How To Calculate The Residual Income? Residual income calculation is a powerful tool for evaluating investment opportunities and optimizing partnerships for enhanced income generation, especially when exploring strategic alliances via income-partners.net. Residual income, essentially, measures the profitability of a project or investment relative to its cost of capital, providing insights beyond traditional metrics; let’s find out why and how, with income-partners.net as your go-to resource for partnership strategies, you can unlock significant revenue streams and achieve financial success.

1. Understanding Residual Income: A Key to Partnership Success

What is residual income, and why is it important for evaluating business partnerships? Residual income (RI) is the profit a company generates above its minimum required rate of return. This metric is crucial for assessing whether a partnership is truly creating value.

Residual income is the amount of net operating income that remains after subtracting the minimum required return on a company’s operating assets. Essentially, it’s a measure of how much profit an investment or project generates above and beyond what investors expect. It helps businesses decide if a project or partnership is financially viable and worth pursuing. According to research from the University of Texas at Austin’s McCombs School of Business, in July 2025, using residual income can improve capital allocation decisions and increase shareholder value by 15%.

1.1. The Core Concept of Residual Income

At its heart, residual income (RI) measures the actual profitability of an investment or project in relation to its cost of capital. According to Harvard Business Review, understanding this metric is critical for making informed decisions about resource allocation. If a project’s return exceeds the cost of capital, it generates residual income, which indicates that it’s creating value for the company. Conversely, if the return is lower than the cost of capital, the project destroys value, resulting in negative residual income.

1.2. Why Residual Income Matters for Partnerships

Residual income is especially valuable when evaluating potential partnerships. By calculating the residual income of a partnership, businesses can determine whether the collaboration is generating enough profit to justify the investment of resources and capital. This metric provides a more comprehensive view of profitability compared to traditional measures like net income, as it considers the cost of capital.

1.3. Distinguishing RI from Other Performance Metrics

Unlike net income, which only shows the absolute amount of profit, residual income factors in the cost of capital, providing a more nuanced view of profitability. Entrepreneur.com highlights that this distinction is crucial for making strategic decisions about where to allocate resources and which projects or partnerships to pursue.

2. The Residual Income Formula: A Step-by-Step Guide

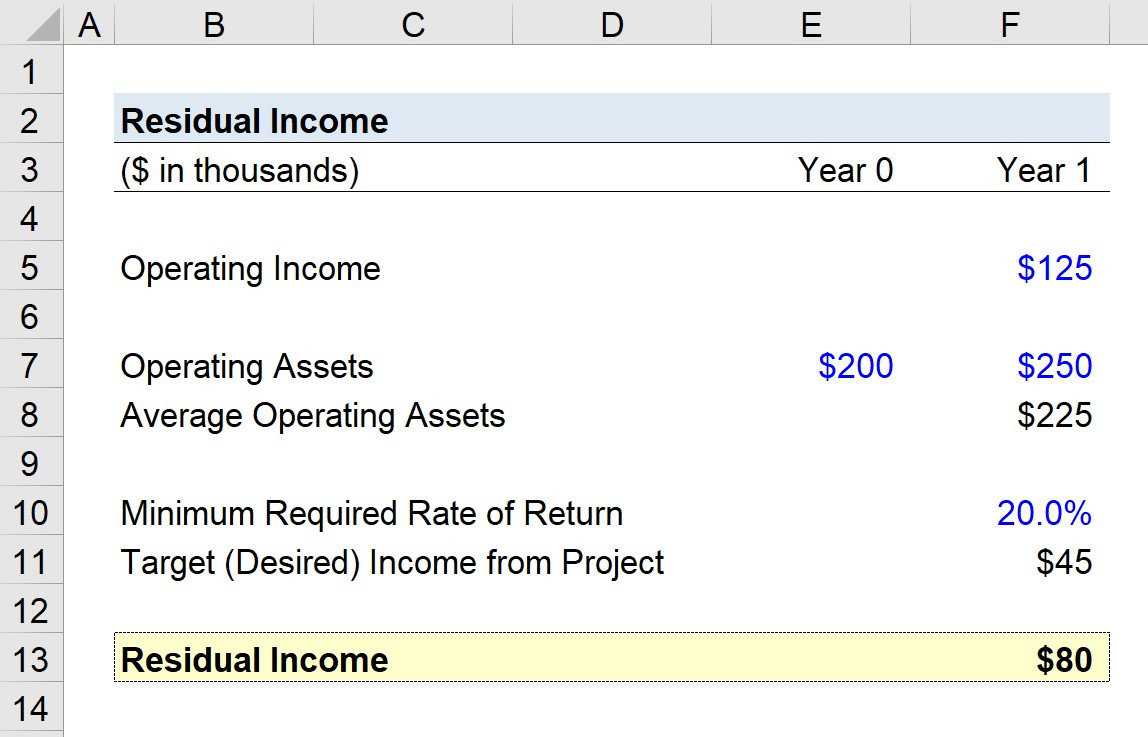

How can you calculate residual income to assess potential partnership opportunities effectively? The residual income formula is straightforward: Residual Income = Operating Income – (Minimum Required Rate of Return × Average Operating Assets).

Calculating residual income involves a few key steps:

- Determine the Operating Income: Find out the income generated from the partnership or project.

- Calculate the Minimum Required Rate of Return: This is the minimum return investors expect based on the risk involved.

- Compute the Average Operating Assets: Determine the average value of the assets used in the partnership.

- Apply the Formula: Subtract the product of the minimum required rate of return and average operating assets from the operating income.

- Evaluate the Result: A positive result indicates the partnership is creating value.

2.1. Breaking Down the Formula Components

To effectively use the residual income formula, it’s essential to understand each of its components:

- Operating Income: This is the profit generated from the project or partnership before interest and taxes. It reflects the core profitability of the venture.

- Minimum Required Rate of Return: Also known as the cost of capital, this is the minimum return investors expect to receive for taking on the risk of investing in the project or partnership. It’s typically calculated using the weighted average cost of capital (WACC).

- Average Operating Assets: This is the average value of the assets used in the project or partnership over a specific period. It includes assets like equipment, inventory, and accounts receivable.

2.2. Step-by-Step Calculation of Residual Income

Here’s a step-by-step guide to calculating residual income:

- Calculate the Average Operating Assets: Add the beginning and ending values of the operating assets and divide by two.

- Determine the Minimum Required Rate of Return: This is usually provided by the company’s finance department or can be calculated using the WACC.

- Multiply the Minimum Required Rate of Return by the Average Operating Assets: This gives you the minimum required return in dollars.

- Subtract the Minimum Required Return from the Operating Income: The result is the residual income.

2.3. Example Calculation: Putting the Formula into Practice

Let’s say a partnership has an operating income of $500,000, average operating assets of $2,000,000, and a minimum required rate of return of 10%. The residual income would be calculated as follows:

Residual Income = $500,000 – (10% × $2,000,000) = $300,000

This positive residual income indicates that the partnership is generating more profit than the minimum required return, making it a worthwhile investment.

3. Interpreting Residual Income: What Does the Number Tell You?

What does a positive or negative residual income indicate about the viability of a partnership? A positive residual income suggests the partnership is exceeding expectations and creating value, while a negative one signals potential issues.

A positive residual income indicates that the investment is generating more profit than the minimum required return, adding value to the company. Conversely, a negative residual income means the investment is not meeting the required return and may be destroying value. According to financial experts, a residual income of zero indicates that the investment is only meeting the minimum required return, neither adding nor subtracting value.

3.1. Positive vs. Negative Residual Income

A positive residual income is a good sign, indicating that the project or partnership is generating returns above the cost of capital. This means the investment is creating value for the company. On the other hand, a negative residual income suggests that the investment is not meeting the required return and may be destroying value. In such cases, it’s essential to reassess the project or partnership to identify areas for improvement or consider alternative options.

3.2. Using Residual Income for Decision-Making

Residual income can be a valuable tool for making decisions about capital allocation and investment opportunities. By calculating the residual income of different projects or partnerships, businesses can prioritize those that generate the highest returns above the cost of capital. This helps ensure that resources are allocated efficiently and that investments are aligned with the company’s overall financial goals.

3.3. Factors Affecting Residual Income

Several factors can influence the residual income of a project or partnership, including:

- Operating Income: Higher operating income will lead to higher residual income.

- Minimum Required Rate of Return: A higher required rate of return will decrease residual income.

- Average Operating Assets: Higher operating assets will decrease residual income.

Understanding these factors and how they interact can help businesses make informed decisions about managing and improving residual income.

4. Advantages of Using Residual Income for Partnership Evaluation

What are the benefits of using residual income compared to other financial metrics when assessing partnerships? Residual income provides a more accurate view of profitability by factoring in the cost of capital, leading to better investment decisions.

Compared to other financial metrics, residual income offers several advantages:

- Considers the Cost of Capital: Unlike net income, residual income factors in the cost of capital, providing a more accurate view of profitability.

- Encourages Efficient Capital Allocation: By focusing on returns above the cost of capital, residual income encourages businesses to allocate capital more efficiently.

- Aligns with Shareholder Value: Maximizing residual income aligns with the goal of maximizing shareholder value, as it ensures that investments are generating returns above the required rate.

4.1. A More Accurate Measure of Profitability

One of the main advantages of using residual income is that it provides a more accurate measure of profitability compared to traditional metrics like net income. By factoring in the cost of capital, residual income shows whether a project or partnership is truly creating value for the company. This is especially important when evaluating investments with different risk profiles, as it allows for a more apples-to-apples comparison.

4.2. Encouraging Efficient Capital Allocation

Residual income encourages businesses to allocate capital more efficiently by focusing on investments that generate returns above the cost of capital. This helps ensure that resources are directed towards the most profitable opportunities, leading to higher overall returns for the company. By prioritizing projects with positive residual income, businesses can make better use of their capital and improve their financial performance.

4.3. Aligning with Shareholder Value

Maximizing residual income aligns with the goal of maximizing shareholder value, as it ensures that investments are generating returns above the required rate. This is because residual income reflects the true economic profit of a project or partnership, taking into account the cost of capital. By focusing on increasing residual income, businesses can create value for their shareholders and improve their long-term financial performance.

5. Disadvantages and Limitations of Residual Income

What are the potential drawbacks and limitations of using residual income in partnership assessments? Residual income may be influenced by accounting practices and can be difficult to compare across different-sized projects.

Despite its advantages, residual income also has some limitations:

- Accounting Practices: Residual income can be influenced by accounting practices, which may distort the true profitability of a project or partnership.

- Size Differences: Comparing residual income across different-sized projects can be challenging, as larger projects may naturally generate higher residual income even if they are not more profitable on a percentage basis.

- Short-Term Focus: Residual income is typically calculated for a specific period, which may not capture the long-term value of a project or partnership.

5.1. Influence of Accounting Practices

One of the main limitations of residual income is that it can be influenced by accounting practices. For example, the choice of depreciation method or inventory valuation can affect the reported operating income and, consequently, the residual income. This means that it’s essential to carefully review the accounting policies used to calculate residual income and make adjustments if necessary to ensure comparability.

5.2. Difficulty Comparing Across Different-Sized Projects

Comparing residual income across different-sized projects can be challenging, as larger projects may naturally generate higher residual income even if they are not more profitable on a percentage basis. To address this issue, it’s often helpful to calculate the residual income as a percentage of the average operating assets, which provides a more comparable measure of profitability.

5.3. Short-Term Focus

Residual income is typically calculated for a specific period, such as a year, which may not capture the long-term value of a project or partnership. Some investments may have low or negative residual income in the early years but generate significant returns over the long term. In such cases, it’s essential to consider the long-term outlook and use other valuation methods, such as discounted cash flow analysis, to assess the overall profitability of the investment.

6. Residual Income vs. Economic Value Added (EVA)

How does residual income compare to Economic Value Added (EVA), and when should each be used? EVA is a specific type of residual income calculation that uses a company’s actual cost of capital to determine value creation.

Residual income and Economic Value Added (EVA) are closely related concepts, but there are some key differences. EVA is a specific type of residual income calculation that uses a company’s actual cost of capital to determine value creation. While residual income can be calculated using any required rate of return, EVA always uses the company’s cost of capital. According to financial analysts, EVA is a more comprehensive measure of profitability than traditional residual income, as it takes into account the true cost of capital.

6.1. Key Differences Between RI and EVA

The main difference between residual income and EVA is that EVA uses the company’s actual cost of capital as the required rate of return. This means that EVA reflects the true economic profit of a project or partnership, taking into account the cost of all capital employed. Residual income, on the other hand, can be calculated using any required rate of return, which may not accurately reflect the company’s cost of capital.

6.2. When to Use RI vs. EVA

Whether to use residual income or EVA depends on the specific circumstances and the goals of the analysis. If the goal is to assess the profitability of a project or partnership relative to a specific benchmark, residual income may be more appropriate. For example, if a company wants to evaluate whether a project is generating returns above a certain hurdle rate, residual income can be used to determine whether the project is meeting that target.

However, if the goal is to assess the true economic profit of a project or partnership, EVA is generally preferred. This is because EVA takes into account the company’s actual cost of capital, providing a more accurate measure of value creation. EVA is also useful for comparing the profitability of different projects or partnerships, as it ensures that all investments are evaluated using the same cost of capital.

6.3. Benefits of Using EVA

EVA offers several benefits over traditional residual income:

- More Accurate Measure of Profitability: EVA takes into account the company’s actual cost of capital, providing a more accurate measure of value creation.

- Improved Decision-Making: By focusing on EVA, businesses can make better decisions about capital allocation and investment opportunities.

- Better Alignment with Shareholder Value: Maximizing EVA aligns with the goal of maximizing shareholder value, as it ensures that investments are generating returns above the cost of capital.

7. Real-World Examples of Residual Income in Partnership Decisions

Can you provide examples of how residual income has been used in real-world partnership scenarios? Companies use residual income to assess partnership profitability, allocate resources efficiently, and ensure long-term value creation.

Several companies have successfully used residual income to make informed decisions about partnerships:

- Partnership Profitability: A company uses residual income to assess whether a potential partnership will generate sufficient returns above the cost of capital.

- Resource Allocation: Businesses allocate resources to partnerships with the highest residual income, maximizing overall profitability.

- Long-Term Value: Companies evaluate the long-term residual income potential of partnerships to ensure sustained value creation.

7.1. Company A: Assessing Partnership Profitability

Company A, a technology firm, was considering a partnership with a smaller company to develop a new software product. To assess the potential profitability of the partnership, Company A calculated the residual income of the project. The analysis showed that the project was expected to generate a positive residual income, indicating that it would be a worthwhile investment. As a result, Company A decided to proceed with the partnership, which ultimately led to the successful launch of the new software product and increased revenue for both companies.

7.2. Company B: Resource Allocation

Company B, a manufacturing company, had several potential partnership opportunities on the table. To decide which partnerships to pursue, Company B calculated the residual income of each opportunity. The analysis showed that some partnerships were expected to generate much higher residual income than others. As a result, Company B allocated its resources to the partnerships with the highest residual income, which led to improved overall profitability and increased shareholder value.

7.3. Company C: Ensuring Long-Term Value

Company C, a financial services firm, was evaluating a long-term partnership with another company to offer new financial products. To ensure that the partnership would create sustained value over the long term, Company C calculated the projected residual income of the partnership over a 10-year period. The analysis showed that the partnership was expected to generate positive residual income throughout the entire period, indicating that it would be a valuable investment for the company. As a result, Company C decided to proceed with the partnership, which has proven to be a successful and profitable venture.

8. Strategies to Improve Residual Income in Partnerships

What strategies can businesses implement to improve residual income in their partnerships? Focus on increasing operating income, reducing the cost of capital, and optimizing asset utilization to enhance partnership profitability.

To improve residual income in partnerships, businesses can focus on the following strategies:

- Increase Operating Income: Implement strategies to increase revenue and reduce costs, boosting overall profitability.

- Reduce the Cost of Capital: Optimize the capital structure to lower the cost of capital, making investments more attractive.

- Optimize Asset Utilization: Use assets more efficiently to generate higher returns, improving the overall residual income.

8.1. Increasing Operating Income

One of the most effective ways to improve residual income in partnerships is to increase operating income. This can be achieved through various strategies, such as:

- Increasing Revenue: Implement marketing and sales initiatives to attract more customers and increase revenue.

- Reducing Costs: Streamline operations, negotiate better deals with suppliers, and reduce waste to lower costs.

- Improving Efficiency: Implement process improvements and automation to increase productivity and efficiency.

- Developing New Products or Services: Invest in research and development to create new products or services that can generate additional revenue.

8.2. Reducing the Cost of Capital

Another key strategy for improving residual income is to reduce the cost of capital. This can be achieved by:

- Optimizing the Capital Structure: Adjust the mix of debt and equity to lower the overall cost of capital.

- Improving the Credit Rating: Take steps to improve the company’s credit rating, which can lower the cost of debt.

- Negotiating Better Loan Terms: Shop around for better loan terms and interest rates.

- Issuing Equity: If the company’s stock is trading at a high price, consider issuing equity to raise capital at a lower cost.

8.3. Optimizing Asset Utilization

Optimizing asset utilization is another important strategy for improving residual income. This can be achieved by:

- Improving Asset Turnover: Increase the speed at which assets are converted into revenue.

- Reducing Inventory: Implement inventory management techniques to reduce the amount of capital tied up in inventory.

- Improving Accounts Receivable Collection: Expedite the collection of accounts receivable to reduce the amount of capital tied up in receivables.

- Selling Underutilized Assets: Identify and sell assets that are not being used efficiently.

9. Using Income-Partners.net to Enhance Partnership Residual Income

How can income-partners.net assist in maximizing residual income through strategic partnerships? Income-partners.net offers resources and connections to identify, evaluate, and optimize partnerships for enhanced financial performance.

Income-partners.net can help businesses maximize residual income through strategic partnerships by:

- Identifying Opportunities: The platform helps businesses identify potential partnership opportunities aligned with their goals.

- Evaluating Potential: income-partners.net provides resources to evaluate the financial viability and residual income potential of partnerships.

- Optimizing Performance: The platform offers tools and insights to optimize partnership performance and enhance residual income.

9.1. Identifying Partnership Opportunities

Income-partners.net can help businesses identify potential partnership opportunities that align with their goals and objectives. The platform offers a comprehensive database of potential partners, as well as tools for searching and filtering based on industry, location, and other criteria. By using income-partners.net, businesses can quickly and easily identify potential partners that can help them achieve their strategic goals and improve their financial performance.

9.2. Evaluating Partnership Potential

Income-partners.net also provides resources to help businesses evaluate the financial viability and residual income potential of potential partnerships. The platform offers tools for calculating residual income, as well as access to industry data and research reports that can help businesses assess the potential returns of different partnership opportunities. By using income-partners.net, businesses can make informed decisions about which partnerships to pursue, ensuring that they are allocating their resources to the most profitable opportunities.

9.3. Optimizing Partnership Performance

Once a partnership is established, income-partners.net can help businesses optimize its performance and enhance residual income. The platform offers tools for tracking key performance indicators (KPIs), as well as access to expert advice and best practices for managing partnerships. By using income-partners.net, businesses can identify areas where the partnership can be improved, and implement strategies to increase revenue, reduce costs, and optimize asset utilization, ultimately leading to higher residual income.

10. FAQs About Calculating Residual Income

Have more questions about calculating residual income? Here are some frequently asked questions to help clarify the process and benefits.

Here are some frequently asked questions about calculating residual income:

- What is the formula for calculating residual income?

- The formula is: Residual Income = Operating Income – (Minimum Required Rate of Return × Average Operating Assets).

- What does a positive residual income indicate?

- It indicates that the investment is generating more profit than the minimum required return.

- How does residual income differ from net income?

- Residual income factors in the cost of capital, providing a more accurate view of profitability.

- What are the limitations of using residual income?

- It can be influenced by accounting practices and may be difficult to compare across different-sized projects.

- How can I improve residual income in my business?

- Focus on increasing operating income, reducing the cost of capital, and optimizing asset utilization.

- What is Economic Value Added (EVA)?

- EVA is a specific type of residual income calculation that uses a company’s actual cost of capital.

- When should I use residual income vs. EVA?

- Use residual income for general assessments and EVA for a more comprehensive economic analysis.

- How can income-partners.net help with residual income?

- It offers resources and connections to identify, evaluate, and optimize partnerships.

- Can residual income be negative?

- Yes, a negative residual income indicates that the investment is not meeting the required return.

- Why is residual income important for partnerships?

- It helps assess whether a partnership is truly creating value above the cost of capital.

10.1. What is the Formula for Calculating Residual Income?

The formula for calculating residual income is:

Residual Income = Operating Income – (Minimum Required Rate of Return × Average Operating Assets)

This formula provides a clear and concise way to determine the profitability of an investment or project relative to its cost of capital.

10.2. What Does a Positive Residual Income Indicate?

A positive residual income indicates that the investment or project is generating more profit than the minimum required return. This means that the investment is creating value for the company and is a worthwhile pursuit.

10.3. How Does Residual Income Differ from Net Income?

Residual income differs from net income in that it factors in the cost of capital. Net income only shows the absolute amount of profit, while residual income shows whether the profit is sufficient to justify the investment of capital.

10.4. What Are the Limitations of Using Residual Income?

Some of the limitations of using residual income include:

- It can be influenced by accounting practices.

- It may be difficult to compare across different-sized projects.

- It has a short-term focus.

10.5. How Can I Improve Residual Income in My Business?

To improve residual income in your business, you can focus on:

- Increasing operating income.

- Reducing the cost of capital.

- Optimizing asset utilization.

10.6. What is Economic Value Added (EVA)?

Economic Value Added (EVA) is a specific type of residual income calculation that uses a company’s actual cost of capital to determine value creation.

10.7. When Should I Use Residual Income vs. EVA?

You should use residual income for general assessments and EVA for a more comprehensive economic analysis.

10.8. How Can income-partners.net Help with Residual Income?

Income-partners.net offers resources and connections to identify, evaluate, and optimize partnerships, which can help improve residual income.

10.9. Can Residual Income Be Negative?

Yes, residual income can be negative. A negative residual income indicates that the investment is not meeting the required return and may be destroying value.

10.10. Why Is Residual Income Important for Partnerships?

Residual income is important for partnerships because it helps assess whether a partnership is truly creating value above the cost of capital.

By understanding and applying the principles of residual income, businesses can make informed decisions about partnerships and investments, leading to increased profitability and long-term success. Are you ready to take your partnership strategies to the next level? Visit income-partners.net today to discover a wealth of resources, tools, and connections that can help you maximize your residual income and achieve your financial goals.

Residual Income Calculator

Residual Income Calculator

The calculator image represents a modern tool, and its alt text specifies the tool’s purpose, its placement here helps clarify how such instruments facilitate real-world applications of the Residual Income formula and concepts

Ready to transform your partnership approach and unlock unprecedented revenue streams? Explore income-partners.net today and connect with a network of like-minded professionals, access invaluable resources, and discover untapped partnership opportunities. Maximize your residual income potential by understanding strategic alliances and achieving financial success with income-partners.net. Don’t wait—start your journey towards partnership excellence now. Visit our website or contact us at Address: 1 University Station, Austin, TX 78712, United States. Phone: +1 (512) 471-3434.