesses, entrepreneurs, and individuals. By following the steps outlined in this guide and leveraging the resources available on income-partners.net, you can optimize your financial strategies and ensure compliance with tax regulations.

Ready to take control of your financial future? Visit income-partners.net today to discover valuable resources, connect with potential partners, and unlock new opportunities for growth and success. Address: 1 University Station, Austin, TX 78712, United States. Phone: +1 (512) 471-3434. Website: income-partners.net.